Argentina: August industrial and construction activity add evidence to slowing recovery; IMF won’t seek spending cuts

Brazil: Retail sales on the clock; tax reform likely delayed to December with FTT in the cards

Peru: Debt rescheduling law moves forward; central bank maintains reference rate at 0.25%

ARGENTINA: AUGUST INDUSTRIAL AND CONSTRUCTION ACTIVITY ADD EVIDENCE TO SLOWING RECOVERY; IMF WON’T SEEK SPENDING CUTS

Annual growth slowed in both industrial production and construction activity in August, according to data released by INDEC on Wednesday, October 7 (chart 1). Industrial production growth pulled back from -6.6% y/y (revised from -6.9% y/y) in July to -7.1% y/y in August, while construction activity growth retreated from -12.9% y/y in July to -17.7% y/y in August. Together, the two sectors account for nearly a quarter of GDP and they provide an early pointer to what was likely a further slowing in the Argentine recovery in August. Growth in the monthly GDP proxy already cooled from -11.7% y/y in July to -13.23% y/y in August.

On Tuesday, October 6, IMF MD Kristalina Georgieva noted in a television interview that the Fund mission wouldn’t seek spending cuts from Argentina under the current pandemic circumstances. Although the Argentine authorities have said that they did not go into the talks seeking anything more than a rollover of their existing borrowing arrangement with the IMF, a combination of no spending cuts, slower growth, ongoing capital flight, and a further collapse in the blue-chip swap rate to USDARS 151 almost certainly points to a larger loan coming out of these negotiations.

—Brett House

BRAZIL: RETAIL SALES ON THE CLOCK; TAX REFORM LIKELY DELAYED TO DECEMBER WITH FTT IN THE CARDS

Today, Thursday, October 8, we are scheduled to get retails sales data for August at 08:00 ET, where we look for a moderate deceleration in annual growth to 4.2% y/y, while consensus expects a 5.8% y/y print following the strong 5.2% y/y growth we got in July. We think the key will be how consumers elected to behave ahead of the gradual paring down of the government’s COVID-19-related stimulus.

In reports out Wednesday, October 7, Brazil’s Economy Ministry said it wants to introduce a financial transactions tax (FTT) of 0.2% after the local elections, whose two rounds are set for November 15 and 29. These taxes are often criticized for the distortions they generate, Their revenue base is initially high and it appears easy to generate collections, but their effectiveness tends to wane over time. Additionally, there is a persistent fear that transactions taxes can lead to financial disintermediation. Nevertheless, they have proven effective at generating short-term boosts to revenue. They can be seen as a form of emergency tax for countries undergoing strong fiscal pressures—as is the case in Brazil.

Across Latam, FTTs have been used in both financial markets, such as Brazil’s IOF, which was raised to 1.1% in March 2020, as well as in broader applications to bank debits. In Brazil’s case, it is expected that the possible 0.2% tax on payments would be introduced to replace the existing tax on wages.

In a sense, the introduction of additional FTTs in Brazil seems like an admission that the fiscal adjustments that are needed to bring the country’s public finances back on to a sustainable path are larger than what is currently politically feasible and an FTT would serve as a bridge until a more fundamental review of the tax system can be undertaken. Our view is that to get public finances back on track, the bulk of the work would need to be done on the spending side.

—Eduardo Suárez

PERU: DEBT RESCHEDULING LAW MOVES FORWARD; CENTRAL BANK MAINTAINS REFERENCE RATE AT 0.25%

I. Debt rescheduling law moves forward accompanied by new subsidies

On Wednesday, October 7, Pres. Vizcarra signed and promulgated Peru’s new debt rescheduling law, which was approved last Friday, October 2, by Congress and features text agreed with the Executive. This initiative adds to the debt rescheduling already carried out to date by the financial system (i.e., a total of PEN 120 bn, equivalent to 15.8% GDP) and maintains an optional element under which financial institutions can identify and choose whose debts will be treated. This additional step contemplates a new program of State guarantees that would be conditioned on a scheme to reduce the cost of existing loans. The value of the State guarantees could reach PEN 5.5 bn (0.7% GDP) and would benefit 7 million debtors.

Based on the good precedent achieved with the new debt rescheduling law, Pres. Vizcarra urged Congress to work together with the Executive on efforts to improve the private and the public (ONP) pension systems. We believe that this is a good sign. The initiative proposed by the government for contributors to the ONP could reach up to PEN 13.6 bn (1.8% GDP) in value.

In other policy news, the Government will start a second round of subsidies to families (PEN 760) from this week, with a cost of PEN 6.5 bn (0.9% GDP) that should benefit around 8.4 million families. The Government is also evaluating a second round of payroll and wage subsidies that would follow their first round that was implemented in April.

II. Central bank maintains its reference rate at 0.25%

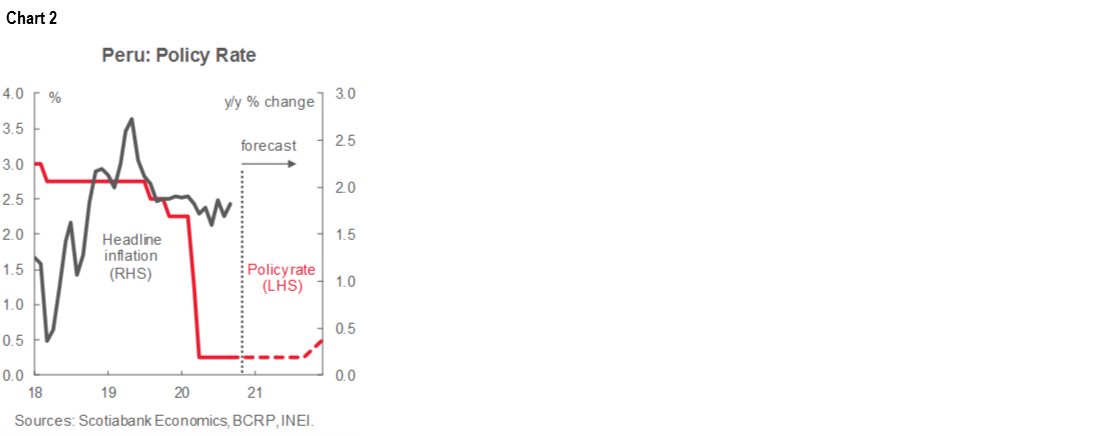

At its meeting in the evening of Wednesday, October 7, the BCRP, Peru’s Central Bank, kept its reference interest rate unchanged at 0.25% for a sixth consecutive month (chart 2), in line with our expectations and a unanimous consensus.

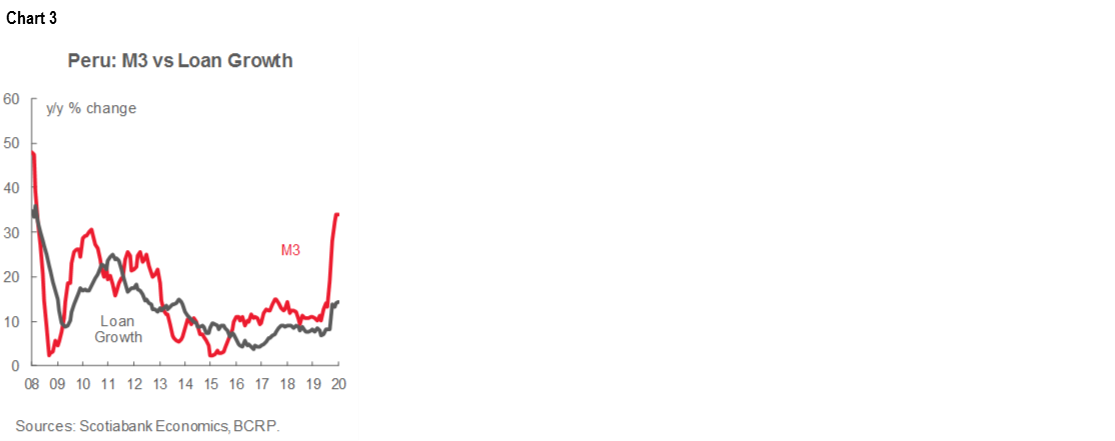

The BCRP is currently focused on the provision of liquidity to the economy. Injections reached PEN 60.5 bn (8.0% GDP) as of October 6, a level similar to the PEN 60.7 bn provided a month ago, of which PEN 47.8 bn corresponded to the Reactiva Program—a State-guaranteed loan program—whose access period has recently been extended until October 30 (see DS N ° 287-2020-EF). The program features guarantees of up to PEN 60 bn. During the last month, the pace by which these funds have been allocated has slowed down significantly, probably because remaining potential borrowers present more difficult risk profiles in this final tranche of the program.

As a consequence of this monetary stimulus, loan growth maintained a pace of 14.4% y/y through August (chart 3).

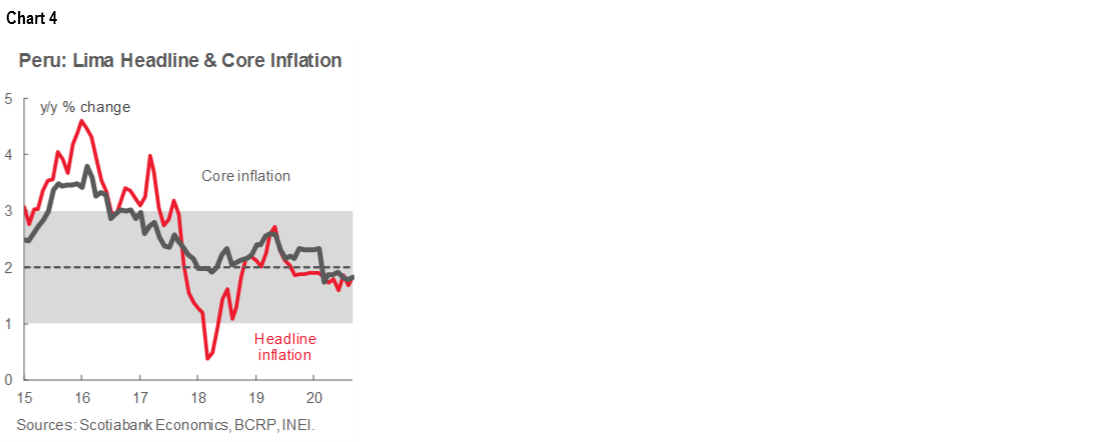

Regarding inflation, the BCRP has altered its view. The Central Bank now thinks that inflation (chart 4) could settle around the lower limit of its target range and not below, as the BCRP had indicated in its previous statements. This is in line with our revised forecast in the October 4 Latam Weekly of a somewhat higher rate of inflation than we had previously expected for this year.

Nevertheless, the BCRP’s main messages remain unchanged: it is committed to maintaining an expansive monetary stance for a prolonged period of time, with a bias to implement greater stimulus, if necessary, through additional measures. For the moment, we do not perceive that the Bank is preparing to implement any new instruments or enhance existing ones, but it has been more active lately in managing the volatility of the PEN.

—Mario Guerrero

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including, Scotiabanc Inc.; Citadel Hill Advisors L.L.C.; The Bank of Nova Scotia Trust Company of New York; Scotiabank Europe plc; Scotiabank (Ireland) Limited; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Scotia Inverlat Casa de Bolsa S.A. de C.V., Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorised by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorised by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V., and Scotia Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.