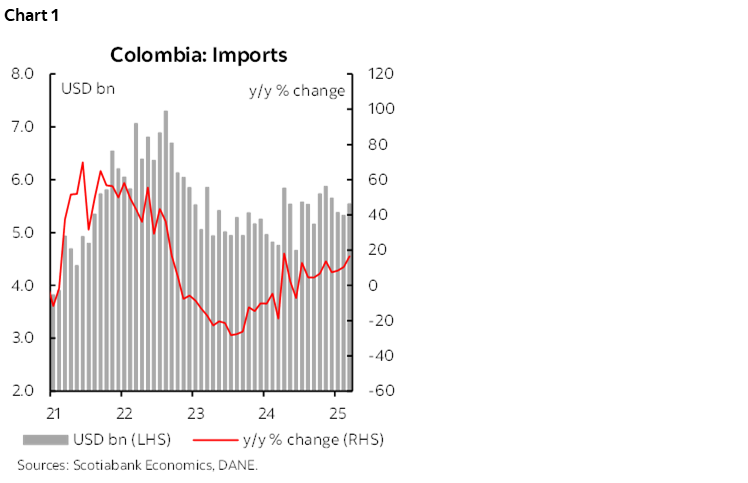

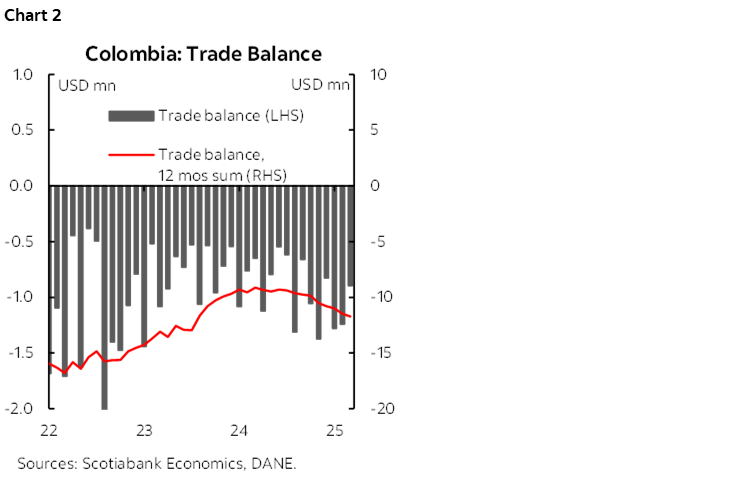

- Colombia: Imports expanded 11% y/y in Q1, while the trade deficit widened 37%

U.S. equities are weaker in early trading, with about a 0.3/4% drop for the S&P 500, with a slight risk-off tone in markets following yesterday’s rollercoaster when equities opened sharply weaker on Moody’s U.S. credit rating downgrade before steadily creeping higher to close roughly unchanged. European indices are solidly bid, rising since their open, while flat Japanese stocks stood in contrast to large gains in Hong Kong’s Hang Seng index thanks to a successful debut for Chinese battery giant CATL. In commodities, oil prices are about 0.5% weaker as volatility continues on the back of back-and-forth developments in Ukraine-Russia and U.S.-Iran tensions, while gold gains about half a percent and copper declines 1%. The USD is mixed against the major currencies, as the MXN and CAD lead with small gains, the EUR and JPY are flat, and the AUD significantly lags with a 0.8% drop on a dovish Reserve Bank of Australia (RBA) decision (see below).

Overarching drivers for global markets are relatively limited today as traders await the release of PMIs from all over the globe on Thursday as well as keeping an eye on the uncertain flood of tariff headlines and U.S. tax bill developments. As expected, Chinese banks lowered their 1- and 5-year prime lending rates by 0.1ppts amid policy easing measures by the nation’s central bank, while several major banks also lowered their deposit rates to safeguard margins. Overnight, Australia’s Reserve Bank (RBA) cut its policy interest rate by 25bps, as expected, bringing it to 3.85%, and highlighting the risks posed by global uncertainty and market volatility. The RBA revised its forecasts for growth and inflation lower, giving the overall decision a more dovish than expected feel to it. Following the decision, markets incorporated ~15bps in additional easing expected by year-end to a total of ~65bps, with about a two-thirds chance that the RBA cuts again by 25bps at its July 8 meeting.

It’s a quiet day ahead in Latin America, with Mexico’s Citi survey of economists the highlight of the session. Recall that Banxico’s rate decision on the 15th showed relatively rosy inflation forecasts as, despite near-term upside surprises, the Board left its year-end projections virtually intact—and, in turn, the expected date of convergence to target in 3Q26. Citi’s survey results should stand in stark contrast to the bank’s outlook and will also likely show that most economists anticipate another 50bps cut in June after last week’s dovish decision.

Elsewhere, BanRep’s Gov Villar is scheduled to speak at a Moody’s event this morning, where he may stick to a cautious stance that supports the market’s view, with only about 10bps priced in in cuts for the June meeting.

—Juan Manuel Herrera

COLOMBIA: IMPORTS EXPANDED 11% Y/Y IN THE Q3, WHILE TRADE DEFICIT WIDENED 37%

On Monday, May 19th, DANE published import data for March 2025. Imports reached US$5.54 billion CIF (chart 1). Imports increased 16.5% compared to the same month in 2024, maintaining the positive trend for the ninth consecutive month, and combining for an 11% y/y rise in 1Q26. The annual growth is explained by a low comparison base given that in March 2024, imports experienced a fall of 18.7%. Compared to the previous month, imports increased 4.1%. Manufactured imports increased 20.9%, contributing 14.8 p.p. (89.8% of the annual growth).

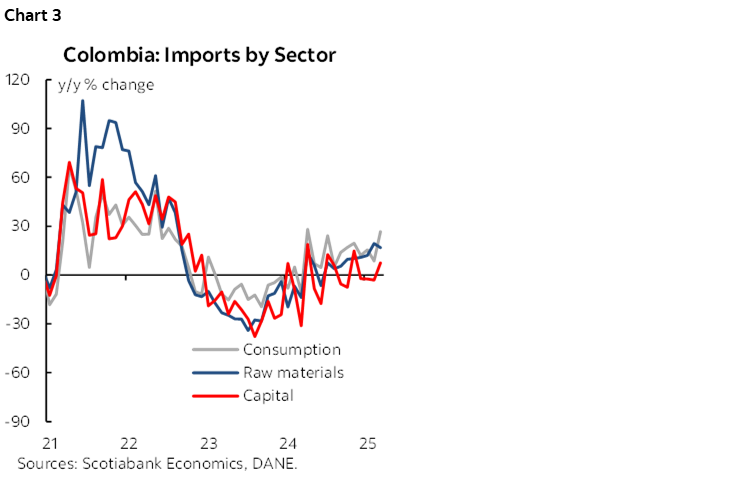

The import increase reflects the recovery in household demand. Imports of consumer goods grew 26.7% in March, the highest growth since April 2024, showing double-digit growth in durable goods, with the vehicle component standing out with 56.6% y/y growth. Imports of consumer goods are associated with better performance in retail sales, since, in the first quarter of 2025, the commerce, transport and hotels sector grew 3.9% compared to the same quarter of 2024, according to GDP figures. For the first quarter of 2025, imports of consumption-related goods increased 16.93%, driven mainly by durable goods with an expansion of 29% y/y.

Imports of raw materials and capital goods also increased in March. Raw material imports (up 16.8% y/y) were driven by the industrial sector (+26.47% y/y), while imports of fuel and agricultural sectors decreased in March, associated with lower gas imports (-34.2% y/y) and lower animal feed imports (-35.5% y/y). Regarding capital goods (+7.53% y/y), there was a notable increase in construction materials imports (+36.1% y/y) and industrial capital goods imports (+22.5%). In the first quarter, raw materials and capital goods imports had a positive balance, growing by 16.1% y/y and 0.68% y/y, respectively.

The trade balance stood at US$897 million, widening the deficit by 37.9% compared to March 2024 (US$650.4 million) (chart 2). During March, exports performed better thanks to a higher volume of oil exports, coffee exports that grew by 137%, and non-traditional exports that maintained a significant expansion. However, the strong export results failed to overcome the positive dynamics in imports. The accumulated trade deficit in the first quarter stood at US$3.41 billion, which represents an increase of 36.9% compared to the first quarter of 2024 (US$2.49 billion).

March highlights:

- Consumer imports maintained positive dynamic. In March, consumer imports grew 26.7% y/y, contributing 6.1 percentage points to total import growth. Imports of non-durable goods grew 14.1% y/y, driven by imports of pharmaceutical products, food, beverages, and textiles. Imports of durable consumer goods increased 46.4% y/y, reflecting a 56.6% y/y increase in vehicle imports.

- Imports of raw materials grew 16.9% y/y. Imports of raw materials increased mainly due to the industrial sector, with growth of 26.5% y/y. Fuel imports decreased -2,5% y/y, primarily due to decreased gas imports. Imports of material for the agricultural sector decreased -4,1% y/y, explained by a lower import of animal feed.

- Imports of capital goods increased 7.4%. Imports of construction materials increased 36.1% y/y. Imports of capital goods for agriculture increased 29.6% y/y, mainly due to tool components and transportation equipment, while in the industrial sector, imports of capital goods increased 22.5%. On the negative side, imports of transportation equipment fell for the fourth consecutive month, decreased in 28.2% y/y.

—Jackeline Piraján & Daniela Silva

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.