- Chile: Congress passed the Pension Reform with broad political support

- Colombia: Monetary Policy Preview—BanRep could pause the easing cycle amid inflationary risks in 2025

- Mexico: Q4 GDP slowdown driven by uncertainty

- Peru: Cement sales—A promising recovery in 2025; Cement sales as of November 2024

CHILE: CONGRESS PASSED THE PENSION REFORM WITH BROAD POLITICAL SUPPORT

On Wednesday, January 29th, Congress approved the Pension Reform with broad support from most political sectors. This reform will increase national savings, thereby improving the depth of the capital market and the demand for fixed-income instruments, among others. It also contributes to reducing the political uncertainty of a pending reform, which had not been completed for more than a decade. With this, the bill is ready to become law. Among the most relevant agreements that were approved, we highlight the following:

- A new employer contribution of 7 ppts of taxable income. This will be added to the 1.5 ppts that employers already contribute to the Disability and Survivors’ Insurance (SIS), so that employers will contribute a total of 8.5 ppts for the benefit of the worker.

- This total will be distributed in 4.5 ppts for individual capitalization, with the aim of strengthening future pensions. The remaining 4 ppts will be administered by Social Security and will have the following composition: 2.5 ppts will cover the SIS contingencies—disability and survival—and the Compensation to Women for longer life expectancy. The difference of 1.5 ppts will be used to finance the Benefit per Contributed Year, an instrument that will improve current pensions and will be transitory.

- The increase of the new contribution of 7 ppts, to reach 8.5 ppts, will be implemented gradually over 9 years. This could be extended by two years if an external evaluation of the Tax Compliance Law, to be carried out in the third year, shows a lower collection effect than expected, in accordance with the recommendations of the Autonomous Fiscal Council.

- The reform also considers an increase in the PGU to CLP 250,000 (USD250). The increase will begin to take effect from the sixth month after the publication of the law and will be gradual, starting with pensioners over 82 years of age until full coverage is completed within 30 months. The current amount of the Basic Pension is CLP 224,000 (USD 224).

- The initiative includes regulatory changes to the pension industry, which will result in more transparency and competition, with lower costs for individuals. For example, it establishes the bidding of the stock of affiliates, a process that will be carried out every two years and in which 10% of the current affiliates will be randomly bid. The process will be awarded to the bidder with the lowest commission, which must be maintained for five years. Affiliates may withdraw or change their investor at any time.

- The AFPs will have the possibility of subcontracting the support functions, among which the Social Security Institute (IPS) may act. In addition, they will have to report the support and account management functions separately.

- The replacement of multifunds by generational funds, a model that seeks to maximize profitability and limit risks. The deadlines for the implementation of generational funds were advanced with respect to what was originally proposed by the Government. This system would begin to be implemented as of the 25th month after the publication of the law. For this purpose, the Central Bank will have until the 12th month to define the investment limits, while the investment regime of the Funds must be defined no later than the 18th month. Such Regime may authorize transitory limits during the 36 months following the implementation of the generational funds.

- The reform also considers various measures to increase the density of contributions. Among others, the expansion of the Pension Gap Insurance.

—Aníbal Alarcón

COLOMBIA: MONETARY POLICY PREVIEW—BANREP COULD PAUSE THE EASING CYCLE AMID INFLATIONARY RISKS IN 2025

On Friday, January 31st, BanRep will hold its first monetary policy meeting of 2025. Throughout 2024, inflation allowed the central bank to implement a gradual and consistent easing cycle; however, fiscal risks, uncertainty about wage increases, and more restrictive international financial conditions were the Board’s main arguments for slowing down the pace of cuts in December. In January, the outlook does not look different as some risks emerged since the last meeting in December, especially for the inflation path after the increase in the minimum wage, which supports the necessity for maintaining a cautious approach in the easing cycle. That said, Scotiabank Colpatria expects rate stability at 9.50%, resuming the easing cycle with cuts in March to close the year at a rate level of 7.75%.

Inflation stopped decreasing in December, standing at 5.20%. Additionally, the increase in the minimum wage was determined at 9.54%, higher than inflation by 434 bps and higher than the range estimated by the market and BanRep (6%–7.5%), which implies a greater indexation in the prices in the services part of the CPI basket. The previous risk increases the probability for inflation remaining above the target range throughout 2025, which leaves less room for the acceleration of cuts. However, the March decision will be key to determine the position of the new members of the Board (Laura Moisa and Cesar Giraldo), since on different occasions the Minister of Finance, Diego Guevara, has hinted that a greater consensus would be reached on a more flexible monetary policy.

Inflationary risks are still present and have even increased. The fulfillment of fiscal obligations by the Government continues to be a variable to monitor, and even though S&P ratified the credit rating, cash flow problems could generate pressure in the future. Additionally, a recent diplomatic conflict between President Donald Trump and President Gustavo Petro opened the door to evaluating possible commercial impacts and their effects on inflation in a scenario in which the relationship between both nations deteriorated.

We expect that the Board will decide to keep the monetary policy rate stable at 9.50% in January and cut the rate by 25bps over the next seven meetings to close at 7.75%, given a start to the year with a lot of uncertainty surrounding it and inflation expectations for 2025 that unanchored in recent surveys. It is worth noting that this month the Bank’s technical team will present the projections of the different macroeconomic variables, which will give us a broader overview of the incorporation of recent new information, since in its last update they anticipated that inflation would reach the target in the fourth quarter of 2025.

Key points to consider ahead of January’s BanRep meeting:

- December inflation was above expectations. General inflation stood at 5.20%, remaining stable compared to the rate observed in November. Core inflation showed moderate progress, going from 5.88% y/y to 5.48% y/y. Food prices stopped contributing to disinflation, and energy rates reversed the downward trend they had maintained for five consecutive months. It is worth noting that the main disinflationary forces in 2024 came from food, regulated prices, and tradable goods, and those forces are not expected to be repeated with the same force in 2025.

- The increase in the minimum wage for 2025 exceeded expectations. The Government determined an adjustment of 9.54%, higher than expected by the Central Bank. The adjustment supposes a greater indexation effect on some prices of goods and services, as well as indirect impacts due to higher payroll costs in companies. The increase is supposed to impact the path of inflation, something seen in BanRep’s analyst survey, which now points to a year-end inflation estimation around 4.21%, 30bps above the previous estimation.

- Economic activity continues to show the disparity in the different sectors, however, 2024 would have registered a better performance than estimated. Economic growth has remained far from being a concern for the Board given a better performance that suggests that the GDP for 2024 would have grown between 1.7% and 1.9%. However, in 2025 Colombia would continue to operate below its potential, and agriculture and some service activities that outperformed in 2024 would moderate its contribution, which may mean a more flexible stance in the medium term.

- Political and fiscal uncertainty remain. The Board, in its last meetings, stressed its concern about the Government’s fiscal problems and their impact on local assets. The COLTES rates are pricing the fiscal uncertainty and the low liquidity buffers that the government has highlighted in its fiscal plans. On the other hand, the diplomatic shock between Colombia and the US maintains political risk as a relevant concern.

- Is there a probability of a 25bps cut? The answer may be based on BanRep’s consistency during the easing cycle. However, the scenario has many inflationary risks that may influence BanRep’s greater caution. The Monetary Policy Report will be published on February 4th. The technical team will announce its projections for the different macroeconomic variables. The inflation path is expected to show upward changes, while growth in 2025 could be more moderate compared to the previous report.

—Jackeline Piraján & Daniela Silva

MEXICO: Q4 GDP SLOWDOWN DRIVEN BY UNCERTAINTY

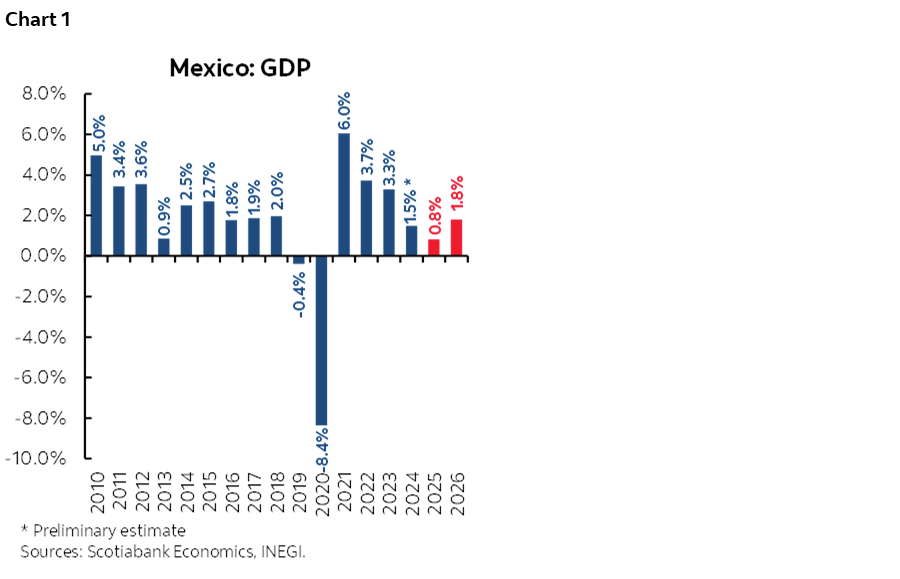

The timely estimate of Q4-2024 GDP confirmed the anticipated economic slowdown amid the significant increase in uncertainty in Mexico. Economic activity recorded a lower-than-expected increase, this time at 0.6% year-over-year in real terms, down from 1.6% in Q3, below the consensus expectation of 1.0% growth. By sectors, industrial activity fell by -1.7% year-over-year (previously 0.5%), while the services sector grew by 2.1% (previously 2.2%), and the primary sector experienced a sharp contraction of -4.6% (previously 4.1%). With the data, GDP registered a 1.5% increase during 2024. In seasonally adjusted quarterly terms, GDP decreased by -0.6% quarter-over-quarter, down from 1.1% previously, below the consensus of -0.2%. The industrial sector fell by -1.2% quarter-over-quarter (previously 0.9%), while services slightly increased by 0.2% (previously 1.1%), and agricultural activities declined by -8.9% (previously 4.9%).

These data confirm the economic slowdown during 2024, with the industrial sector being the most affected, while services maintained growth and the agricultural sector showed volatility. Looking ahead, we expect that uncertainty related to the impact of the new administration’s policies in the United States, as well as political and economic challenges in Mexico, will continue to negatively affect economic growth. Thus, we forecast weak growth of 0.8% in 2025. However, we do not anticipate an economic recession in the near future, although the probability of experiencing a negative quarter in 2025 increases due to lower consumption and investment (chart 1).

—Rodolfo Mitchell, Brian Pérez & Miguel Saldaña

PERU: CEMENT SALES—A PROMISING RECOVERY IN 2025

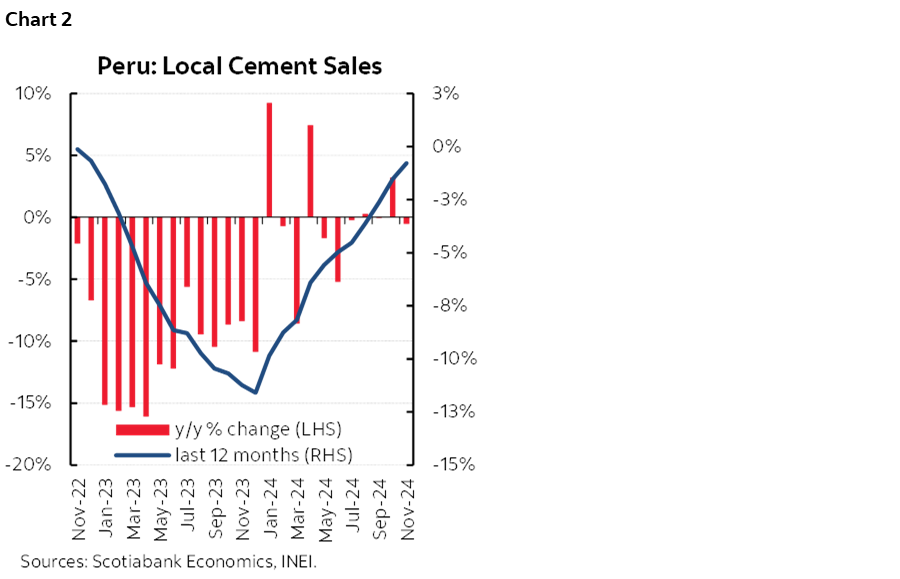

Peru’s Cement Producers Association (Asocem) forecasts cement sales in the country to reach 12 million tons in 2024, similar to the level reached in 2023. Cement production is important as it is a major component in determining construction GDP growth. The cement industry saw a number of positive drivers in 2024, that were, however, counterbalanced by factors that curtailed growth. The positive drivers included: i) a record level of public investment; ii) a strong performance in the formal real estate sector in Lima, especially in the development of high-value housing projects; and iii) increased investment in concessioned transportation infrastructure projects (chart 2).

At the same time, however, weak self-construction and the slowdown in social housing projects limited cement demand. Self-construction, which accounts for nearly 70% of total cement consumption, is likely to have declined in 2024 due to the slow recovery of private formal employment, as real household income levels have not yet recovered fully from the 2022–2023 inflationary period. Additionally, there has been a decrease in demand for cement for developing social housing projects under the Fondo Mivivienda (FMV) due to regulatory changes and a lack of predictability in budget allocations.

For 2025, we anticipate a return to growth in cement sales at a rate close to the 3.3% expansion we forecast for the entire construction sector. This recovery is expected to be driven by improvements in a number of segments—particularly during H1-25. We predict an increase in private formal employment, which will contribute to higher incomes available for self-construction. We also expect the continuation of projects in the formal real estate sector, particularly in the construction of high-value housing in Lima, aided by the gradual decrease in mortgage interest rates, and an expansion in social housing construction due to increased public budget allocations. Furthermore, we foresee greater investment in concessioned infrastructure projects, including some works tendered at the beginning of 2024, as well as an uptick in demand for public investment projects, which is expected to grow in 2025, albeit at a slower rate than in 2024.

Cement Sales as of November 2024

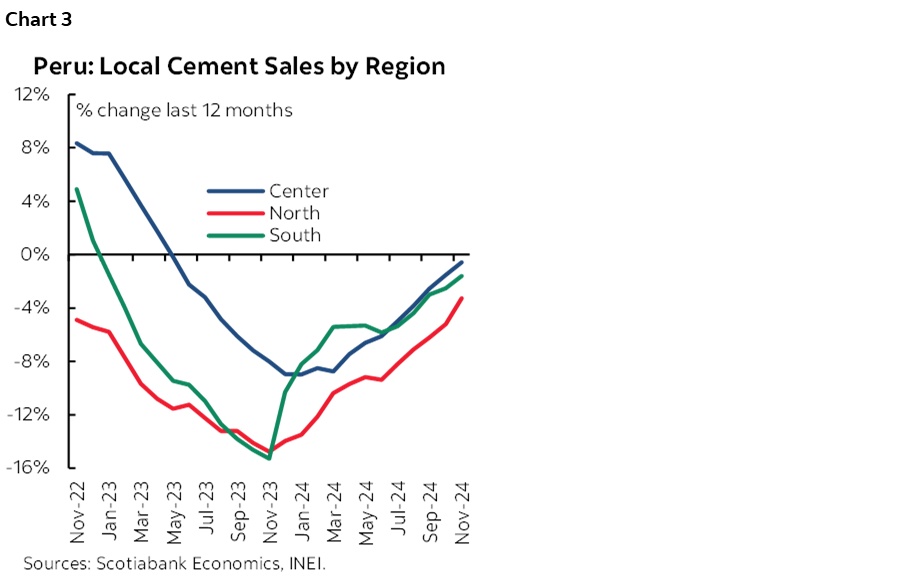

As of November 2024, cement sales showed a slight increase (+0.2%) compared to the same period in 2023, according to the National Institute of Statistics and Informatics (INEI). Regionally, the central part of the country experienced the most significant recovery, accounting for slightly over 50% of domestic cement dispatches, and being the only region to close 2024 with positive results. The dynamism of public investment from January to November—especially from the National Government (+24%) and Regional Governments (+41%)—drove up cement demand. This was complemented by vigorous investment in formal real estate in Lima, particularly in high-value projects, as housing sales grew by 28% as of October, according to the Association of Real Estate Companies (ASEI). Additionally, investment in concessioned transportation infrastructure projects surged by 50%, according to figures from Ositran (chart 3).

Conversely, lower demand for cement in self-construction and social housing projects has constrained the overall results for 2024. The slow recovery of incomes and private formal employment, compounded by weak private investment—particularly during H1-24—has negatively impacted cement demand. Furthermore, the limited development of real estate projects for social housing has also affected demand, as Mivivienda loan placements fell by 20% in 2024, according to FMV figures.

—Carlos Asmat

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.