- Mexico: Dovish Banxico minutes back expectations for a repeat 50bps

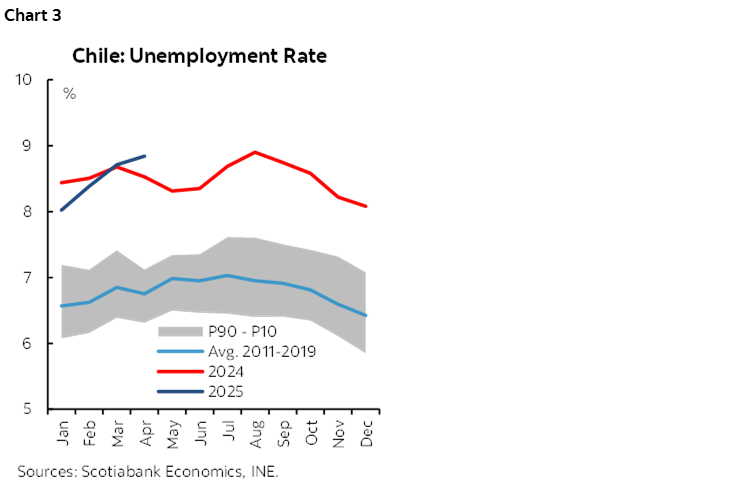

- Chile: Unemployment rate rises to 8.8% in the quarter to April

MEXICO: DOVISH BANXICO MINUTES BACK EXPECTATIONS FOR A REPEAT 50BPS

- The arguments of the Governing Board members focused on the economic slowdown, the current level of inflation, and the uncertainty generated by tariffs.

- The Governing Board members expect greater weakness in economic activity for 2025. They noted that private consumption has moderated, largely due to a slower pace in both domestic and imported goods, and that investment remains weak.

- They mentioned that the disinflationary process continues and that a decline in economic activity was observed during the first quarter of 2025. The Governing Board highlights that both headline and core inflation remain below the levels seen during the pandemic and close to their historical average (2003–2019).

- We believe that in the next monetary policy meeting, Banxico will opt to repeat a 50 basis point cut. We anticipate that the benchmark interest rate will end the year at 8.00%, although the likelihood of a downward revision is increasing.

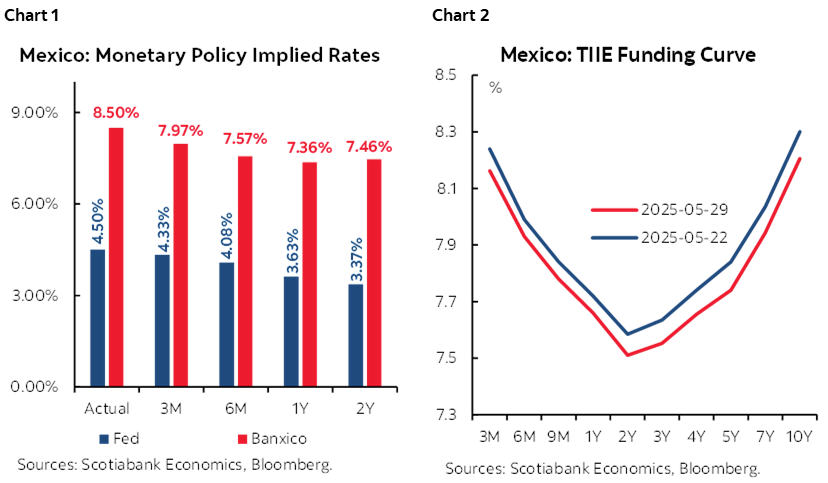

The Bank of Mexico published the minutes of the May 15th meeting this morning, providing details about the discussion surrounding inflation and monetary policy within the Governing Board, with a unanimous decision to cut 50 basis points, bringing the benchmark interest rate to 8.50%. Overall, we highlight the arguments which focused on the ongoing disinflation process, noting that the recent uptick in inflation is largely due to more volatile components. The Governing Board members suggest that the inflationary period has ended and that they can continue cutting the benchmark rate by a similar magnitude, as lower inflation is expected amid weaker growth in the Mexican economy.

Regarding the Mexican economy, comments highlighted economic weakness, with GDP growth in the first quarter of 2025 at just 0.2%, consistent with the slower pace observed since late 2023. This was due to declines in industry, a slowdown in services, while primary activities led the advance. Weakness is expected to persist throughout the year. The members referenced that private consumption has remained weak for both domestic and imported goods. Additionally, Gross Fixed Investment has declined in both public and private components, along with deteriorating business confidence. They also noted a reduction in growth expectations according to the Quarterly Inflation Report and acknowledged that the probability of a recession has increased, affected by uncertainty related to the Trump administration and potential tariffs. Regarding employment, it was noted that job creation shows signs of stagnation, with a decline in the labour force participation rate and a drop in employer registrations.

In the external environment, they mentioned that the period between decisions continued to be marked by trade policy announcements between the United States and its partners. They noted that economic activity showed a slower pace, evidenced by the quarterly contraction of U.S. GDP, as well as reduced activity in China. On the other hand, despite some inflation upticks, they stated that the global disinflation process has continued and is approaching central bank targets, although challenges remain in service prices. In line with this, an economic slowdown is expected in the U.S., driven by lower consumption, supported by a significant decline in both consumer and business confidence. They also mentioned that the Federal Reserve kept its rate unchanged amid an uncertain outlook, and the central bank will wait for more data before cutting the benchmark interest rate. However, the market anticipates two cuts during the year. They acknowledged that markets have shown volatility due to trade tensions, with a broad depreciation of the dollar and declines in major stock indices.

On inflation, the Governing Board emphasized that both headline and core inflation are at lower levels than during the pandemic and close to their historical average (2003–2019). Some members mentioned that inflationary pressures have eased, so price formation is expected to be more stable. They noted that inflation has been partly affected by the core component due to a rebound in goods, mainly food, driven by international input pressures, while services have remained below 5% for seven consecutive months and could continue to decline in the coming periods due to greater economic weakness. On the other hand, non-core inflation has helped contain headline inflation based on data through April. It was mentioned that inflation expectations have remained stable, without significant short- or medium-term advances anticipated. Regarding risks, most considered that the balance remains tilted to the upside, although it has improved, and downside risks have gained relevance, particularly the weakening economy, which could lead to lower pressures. Most notably, the majority noted that changes related to U.S. trade policy pose both upside and downside risks, although some members considered that the impact of greater economic weakness would be more lasting and relevant than the upward effect of currency depreciation. However, one member emphasized that private analysts’ inflation forecasts remain higher than those estimated by the Bank of Mexico in the short and medium term.

In the monetary policy discussion, we noted a clear inclination by most members to repeat a cut of the same magnitude at the June meeting. The arguments for this cut remain based on the current level of inflation, close to the historical average, and downward pressures on prices due to greater economic weakness. However, they acknowledged some risks both to the downside and upside stemming from the imposition of tariffs by the United States and the resulting volatility and uncertainty. On the other hand, one particular member noted that the lack of progress in inflation convergence so far this year and the upward bias in the inflation risk balance would limit the room for further monetary easing. This member also expressed that it is time to remove the forward guidance reference suggesting that future meetings could continue adjusting the monetary stance by a similar magnitude, as this should reflect that the current pace of cuts would only continue if the disinflationary process toward the 3% target resumes. Another member highlighted that the narrowing of the interest rate differential between Mexico and the U.S. is becoming increasingly relevant in relation to the relative monetary stance, which will eventually imply a more gradual approach to monetary policy decisions. In line with this member, we believe that a differential below 350 basis points could generate volatility in the exchange rate and financial markets.

Looking ahead, based on the comments from the Governing Board members, we believe the June meeting will repeat a 50 basis point cut in the benchmark rate, bringing it to 8.00%. However, due to upside inflation risks, we believe this cut will not be unanimous and that the forward guidance will likely be revised to indicate smaller cuts. Given the environment of uncertainty, an upward-skewed risk balance, and a restrictive stance from the Federal Reserve, we maintain our expectation for a terminal interest rate of 8%. However, the likelihood of revising this downward is increasing.

—Rodolfo Mitchell, Brian Pérez & Miguel Saldaña

CHILE: UNEMPLOYMENT RATE RISES TO 8.8% IN THE QUARTER TO APRIL

- The decline in salaried employment raises the alarm about the incipient recovery in the labour market

On Thursday, May 29th, the INE released data showing the unemployment rate rising to 8.8% in the quarter ending in April, exceeding market expectations (8.6%) and showing a counter-seasonal increase (chart 3). In fact, the seasonally adjusted unemployment rate increased from 8.5% to 8.7%, the highest since the quarter ending in January 2024. Regarding employment, 30k jobs were lost, most of them in formal sectors and businesses, ending a streak of five consecutive rolling quarters of formal job creation. The INE reported a decrease in the labour force of 17k people, while the habitually inactive population increased by 64k people, largely explained by permanent studies reasons. The decline in the labour force stands out as the largest in recent history observed for a month of April, excluding the pandemic period.

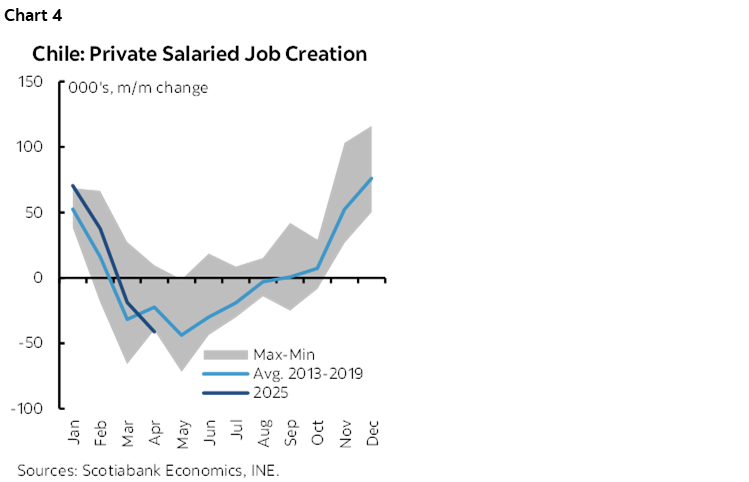

The destruction of nearly 30k jobs was due to the decline in private salaried employment (chart 4), with the most notable decline in sectors such as construction, manufacturing, and some services. After several months of above-expected performance, payrolled employment decreased by more than 41k jobs, its largest drop since 2013, excluding the pandemic period (2020). Beyond the seasonal decline in payrolls in some sectors (agriculture, accommodation and food, among others), the construction sector stands out negatively, having failed to show sustained improvement over the past two years. Likewise, manufacturing showed a decline of 16k private wage jobs this quarter, marking a setback after showing recovery in previous months. Undoubtedly, the figures for the quarter ending in April are not positive and raise alarms regarding the incipient recovery that the labour market had begun to show in previous months.

Our assessment of labour market fragility remains unchanged for now, although the outlook is positive for the coming months, especially starting in the second half of the year. While this figure reveals a fairly widespread deterioration in the labour market, it is preceded by positive figures in previous months, both from this survey and from administrative records. For the remainder of the year, we project that the peak in job demand could be observed in the third quarter and would be driven by the mining and industrial sectors. However, it will remain critical for new investment projects to continue entering sectors such as real estate and public works, where job demand is typically higher and could strengthen the labour market in the coming quarters.

—Aníbal Alarcón

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.