- Colombia: BanRep Minutes—Volatile international conditions motivated the central bank to maintain a cautious approach; Exports closed the first quarter of 2024 in contraction

Tuesday’s rates selloff that kicked off as European markets closed continued through Asia hours, as heavy corporate issuance combines with the US’s 3/10/30s cycle to somewhat stall progress made post-Fed and NFP. European trading has a more positive to neutral attitude towards debt, setting aside EGBs and gilts opening weaker in catch-up moves to USTs. It is an extremely quiet hump day in the G10, following Sweden’s Riksbank’s expected 25bps cut but with relatively dovish guidance.

The USD is making the most out of yield moves with gains versus all majors except for the unchanged MXN, with a standout 0.5% drop in the JPY that nears the mid-155s. Currencies are failing to benefit from soft crude oil prices (Brent ad WTI down 1.5%) that have now fully erased the jump in Mar/Apr on geopolitical risks; iron ore and copper are also taking big hits of 3% and 2%, respectively. SPX futures are flat while Euro and UK cash indices track small increases.

In contrast to the quiet G10 calendar, Latam’s schedule has a couple of top tier items to follow. At 8ET, Chile publishes April CPI data that our team in Santiago expects will show a steady pace of monthly inflation at 0.4% m/m that would result in a 3.4% y/y reading (non-chained). According to our economists, roughly half of this overall prices increase will owe to energy/fuels prices , and they also projected that inflation ex. volatiles will make a strong move lower towards target; from 3.7% to 3.3% y/y thanks to easing services inflation. At yesterday’s close, local markets were pricing in about 40bps in cuts at the May meeting; an encouraging trend in core inflation and the CLP trading at its best levels since early-February may very well motivate a 50bps move.

At 17.30ET, the median economist and markets expect the BCB to cut 25bps after six consecutive and well-telegraphed 50bps moves. Expectations for today’s decision have swung around in recent weeks, as hawkish/cautious comments from policymakers (namely Gov Campos Neto), BRL weakness, and rising US yields challenged an improvement in inflation trends in recent prints after some uncomfortable readings at the start of the year. Economists are certainly not as convinced as markets, with a third of those polled by Bloomberg expecting a 50bps move while markets see only a 25bps cut today and less than one more across the following two meetings. The 25 or 50bps reduction will be the highlight, but guidance on future moves is also a major component of today’s decision.

—Juan Manuel Herrera

COLOMBIA: BANREP MINUTES—VOLATILE INTERNATIONAL CONDITIONS MOTIVATED THE CENTRAL BANK TO MAINTAIN A CAUTIOUS APPROACH

The central bank released minutes regarding April’s monetary policy meeting on Monday, May 6th. The economic diagnostic is very similar compared to the March meeting. However, this time, the majority group said that volatile international conditions affirmed the necessity to maintain a cautious approach. What is also important from the minutes is that, in any case, the majority group considers the 50 bps rate cut pace as “substantial” since it reduces the ex-ante real rate significantly, which, in our opinion, is pointing that, for now, there is not a big concern around the economic activity performance and that prevails the focus to take the inflation to the target by mid-2025. It is also important to highlight that most of the board is concerned about the fiscal situation. While at the same time, they dropped references to their concern about political risk.

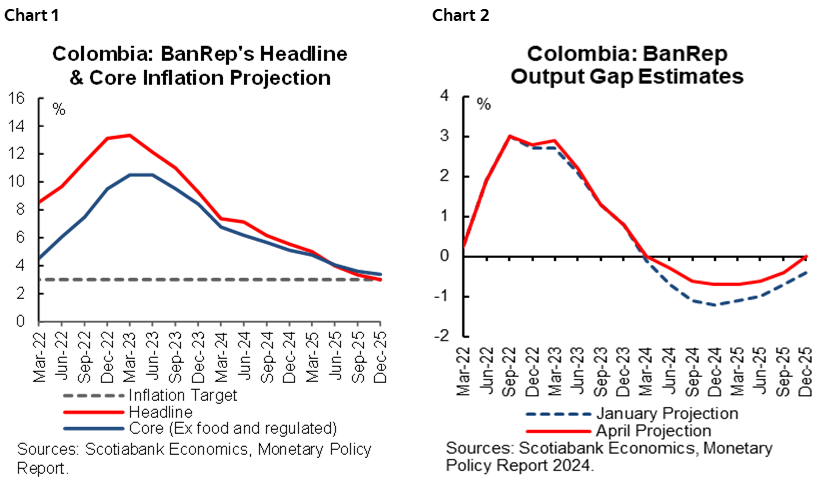

It is worth noting that on Friday, May 3rd, the central bank staff released the Monetary Policy Report, revising the downside inflation forecast and reducing their estimate for the output gap, which points that staff is also tilted to recommend cautious moves in the easing cycle as they said that inflation risk is still skewed to the upside. At the same time, the picture is more mixed in terms of growth. The central bank’s staff said that, on average, their estimated interest rate path is compatible with the convergence of the inflation to the target is higher than expected by market consensus.

The macroeconomic assessment from the central bank, board, and staff continues to favour a cautious approach, at least for the forthcoming meeting. We expect a 50 bps rate cut in the June 28th meeting, highlighting by this time, the board will have a couple of inflation readings, which probably will continue showing moderate progress towards lower levels, Q1-2024 GDP number (to be released on May 15th) showing a positive balance due to temporary factors but still weakness in key sectors. More importantly, the board will also know the decision of the Federal Reserve (June 12th), which could clarify somehow expected rate cuts. In our opinion, the above won’t be enough to trigger an immediate acceleration in the easing cycle, but at least it would put the discussion in the cards. For end-2024, we project an 8.25% monetary policy rate and 5.5% by mid-2025.

Further details about BanRep’s minutes:

- BanRep’s board recognized that inflation has made progress and that the uncertainty around the impact of the El Niño weather phenomenon on prices has been dissipated. They said that the job market is deteriorating as informality is increasing, while economic activity is weakening, especially in the manufacturing, commerce, and housing construction sectors, amid the context of high interest rates and other factors that deteriorate the investment environment. This time, the board wasn’t as explicit as in the previous minutes, but they probably referred to political issues when referring to the “other factors” that deteriorate investment.

- For the majority group, defending the anchoring of inflation expectations is the priority. This group, who voted for a 50bps, said they preferred not to surprise market expectations since it could motivate a reversal in anchoring inflation expectations and a negative impact on domestic assets, especially the FX market. This group is concerned about fiscal perspectives since widening the fiscal deficit could delay the inflation convergence toward its target.

- The board member who voted for a 75 bps cut said that accelerating the easing cycle won’t put the progress of inflation at risk. Instead, this member considers that it is more relevant to give positive signals to the investors and contribute to impulse economic growth.

- The board member who voted for a 100 bps (Finance Minister) said that the real monetary policy rate remains very restrictive and said that now the priority should be to impulse the economy, which in turn will contribute to strengthening public finances.

- In addition to the minutes, the Central Bank staff released the Monetary Policy Report on Friday, May 3rd. In the report, the technical staff said inflation had made higher-than-expected progress during Q1-2024. However, risks are tilted to the upside, especially due to uncertainty around geopolitical conflicts and their impact on international food prices, as well as climatic effects on the CPI basket. On the economic activity side, they highlighted that the activity started stronger than expected; however, in the medium term, risks are mixed and tend to be skewed to the downside. In any case, what caught our attention was that the staff now is estimating a less negative output gap, which, in fact, suggests there is less worry about cutting interest rates at the fastest pace. All in all, the central bank’s economic staff concluded that the interest rate path compatible with inflation achieving the 3% target by mid-2025 is, on average, above economists’ consensus. The previous assessment clearly signals that the staff is on the hawkish side.

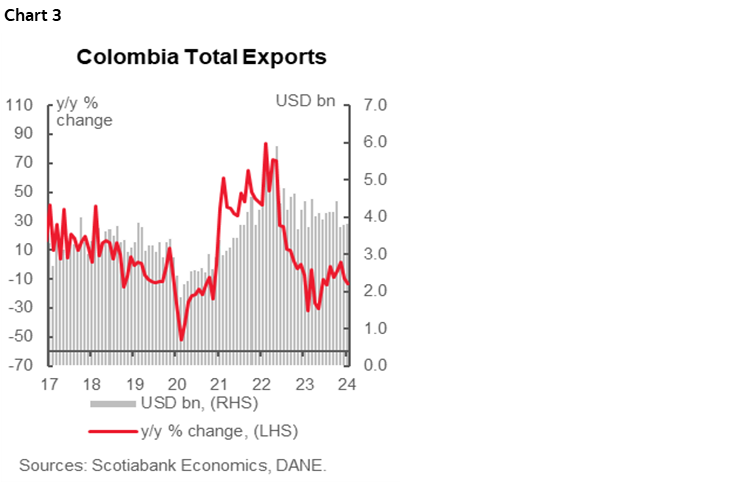

- About specific projections, BanRep’s staff projects inflation to close at 5.54% in 2024, while by the end of 2025, they expect to comply with the punctual target of 3% (chart 1), which is below market consensus projections of 3.90% according to the most recent survey. In the case of economic growth, Colombia is expected to expand by 1.4% in 2024, accelerating to 3.2% in 2025, which, on average, means a 0.7 % negative output gap (chart 2), which is not that big compared with previous cycles and is expected to close in 2025. Previous mix points that the staff will tend to recommend a contractionary stance to achieve the inflation target by mid-2025 since, according to projection, economic activity is still not a big concern. In our opinion, the central bank could tend to accelerate the easing cycle in the second half of the year, as we think a critical issue in deciding to speed up is having the Federal Reserve kick off the easing cycle.

—Sergio Olarte & Jackeline Piraján

EXPORTS CLOSED Q1-24 IN CONTRACTION

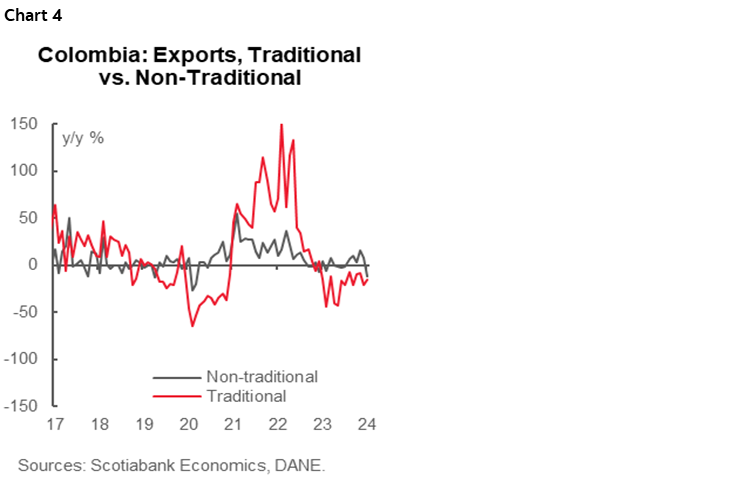

The National Statistics Institute (DANE) published the export data on Tuesday, May 7th. Monthly exports in March 2024 amounted to USD 3.83 billion FOB, a decrease of 14.2% y/y (chart 3). The March export level is one of the weakest since 2021. In terms of volume, there was a 2.4% y/y contraction to 8.43 million tons in March 2024, compared to 8.63 million tons in the same month of 2023.

Exports contraction was mainly explained by the 15.5% y/y decrease in external sales of fuels and products from the extractive industries, which amounted to USD 1.91 billion FOB and negatively contributed to the variation by -7.8 pp. Coal, coke, and briquettes exports contracted the most (-46.1% y/y), dragging -19.5 pp to the group’s variation. In terms of volume, the Fuel Group exported a total of 7.72 million tons, a decrease of 1.7% y/y, which suggest that the main source of the exports contraction was due to lower international prices. Coal, coke, and briquettes exports fell to 4.92 million tons in March 2024 from 5.03 million tons in March 2023 (-2.1% y/y and -1.2 pp), followed by oil and its derivatives, which went from 2.70 million tons in March 2023 to 2.65 million tons in March 2024 (-1.5% y/y and -0.5 pp).

On the other hand, external sales of agricultural products, food, and beverages amounted to USD 924.2 million FOB and showed a decrease of 6.2% y/y compared to March 2023, along with a contribution of -1.4 pp to the variation. This was mainly due to the fall in coffee exports (-18.8% y/y) and palm oil and its fractions (-26.2% y/y), which together contributed -7.3 pp to the group’s variation. In terms of volume, the group of agricultural products, food, and beverages fell by 4.8% y/y and contributed -0.3 pp to the total variation (459,843 metric tons).

As for the exports of manufactured articles, in March they amounted to USD 766.7 million FOB, registering a decrease of 16% y/y, with a contribution of -3.3 pp to the total variation. This behavior is mainly explained by the decrease in external sales of manufactured articles, mainly classified by material (-29.5% y/y) and chemical and related products (-15.7% y/y), which together contributed -15.9 pp to the Group’s variation. In terms of volume, there was an annual decrease of 15.5% y/y, going from 289,950 tons in March 2023 to 245,114 tons in March 2024 (-0.5 pp). In that sense, the manufacturing sector is reflecting a weaker external demand and not only a deterioration in prices.

In March 2024, the “Other sectors” group decreased by 25.3% y/y (USD 227.939 million and a contribution of -1.7 pp to the variation), mainly explained by the decrease in non-monetary gold exports, which negatively contributed 25.2 pp to the variation of the group.

In terms of participation, in March 2023, the reference month, exports of fuels and products from extractive industries participated with 49.9% of the total FOB value of exports; likewise, agriculture, food, and beverages with 24.1%, manufacturing with 20.0%, and other sectors with 6.0%.

In the YTD until March, Colombian exports so far this year amounted to USD 11.26 billion FOB and recorded a decrease of 9.4% compared to the same period of 2023, mainly due to a decrease of 16.8% y/y and -9.1 pp in exports of the group of fuels and products of extractive industries (USD 5.56 billion FOB).

It is anticipated that in 2024 there will be a widening of the external deficit, driven mainly by the increase in imports of goods due to the expected increase on inventories and the expected decrease in the prices of coal and coffee compared to 2023. This situation could lead to a reduction in dollar exports, despite favourable prospects in the international price of oil in recent weeks. However, a marginal increase in the current deficit is expected with a relatively stable level projected for 2024. These factors represent an improvement in the country’s external position, which reduces the vulnerability of the economy to possible significant deteriorations in the global context. All of this occurs in an environment of inflation going down and a cautious easing cycle from the central bank.

Highlights:

- Traditional exports (related to coffee, oil, and mining) declined in both value and volume. In March, traditional exports amounted to USD 2.09 billion FOB, down -16.3% y/y, with a total of 7.64 million tons exported (down 2% y/y).

- Among the components of traditional exports, oil and its derivatives grew by 10.1% y/y in March (USD 1.32 billion FOB). On the other hand, the most significant declines were coal exports, which fell 46.1% y/y in March (USD 516.88 million), and coffee exports, which fell 19.7% y/y (USD 246.26 million).

- In terms of volume, external sales of oil and its derivatives fell by 1.5% y/y in March (2.66 million tons exported). As for coal exports, they recorded a decline of 1.5% y/y in March (4.92 million tons), while coffee exports abroad contracted by 9% y/y in March (~49 thousand tons).

- On the other hand, non-traditional exports reached USD 1.74 billion in March 2024, recording a decline of 11.5% y/y (chart 4). In addition, in terms of volume, non-traditional exports reached 795,923 metric tons (-5.8% y/y vs. March 2023).

—Jackeline Piraján & Santiago Moreno

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.