- Chile: Favourable composition (but not the best) for Kast in both Chambers

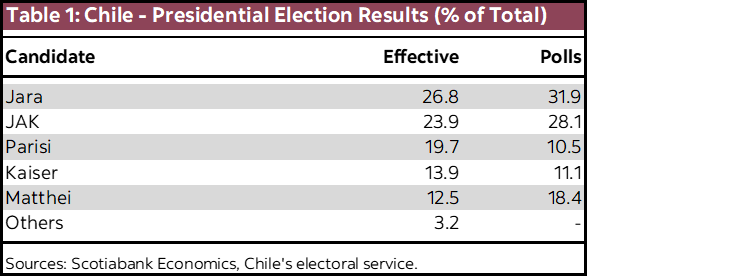

On Sunday, November 16th, with 100% of ballots counted, left-wing candidate Jeannette Jara (Unidad por Chile coalition) and right-wing conservative José Antonio Kast (JAK—Cambio por Chile coalition) advanced to the runoff scheduled for December 14th, as widely expected. Ms. Jara secured first place with 26.8% of the vote, while JAK came in second with 23.9% (table 1). The main surprise was Jara’s weaker-than-expected performance compared to polls and Kast’s stronger showing, narrowing the gap to less than 3 pp—an outcome that gives Kast a significant advantage heading into the second round. Turnout reached 85.3% (around 13.5 million voters), slightly above the 2024 regional elections (84.9%). A lower turnout is anticipated for the runoff. In our view, these results carry positive implications for markets.

JAK is now the clear favourite for the December 14th runoff. In Sunday’s election, right-wing candidates collectively mobilized 50.3% of voters. Both Mr. Kaiser and Ms. Matthei have endorsed Kast for the second round, reinforcing his frontrunner status. While Ms. Jara also qualified for the runoff, her support base appears weaker than expected. Meanwhile, Franco Parisi captured 19.7% of the vote (up from 12.8% in 2021), making his electorate the key prize to secure.

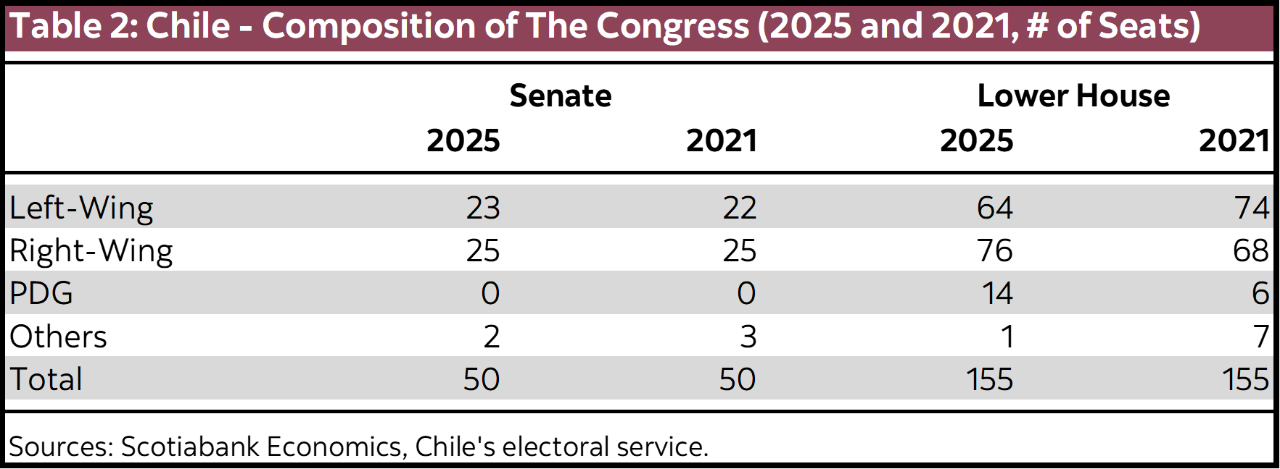

Right-wing coalitions expanded their representation in the Congress, though they fell short of an outright majority (table 2). In the lower house, right-wing parties hold 49% of seats, while in the Senate they control 50%, granting them veto power. Achieving a Senate majority seems easier for the right than for the left, given the presence of a senator formerly aligned with the right-wing bloc (M. Calisto). In the Chamber of Deputies, the Partido de la Gente (PDG—Parisi’s party) becomes pivotal for building majorities, holding 14 of 155 seats (9%). PDG is a heterogeneous group: its new legislators come from diverse political backgrounds and lack prior parliamentary experience, except for one female member. Two previously belonged to UDI, while two others were affiliated with the center-left (PPD). Their positions are broadly populist, and they currently act as opposition to the government. Notably, PDG supported Kast in the second round of the 2021 presidential election.

The combination of a likely Kast victory and a balanced congressional composition—requiring negotiations and coalition-building, particularly with swing actors like PDG—is viewed favourably by markets. This explains recent peso appreciation and equity gains, which we expect to be followed by a decline in short-term interest rates.

—Jorge Selaive, Aníbal Alarcón & Waldo Riveras

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.