- Colombia: Unemployment reached historically low levels in April on rising self-employment

On May 30th, DANE published labour market data for April 2025. The national unemployment rate stood at 8.8%, decreasing by 1.9 p.p. compared to 10.6% in April 2024, posting the lowest unemployment rate seen in an April month since 2001. The urban unemployment rate decreased 1.6 p.p. to 8.7% compared to 10.3% in April 2024. Seasonally adjusted, the national unemployment rate decreased to 8.8% from the previous month and remains below that one year ago at 10.6%, while the urban unemployment increased at 8.8%.

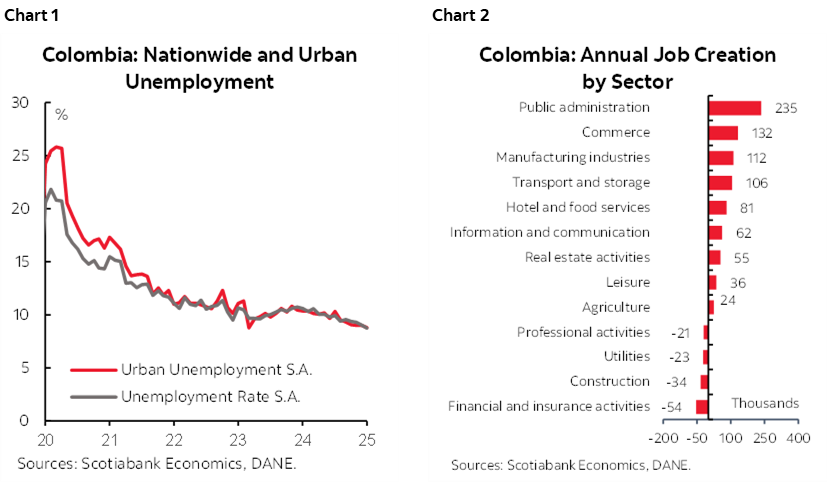

Employment reflects the economic recovery; however, it lacks in quality as the main source of employment is informal. In April, 711 thousand jobs were created, with the most significant contribution coming from public sector, commerce, manufacturing, and transport which contributed with 82% of total. In contrast, construction registered a destruction of 34 thousand jobs, and public administration services, financial and insurance activities, and professional activities—which contribute the most to formality- offset the increase in job creation with a destruction of 74 thousand jobs.

The three-month moving average of job creation continue with a significant acceleration. In the February to April 2025 quarter, job creation averaged 915 thousand, compared to 78 thousand in the February to April 2024 quarter, reflecting that job creation has accelerated at the beginning of 2025. With these results, the economy is reaching pre-pandemic levels with an increase in occupation rate. However, high interest rates and the lack of investment continue to hinder greater dynamism, especially in activities such as industry and construction which represent 90% of the total investment in Colombia.

On a seasonally adjusted basis, the unemployment rate decreased compared to the previous month. The national unemployment rate decreased to 8.8% and in urban areas to 8.8%. At this point, the number of people outside the labour market has increased by 300 thousand people compared with the last year and was reflected on a decrease in labour participation rate from 64.0% in April 2024 to 63.7% in April 2025. However, in our take the labour participation will continue to recover after a drop of 0.2 pps in 2024 that could be related to the historical inflow of remittances in 2024 (+17%), discouraging labour participation. But for now, the April results showed an increase in the occupation rate and a decrease in labour participation, which explained the unemployment rate performance.

As we have seen, these results suggest that job creation is gaining momentum but with a higher cost in informality. The stunning sectors leading the economic activity during most of 2024 are now losing steam, mainly in formal sectors such as professional activities and financial and insurance sector, while some sectors that are starting to show stabilization signals in their production dynamic are now showing better job creation, mainly in informal occupations. For now, we don’t rule out that unemployment may even be below what we estimate, which depends on the degree of absorption of new labour force by the economy.

The data definitively reduce the pressure on the central bank to cut interest rates. However, we affirm our expectation of a rate cut at the June 27th central bank meeting. By this time, we expect a new reading of inflation to be likely lower, while there will also be greater clarity on the fiscal scenario (even if it remains challenging). We believe that the timing for central bank cuts is determined by inflation dynamics. If BanRep decides not to cut in the forthcoming two meetings, we see that the second half cut will be even more challenging, as inflation has risks of rebounding, erasing the possibility of delivering actions to reduce the contractionary stance.

Employment data highlights:

- In April +711 thousand jobs were created, with 9 of the 13 economic sectors recording positive changes. Job creation was concentrated in public administration—mainly in public health activities (+235 thousand)—commerce (+132 thousand), manufacturing (+112 thousand) and transport (+106 thousand). In contrast, the decline in financial and insurance sector (-54 thousand), construction (-34 thousand), utilities (-23 thousand) and professional activities (-21 thousand) offset the general result.

- Surprisingly, informality decreased in April. The informality rate decreased significantly compared to the same period of the previous year, from 55.7% to 55.0%, indicating a better performance domestically. In addition, the quality of employment in urban areas improved, with the informality rate falling from 41.5% in April 2024 to 40.7% in April 2025. However, despite the employment improvement, the new jobs have been focused on informal occupations such as self-employed which increased by +528 thousand in this period (74% of total job creation).

- Colombia’s labour market maintains a high gender gap. In April, the national unemployment rate for women was 11.2% and for men was 7.0%. Thus, men absorbed +538 thousand new jobs, of which +436 thousand were in self-employed workers, + 138 thousand in private sector, +24 thousand in domestic activities, and +11 thousand in day-labourer, offset by the destruction of -72 thousand jobs in public sector, employers and unpaid family worker. The female population created +174 thousand jobs of which +154 thousand in the private sector, +92 thousand in self-employed, and +32 thousand in day-labourer and public sector, offset by -100 thousand jobs in domestic activities, employer and unpaid family worker.

- For 2025, we expect a restructuring of the labour market with improvements in the labour participation rate, but an increasing informality. The balance will depend on the capacity of the labour market to absorb the new labour force that will be incorporated in 2025.

—Valentina Guio

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.