- Mexico: Mexican peso rollercoaster as Mexico and US reach agreement to avoid February 4th tariffs

- Chile: GDP expanded 6.6% y/y in December (2.5% in 2024); Unemployment rate drops to 8.1% in December, with low participation and job creation

- Colombia: In December, the unemployment rate improved, while in 2024 labour force participation decreased

MEXICO: MEXICAN PESO ROLLERCOASTER AS MEXICO AND US REACH AGREEMENT TO AVOID FEBRUARY 4TH TARIFFS

On February 1st, the White House confirmed 25% across the board tariffs on Mexican exports into the US, and 25% on imports from Canada except oil and gas which got 10%. Trump vowed “This tariff will remain in effect until such time as drugs, in particular Fentanyl, and all Illegal Aliens stop this invasion of our Country!”. In the statement, the White House also used aggressive language against Mexico, accusing its government of links to drug trafficking. This could further concerns over the looming executive action pledged on designating Mexican drug trafficking cartels as Foreign Terrorist Organizations (FTOs).

Yesterday, Mexico’s President Claudia Sheinbaum delivered what could be characterized as a balanced response, suggesting that the US government’s concerns are best addressed with collaboration and offered to establish cooperative dialogue. She also stated that sovereignty is “not negotiable by force”, and suggested a retaliatory “Plan-B” would be implemented, including tariff and non-tariff measures, the details of which would be unveiled at a press conference on Monday morning. At the end of her Sunday message, Sheinbaum suggested she had hope that her offers to the US Government could still avoid US tariffs coming into effect—and, in fact, they did (more on this later). Sunday evening trading saw the peso trade about -2.7% weaker vs the greenback (making it the worst performer out of the World’s 32 most liquid FX).

On Monday morning (note that today is a holiday in Mexico), Ministry of Finance, Rogelio Ramirez de la O, spoke to investors about the state of the economy, which he mentioned is resilient, while he added that International Reserves, hold by Banco de México, could be used to cover shocks in imports. Furthermore, he mentioned that the Finance Ministry is closely working with Central Bank on liquidity. Even though, the above mentioned, he is expecting a growth moderation, while manufacturing, autos, computing, and other goods and industries will face headwinds.

Moments after Ramirez de la O’s conference call, President Claudia Sheinbaum announced in social media that she and Trump had a good conversation with much respect for their relationship and sovereignty. As a result, they had reached a series of agreements that includes the compromise that Mexico will immediately reinforce the northern border with 10,000 National Guard members to prevent drug trafficking from Mexico to the United States, particularly fentanyl. Additionally, The United States commits to working to prevent the trafficking of high-powered weapons to Mexico. Also, Mexico and US teams will start working today on two fronts: security and trade, plus migration.

Finally, she mentioned that President Trump has agreed to pause tariffs for one month starting now. This extension will undoubtedly be a period and process of negotiation, in which Trump started by showing that he is willing to use all the tools available. After Sheinbaum’s post on “X”, the MXN has appreciated to the mid-20s level (20.50 at writing) from a maximum level of 21.30 pesos per USD. The peso’s ~1% rise on the day now makes it the best performing major currency, followed by the JPY’s ~0.5% rise.

The other important Mexican news for markets over the weekend, was the nomination of Jose Gabriel Cuadra to Banxico’s board, replacing Irene Espinosa whose term ended December. Irene was arguably the most hawkish member on Banxico’s board. Cuadra’s appointment needs to be approved by the Senate, where the government has an overwhelming majority. Cuadra is a career central bank whose latest role was as Director in Banxico’s Economic Studies Department. He holds a BSc in Economics from ITAM, a PhD in Economics from Rochester, and can be described as a career central banker. The nomination of a career Banxico civil servant is a good signal of respect for Banxico’s independence from the new President, and should, at least on the margin, help local sentiment.

Even with the strong reaction we’ve seen by MXN to the tariff announcement, we would argue that at most 50% of the tariff’s impact has been absorbed by the peso. Hence, we would either expect material additional MXN weakness if the tariffs come into effect and prove long lasting, or alternatively, if the peso holds it ground, the bulk of the tariffs will become a competitiveness shock for Mexican exports that likely tips Mexico into recession. Now that Mexico has reached an agreement to postpone tariffs for one month, it is very likely that Banxico will be encouraged to cut 50 basis points on Thursday, February 6th.

—Eduardo Suárez & Rodolfo Mitchell

CHILE: GDP EXPANDED 6.6% Y/Y IN DECEMBER (2.5% IN 2024)

- Calendar effects explained almost half of year-on-year GDP growth. Non-mining activity continues to show genuine recovery.

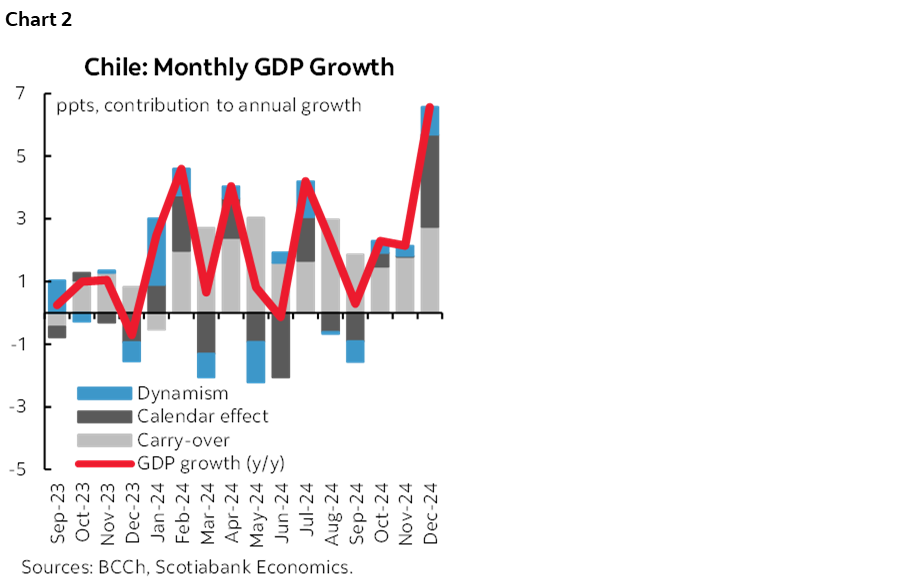

On Monday, February 3rd, the Central Bank (BCCh) released December GDP data that showed a 6.6% y/y expansion, surprising market expectations (Economists’ Survey: 2.7%) and our own (Scotia: 3.7%), largely due to a relevant seasonal effect derived from the existence of two additional working days with respect to December 2023. Although the monthly GDP expansion surprised to the upside (0.9% m/m), the growth was explained by the strong calendar effect, which contributed close to 3 ppts of the year-on-year GDP growth rise. With this, 2024 would have ended with 2.5% growth, higher than the 2.3% projected by the Central Bank in the December IPoM.

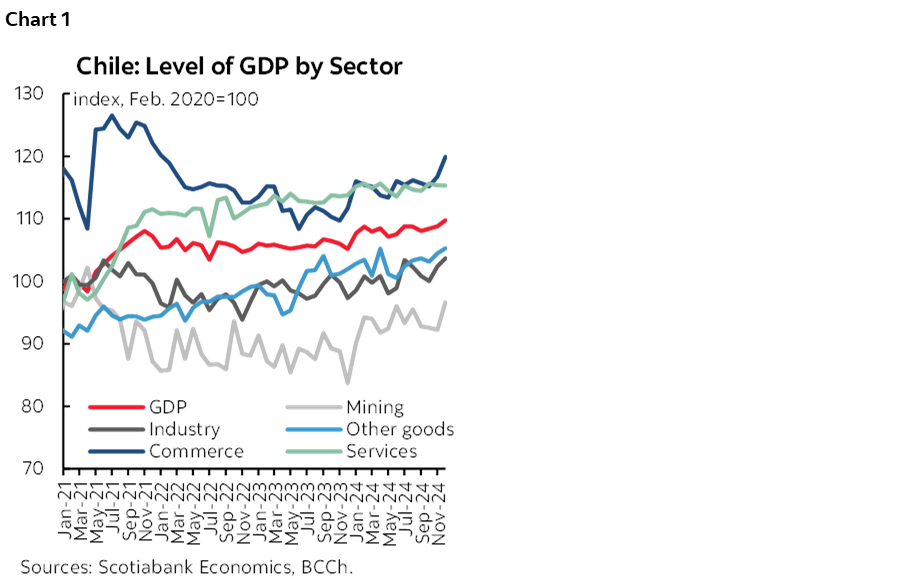

There has been an outstanding performance of commerce, for the second consecutive month (chart 1). The sector grew 2.7% m/m (seasonally adjusted), reaching the highest level of activity in almost three years thanks to the wholesale and automotive sectors, according to the BCCh. However, at Scotiabank we estimate that the contribution of tourism would also be relevant in the year-end activity figures, especially due to the entry of Argentine tourists, which has become more evident in recent weeks. Based on figures from Sernatur, we estimate that a third of the expenditure made by Argentine tourists in Chile (around USD 500 per visit) is destined to the commerce sector, which would have had an important impact on the year-on-year growth of the sector in recent months. Preliminary figures for January would be even more positive, approaching levels not seen since the boom in Argentine tourist arrivals between 2016 and 2018.

Services continue to show poor performance, registering zero monthly growth for the month. Excluding strong January 2024 growth, services virtually remained stagnant for the rest of 2024. Part of this dynamic would have been explained by a slow execution of private investment throughout the year, as well as a slowdown in the growth rate of public investment in the second part of 2024 due to necessary budget cuts that also affected investment.

The seasonal factor of non-mining GDP was surprisingly high. Beyond the two additional working days that this month of December had over the previous year, 21 working days in total, the seasonal factor was surprisingly high, the highest recorded for the month, even in years when we had 22 working days. In 2024, the influence of the seasonal factor or calendar effect on GDP was particularly higher than in other years, given the leap year, the composition of the calendar in some months and some weather events. December’s GDP was no different in terms of the influence of the calendar effect, registering a strong surprise that this time contributed positively to the activity record (chart 2).

The carry-over for the year 2025 remains at 1.4%. Given that the surprise occurred mainly in the seasonal factor and not in the seasonally adjusted series, the carryover for the year 2025 remains at 1.4%. That is, in the event that monthly GDP growth was zero in all months of the year, GDP would reach a rate of 1.4% in 2025. Although December GDP showed a strong expansion, partly explained by the positive calendar effect, a real surprise was observed in some sectors, especially in trade and mining. This can be seen when looking at the seasonally adjusted GDP annual growth rate, which was 4.3% and shows a relevant acceleration since October. At Scotiabank, we continue to project a GDP expansion of 2.5% in 2025, partly thanks to strong investment growth.

UNEMPLOYMENT RATE DROPS TO 8.1% IN DECEMBER, WITH LOW PARTICIPATION AND JOB CREATION

- Job creation continues to worsen its performance, marking historic lows for the month

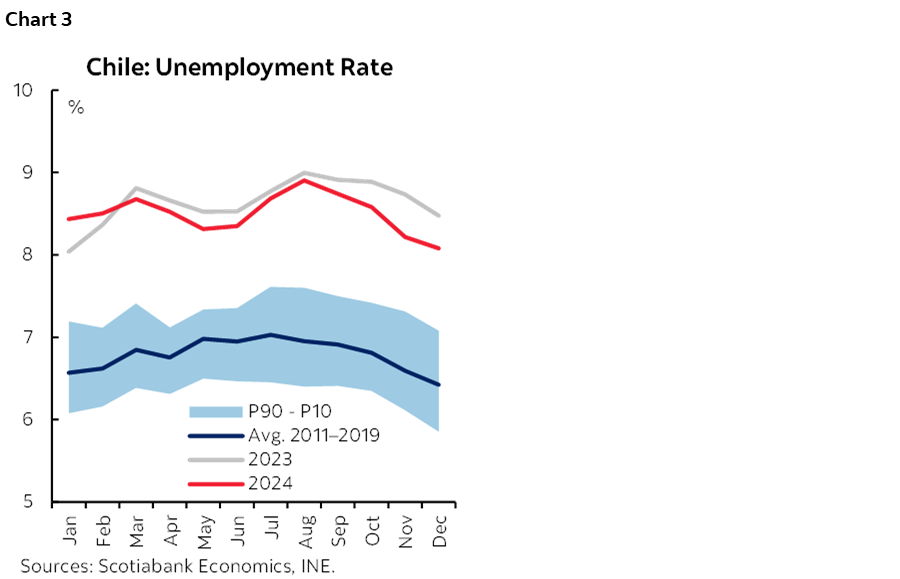

The labour market continues to show marked weakness, with minimal job creation, mainly due to seasonal reasons. On Friday, January 31st, INE published unemployment rate data for the quarter ending in December, that showed a decline to 8.1% (chart 3), a figure that disappointed market expectations (8%) and does not change the diagnosis of a very weak labour market. On the other hand, only 20k jobs were created at the national level, marking a historic low for the quarter. This figure is composed of the creation of 64k formal jobs, concentrated in the agricultural sector, and the destruction of 44k informal jobs. Although the unemployment rate continues to decline, this is partly explained by the slow growth of the labour force in recent quarters. There is still a risk of observing higher unemployment rates in the coming quarters, as the increase in the population outside the labour force continues to be associated with potentially active people for educational reasons (that would eventually join the labour force).

The seasonally adjusted unemployment rate increased after three consecutive quarters of declines. In seasonally adjusted terms, the diagnosis is even more negative, with an increase in the unemployment rate to 8.5% and a destruction of 34k total jobs, being the largest drop observed since May 2021.

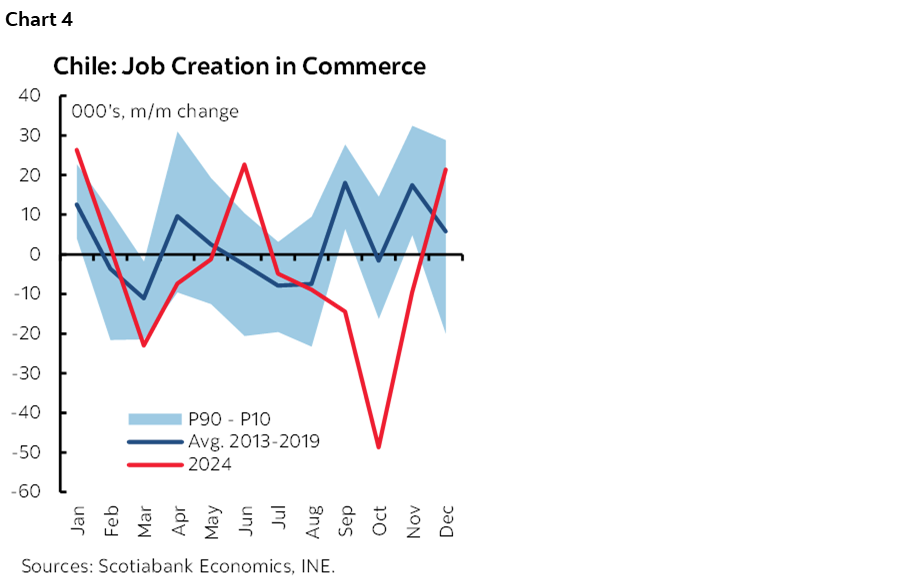

There is sectoral heterogeneity in job creation, although it’s explained by seasonal factors. Although the agriculture sector led in terms of job creation, in seasonally adjusted terms the increase was lower than usual, as were some service sectors. On the other hand, commerce and public administration led in terms of job creation, which grew more than seasonally in both sectors. With this, commerce is recovering after several months of strong job destruction (chart 4). Job creation in this sector reached 21k jobs, leaving behind three months with a sharp drop in its employment level. Although this is positive and contributes to an incipient recovery, the level of employment in the sector remains well below its trend.

—Aníbal Alarcón

COLOMBIA: IN DECEMBER, THE UNEMPLOYMENT RATE IMPROVED, WHILE IN 2024 LABOUR FORCE PARTICIPATION DECREASED

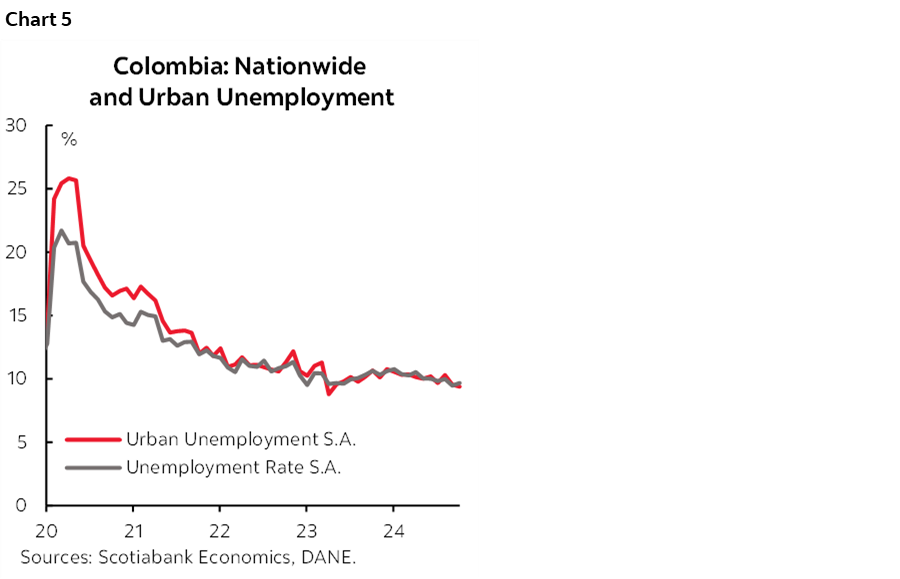

On January 31st, DANE published labour market data for December 2024. The national unemployment rate stood at 9.1%, decreasing 0.9 ppts compared to 10.0% in December 2023. The urban unemployment rate decreased 1.2 ppts to 9.0% compared to 10.2% in December 2023. Seasonally adjusted, the national unemployment rate increased to 9.7% from the previous month, however, it remains below the level from one year ago, 10.6%, while the urban unemployment rate decreased 0.2 ppts from November 2023 to 9.4% (chart 5).

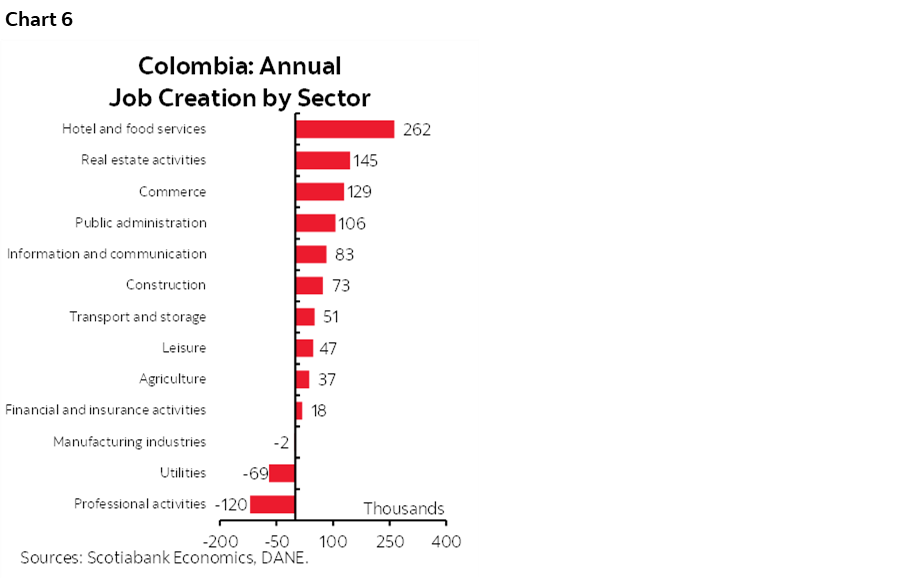

Job creation in some sectors has slowed compared to one year ago, while in others, it is starting to reflect a potentially better business perspective. In December, +756 thousand jobs were created, mainly concentrated in hotel and food services (+262 thousand), real estate (+145 thousand), commerce (+129 thousand), and public administration (+106 thousand), offset by professional activities (-120 thousand), utilities (-69 thousand) and manufacturing industries (-2 thousand). The improvement in employment in sectors such as commerce and construction reflect a recovery of some job losses one year ago, but also would suggest a better economic growth perspective (chart 6).

If we take a three-month moving average of job creation, we can see a slowdown. In the October to December 2023 quarter, job creation averaged 524 thousand, compared to 496 thousand in the October to December 2024 quarter, reflecting that job creation is slowing down—though increasing, at the margin, compared to the 279 thousand created in the September to November 2024 quarter.

On a seasonally adjusted basis, unemployment worsened compared to the previous month. The unemployment rate for the country increased to 9.7% in December, in contrast, in urban areas, it decreased from 9.6% in November to 9.4% in December. At this point, the number of people outside the labour market has increased by more than 290 thousand people so far in 2024, which could be related to the historical inflow of remittances (+17% between Jan–Sept 2024), discouraging labour participation, especially in the female population.

Employment registered a slight acceleration in sectors such as manufacturing and construction. However, we continue to believe that these activities still need a stronger boost to reach pre-pandemic levels, as high interest rates and the lack of investment continue to hinder greater dynamism, emphasizing that these activities contribute to the entire production chain in Colombia.

All in all, these data suggest that employment creation remains weak but shows that the composition is changing. The sectors that led economic activity during 2024 are now losing steam, while some sectors that are starting to show stability in their production dynamic are now showing better job creation. Friday’s data supports our call for a 25bps rate cut at the next Banco de la República meeting after maintaining the 9.50% rate at the January meeting. Economic activity is still operating in a negative output gap and despite the unemployment rate being under control, its composition suggests it needs a better impulse. However, the board will continue to be cautious due to the international and domestic uncertainty around fiscal accounts, which prevents the board from taking more significant steps in the cutting cycle.

Key information on employment data:

- In December, +756 thousand jobs were created, with 10 of the 13 economic sectors recording positive changes. Job creation was concentrated in hotel and food services (+262 thousand), real estate activities (+145 thousand) and commerce (+129 thousand). In the services sector, public administration recovered its employment levels (+106 thousand) and leisure continued with an acceleration in job creation (+47 thousand). In contrast, the decline in professional activities (-120 thousand) responds to the expiration of employment contracts that had been executed in 2023, utilities (-69 thousand), and manufacturing industries (-2 thousand) also registered a contraction in employment levels. The slowdown in job creation in the agricultural sector (+37 thousand) is a response to high employment growth in 2023 due to better climate conditions, and its contribution has been more than 50% to Colombia’s economic growth.

- Informality increased in December. The informality rate increased slightly compared to the same period of the previous year, from 56.3% to 56.8%, indicating a weaker performance domestically. The quality of employment in urban areas has deteriorated, with the informality rate rising from 41.6% in December 2023 to 42.3% in December 2024.

- The female population has created more jobs in this period. In December, men created +329 thousand new jobs, of which +366 thousand were in self-employed workers and +67 thousand were in domestic activities and day labourers, offset by the destruction of 103 thousand jobs in employers and the private sector. The female population created +427 thousand jobs, of which +286 thousand were in self-employed workers, +197 thousand in the private sector and +60 thousand in domestic activities and day labourers, offset by the loss in employer work, public employee and unpaid domestic workers (-111 thousand).

- For 2024, the Colombian unemployment rate stood at 10.2%, the same as last year. Throughout the year, the economy created +240 thousand jobs but registered a drop in the employment rate from 57.6% in 2023 to 57.4% in 2024. This responds to an increase in the number of people outside the labour market (+297 thousand) reflected in a decrease in the labour participation rate from 64.1% in 2023 to 63.9% in 2024. For 2025, we expect a restructuring of the labour market with improvements in the labour participation rate. The balance will depend on the capacity of the labour market to absorb the new labour force that will be incorporated in 2025, highlighting the loss of momentum in public employment creation.

—Valentina Guio

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.