- Mexico: Sharp y/y drop in industrial production in April on Easter timing, in contrast to monthly rise

- Colombia: MinFin unveils 2025 Financial Plan

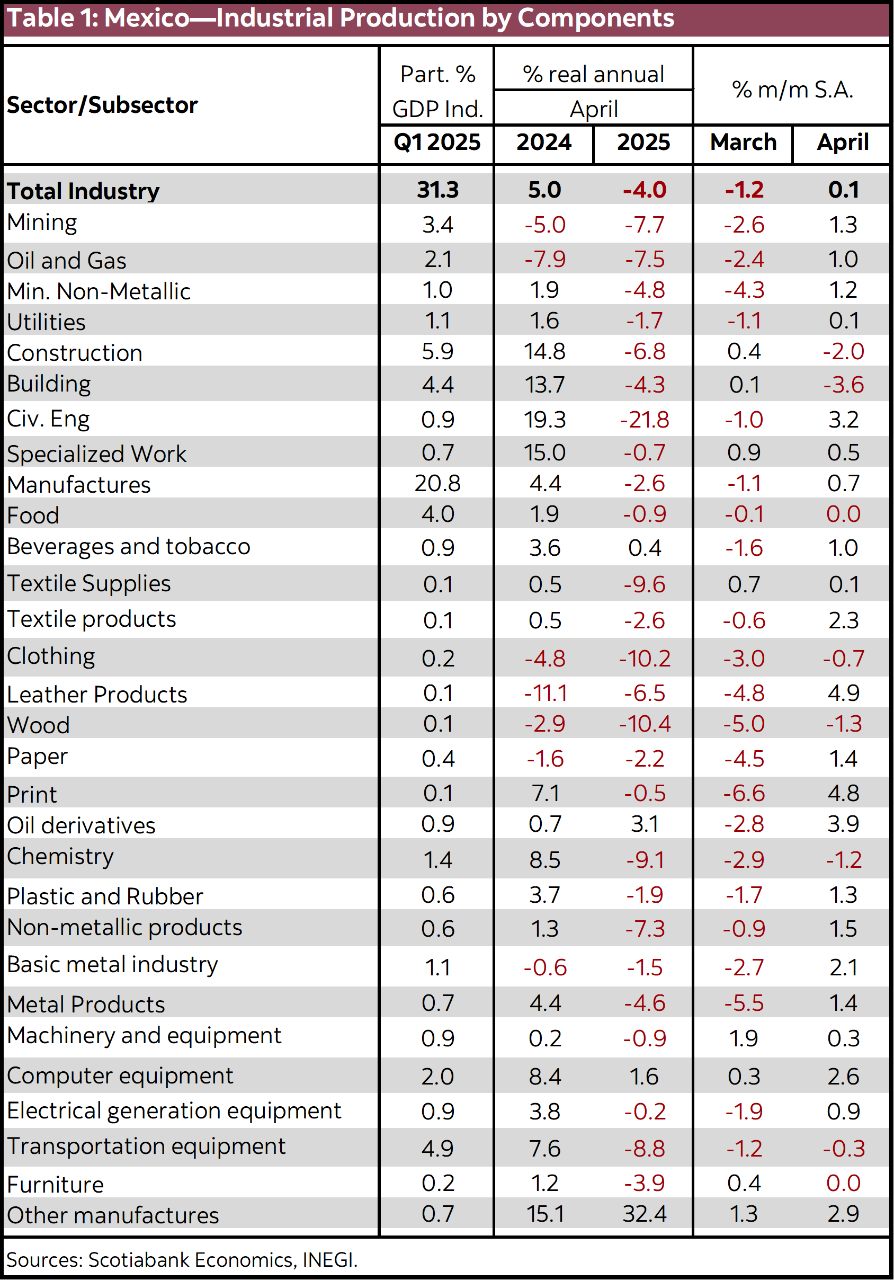

MEXICO: SHARP Y/Y DROP IN INDUSTRIAL PRODUCTION IN APRIL ON EASTER TIMING, IN CONTRAST TO MONTHLY RISE

In April, industrial activity surprised by registering a -4.0% annual decline, down from a 1.9% rise in March, and compared to a Bloomberg median forecast of –3.5% y/y; in workday-adjusted terms, however, it ‘only’ fell 0.9 y/y after a 1.4% drop in the previous month. On a monthly basis, the index showed a slight increase of 0.1% m/m from -1.2% previously, based on seasonally adjusted figures, with construction down -2.0% and manufacturing up 0.7%.

Within the industrial sector, construction fell by -6.8% y/y (5.3% previously) as buildings construction that had expanded by double digits in each of February and March flipped into negative territory while heavy and civil engineering construction recorded another massive decline, of 22% y/y, off a very high base of comparison due the past administration’s mega projects. Mining decreased by -7.7% (-9.4% previously), remaining in negative territory since July 2023 given the drag from the oil and gas sector. Meanwhile, utilities declined for the third consecutive month by -1.7% (-2.0% previously).

Manufacturing slipped into a 2.6% y/y contraction in April that followed a strong March showing at 3.1%, with negative readings across practically all subsectors. Calendar effects may have played an important role here, however, as the timing of Easter in April of this year compared to March in 2024 resulted in fewer working days reflected in today’s data. Adjusted for working days, Mexican manufacturing expanded by 1.3% in April after a 1.0% drop in March. On a monthly seasonally adjusted basis, transportation output suffered another monthly decline, albeit smaller than in March, of 0.3% m/m from –1.2% m/m. possibly reflecting a small scaling back of operations in response to U.S. tariffs. Machinery manufacturing decelerated but remained in expansionary territory, up 0.3% in April from 2% m/m in March.

—Rodolfo Mitchell, Brian Pérez & Miguel Saldaña

COLOMBIA: MINFIN UNVEILS 2025 FINANCIAL PLAN

In a private meeting with members of Market Makers’ program yesterday, the MoF presented the updated 2025 Financial Plan (sources and uses), which shows that the total fiscal deficit would be 7.1% of GDP (vs. 5.1% of GDP expected in the first update), in line with our forecast range for this year. Specifically, additional financing needs would be COP 56.4 tn (USD 13.4 bn) higher, which would be used as follows: i) COP 39 tn (USD 9.3 bn) would be used to finance the additional deficit, and ii) COP 19 tn (USD 4.5 bn) would be used to increase cash reserves at the end of the year.

The composition of the financing sources is striking, where: i) COP 12 tn (USD 2.9 bn) comes from bond issuance, ii) COP 16 tn (USD 3.8 bn) will be through increased issuance of short-term bonds (TCO), iii) COP 14 tn (USD 3.3 bn) will be obtained from government-managed funds held in trusts, and iv) COP 12 tn (USD 2.9 bn) will be raised via Total Return Swaps (TRS) with offshore banks, using TES securities as collateral. From Scotiabank Colpatria’s market perspective “by avoiding excessive pressure on primary bond auctions—where we had expected at least COP 20 tn in new issuance—and instead relying on short-term debt instruments, the strategy minimizes near-term debt servicing costs”.

According to the MoF, the increase in the deficit is due to the recognition of inflexible spending, without which the government would have faced a potential government shutdown in November. For now, this could affect the risk perception of rating agencies because the fiscal consolidation process expected in the first update of the 2025 Financial Plan would not occur. In contrast, the national government is even using the resources it holds in trust funds from local government entities.

This adjustment to the 2025 Financial Plan and its consistency with the fiscal accounts over the next 10 years will be reflected in the publication of the 2025 MTFF on Friday, where the suspension of the fiscal rule for at least three years will also be announced (see here).

While the outlook for fiscal accounts is negative, the most recent inflation data support the continued rate cuts by the central bank, where we maintain our expectation of a 25bp cut to 9%. We believe BanRep will give greater weight to the decline in inflation observed in May. However, fiscal risk will continue to be a risk to be assessed in upcoming meetings as local assets incorporate higher risk premiums.

—Valentina Guio

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.