- Chile: June GDP of 3.1% y/y, consistent with 2025 GDP growth of 2.5%

- Colombia: A new strong print for Colombia’s labour market

CHILE: JUNE GDP OF 3.1% Y/Y, CONSISTENT WITH 2025 GDP GROWTH OF 2.5%

- Non-mining GDP reaches its highest level ever, while mining activity shows unusual volatility. The output gap, measured by GDP, is closing more rapidly, while the gap measured by the labour market is widening.

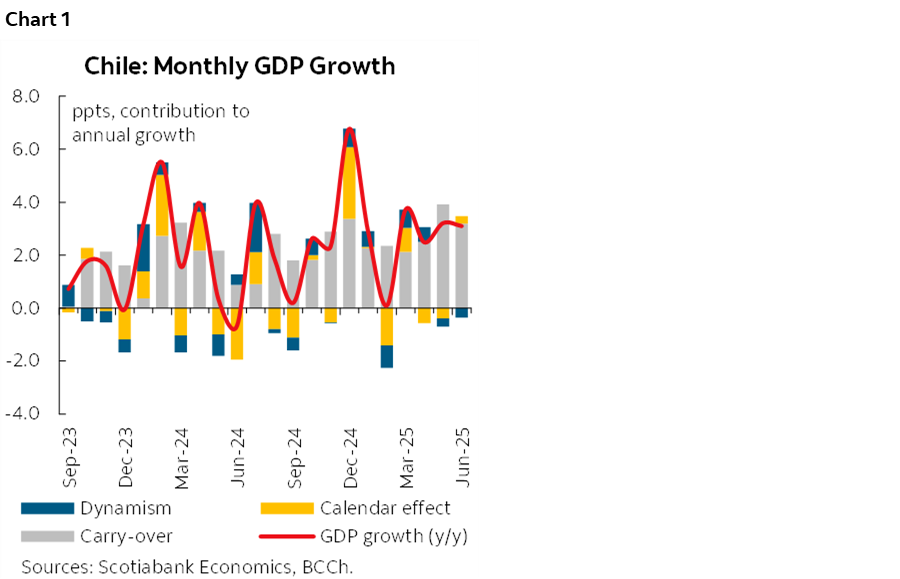

June GDP grew 3.1% y/y (chart 1), leading to a quarterly expansion of 2.9% y/y in Q2-25. The economy is clearly on track for a 2.5% GDP expansion for the year, similar to our baseline scenario. However, it is worth noting the volatility in the mining sector during the first half of the year, which was also evident in the sixth month of the year, and was responsible for the seasonally adjusted 0.4% m/m drop in overall GDP. Indeed, the non-mining GDP showed solid seasonally adjusted expansion of 0.8% m/m, reaching its highest level ever.

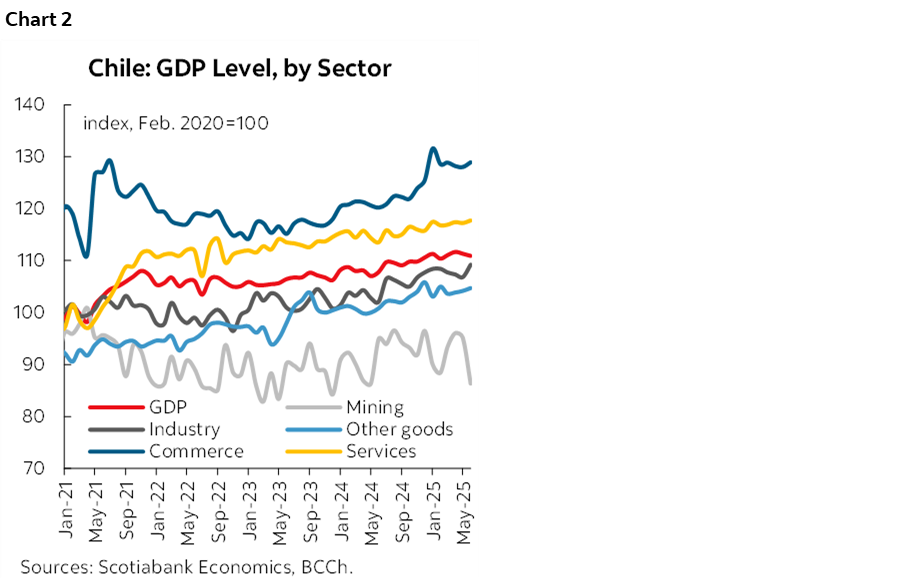

The positive performance across economic sectors was widespread (chart 2). Industry stood out, expanding 2.2% month-over-month, leaving behind three consecutive months of declines in economic activity. Behind this positive performance is primarily the food processing sector, especially fish processing, due to a greater quantity available for capture. This is how the industry reached its highest level of activity ever. A similar situation is observed in services. On the commerce side, after the significant impact of shopping tourism observed in the summer, which led to historically high levels of activity in the commerce sector, we see a particularly unexpected acceleration in the margin, this time driven by residents.

Mining showed its largest seasonally adjusted monthly decline in more than eight years, albeit due to specific factors that would reverse in the coming months, maintaining particularly high volatility in this sector. Mining GDP contracted 9.3% m/m in June, the largest drop since February 2017 (-9.9% m/m) when a strike at Escondida Mining lasted 43 days. This time, Escondida Mining again explained the contraction in mining production, but due to maintenance and, likely, the commercial strategy of the world’s largest mining operation at the end of its fiscal year. The impact on year-on-year growth in GDP was significant, subtracting approximately 1.2 ppts from the year-on-year growth rate. We estimate that mining production would have returned to normal levels in July, recovering much of what was lost in June, which would contribute at least 1 pp with the highest year-on-year GDP recorded in July. However, the volatility of the seasonally adjusted mining GDP series reached its highest level in the post-pandemic period, even higher than that seen last year after heavy rains caused flooding at some mining sites.

The output gap measured by GDP is expected to close rapidly (if not closed at the margin). The implication for monetary policy is one of additional caution in the face of a somewhat greater-than-expected acceleration in non-mining activity relative to the central bank’s baseline scenario. The non-mining output gap is closing somewhat faster than expected by the central bank. This may seem contradictory given that the quarterly growth of 2.9% y/y was below the 3.1% y/y implied by the central bank’s scenario. However, this is entirely due to mining, as we noted earlier. In this context, this recent activity figure injects an additional dose of caution into the cutback process, especially when non-mining activity is showing a widespread acceleration across sectors. Thus, for now, at Scotiabank, we reiterate our lower conviction regarding a further cut in the policy rate in September.

On the other hand, the capacity gap measured by the labour market sends a different message, given that the seasonally adjusted unemployment rate of 8.9% is markedly above the NAIRU (between 8.0% and 8.5%). The direct message from this perspective would be to continue cutting the policy rate. However, this lack of employment growth could be revealing a structural adjustment in the labour market, which is currently difficult for the BCCh to quantify. Ultimately, the economy is expected to show a significant increase in productivity in 2025 due to the reduction in hours worked, a decrease in employment, but historically high GDP levels.

—Aníbal Alarcón

COLOMBIA: A NEW STRONG PRINT FOR COLOMBIA’S LABOUR MARKET

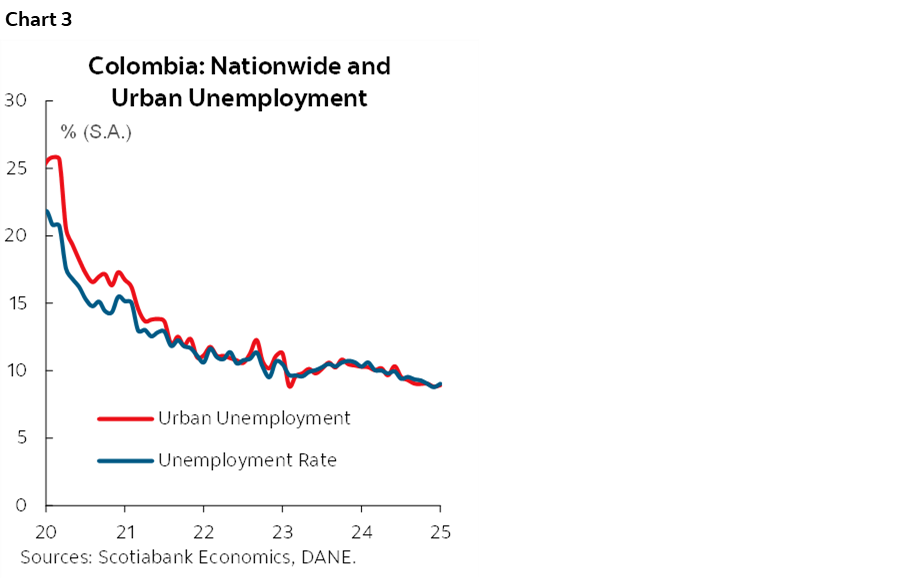

On July 31st, DANE published labour market data for June 2025. The national unemployment rate stood at 8.6%, decreasing by 1.7 percentage points compared to the 10.3% recorded in June 2024 and reaching the lowest unemployment rate since 2015. The urban unemployment rate decreased by 1.8 percentage points compared to June 2024, reaching 8.3%. Seasonally adjusted, the national unemployment rate fell slightly from 9.0% the previous month to 8.9%, and below the 10.6% level recorded a year earlier. Similarly, the urban unemployment rate fell to 8.4% from the 8.9% recorded in May (chart 3).

The recovery in economic activity continues to be reflected in increased job creation. However, we still observe a strong influence from public sector hiring on overall performance. In June, 831 thousand jobs were created, with 8 out of the 13 sectors reporting job growth. The most significant increases were seen in manufacturing, public administration, health and education, and utilities—together accounting for 84% of total job creation. By occupational category, the number of self-employed workers rose by 443 thousand, remaining notably high. However, part of this increase is linked to public sector hiring, which does not necessarily indicate a rise in informal employment.

Job creation remains robust. The three-month moving average in the original series for the April–June 2025 quarter was 713 thousand, higher than the 152 thousand created in the same period in 2024. The seasonally adjusted series shows a creation of +150 thousand jobs compared to May 2025, an increase in labour force participation to 64%, and a reduction of -46 thousand in the group of people outside the labour market. However, in urban areas, +59 thousand people left the labour market compared to May 2025.

Job creation is gaining momentum, though there is a noticeable gap between formal employment indicators and the grow of self-employment. In June 2025, self-employment increased by 443 thousand jobs, accounting for 40.8% of total employment growth. However, the informality rate declined from 56% to 55.1%, and one possible explanation is the rise in government contractors, who are classified as self-employed but formal. Looking ahead, it will be important to monitor the dynamics of the private sector in the labour market, as there are evident gaps in job creation in some sectors.

The average unemployment rate is expected to decline from 10.2% in 2024 to 9.7% in 2025, driven by a stronger increase in labour force participation and a faster pace of job creation. However, the possibility that unemployment could be lower cannot be ruled out, depending on the degree of absorption of new labour by the economy. The implementation of some aspects of the labour reform will also be a point of assessment in the coming months.

Employment data highlights:

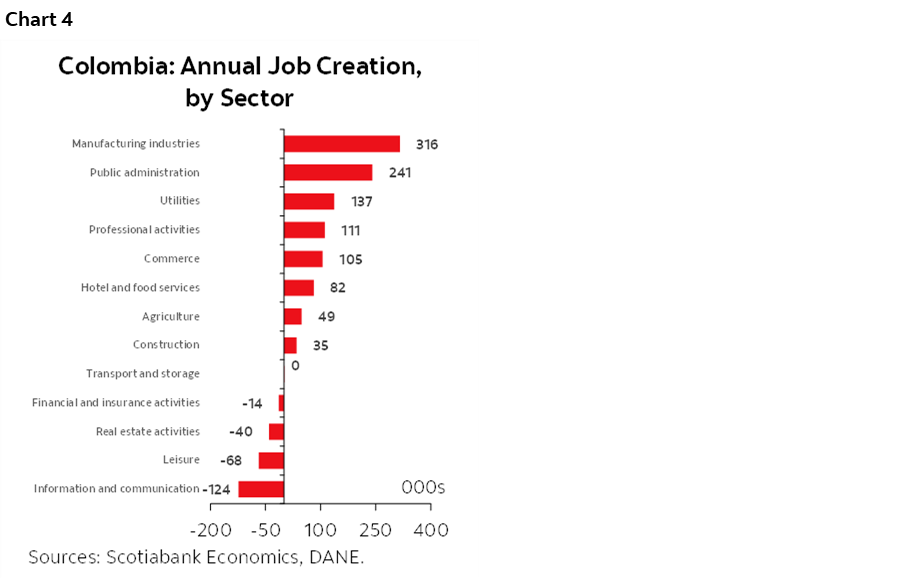

- In June, more than 831 thousand jobs were created, with 8 of the 13 economic sectors registering positive changes. Job creation was concentrated in the manufacturing industry (+316 thousand), public administration (+241 thousand), utilities (+137 thousand), and commerce (+106, thousand). In contrast, the decline in information and communications (-124 thousand) and leisure (-68 thousand) offset the overall result (chart 4).

- The informality rate decreased in June. The informality rate decreased significantly compared to the same period last year, falling from 56% to 55.1%, suggesting an improvement in domestic working conditions, likely driven by the growth in government contractor positions. In contrast, the quality of urban employment deteriorated, and the urban informality rate fell from 41.6% in June 2024 to 42.1% in June 2025.

- The gender gap narrowed, and the unemployment rate among women reached its lowest level. In June, the unemployment rate for women was 10.8% and that for men was 6.9%. Women gained +491 thousand jobs, of which about 50% were concentrated in the manufacturing sector with +242 thousand positions followed by public administration with +153 thousand jobs. Men gained +340 thousand jobs, of which +117 thousand were concentrated in utilities and +88 thousand in public administration.

—Jackeline Piraján & Daniela Silva

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.