- Colombia: Inflation undershoots in May, reaching its lowest rate since October 2021; On the fiscal rule suspension and the release of the short-term fiscal framework

COLOMBIA: INFLATION UNDERSHOOTS IN MAY, REACHING ITS LOWEST RATE SINCE OCTOBER 2021

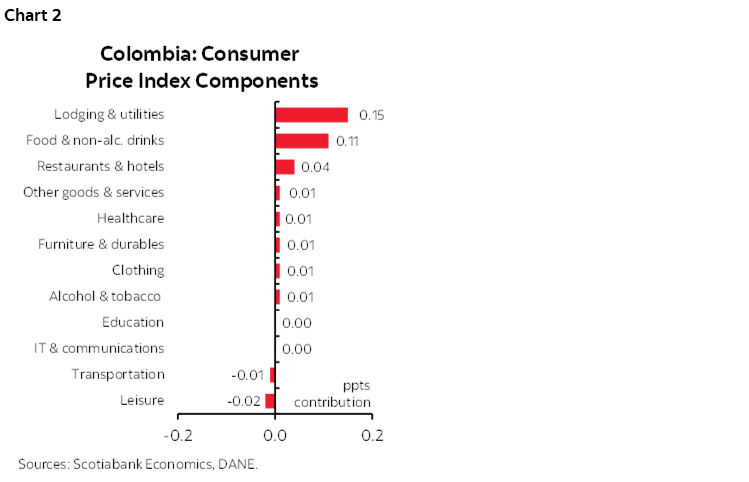

Colombia’s monthly CPI inflation rate was 0.32% m/m in May, according to data published by DANE on Monday. The result was below analysts’ expectations in the BanRep survey of 0.38% m/m, as was Scotiabank Colpatria’s forecast. During the month, 9 of the 12 groups had a positive monthly variation, with lodging and utilities, and food contributing the most to the result, accounting for around 80% of total monthly inflation.

May inflation reflected seasonal changes due to the timing of Easter in April, with tourism-related services showing negative variations. Indexation effects have been diluted, though they are still present in some services such as restaurants and rental prices, while services such as transportation may have already incorporated these effects into their prices. Regarding food, the monthly variation was higher than the average for May; however, this may be related to calendar changes (Easter) and the winter season.

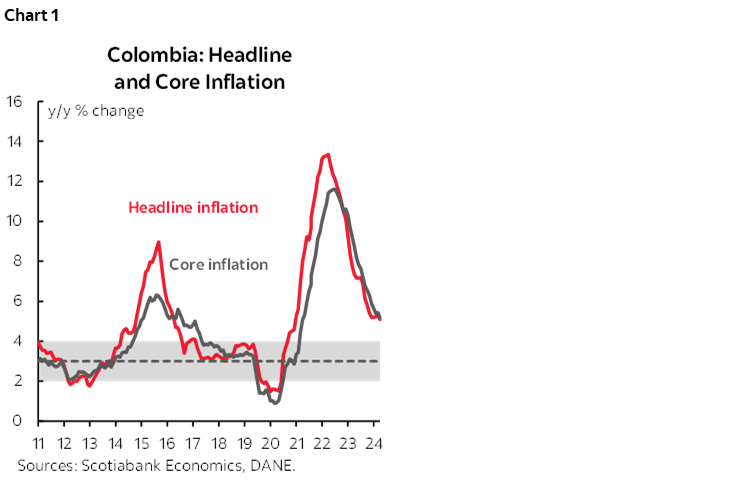

In annual terms, inflation fell from 5.16% in April to 5.05% in May (chart 1), resuming its downtrend and showing a decrease of 0.15ppts compared to the end of 2024 (5.20% y/y). Inflation excluding food fell from 5.29% to 5.13%, while inflation excluding food and regulated items fell from 4.90% to 4.77%, reaching its lowest level since March 2022. Goods inflation maintained its uptrend, rising from 1.1% to 1.45%, but remaining below the target range (2%–4%), while services inflation (excluding regulated services) fell from 6.37% to 6.06%.

May inflation reflected that most of the indexation effects were transmitted in the first four months of the year, which can be seen as a positive development for the upcoming BanRep meeting. Inflation has driven the Central Bank’s decisions, and we hope that with the May surprise, the board of directors will continue the easing cycle at its June 27th meeting. Our scenario is a 25 bps cut to 9.00%, a level that remains contractionary enough to support inflation falling to the 3% target. However, the fiscal scenario remains a headwind and is consolidating as the main risk to imported inflation, in a scenario with higher risk premiums on local assets.

Other highlights:

- Two large groups accounted for 80% of inflation. Lodging and utilities were the largest contributors to inflation, with a monthly increase of 0.48% and a contribution of 0.15 ppts (chart 2). Rental rates were the largest contributors, along with an increase in water supply (+1.29% m/m). Energy rates had a negative variation of -0.93%, while gas rates broke two months of negative variations, reaching 0.65% m/m.

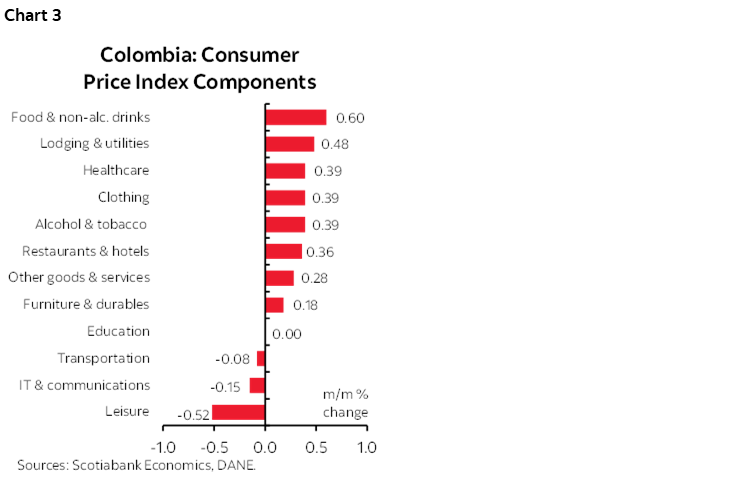

- The second largest contributor was food prices, with a variation of 0.60% m/m and a contribution of 0.11 ppts (chart 3). Monthly inflation was higher than the historical May average of 0.33%; however, this could be a temporary effect of the winter season, which affects crops and the goods transportation. The foods that contributed most were tomatoes (+12.28% m/m), onions (+5.66% m/m), and coffee (+5.46% m/m), while some foods that partially offset this performance were potatoes (-3.68% m/m), chicken (-0.97% m/m), and fresh fruit (-0.81% m/m).

- Three groups recorded negative growth. Leisure registered a monthly growth of -0.52%, subtracting 0.02ppts from the total monthly growth. Tour packages (-2.16% m/m) and other recreational services recorded negative growth. The information and communications, and transportation groups also recorded negative growth of -0.15% m/m and -0.08% m/m, respectively, with the negative growth in air transportation (-2.09% m/m) standing out.

—Daniela Silva

ON THE FISCAL RULE SUSPENSION AND THE RELEASE OF THE SHORT-TERM FISCAL FRAMEWORK

The fiscal rule in Colombia has a mechanism to justify non-compliance in unforeseen circumstances, and these are the famous escape clauses. For instance, during the pandemic, it was clear that Colombia was going to exceed the deficit established by the fiscal rule, so it used the escape clause by announcing that (for obvious reasons) it would have to spend more due to COVID. This suspended the fiscal rule for two years while the pandemic passed.

Currently, what's being discussed and the different reports in media are saying that at the CONFIS (fiscal policy council, the country's highest fiscal policy authority) meeting on Monday, June 9th, the first item on the agenda was to discuss the possible activation of the escape clause for now to up to three years. If that happens, the government must justify whether there are extraordinary events that compromise the country's macroeconomic stability and justify suspending the fiscal rule mechanism. So, the only indication we have of the activation of an escape clause since the fiscal rule began in Colombia (2011) is the pandemic.

The only thing the Autonomous Fiscal Rule Committee (CARF) can do is issue a non-binding opinion on whether the activation of this clause is justified. The media published that the CARF refrained from giving a favourable opinion, and the law indicates that the CARF has one week after the clause activation to publish an official announcement. For now, according to Reuters, the official CONFIS press release scheduled for Tuesday, June 10th, 11 AM (Bogotá time) has been canceled and rescheduled for Friday, June 13th, after the 2025 MTFF publication.

For the 2025 Medium (Short) Term Fiscal Framework (MTFF), we estimate a total fiscal deficit of between 6.0% and 7.4% of GDP in 2025, but with a higher probability that the release will show an estimate closer to or even exceed 7.4%, which concludes the government would have neither the capacity nor the will to cut spending. Also, we are expecting increases in additional borrowing needs of between COP 20 trillion and 48 tn (see here) under those scenarios.

—Valentina Guio & Daniela Silva

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.