Brazil: BCB’s Copom holds Selic rate and forward guidance steady

Colombia: Monetary policy preview; S&P affirmed investment grade

BRAZIL: BCB’S COPOM HOLDS SELIC RATE AND FORWARD GUIDANCE STEADY

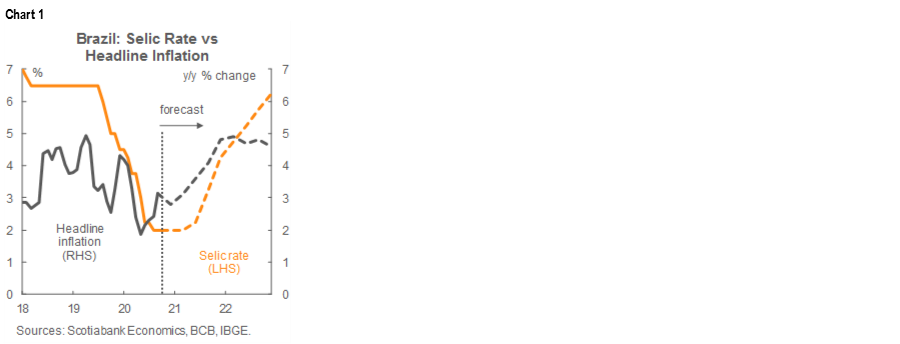

In its statement released on the evening of Wednesday, October 28, the BCB’s Copom announced that it had unanimously decided to hold the Selic rate at its record low of 2.00% for a third time in a row, in line with our expectations (chart 1) and the unanimous consensus of analysts.

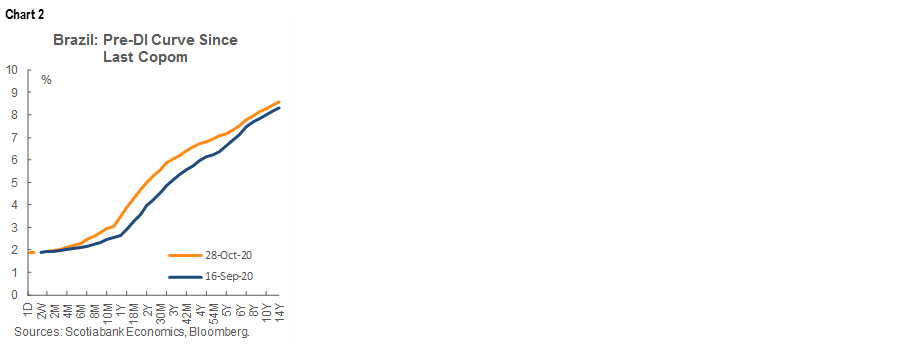

The Copom entered Wednesday’s announcement with some big question marks hanging over it: there was uncertainty on how the message from the central bank would change in light of the market’s reaction to the communications from its last meeting on September 16. At that meeting, the Copom intensified the forward guidance introduced at its August 5 policy decision: in September, the Copom moved from a stance that it did not “foresee” a reduction in the extent of monetary stimulus to a stronger view that it did not “intend” such a pullback unless inflation returns to the target over the relevant policy horizon to end-2021. However, despite that clear signal, the Brazilian DI curve has since widened by about 100 bps in the 2-year space (chart 2).

In its statement following yesterday’s meeting, the Copom stood firm: it signalled that it perceives the current level of stimulus as appropriate and that it would not change it so long as the Committee’s identified conditions continue to be met: inflation expectations are below target for the relevant policy horizon, growth is subdued, the fiscal stance remains unchanged, and longer-term inflation expectations are still anchored. As has been the case for several months, the Copom’s main concerns are centred on fiscal stability despite a recent upturn in IPCA inflation (chart 3).

On the basis of the Copom’s communications, we don’t see any reason to alter our existing baseline forecasts. We anticipate a first increase in the Selic rate late in Q2-2021 (chart 1, again).

—Eduardo Suárez

COLOMBIA: MONETARY POLICY PREVIEW; S&P AFFIRMED INVESTMENT GRADE

I. BanRep Board expected to hold on Friday

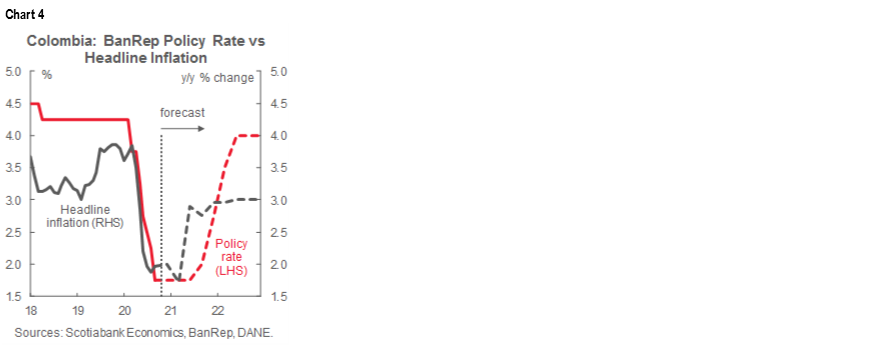

On Friday, October 30, BanRep, will hold its regularly scheduled Board meeting on monetary policy and we, along with the consensus, expect the benchmark policy rate to be held at its record low of 1.75% (chart 4). At its last meeting on September 25, the central bank delivered what we think was the final rate cut in a split 4-3 vote, where the minutes of the meeting indicated that the minority preferred to hold the policy rate unchanged at 2.00%.

At this meeting, a fresh set of the macroeconomic forecast is expected from the central bank staff, to be followed by the release of the Q4 Monetary Policy Report next Tuesday, November 3. Revisions to the Bank’s expectations for key macroeconomic indicators are likely to reinforce our sense that the Board will stay on hold from here. These updates could be accompanied by guidance in the Board’s and Governor’s communications that would emphasize some concerns about the current and expected economic situation.

Since the last meeting, the September CPI inflation reading surprised to the upside as, finally, the effects from an end to public support to keep regulated prices down started to materialize. Still, inflation remains at the bottom of the BanRep’s target range of 2% y/y to 4% y/y (chart 4, again). Nevertheless, September’s uptick in prices led to adjustments in inflation expectations to take them closer to the 2% y/y target by the end of the year and to 2.9% y/y toward end-2021. On the economic activity side, labour market indicators for August were also stronger than expected. As a result, business confidence indicators now point to more positive outlooks for economic activity and employment recovery.

All of this augurs for a pause—and likely an end—to the easing cycle at Friday’s BanRep Board meeting; the Board’s messaging will be strengthened if we see a unanimous vote from its members. However, there is a possibility of another divided decision. We will carefully review next week’s Monetary Policy Report for indications of expected developments that could trigger a change in stance from the Board in the future.

II. S&P affirmed lowest notch of investment-grade for Colombia's LT sovereign debt; outlook remained negative

Late on Wednesday, October 28, S&P announced that it had affirmed Colombia’s sovereign credit rating at “BBB-” with a “negative” outlook. S&P emphasized that the rating reflects a stable democracy and a tradition of credible economic-policy institutions, which together have maintained predictability and caution in macroeconomic management for many years in the face of macroeconomic shocks. S&P last downgraded Colombia’s credit rating to “BBB-” in late-2017. After the arrival earlier this year of the pandemic and its related economic shocks, the credit rating agency changed its outlook to “negative”.

The rating agency highlighted the flexible exchange rate and nimbleness in monetary policy as appropriate buffers against external shocks. Additionally, S&P considered Colombia’s access to the IMF’s Flexible Credit Line (FCL) as a good buffer for external vulnerabilities.

S&P’s “negative” outlook reflects the risk of a significant economic contraction in 2020 with only a moderate recovery in 2021. If a softer macroeconomic scenario materializes and it continues weakening public finances or impedes a fiscal consolidation through tax reform or other budgetary policies, it could trigger a downgrade to the rating. S&P’s macro scenario points to a -8.0% y/y GDP contraction in 2020 and a recovery of 5.5% y/y in 2021; we view S&P’s baseline projections as reasonable since they are close to our forecasts of -7.5% y/y in 2020 and 5.0% y/y in 2021. S&P expects general government net debt to peak at 63% of GDP in 2021—a bright line for future credit reviews.

Going forward, government announcements on fiscal reform will likely be key considerations for future ratings actions. Any consolidation of public finances will require the pandemic to be under control and economic recovery to be underway. We think this discussion could start by the end of H1-2021, led by the government’s expert committee on fiscal issues.

All in all, S&P’s decision gives Colombia some time to bring forward fiscal adjustment strategies to stabilize and reduce its debt-to-GDP ratio over time. Fitch and Moody’s are likely to announce sovereign credit-rating actions in the forthcoming weeks as the Ministry of Finance has announced that it is receiving technical visits from both agencies. There is a chance that Fitch could take a ‘wait and see’ approach given its actions earlier this year, while Moody’s still has space to cut the credit rating by one notch without taking Colombia below investment grade (table 1).

—Sergio Olarte & Jackeline Piraján

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including, Scotiabanc Inc.; Citadel Hill Advisors L.L.C.; The Bank of Nova Scotia Trust Company of New York; Scotiabank Europe plc; Scotiabank (Ireland) Limited; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Scotia Inverlat Casa de Bolsa S.A. de C.V., Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorised by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorised by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V., and Scotia Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.