- Colombia: May’s retail sales and manufacturing beat expectations

On Tuesday, July 15th, the National Institute of Statistics (DANE) published the manufacturing production and retail sales data for May 2025. Manufacturing production increased 3.0% y/y, above market expectations (2.0% y/y), and retail sales increased 13.2% y/y above market expectations (12.1% y/y). These results are encouraging for economic growth. As observed, household consumption continues to follow a positive trend, and industrial sectors that experienced a downturn last year are now showing signs of recovery and contributing to the overall boost.

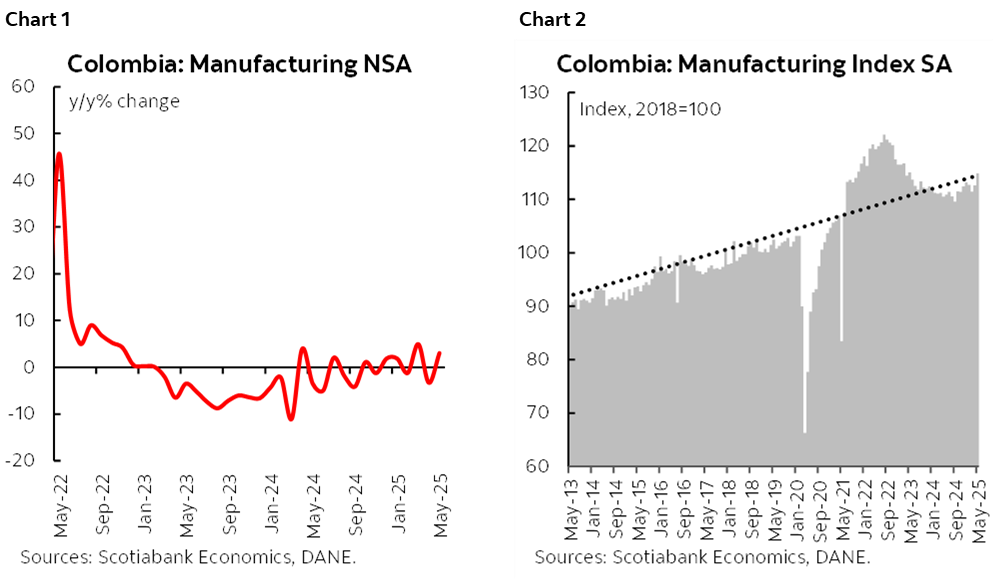

Manufacturing output increased by 3.0% y/y (charts 1 and 2), driven by higher sales in vehicles, apparel, and food and beverages. The May results reflect a positive turnaround in the manufacturing sector compared to the same month last year, when output contracted by -3.5% y/y. Seasonally adjusted data also showed a 2.0% m/m expansion. Within this context, the food, chemicals, and apparel industries contributed positively to the overall increase, partially offset by declines in the iron and steel, oil and fuel, and metal products sectors.

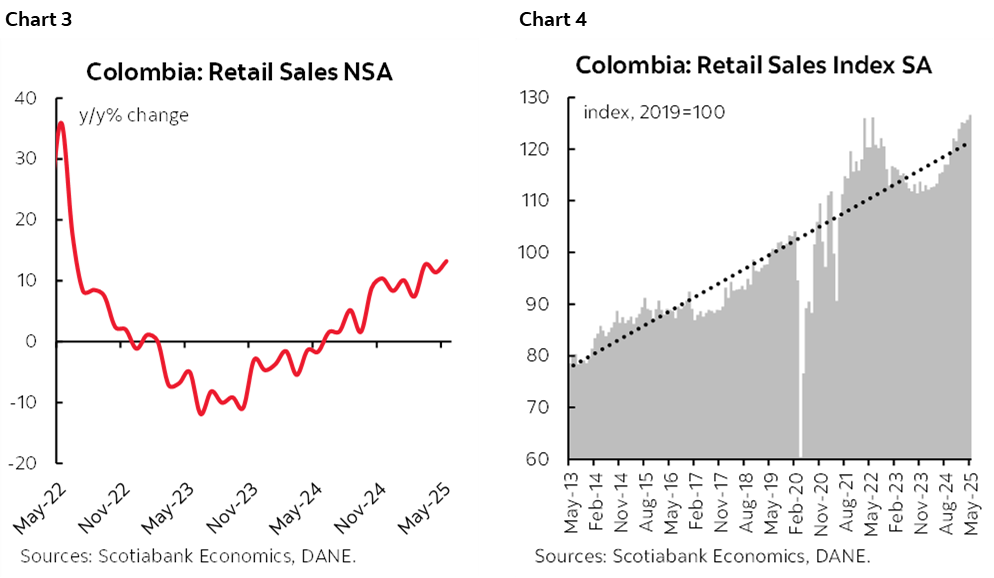

Retail sales maintained their positive momentum (charts 3 and 4), recording the highest expansion in the past three years. In May, retail sales rose by 13.2% y/y, while seasonally adjusted data (excluding vehicles) showed a 0.7% m/m increase. The annual growth was driven by strong performance in vehicle sales, telecommunications equipment, and durable goods such as household appliances and other domestic products. This robust performance is occurring despite persistently high interest rates and inflation that has yet to fully normalize. This may suggest that Colombian households are getting used to the current context and engaging their consumption decisions with better confidence. As we have seen, households are using credit moderately and instead the savings buffer remains solid, leading us to think that the recovery of the private consumption has stronger bases compared to the post-pandemic rebound.

On Friday, July 18th, DANE will release the Economic Activity Index for May 2025. This release will be key to monitoring the structural adjustment of the Colombian economy, where sectors such as commerce and manufacturing are emerging as the main drivers of growth, in contrast to services like leisure and the public sector, which have lost momentum. The recent economic performance provides an additional reason for the central bank to remain cautious. Accordingly, the board decided to keep the policy rate unchanged at its June 27th meeting, in line with market expectations. In our view, although economic activity is showing solid performance, the output gap remains negative and recent inflation data has surprised to the downside. For these reasons, we see room for a rate cut at BanRep’s upcoming meeting on July 31st, potentially bringing the policy rate down to 9%.

Highlights:

- Manufacturing production increased 3.0% y/y. 25 of the 39 activities showed annual expansion. On the positive side, food (+19.5% y/y), chemical products (+13.2% y/y), apparel (+12.7% y/y), and mineral products (+7.1% y/y) contributed +2.3 ppts to the result. On the negative side, the iron and steel industry (-16.6% y/y), the oil and fuel industry (-7.4% y/y) and metal products (-8.9% y/y), were the main sectors offsetting the boost in the period, contributing with -1.9 ppts

- Retail sales grew by 13.2% y/y. The 19 activities registered positive variations. Vehicle sales (+29.8% y/y for household vehicles and +15.8% y/y for other ones), telecommunications equipment sales (+56.5% y/y), and household appliances (+23.3% y/y) were the ones that contributed the most to retail sales growth. It’s important to highlight the increase in apparel in 2025 after almost two years of contraction, but still below pre-pandemic performance.

- From June 2024 to May 2025, retail sales expanded by +7.7% y/y where apparel sales experienced a drop of 4.4%, while the sales of telecommunications equipment have had the best contribution to the result with an expansion of +39.4. Furthermore, during the same period, the manufacturing output dropped -0.2% y/y explained by the pharmaceutical industry (-9.5% y/y), oil and fuel production (-5.6% y/y) and the beverages industry (-1.8% y/y). In contrast, transport equipment (+31.1%) and the cleaning industry (+3.8%), maintain a positive contribution in the indicator.

—Valentina Guio

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.