- Peru: The buoyant Peruvian economy—expected to grow 4% in the first quarter after strong end to 2024.

PERU: THE BUOYANT PERUVIAN ECONOMY—EXPECTED TO GROW 4% IN THE FIRST QUARTER

Peru’s GDP grew 3.3% in 2024, above our 3.0% forecast and the official 3.1% target. Economic activity followed an uptrend throughout 2024 (chart 1), posting a strong 4.2% expansion in Q4-2024.

In December alone, Peru’s GDP grew 4.9%, its fastest expansion in the last eight months. Growth was led by the fishing and primary manufacturing sectors, boosted by a successful second anchovy fishing season. Together, these sectors contributed 1.2 percentage points (ppts) to the month’s result. Additionally, the sustained recovery of non-primary sectors linked to domestic demand, such as commerce and services, also played a role.

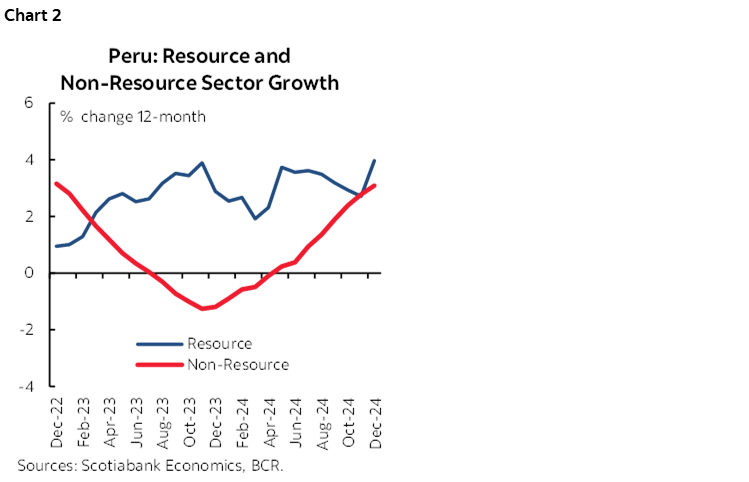

In January 2025, Peru’s GDP is estimated to have grown around 4%, with the fishing sector contributing positively but at a slower pace than in November and December 2024. Growth in February should slow due to a base effect—2024 was a leap year—and because fishing will no longer add to growth following the end of the second anchovy season. In March, GDP could grow above 4% due to a calendar effect—Easter week in 2024 fell in March (two fewer working days), whereas this year it will be in April (chart 2).

STRONG END TO 2024

Economic activity in December was driven by the strength of primary sectors. Fishing GDP (+76.7%) benefited from favourable oceanographic conditions that enabled a strong anchovy catch: 928K metric tons vs. 153K in December 2023—when landings were affected by El Niño. This also had a positive impact on the fishmeal industry and, in turn, on resources manufacturing (+37.5%).

The agricultural and livestock sector (+7.5%) was boosted by the strong performance of the agricultural subsector (+10.8%), which posted double-digit growth for the third consecutive month. Notably, higher harvests of export-oriented crops—such as mangoes, grapes, blueberries, and asparagus—as well as domestically consumed crops like potatoes and tomatoes, contributed to growth. Meanwhile, the livestock subsector (+2.7%) was driven by higher poultry production.

The mining and hydrocarbons sector (+2.0%) rebounded after two consecutive months of contraction, supported by higher production of molybdenum, copper, and silver due to increased processing volumes and higher ore grades. This was partially offset by lower zinc and tin output. Meanwhile, the hydrocarbons subsector (+1.5%) saw mixed results, with higher natural gas liquids production, stable oil output, and a decline in natural gas production.

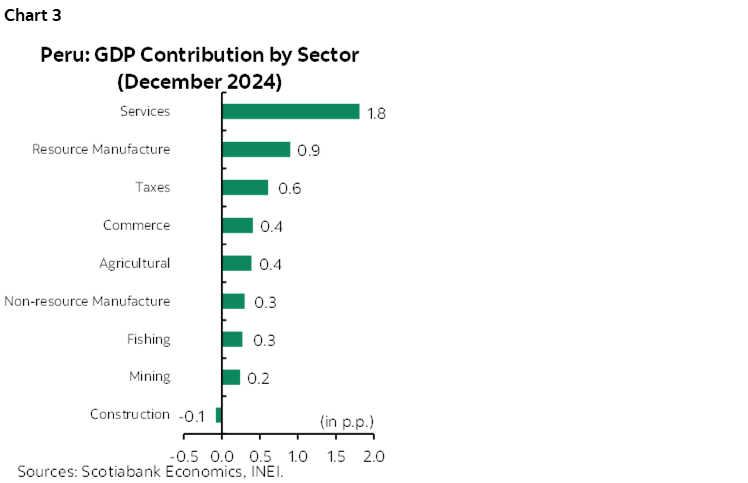

Among non-resources sectors, services (+4.0%) stood out, supported by recovering domestic demand. At a disaggregated level, transportation (+7.3%) benefited from increased passenger flows due to the holiday season and higher cargo movement as economic activity picked up. The hotels and restaurants sector (+4.5%) was driven by stronger domestic and inbound tourism, as well as higher dining out amid increased incomes from year-end bonuses. Other services (+4.7%) grew on the back of stronger demand for personal and real estate services (chart 3).

The commerce sector (+3.6%) was supported by improving employment conditions—formal private employment rose 6.3% YoY in December—and higher purchasing power, driven by rising wages and declining inflation. Retail sales performed well, especially in technology —hardware and software—supermarkets, and department stores.

Non-primary manufacturing (+3.4%) posted positive results led by higher consumer goods production. Notably, the beverage, pharmaceutical, furniture, and apparel industries benefited from accelerating private consumption. This was partially offset by lower intermediate goods production, with declines in the metal products, printing, and wood industries.

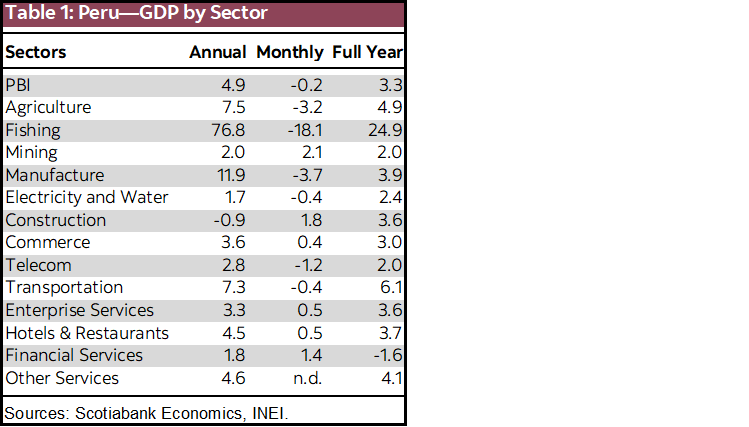

Finally, construction (-0.9%) was the only sector to post a decline in December. Public investment, measured through the Physical Progress of Works Index (IAFO, -2.1%), recorded its second negative monthly performance of 2024 due to slower execution by local and regional governments. Meanwhile, domestic cement consumption (+0.5%) remained stagnant, although we expect a gradual acceleration in 2025 driven by a recovery in self-construction (table 1).

—Pablo Nano

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.