- Peru: Sustained expansion in new vehicle sales—July marks another high

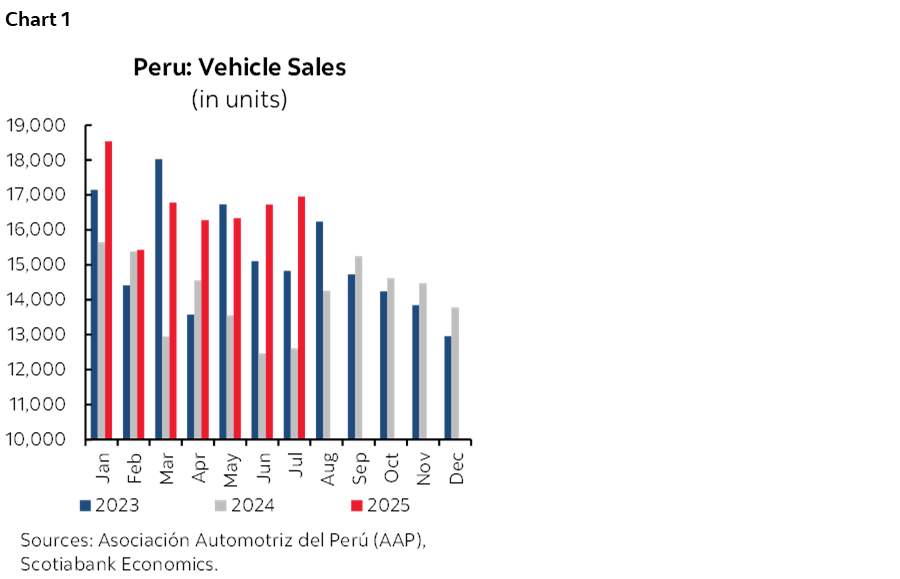

New vehicle sales once again exceeded our projections in July, with growth reaching nearly 35% y/y. This marks the eleventh consecutive month of expansion since September 2024, underscoring the sustained momentum in the automotive market. Notably, July’s annual growth rate was the highest recorded since July 2021, and the month registered the second-highest sales volume of the year. Both light and heavy-duty vehicle segments have maintained a steady uptrend in recent months, reflecting broad-based strength across the industry (chart 1).

This sustained momentum can be attributed to several key factors. First, real income levels have improved, supported by rising formal employment and easing inflationary pressures. Additionally, the appreciation of the Peruvian sol against the U.S. dollar has led to a more favourable exchange rate, enhancing consumer purchasing power. Market dynamics have also benefited from a broader availability of vehicle models—particularly those of Chinese origin—and more accessible credit conditions. Furthermore, demand for heavy vehicles has increased, driven by private sector investment, especially from construction and mining firms. The bus segment has also seen a notable rise in demand, primarily from private transportation companies.

2025 Outlook

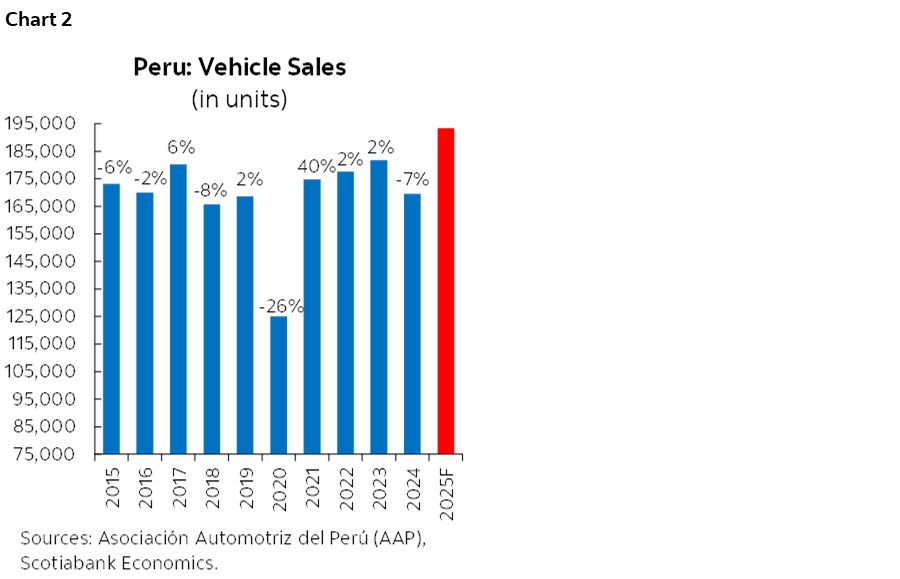

By year-end 2025, we anticipate the automotive sector will expand by approximately 15%, outperforming our initial forecasts and significantly exceeding the projected 3.2% growth for the broader commerce sector. We expect this uptrend in vehicle sales to persist through mid-August, following a period of negative annual variation between May and August 2024. However, growth is likely to moderate in the final quarter, partly due to the onset of the 2026 election cycle.

Our year-end projection is underpinned by several structural drivers. The continued improvement in formal private employment is expected to support demand for light vehicles, while the appreciation of the Peruvian sol against the U.S. dollar has contributed to a more favourable exchange rate environment. Enhanced business sentiment, linked to stronger private investment performance, is also expected to boost demand for heavy vehicles.

Additional tailwinds include relative price stability—supporting real income growth—a lower average cost of imported vehicles due to currency appreciation, improved vehicle financing conditions through reduced credit rates, and a broader range of available models, particularly in the light SUV segment. While the sector’s outlook remains positive, several factors could temper growth in the coming months. The approaching 2026 election season may introduce political uncertainty, potentially weaken consumer confidence and slowing sales momentum toward the end of 2025. Additionally, evolving global trade dynamics—particularly shifts in tariff policies—could disrupt supply chains and affect vehicle availability and pricing (chart 2).

Market performance as of July 2025

From January to July 2025, new vehicle sales totaled 117,029 units, marking a 21% increase compared to the same period in 2024, according to the Automotive Association of Peru-Asociación Automotriz del Perú (AAP). July recorded the second-highest monthly sales volume of the year (after January).

Light vehicle sales reached 103,689 units, up nearly 20% to July, while heavy vehicle sales rose to 13,240 units, a strong 29% increase. The expansion in light vehicle sales is largely driven by rising household purchasing power, supported by a steady recovery in formal private sector employment, which has been gaining traction since April 2024.

Within vehicle categories, SUV sales stood out with a 26% to July, reflecting strong consumer preference for high-capacity units—led by a Chinese brand. Pickup truck sales also rose sharply by 30%, driven by demand from the mining and construction sectors, where such vehicles are valued for their ability to navigate challenging terrain.

A notable trend is the sustained growth in SUV sales, which has been a key driver of the light vehicle segment. This category has shown consistent expansion since September 2024, mirroring the overall trajectory of light vehicle sales. Between January and July, SUVs accounted for 51% of total light vehicle sales, a significant increase compared to previous years (40% in 2021), underscoring a structural shift in consumer preferences.

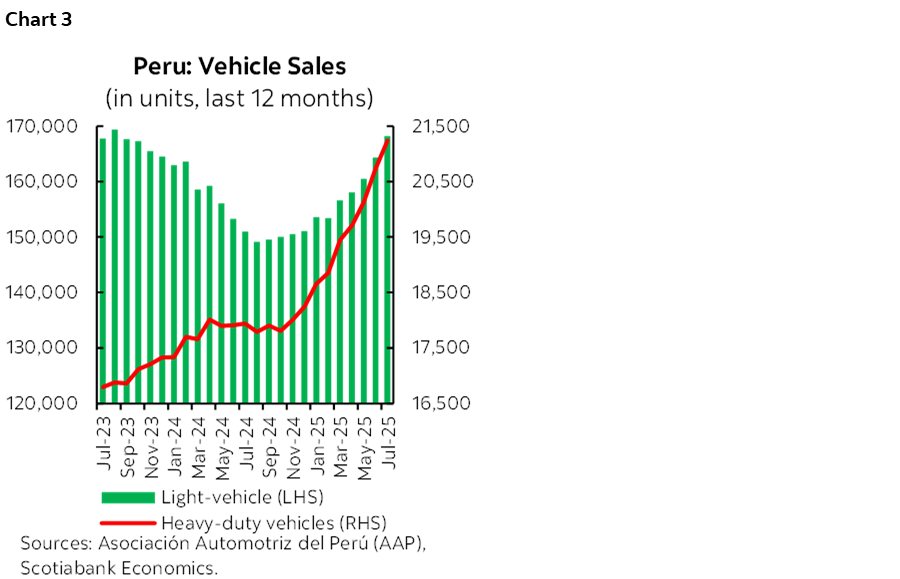

Heavy vehicle sales also posted strong gains, rising nearly 29% through July. This growth was fueled by increased demand for both trucks, particularly heavy-duty models—and buses. July’s performance in this segment was especially notable, marking the highest monthly sales since October 2013. Between January and July, heavy-duty truck sales rose by 27%, driven by operational needs in the mining, manufacturing, and construction sectors, in line with the broader trend of rising private investment. Bus sales surged by 37%, supported by increased orders from personnel transport and interprovincial transport companies, although growth momentum has moderated slightly compared to earlier months (chart 3).

—Carlos Asmat

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.