- Mexico: Retail sales stall in September, wholesale receipts increase

- Peru: Private investment takes off amid absence of electoral turbulence

MEXICO: RETAIL SALES STALL IN SEPTEMBER, WHOLESALE RECEIPTS INCREASE

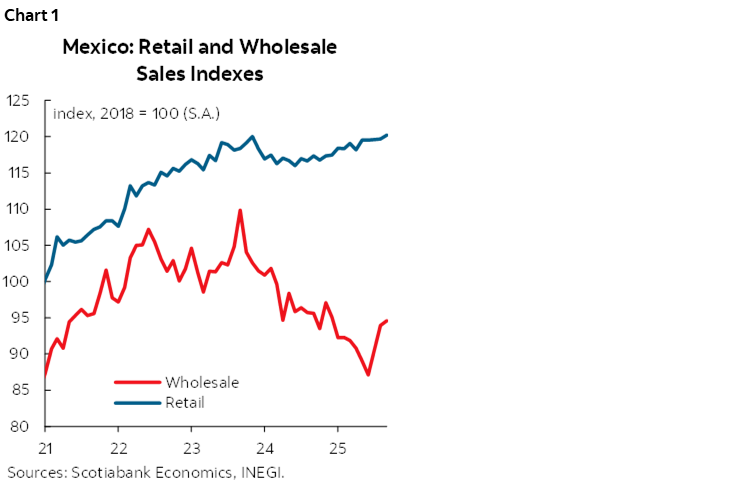

In September, according to the Monthly Survey on Commercial Enterprises (EMEC), retail sales showed no monthly growth in seasonally adjusted figures (chart 1), with a variation of 0.0%. Regarding employed personnel and average wages, they recorded changes of 0.1% and -0.2%, respectively. As for wholesale trade, total revenues increased by 2.5%, while employed personnel and average wages were revised downward, with figures of -0.2% and -1.2%, respectively. On an annual basis and in original figures, retail trade posted widespread increases: revenues grew by 3.3%, employed personnel by 1.0%, and average wages by 4.3%. Wholesale trade showed mixed signals, with a 2.4% increase in revenues, 1.1% in employed personnel, and -0.6% in average wages.

—Rodolfo Mitchell, Miguel Saldaña & Martha Cordova

PERU: PRIVATE INVESTMENT TAKES OFF AMID ABSENCE OF ELECTORAL TURBULENCE

- Private investment posted its highest quarterly growth rate since 2013, excluding the post-pandemic rebound.

- Improvements in employment and income, along with lower inflation, are driving the expansion of private consumption.

- The dynamism of mining and infrastructure investment is expected to sustain growth in 4Q25 despite the electoral cycle.

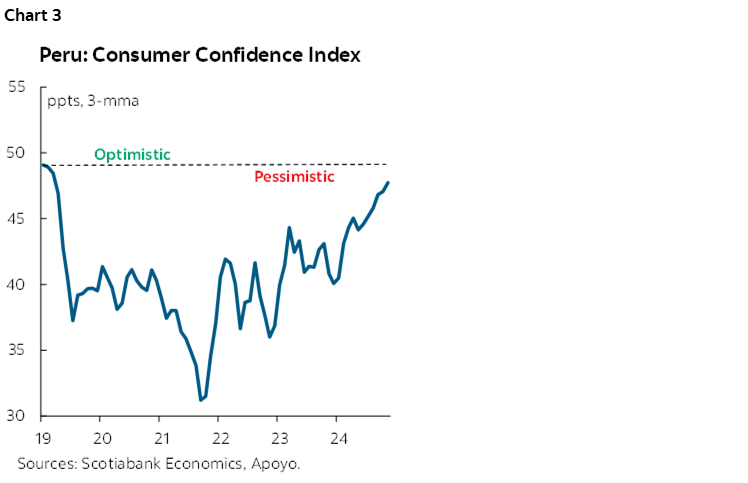

Domestic demand expanded by 5.9% in the third quarter of 2025 (3Q25), marking its seventh consecutive quarter of growth, according to data from the Central Reserve Bank (BCRP). This performance outpaced GDP growth of 3.4%, which was constrained by the modest increase in export volumes (table 1).

The sustained momentum in domestic demand was primarily driven by private expenditure. Private investment accelerated despite the proximity of the electoral period, supported by the advancement of mining projects and transportation infrastructure. Similarly, private consumption remained robust, underpinned by higher employment and income levels. Meanwhile, public spending registered a stronger pace of growth during 3Q25, reflecting increased public investment by regional and local governments.

For the fourth quarter (4Q25), we project that domestic demand will continue to expand, albeit at a slower pace, considering the base effect—it grew 6.4% in 4Q24 versus 3.0% in 3Q24. The most dynamic component is expected to remain private investment, as mining and infrastructure projects are less sensitive to the electoral cycle. In addition, private consumption will benefit from the start of payments associated with the eighth withdrawal of pension funds. Finally, we anticipate a moderation in public investment, particularly at the National Government level, given the Ministry of Economy’s efforts to meet the fiscal deficit target.

Performance of Domestic Demand During 3Q25

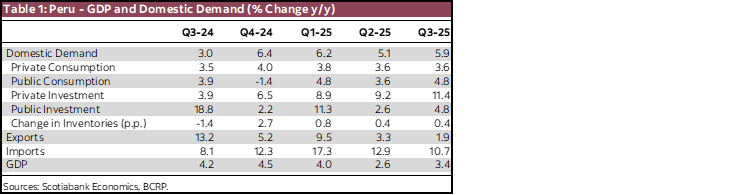

Private investment (+11.4%) recorded its highest quarterly growth rate since 2013, excluding the post-pandemic rebound (chart 2). This positive trend was driven by higher mining investment (+23.9%), as elevated metal prices—such as copper and gold—have allowed mining companies to allocate larger investment budgets, while reduced social conflict has facilitated progress on projects like Tía María and San Gabriel. Likewise, non-mining non-residential investment stood out, supported by the execution of infrastructure projects such as Line 2 of the Lima Metro and initiatives across various sectors, including electricity, manufacturing, and telecommunications. Meanwhile, residential investment (+2.4%) grew for the third consecutive quarter, showing a gradual improvement in line with the recovery of household income—which has enabled greater spending on self-construction—along with the dynamism of formal real estate investment, boosted by the decline in mortgage interest rates.

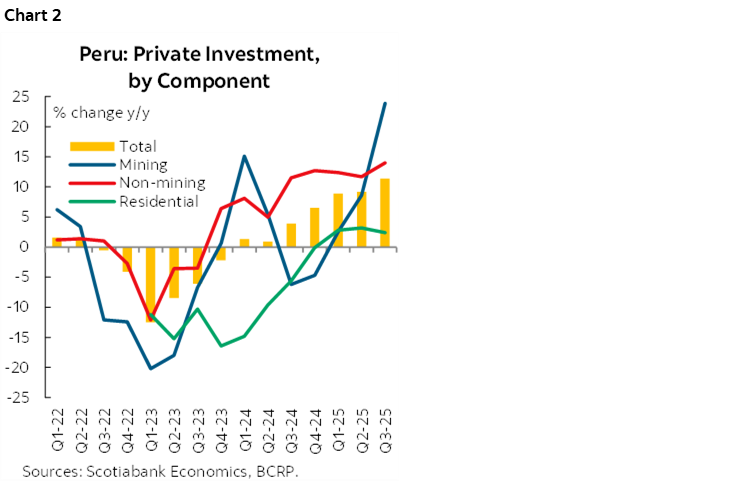

Private consumption (+3.6%) continued the momentum observed since mid-2024, marking five consecutive quarters of growth above 3.5%. This positive performance was driven by higher employment—particularly in agro-export and services sectors—and increased income, especially among formal workers. Additionally, the downtrend in inflation supported consumers’ purchasing power. Consumer credit also recovered in a context of declining delinquency rates and lower interest rates. The rebound in consumer confidence to pre-pandemic levels (chart 3), together with the start of payments associated with the eighth withdrawal of pension funds (AFPs), leads us to anticipate that the positive trend in private consumption will persist during 4Q25.

Public investment (+4-8%) accelerated its pace of expansion in 3Q25, supported by greater project execution by subnational governments. Local government investment (+22.2%) was driven by transportation and urban improvement works, particularly in the departments of Lima, Cajamarca, and Huánuco. Meanwhile, regional government investment (+7.9%) benefited from increased resources allocated to projects in health, education, sanitation, culture, and sports, especially in Ayacucho, Cajamarca, and Pasco. In contrast, National Government investment (-14.0%) was affected by reduced transfers of resources to projects executed by the National Infrastructure Authority (ANIN).

Public consumption (+4.8%) increased, led by higher spending on goods and services (+7.5%), notably Administrative Service Contracts (CAS), service outsourcing, and professional and technical services. Additionally, payments for wages rose (+3.5%), highlighting higher compensation granted to workers in the interior, defense, education, health, and justice sectors.

—Pablo Nano

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.