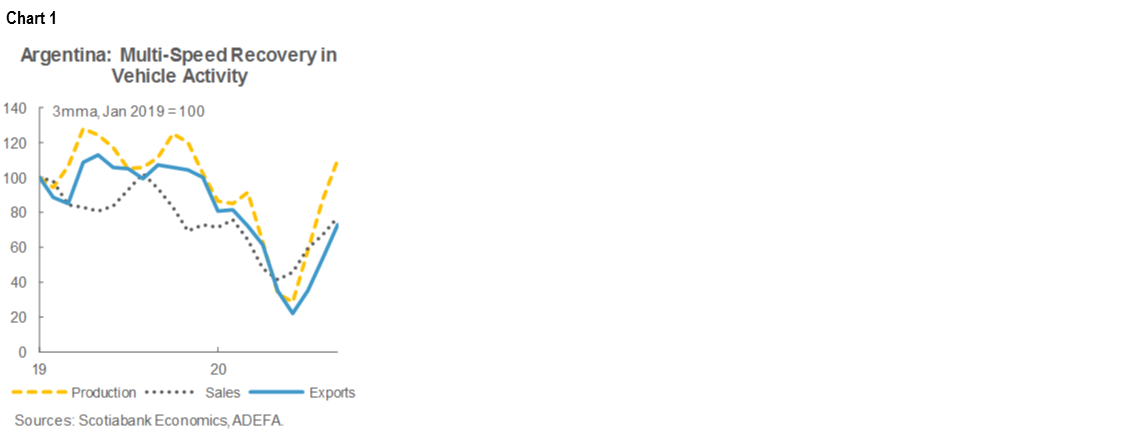

Argentina: September vehicle production recovered to pre-lockdown levels, but that’s a low bar

Colombia: Biosecurity costs and higher regulated prices in September took headline inflation up to 1.97% y/y

Mexico: Government and business leaders unveiled investment plan; consumer confidence remains weak

Peru: New bank debt relief initiative; vehicles sales in September were just under pre-COVID-19 levels

ARGENTINA: SEPTEMBER VEHICLE PRODUCTION RECOVERED TO PRE-LOCKDOWN LEVELS, BUT THAT’S A LOW BAR

In data for September released Monday, October 5, by the ADEFA, the Argentinian Association of Auto Manufacturers, production was up 16% y/y to 32.1k total vehicles (chart 1), marking a full recovery to pre-lockdown levels, but leaving production still down 35% from early-2018, the beginning of the current three-year recession, and 48% from 2014. Domestic sales hit 35.1k units, up 30.5% y/y, the first positive annual reading since the lockdown began. Arguably, about 5k of these total sales represent pent-up demand from previous months that is unlikely to continue through the remainder of the year. Still, the September sales print was strong. September exports, at 17.1k units, were still down -17.0% y/y, reflecting weak regional demand.

The relatively strong September vehicle numbers don’t alter our forecast of an economy-wide -10.8% y/y contraction in activity for 2020 as a whole.

—Brett House

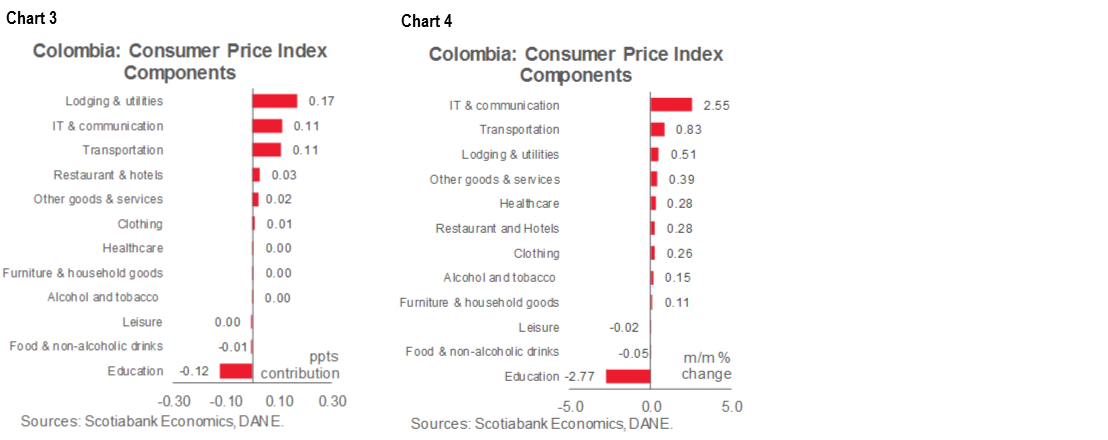

COLOMBIA: BIOSECURITY COSTS AND HIGHER REGULATED PRICES IN SEPTEMBER TOOK HEADLINE INFLATION UP TO 1.97% Y/Y

Monthly CPI inflation was 0.32% m/m in September, according to DANE’s data published late on Monday, October 5. The result came in well above market expectations (0.11% m/m, according to the BanRep survey) and closer to our projection of 0.17% m/m. September inflation resulted from the upside effect of the end of some government price supports and higher biosecurity costs in transport services that more than offset reductions in tuition fees by universities and technical colleges. The annual inflation rate increased by 9 bps to 1.97% y/y, close to the lower bound of BanRep’s target of 2% (chart 2). Core inflation stood at 1.57% y/y (previous: 1.37% y/y). Although core inflation remained well below the central bank’s target range, it increased by 20 bps in September.

The housing-related sector provided the largest positive contribution to headline inflation in September (17 bps), due to the gradual withdraw of government aid to regulated water and electricity prices (chart 3). IT and communication sectors (also regulated) added 11 bps to the headline mainly because of the effect from the expiry of the VAT reduction on mobile plans. Price increases also came from transport costs (0.83% m/m, chart 4), which received a boost from vehicle prices (0.56% m/m) and intermunicipal transportation that reactivated in September with very strict biosecurity measures that made bus fees to increase by 20.14% m/m. Education inflation contracted -2.77% m/m (chart 4, again), which provided a -12 bps on headline inflation (chart 3, again). Tuition fees in universities and technical education institutes fell -7.47% m/m.

Goods inflation increased by 16 bps to 1.15% y/y, services inflation stood at 1.86% y/y (previous: 1.79% y/y), and regulated prices increased by 60 bps to 1.19% y/y. Core inflation measures also increased: ex-food inflation came in at 1.57% y/y (up 20 bps from the previous month), while ex-food and regulated inflation increased by 10 bps to 1.67% y/y.

Altogether, September’s CPI inflation showed that the new government re-opening strategies put a stop to the free fall in annual inflation seen since the pandemic started. We think the “new normality” and further re-opening will continue stabilizing the economy, which should keep inflation hovering around 2% y/y for the rest of the year. Yearly inflation is expected to begin rising in 2021. We still forecast next year’s annual inflation rate to converge to BanRep’s 3% target by end-2021. The September CPI results support our call that BanRep will keep its policy rate at 1.75% for the rest of 2020 and into 2021.

—Sergio Olarte & Jackeline Piraján

MEXICO: GOVERNMENT AND BUSINESS LEADERS UNVEILED INVESTMENT PLAN; CONSUMER CONFIDENCE REMAINS WEAK

On Monday, October 5, the Mexican President, AMLO, presented an infrastructure and investment program, joined by the representative of the Mexican Business Chamber, Carlos Salazar, in a new attempt to boost private capital spending. The plan, which amounts to a total of USD 14 bn, focuses on 39 projects in strategic sectors such as energy, transportation, water, roads, and tourism, among others. Gustavo de Hoyos, President of the Mexican Republic's Employers' Confederation (Coparmex in Spanish), underscored that the projects are 100% private—private in their ownership, private in their execution, and private in their financing—with the government simply releasing regulatory obstacles to enable them to move forward. The plan seeks to boost the economic recovery by increasing jobs and generating spillovers.

Data released on Monday, October 5, by INEGI shows that consumer confidence remained weak in September, a sign that Mexicans are still worried about the general economic outlook as the pandemic drags on. The consumer confidence index stood at 35.9 ppts nsa in September, down 9.1 ppts from a year earlier, which marked a 10th consecutive month where sentiment was weaker than the year before (chart 5). On the other hand, confidence improved for the fourth consecutive month in a row, reaching its highest level since closures were widened in April—which is encouraging for the entire economy since consumer spending accounts for about 65% of economic growth in Mexico—but the level of the index still points to only a gradual recovery ahead.

—Paulina Villanueva

PERU: NEW BANK DEBT RELIEF INITIATIVE; VEHICLES SALES IN SEPTEMBER WERE JUST UNDER PRE-COVID-19 LEVELS

Congress and the Executive joined forces to enact a law on Friday, October 2, to promote the reprogramming of bank debt held by the general public and small businesses through the provision of government guarantees. Under this law, the State would provide guarantees totaling PEN 5.5 bn for personal, consumer, car, mortgage, and small business loans. The bill received 115 votes in its favour and only one against. The initiative will allow for payments on loans to be postponed for between six and nine months. The loans will continue to accumulate interest over this time, but financial institutions will need to grant some sort of relief, such as lower interest rates or lower commissions, for government guarantees to be triggered. There are a number of conditions that debt holders must meet, as well, and it is not clear how useful this initiative will be in the end. Thus, it is not easy to gauge the impact of the measure quite yet, outside of saying that it will likely be small compared to that of, say, the REACTIVA program. The measure has political significance, however, as the law was designed jointly by the Ministry of Finance and Congress, in what is hopefully a sign of a change in the relationship between the two—from one of confrontation to one of collaboration. The heavy vote in favour of the bill implies that Congress appears to have adopted a different attitude in working with the Government. We will be more convinced, however, once it becomes evident that other, more aggressive, debt-relief initiatives that have recently been introduced in Congress are left aside.

According to a local private sector automobile association (Asociación Automotriz del Perú), light vehicle (automobile) sales in September were down a mild -5.8% y/y and up a hefty 18% m/m. Heavy vehicle (truck) sales did even better, up an impressive 46% y/y and 16% m/m. Taking the two together, vehicle sales were down only -1.2% y/y in September and, thus, were very close to pre-COVID-19 levels (chart 6). All figures were better than expected, with trucks sales especially so. Thus, vehicle sales constitute yet another market that is showing a robust recovery to pre-lockdown levels. The strong performance of truck sales, in particular, may be linked to construction. Cement sales have also surpassed pre-COVID-19 levels (see the October 4 edition of the Latam Weekly).

—Guillermo Arbe

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including, Scotiabanc Inc.; Citadel Hill Advisors L.L.C.; The Bank of Nova Scotia Trust Company of New York; Scotiabank Europe plc; Scotiabank (Ireland) Limited; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Scotia Inverlat Casa de Bolsa S.A. de C.V., Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorised by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorised by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V., and Scotia Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.