- Peru: Headline and core inflation continued to decline in January

After global markets opened the week with a bang on the weekend’s tariffs announcements, quieter trading has taken hold today after a measured Chinese response to US tariffs, while we continue to watch for trade headlines (maybe now it’s the EU in focus for Trump) and await the release of US job openings data at 10ET. The Latam day ahead will give us the results of the latest Banxico survey of economists at 10ET as well as the presentation of BanRep’s monetary policy report on the Colombian economy. There were no key data out in Asia nor Europe to shape prices and we think volatile job openings data should be of secondary concern for markets that are trading at the whim of White House announcements.

In retaliation to the US’s 10% additional tariff on Chinese goods effective today, China has unveiled a 10% additional charge on roughly USD10bn of US oil and agricultural equipment and a 5% additional duty on roughly USD5bn of US coal and LNG, as well as targeted measures on some US companies and restrictions on critical metals exports (namely tungsten). China’s restrained response package was but a scratch for global risk sentiment as US equity futures track unchanged on the day (slightly dipped on the announcement but then came back) while cash European indices sit mixed with Euro Stoxx and FTSE up and down, respectively, about 0.5%.

Currencies are mixed, with the MXN lagging all majors with a 0.5% drop after its outperformance yesterday (+1.5%) on the one-month tariffs pause, but unlike the MXN the CAD is also stronger today (about 0.5%) as it catches up to the peso’s gains on Canada’s own tariffs pause. The JPY, on an improved risk mood and a rise in US yields, is the day’s second worst performer, down 0.3%. Like USTs, gilts and EGBs are trading cheaper on the day but while US yields rise by 1–2bps, German and UK yields are 3–5bps higher. Though currencies and equities are calm on the China news, crude oil is off about 3% in anticipation of reduced Chinese demand but iron ore and copper prices are flat to slightly bid.

—Juan Manuel Herrera

PERU: HEADLINE AND CORE INFLATION CONTINUED TO DECLINE IN JANUARY

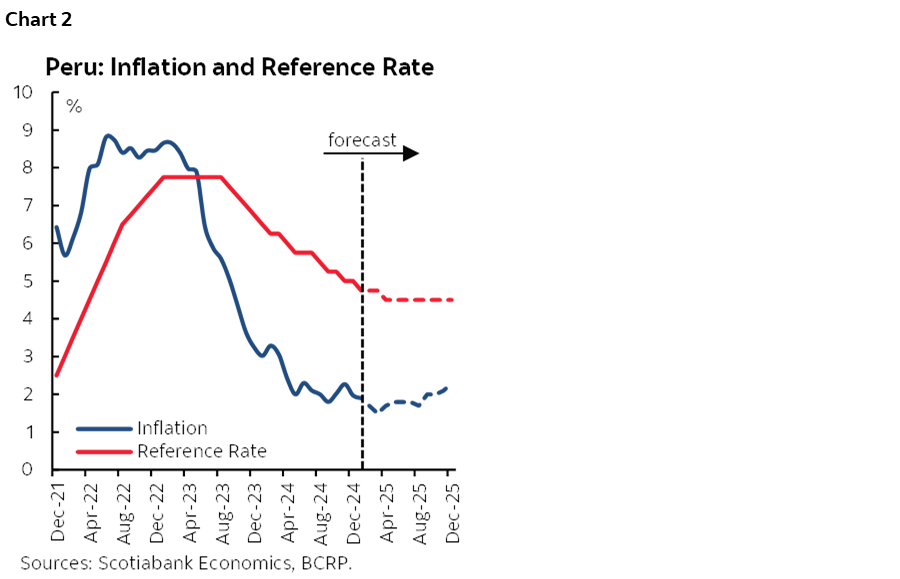

Peruvian price growth was negative in January, reducing the annual rate of inflation from 2.0% to 1.9%. This trend is expected to continue during Q1-25, reaching levels of around 1.5% due to a high base effect that would be partly offset by the price correction of some products. We maintain our forecast of 2.3% inflation for end-2025 and a 4.50% terminal reference policy rate.

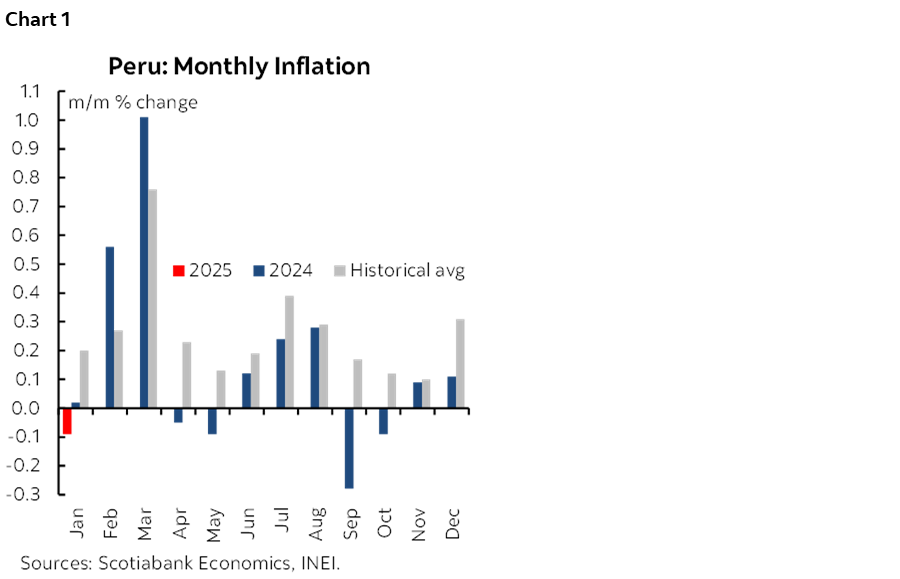

Headline inflation was -0.09% month-on-month in January, in contrast to the +0.05% expected by the Bloomberg median and the historical average of the last 20 years (+0.20%). As a result, annual inflation slowed from 2.0% at the end of 2024 to 1.9% in January, below the midpoint of the Central Reserve Bank’s (BCRP) target range. Thus, inflation has remained within the target range for 10 consecutive months (chart 1).

Core prices, the trend component that excludes food and energy, fell by -0.15% m/m, being more negative than the historical average of the last 20 years (-0.03%). In year-on-year terms, core inflation decreased from 2.6% recorded at the end of 2024 to 2.4% in January. The BCRP sees core inflation at the midpoint of the target range (2.0%) as ideal, but controlling overall inflation within the target range is a higher priority.

The reduction in headline inflation during the month is explained by lower prices for chicken (-10.5%) due to increased supply, as well as lower prices for national air transport fares (-21.5%), interprovincial transport fares (-15.4%), and taxi fares (-1.8%), which corrected after the holidays for the end of the year. The drop in chicken prices is significant, given that it is the product with the greatest weight in the basic consumer basket and if its price had been maintained, monthly inflation would have been between 0.3% and 0.4%.

At the end of Q1-25, headline inflation would be around 1.5%, given that there is a high base effect in February and March, the only months of 2024 that had a reading well above the historical average of the last 20 years. This would be offset by products that are at low levels and should correct, as is the case of chicken (the most important product in the basic consumer basket), due to the fact that it had a significant drop in January. Additionally, the international price of corn has been recovering since the beginning of November. We are also seeing the base effect on the side of underlying inflation and during the next few months it would converge to the midpoint of the target range (2.0%), and could even be located below it.

Regarding Trump’s economic policies, there is greater risk in the world, which leads us to maintain our projections with a neutral bias (previously the bias was downward). We maintain our forecast of 2.3% inflation for end-2025, given that we expect greater price pressures during H2-25. Regarding the BCRP reference rate, we expect that at the next meeting on February 13th the board will keep its rate unchanged at 4.75%. We maintain our base scenario of a 4.50% terminal rate, which would be reached during Q2-25 (chart 2).

—Ricardo Avila

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.