- Mexico: Weak end to the year for commercial activity; Banxico minutes reinforce expectation for an additional 50bps cut

Global markets are trading with a slightly negative tone this morning as comments by Trump on tariffs and geopolitics weigh somewhat on equity markets that, despite all the noise from the White House, are still reaching new highs in the US every couple of days. Outside of strong jobs data out of Australia (with no massively oversized impact on local assets), the overnight session was quiet on the data releases front. This morning, US jobless claims figures were practically in line with expectations—and not yet showing a clear impact of US government job cuts—while Mexican retail sales (see below) came in better than expected with a surprise month-on-month rise and positive revisions to November, and Banxico’s meeting minutes (see below also) were broadly in line with what the policy statement had guided as well as comments by officials in the days after the meeting. Walmart’s disappointing profit forecasts amid economic uncertainty is heavily dragging on the retailer’s share price, down about 6% on the day. The day ahead is quiet in Latam and the G10 aside from some Fed speakers and whatever pops up on Truth Social by Trump, with global markets looking ahead to tomorrow’s PMIs flood. In Mexico, we’re keeping an eye on what emerges from Econ Minister Ebrard’s meeting with US Comm Sec Lutnick today, with less than two weeks away from the one-month tariffs ‘pause’ lapsing. Initial comments by Mexico’s representative suggest little came out of the meeting, while he indicated that US-Mexico joint work begins on Monday.

After chunky losses of ~1.0–1.5% in Hong Kong and Tokyo indices and Euro Stoxx and FTSE trading 0.5% gains and drops, respectively, SPX and Nasdaq opened with small ~0.2% declines on the day, but the equity mood worsened soon after the open (on nothing obvious) to leave the main US indices down about 1% on average. The rates mood is mixed as US yields drop about 1bp in the front-end to 2/3bps in the long-end with no major drivers but chopping around the release of US data and Trump calling for balancing the US budget. European yields are little changed in the UK but richer in bull steepening fashion in Germany and France (2s down 3/4bps, 10s down 2bps), and Japanese rates closed a touch cheaper as domestic markets await CPI data on Friday morning (local time, 19.30ET Thursday). The USD is broadly weaker where the JPY is tracking a 1.3% rise thanks to BoJ hike expectations and the lower US yield environment, while high-beta FX like AUD and NZD rise ~1%, the MXN sits around the middle of the leaderboard 0.6% higher, and key FX like the EUR, CAD, and GBP similar gains.

—Juan Manuel Herrera

MEXICO: WEAK END TO THE YEAR FOR COMMERCIAL ACTIVITY

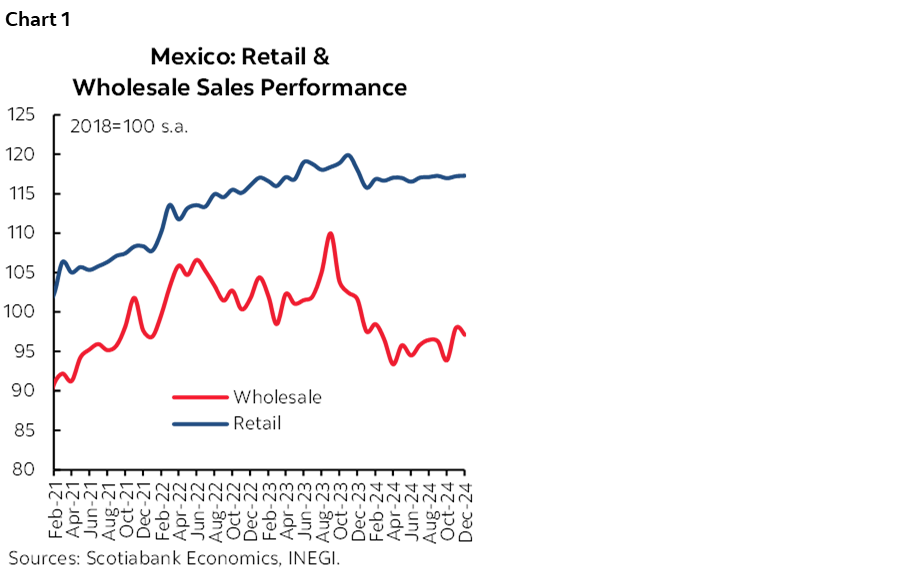

In December, retail sales fell by -0.2% y/y, compared to -1.9% y/y previously, marking the eighth consecutive month of decline. By components, there was a significant increase in grocery and tobacco trade at 9.3% (1.8% previously), textiles rose by 2.4% (0.1% previously), while the most significant decline was in recreation at -3.0% (-4.0% previously), and hardware items at -2.9% (-8.4% previously), among others. On a monthly comparison, retail sales increased by 0.1%.

Wholesale trade experienced a decline of -3.4% y/y, from -5.0% previously, with five of its seven components being negative. The most important drop was in intermediation at -35.3% (-13.6% previously), while the largest increase was in trucks and auto parts at 18.4% (4.1% previously). Monthly, wholesale sales fell by -0.9%, from 4.4% previously.

These data indicate that the slowdown in retail sales continues across most components, which could be a positive indicator for inflation, particularly in goods. On the other hand, wholesale sales continue to decline, having experienced thirteen months of negative annual variations. In cumulative basis for 2024, retail sales fell by -0.6% y/y, while wholesale sales declined by -6.3% y/y.

BANXICO MINUTES REINFORCE EXPECTATION FOR AN ADDITIONAL 50BPS CUT

- The arguments of the Board members revolved around the deceleration process and the current level of inflation.

- The Governing Board members expect low economic activity in 2025.

- They noted that private consumption has moderated, and that investment remains weak.

- Several members highlighted that both headline and core inflation are close to their historical average from 2003–2019.

- We consider that there are increasing risks and greater uncertainty regarding the trade relationship between Mexico and the U.S. under the new Trump administration.

- At the next policy meeting, we expect that Banxico will opt for another 50 basis point cut.

- We anticipate that the reference interest rate will end the year at 8.50%, in line with the consensus of analysts.

Banxico published the minutes of the February 6th meeting, detailing the discussion on inflation and monetary policy within the Governing Board. The majority voted to cut the reference rate by 50 basis points to 9.50%. Deputy Governor Jonathan Heath voted for a 25 basis point cut. Overall, the arguments of the Board members focused on the process of decelerating inflation. Most members suggested repeating a cut of the same magnitude at the March meeting, while awaiting policy decisions in the international and domestic context.

Regarding the Mexican economy, comments highlighted economic weakness, with a GDP contraction of -0.6% quarter-on-quarter in Q4-2024. For the entire year, growth was lower than in 2023 (1.5% in 2024 vs. 3.3% in 2023). Services showed less dynamism compared to previous quarters, while industrial activity contracted due to weakness in manufacturing, construction, and mining. Primary activities also declined in Q4. Private consumption moderated due to lower consumption of domestic goods and services, as well as imported goods, although the latter remained at high levels. Additionally, most members noted a significant slowdown in investment, albeit with some dynamism in machinery and equipment. The Governing Board expects low economic activity growth (0.6% in 2025 and 1.2% in 2026), as it was published earlier in the Quarterly Inflation Report, due to uncertainty related to the Trump administration, particularly around potential tariffs on Mexican products and migration policy. Employment creation has slowed, although there has been no increase in the unemployment rate.

Global economic activity decreased in Q4-2024, which is lower than the rest of the year. Services drove growth, while manufacturing remained weak. In the United States, the economy remained strong due to robust private consumption, with a rebound in goods and a solid labour market. In developed economies, employment indicators showed a reduction in job vacancies and slight increases in real wages. The document also mentioned that the disinflationary process continued, despite persistent core inflation. In line with this, major central banks showed caution in reducing interest rates, while in Latin America, the process was faster, with significant interest rate cuts. Volatility persisted in international financial markets due to expectations of measures by the new U.S. administration, mainly tariff impositions.

Regarding inflation, there was consensus among members on the disinflationary process. Several members highlighted that in January, both headline inflation and core inflation were close to their historical average since the 3.0% target was adopted (2003–2019). However, several members noted the possibility of rigidities in core inflation. Additionally, one member highlighted the possibility that non-core inflation could be higher than estimated in the coming months, as it is highly volatile and currently well below its historical average. Most members recognized the risk associated with the new U.S. administration’s policies, with potential upward and downward effects on inflation. Several members mentioned the upward risk of tariff impositions and a higher USDMXN, but also a downward risk from lower-than-expected economic activity. We agree that tariff policies could have opposing effects, but we consider that the net effect would be inflationary, accompanied by a risk-averse sentiment in the economic environment due to increased uncertainty.

In the monetary policy discussion, the Governing Board was mostly in favour of maintaining the pace of 50 basis point cuts at the next meeting. It appears that most of the Board considers that, given the current level of inflation, close to its historical average, the disinflationary process is at a point that allows for a faster rate cut while remaining in restrictive territory, despite increased uncertainty and risks in the outlook. One member argued that “we should not get ahead of events and make decisions without knowing the facts,” as tariff implementation has not yet occurred. Another member mentioned that economic activity could be lower than anticipated, contributing to inflation converging to the target. However, they considered that potential trade and migration disruptions present additional challenges, and their impacts on inflation will depend on the opposing effects of the exchange rate and economic dynamics, as well as the duration and magnitude of the shocks. Another member referred to the interest rate spread between Mexico and the United States, noting that both economies are at different stages, with the U.S. economy showing resilience while the Mexican economy is significantly sluggish. Additionally, they pointed out that the current differential is above the pre-pandemic average and what would be expected if both rates were in a neutral steady state. A fourth member highlighted that the risk balance is less adverse than in previous years, despite the risks, partly due to potential changes in trade policy, which they indicated could be addressed with a lower degree of restriction. Finally, we highlight the comments possibly made by Deputy Governor Heath, given his dissenting vote, where he expressed doubts about the continuation of the disinflationary process. He also stated that concerns about economic slowdown should be secondary given the primary mandate (of low and stable inflation), and that caution is needed in the face of risks and challenges in the outlook, considering that the rate differential is consistent with an environment of uncertainty and increased risk premiums. This week, the dovish stance remains as Governor Rodriguez Ceja mentioned in the Quarterly Inflation Report conference that the Board still considers another 50bps cut in the coming meeting.

Looking ahead, given the comments of the Governing Board, and the latest inflation print, we expect that the March meeting will repeat a 50 basis point cut in the benchmark rate to 9.00%. However, due to the uncertain environment, a balance of risks biased upwards, and a more restrictive stance from the Federal Reserve, we consider that the interest rate will remain in restrictive territory at the end of the year, at 8.50%, which implies that after the March meeting it could follow lower cuts and pauses in the cutting cycle.

—Rodolfo Mitchell, Brian Pérez & Miguel Saldaña

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.