- Mexico: Sixth straight fixed investment decline; private consumption contraction deepens

Markets are trading with a relatively negative tone as recent optimism is checked somewhat by a lack of positive developments on the international trade front while we look ahead to the Fed’s decision tomorrow afternoon. Ford halting guidance, yesterday, due to tariffs is also a headwind for sentiment, while European markets took a hit from Germany’s Merz failing a confirmation vote in Parliament before being confirmed in a second vote just a moment ago. It was an otherwise quiet overnight session where U.K. markets reopened from holidays. The release of final PMIs in Europe with small revisions higher for the Eurozone and the UK had limited impact on sentiment. U.S. equities are about 0.5% weaker in early trading, in line with losses in the Eurozone while U.K. stocks trade flat. Japanese equities gained ~1% despite reports that trade negotiations with the U.S. are not going all that well. Bear steepening in EGBs and antipodean rates stands in contrast to twist steepening USTs and gilts. Oil is bouncing back 3.5% today as the market starts to call the bottom for prices while iron ore and copper are roughly 1% firmer. Currencies are mixed against the USD, as the JPY leads on a ~1% gain while the MXN and BRL lag on 0.2% and 0.5% declines, respectively.

U.S. international trade data for March published this morning showed an (expected) surge in imports as domestic buyers rushed ahead of tariffs. Total U.S. imports jumped 32.2% y/y in March (+71% y/y from the Eurozone) to complete a 25.5% spike for the quarter. U.S. imports from Mexico surged 15.4% y/y following a relatively muted gain in February of 3.5% where leap-year base effects likely softened the headline figure. Recall that on March 4th the White House imposed 25% tariffs on Canada and Mexico before narrowing their imposition to non-USMCA compliant goods from March 7th. In the lead-up to a possible end to USMCA exemptions or another tariffs wave, firms ramped up imports from Mexico and Canada, although U.S. imports from the latter ‘only’ rose 4.2% (slower than February’s 4.6% rise). As for China, tariffs imposed in the year to March seemed to have already weighed on U.S. imports from the country, with a decline of 1.9% y/y in the month after a 0.8% drop in February that followed a 16.3% jump in January.

The Latam day ahead is quiet outside of the release of the minutes to last week’s BanRep rate decision. As our team in Colombia anticipated, officials in the country voted for a 25bps rate cut with the backing of macroeconomic fundamentals, namely inflation resuming its downtrend in headline terms while core inflation continues its deceleration. In the minutes, we’ll be looking for whether dovish board members floated the possibility of a larger rate cut (as they had voted for a 50bps move in the March decision) and gauge the chance that BanRep may cut again at the late-June announcement—for which markets are pricing in a 25bps move, followed by about an 80% chance of a cut in late-July. The current terminal rate implied by markets is in the 8.00-8.25% range.

—Juan Manuel Herrera

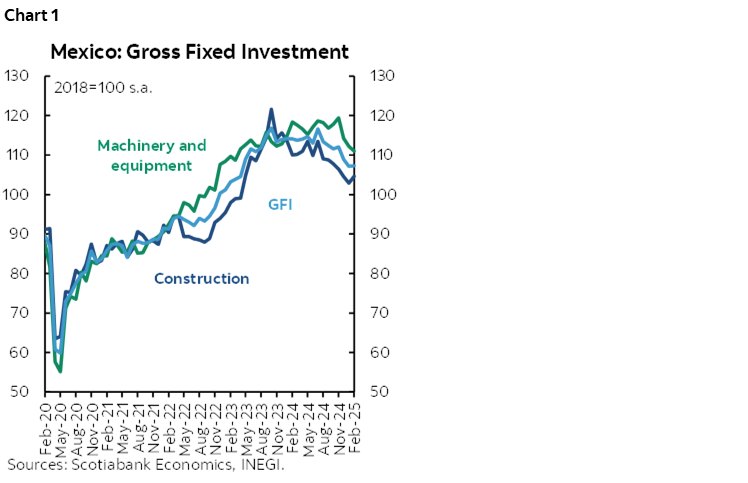

MEXICO: SIXTH STRAIGHT FIXED INVESTMENT DECLINE

In February, gross fixed investment marked a sixth consecutive month of declines, falling by 7.8% y/y (-7.0% previously). Within the components, machinery and equipment slowed to -10.4% y/y from -3.2%; specifically, the domestic subcomponent decreased by -3.2% (-3.4% previously), and the imported component dropped by -15.1% (-3.0% previously). Construction remained weak, falling -5.2% (-10.4% previously), marking seven consecutive months of contraction. Within construction, non-residential investment declined by -18.0% (-16.8% previously), while residential investment rebounded by +14.1% (-1.8% previously). On a seasonally adjusted monthly comparison, gross fixed investment showed a slight increase of +0.1% m/m (-1.6% previously), with construction rising 1.7% m/m, while machinery and equipment fell by -1.1%. Looking ahead, we believe that both internal and external uncertainty and volatility will lead to greater risk aversion, potentially resulting in a year of continued declines in investment.

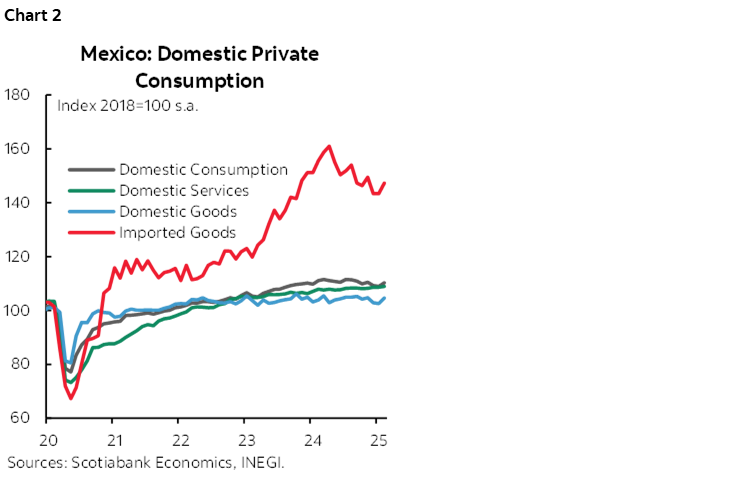

PRIVATE CONSUMPTION CONTRACTION DEEPENS

Private consumption deepened its annual decline in February, falling from -1.3% to -1.9%, marking three consecutive months of contraction. Breaking it down, domestic goods fell by -0.5% (-1.0% previously), although there was a rebound in durable goods (10.0%) and a slight increase in semi-durable goods (+0.5%), which offset the decline in non-durable goods (-2.2%). Meanwhile, services moderated to 0.3% (1.5% previously). On the other hand, imported goods dropped by -9.2%, extending their downward trend to four consecutive months. On a seasonally adjusted monthly basis, private consumption rebounded by 1.2% (from -0.3% previously), driven by a recovery across all three components: imported goods rose by 2.7% (0.0% previously), domestic goods increased by 2.1% (-0.3% previously), and services edged up by 0.3% (0.1% previously). We believe the rebounds in February and March may reflect anticipatory behavior by economic agents considering a potential economic slowdown and weaker job creation, which could weigh on consumption going forward.

—Rodolfo Mitchell, Brian Pérez & Miguel Saldaña

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.