- Mexico: Inflation accelerates in H1-Feb

Markets have a strange feel to them this morning. Trump saying yesterday afternoon that “tariffs are going forward on time” (when asked about those on Canada and Mexico) alongside reports that the US is eyeing stricter controls on China’s weighed heavily on equities in Asia, dragging the main Chinese, Japanese, and HK indices by about 1–1.5%. But, European indices are tracking ~0.5% gains in Euro Stoxx and FTSE and US equity futures are broadly unchanged though with a continued underperformance of Nasdaq (which lost 1.2% yesterday). Oil and gold are about half a percentage point lower, while copper and iron ore are rising about the same amount. In the FX world, the CAD and MXN are flat on the day (though this comes after late-session declines, especially in the former), while the AUD and NZD’s small 0.2% losses today don’t suggest there was a big risk-off mood in APac. The EUR and GBP are rising a touch (0.3%), where another decent leg lower in US yields is helping the currencies on rate differentials narrowing. US 2s are down by 6bps and 10s are down by 8bps, compared to 5bps for each in the UK and 2bps for each in Germany.

Though that’s another interesting move in markets. Equities sold off in Asia on tariff fears, but these tariff fears were not reflected in inflationary expectations via higher US yields? Maybe we’re just reading too much into things, and Trump’s media Q&A yesterday (alongside French PM Macron) was kind of all over the place—and there was a chance that he was talking about tariffs more broadly, specifically the reciprocal tariffs that are being studied.

In European hours, German Q4 GDP was held at -0.2% q/q as in the preliminary reading, but accompanied by a mixed mix across the consumption categories; private spending disappointed with much lower growth (0.1% vs 0.4% median), but investment surprised with a 0.4% expansion against a half-ppt expected drop, with government spending growing by 0.4% also. On that final note, Germany’s incoming chancellor Merz is reportedly in talks with would-be coalition allies to ramp up defense spending, a move that would add to the importance of the public sector to drive the economy and likely weigh on German debt. The ECB also published Q4-24 negotiated wage rates data that showed a 4.1% y/y expansion, down from the 5.4% record in Q3, to slightly add to the case for ECB cuts (though the ECB already anticipated a decent deceleration).

Trump news aside, overnight markets had limited information to trade on (German and ECB data didn’t really move the needle), as we head into another quiet morning that is relatively bare of on-calendar risks in the G10 and Latam while we monitor geopolitical developments for episodes of trading volatility (Trump and tariffs, Ukraine-Russia peace talks). The results to the US Conference Board’s consumer survey are on tap at 10ET, with a focus on inflation expectations and/or the possible impact of Trump policy on household sentiment (see last Friday’s poor U Michigan numbers). In Mexico, Q4 current account data out just now are not moving markets or macro expectations (as per usual, and despite a nice upside surprise at USD12.6bn vs USD9.2bn) but we are keeping track of these figures for foreign investment trends considering Trump risks.

—Juan Manuel Herrera

MEXICO: INFLATION ACCELERATES IN H1-FEB

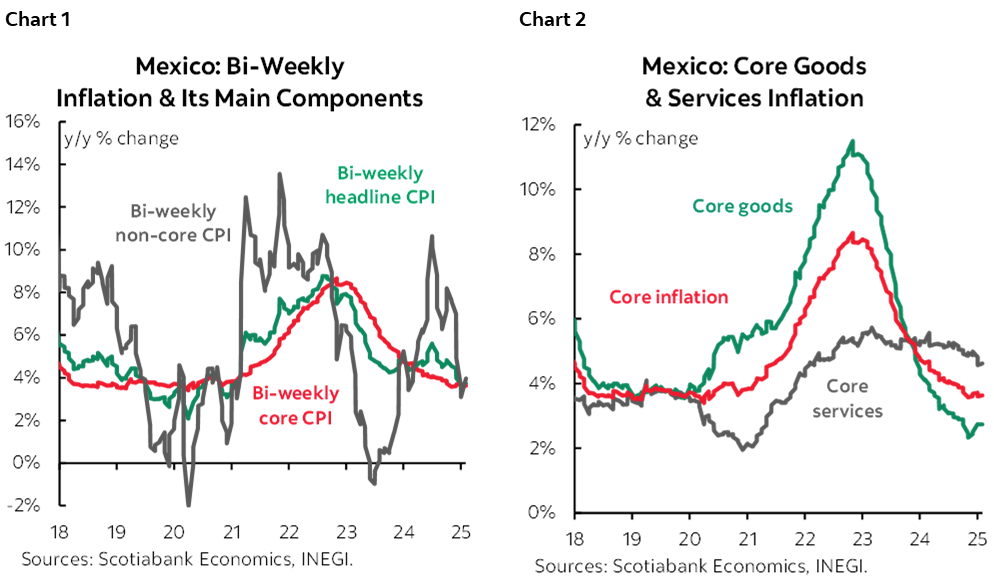

Inflation in the first half of February accelerated less than expected, reaching 3.74% from 3.48% (vs. 3.76% consensus in the Citi Survey). However, core inflation slightly increased to 3.63% from 3.61% previously (vs. 3.62% consensus) (chart 1). Within this, goods remained at 2.74%, while services rose to 4.62% (4.57% previously) (chart 2). On the other hand, non-core inflation jumped to 3.98% (3.09% previously), with agricultural products increasing to 3.31% (0.05% previously) and energy and government tariffs at 3.89%. Sequentially, general inflation rose to 0.15% w/w (0.12% previously, 0.17% consensus in the Citi Survey), core inflation increased to 0.27% w/w (0.22% previously, 0.25% consensus), and non-core inflation fell to -0.25% (-0.17% previously). Looking ahead, we consider that inflationary risks remain skewed to the upside. We highlight the potential impact of tariff measures between Mexico and the U.S., as well as possible price pass-through due to further depreciation. Additionally, there could be a significant rebound in the non-core component due to climatic events in the coming months.

—Rodolfo Mitchell, Brian Pérez & Miguel Saldaña

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.