- Chile: April GDP of 2.5% y/y in line with our expectations

- Mexico: In Banxico’s Survey of Expectations, the year-end policy rate forecast was revised downward to 7.50%; Remittances continue to decelerate

- Peru: Inflation remains stable in May

CHILE: APRIL GDP OF 2.5% Y/Y IN LINE WITH OUR EXPECTATIONS

- We project that GDP will grow between 3.75–4.25% y/y in Q2-25

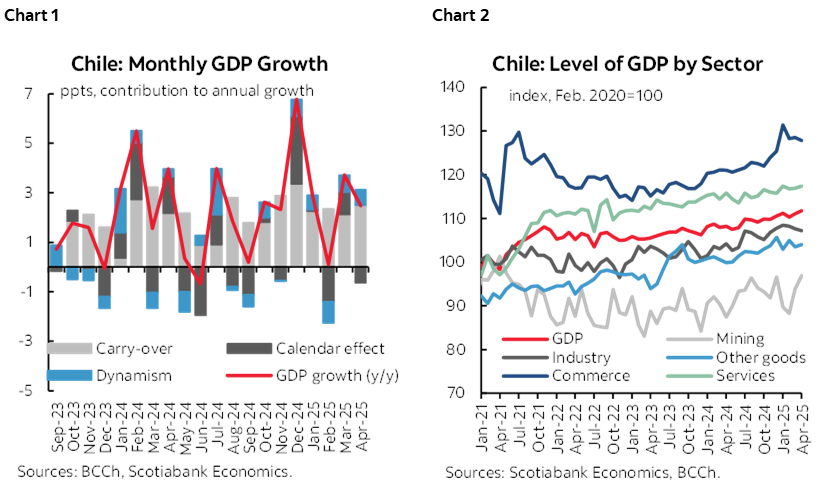

On Monday, June 2nd, the Central Bank (BCCh) released April GDP data, which showed an expansion of 2.5% y/y, above market expectations (2.2% y/y) and closer to our earlier projection at Scotia (see our Latam Daily, May 5th). Despite having one less business day than last year, non-mining GDP grew 0.3% m/m, mainly thanks to the positive contribution of business services. Similarly, the mining sector registered a 3.3% m/m expansion, with aggregate GDP growing 0.6% m/m (seasonally adjusted). With this information in hand, we estimate that the BCCh will once again revise upward its 2025 GDP growth projection in the June Monetary Policy Report (IPoM) to be released on June 18th, bringing it closer to our 2.5% projection for the year.

Economic activity continues to recover, this time driven by services and mining. In seasonally adjusted terms, GDP expanded 3.3% y/y, 0.8 ppts above the year-over-year rate derived from the unadjusted series, due to the negative calendar effect experienced during the month (chart 1). While this latter effect detracted from the year-over-year growth rate, its magnitude was within our estimates and what was expected considering the difference in days and the composition of the calendar. At the sector level, the solid dynamism shown by services since mid-2024 stands out (chart 2), especially business services, linked to the materialization of investment projects. Alongside this, the rebound in mining activity stands out, reaching its highest level of output since May 2021, revealing the solid recovery in copper production after maintenance and one-off effects during previous months.

Due to the more favourable bases of comparison in May and June, Q2-25 GDP growth is projected in a range between 3.75% and 4.25% y/y, supporting our 2.5% growth projection for the whole of 2025. The base effect alone would boost May’s year-over-year growth to between 3% and 4% y/y, and June’s to between 4.5% and 5.5% y/y. Even in a scenario of stagnant economic activity from May to December, GDP growth is projected to grow 2.3% in 2025 (carryover effect from end-2024), which we consider a floor for GDP growth this year.

The BCCh is expected to revise its growth projection upward to a range between 2.0% and 2.75% (midpoint at 2.4%). On the one hand, Q1-25 readings overshot the IPoM’s projections, with activity growing 0.7 ppts faster than the March IPoM’s forecast (actual: 2.3% y/y; IPoM: 1.6% y/y). On the other hand, while external risks remain, they appear to have moderated following recent rapprochement between the United States and some of its trading partners.

Considering the above, we estimate that the IPoM’s baseline scenario would give a higher weight to the better-than-expected start of the year in terms of economic activity, with the lower end of the growth range representing those scenarios where the effects of increased global uncertainty generate significant impacts on domestic activity. Overall, the strong start to the second quarter would confirm improved GDP growth expectations for this year.

Why would the Central Bank cut the policy rate in a scenario of upward revisions to its GDP growth projection?

- The upward adjustment in GDP will be driven by positive surprises in the external sector and likely upward adjustments in domestic demand due to improved investment prospects.

- In the second quarter, consumption of goods is expected to be marginally negative given the reversal in purchases by foreigners and residents, whose consumption has not yet accelerated.

- April labour market data showed significant job losses, especially among salaried employees, which were widespread across sectors.

- Core inflation has surprised to the downside.

- The real exchange rate is around 103 points on the margin, at levels similar to those in February of this year, while the multilateral exchange rate is at levels similar to those in March.

—Aníbal Alarcón

MEXICO: IN BANXICO’S SURVEY OF EXPECTATIONS, THE YEAR-END POLICY RATE FORECAST WAS REVISED DOWNWARD TO 7.50%

In Banxico’s latest Survey of Expectations, 2025 GDP growth forecasts were revised downward to 0.18% (from 0.20% previously). The outlook for 2026 also declined to 1.41% (from 1.50%), indicating anticipated weakness in economic activity over the coming quarters. Meanwhile, the median year-end policy rate forecast was lowered to 7.50% for 2025 (vs. 7.75% prior) and held steady at 7.00% for 2026. Inflation expectations were revised upward to 3.90% for this year and 3.77% for 2026, while core inflation is now projected at 3.98% by year-end and 3.70% by the end of 2026. Additionally, analysts now expect a stronger peso, with the exchange rate forecast at 20.50 pesos per dollar by the end of this year and 21.00 in 2026.

REMITTANCES CONTINUE TO DECELERATE

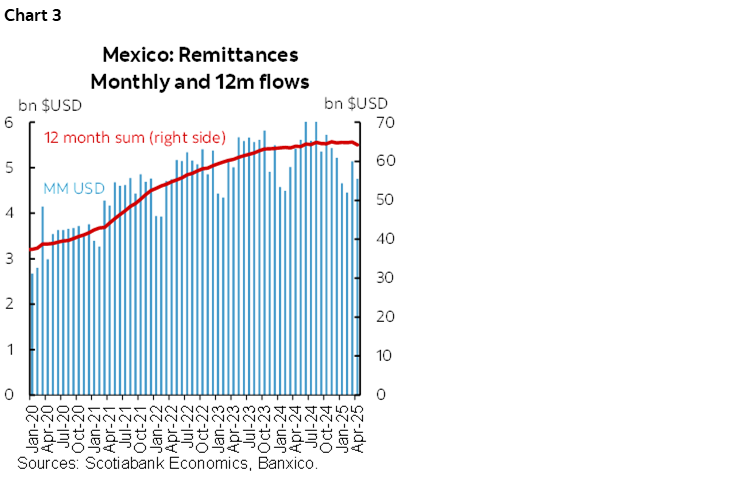

According to Banco de México, remittances in April totaled USD 4.8 bn , marking a year-over-year decline of -12.1% (chart 3). On a twelve-month cumulative basis, remittances continue to show signs of moderation, reaching a total of USD 64.3 bn, representing a modest annual increase of 0.7%. The number of transactions also fell by -8.1%, accompanied by a lower average remittance amount of USD 385, down -4.4%. Looking ahead, remittance flows are expected to face headwinds from the Trump administration’s immigration policies and weaker U.S. growth prospects. However, this negative impact could be partially offset by potential tax cuts in the United States.

—Rodolfo Mitchell, Brian Pérez & Miguel Saldaña

PERU: INFLATION REMAINS STABLE IN MAY

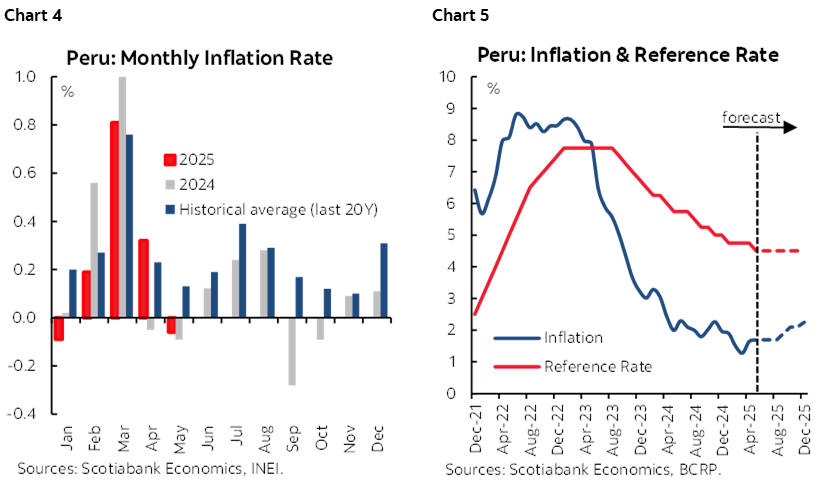

In May, monthly headline inflation was negative, while monthly core inflation increased slightly (chart 4). In year-on-year terms, both remain comfortably below the midpoint of the BCRP’s target range (2.0%). We maintain our end-2025 scenario for headline inflation at end-2025 and 4.50% for the terminal reference rate (chart 5).

Headline inflation stood at -0.06% m/m in May, in line with the -0.1% we expected. However, it deviated from Bloomberg’s market consensus average (+0.13%). The monthly figure stands against the historical average of the last 20 years (+0.13%) but was similar to the figure for the same month in 2024 (-0.09%). As a result, the annual inflation rate remained stable at 1.7% in May, continuing below the midpoint of the BCRP’s 1–3% target band.

The drop in headline inflation during the month can be attributed to price reductions in the food category, down 0.47%, as previous supply constraints on the production of chicken were corrected, leading to a decline in prices. In addition, transportation prices fell 0.26%, as the increase in fares due to the Easter holidays in April was reversed in May. Energy prices such as electricity and gas (-0.21%), in part linked to a weaker USD, also played a role.

Core inflation, the trend component that excludes food and energy, increased slightly by +0.05% in May, lower than the historical average of the last 20 years (+0.14%) and the level recorded in the same month of 2024 (+0.16%). In annual terms, it decreased from 1.9% to 1.8%.

For June, headline inflation is likely to be slightly positive, on balance. Moving forward, inflation would continue to increase mildly, reaching the 2.3% we expect by the end of the year. On the other hand, core inflation would still remain around 1.8% for a few more months.

Regarding the reference rate, we expect the BCRP to hold steady at its next meeting on June 12th, at 4.50%, after surprising the market with a 25bps cut in May. We believe that the cut was due to a deterioration in economic activity expectations, though it was not significant and remained within the optimistic range (above 50 points). However, it is likely that the BCRP anticipated a significant decline, which is why it decided to stimulate economic activity. Going forward, decisions regarding the reference rate could focus on economic activity expectations (the BCRP releases the results to its survey on Thursday, June 5th).

—Ricardo Avila

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.