Argentina: Recovery on track despite mid-year COVID-19 surge

Brazil: Early-November IPCA-15 added yet another challenge for the BCB’s “forward guidance”

Colombia: November’s Citi survey shows consensus on medium-term scenarios

Mexico: Early-November inflation back in target range, labour market kept improving in October

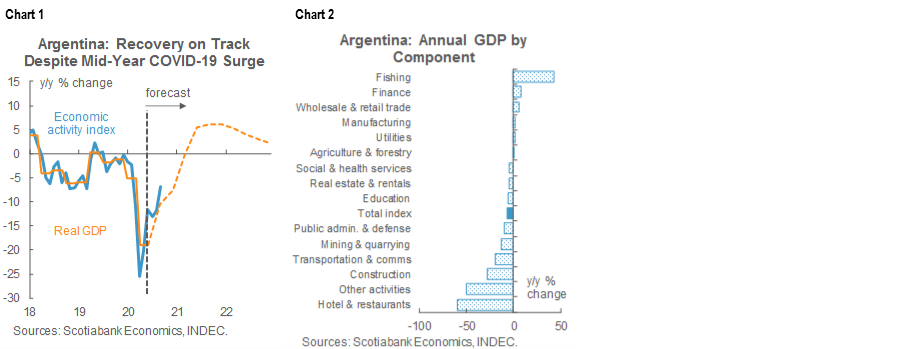

ARGENTINA: RECOVERY ON TRACK DESPITE MID-YEAR COVID-19 SURGE

Argentina’s post-lockdown recovery—such as it is—remained on track in September as economic activity strengthened from being down -11.6% y/y in August to -6.9% y/y in September (chart 1). While this was much better than the consensus expectation of -8.6% y/y, it was close to the -6.0% y/y we forecast on the basis of other data points that have been received through the end of Q3. In sequential monthly terms, growth picked up from 1.1% m/m sa in August to 1.9% m/m sa in September. We had forecast a 1.5% m/m sa gain based on a different seasonal adjustment than INDEC appears to employ. Fishing led September’s gains, but this is a seasonal phenomenon (chart 2). More encouragingly, beyond fishing five of 15 other sectors showed annual gains, adding breadth to the post-lockdown rebound.

—Brett House

BRAZIL: EARLY-NOVEMBER IPCA-15 ADDED YET ANOTHER CHALLENGE FOR THE BCB’S “FORWARD GUIDANCE”

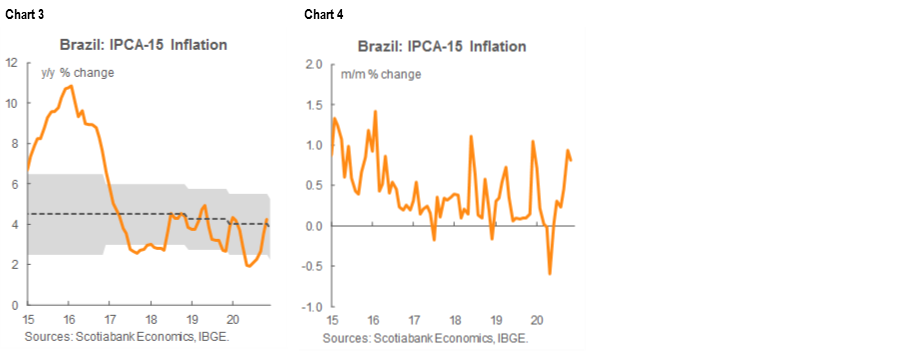

Another week, and another headache arrives for the BCB. IPCA-15 inflation for the first half of November, released on Tuesday, November 24, printed at 4.22% y/y, above the 4.13% y/y consensus and our own projection of 4.1% y/y—a strong rise from late-October’s 3.52% y/y (chart 3), but it was driven in part by level effects. Sequential inflationary pressures actually moderated slightly from 0.94% m/m to 0.81% m/m (chart 4).

As has been the case in the past few prints, non-durable consumer-goods prices generated the bulk of inflationary pressures (chart 5): food & beverage prices were up 2.16% m/m, appliance prices rose 1.4% m/m, and clothing prices gained 0.96% m/m. Amongst services, transportation prices, up 1.00% m/m, saw substantial gains. The government’s stimulus to consumer spending was likely one of the main factors that boosted prices. One consolation for the BCB is that we have not, at least yet, seen material inflationary contagion into prices for services and durable goods and, overall, sequential monthly inflation didn’t accelerate further.

Nevertheless, the DI and BRL-denominated Brazilian government curves are pricing around 340 bps of hikes over the next 12 months—a clear sign that the market sees further inflationary pressures ahead and isn’t buying the BCB’s arguments for patience.

—Eduardo Suárez

COLOMBIA: NOVEMBER’S CITI SURVEY SHOWS CONSENSUS ON MEDIUM-TERM SCENARIOS

November’s Citi Survey, which BanRep uses as one of its key indicators of expectations for inflation, the monetary policy rate, GDP, and the COP, came out on Monday, 23 November. Key points included:

- Growth forecasts were revised marginally downward. For 2020, a contraction of -7.18% y/y, 0.3 ppts below last month’s survey reading of -6.89%, is now expected in the wake of the Q3 GDP results. In 2021, the recovery is expected to hit a pace of 4.54% y/y, below the previous survey’s 4.67% y/y consensus. We expect -7.5% y/y in 2020 and a rebound to 5.0% y/y in 2021 (see our Nov. 14 Latam Weekly).

- Inflation expectations for 2020 fell, but for 2021 they remained anchored. November’s monthly inflation rate is, on average, expected to be 0.08% m/m and 1.72% y/y; we project 0.09% m/m and 1.73% y/y on the back of neutral education inflation and positive inflation in foodstuffs, which would be offset to some extent by the effects of the VAT holiday. For December 2020, the survey’s average forecast is 1.75% y/y, lower than September’s reading (1.89% y/y), due to October’s inflation downward surprise. Having said this, by December 2021, inflation is anticipated to hit 2.80% y/y, a bit below the 2.87% y/y average projection in the October survey. In all cases, these results are just a few basis points off the results of the BanRep November survey of macroeconomic expectations, which we summed up in our November 18 Latam Daily.

- Market consensus points to rate stability. A full 100% of analysts surveyed expect the monetary-policy rate to remain at 1.75% for the rest of 2020. In 2021, consensus expects one 25 bps hike: although analysts’ projections are dispersed between stability and 125 bps hikes, the mode is at 2.00% (chart 6).

- The USDCOP forecasts point to a relatively stable currency through December 2020 and a COP appreciation in 2021. On average, respondents expect a level of USDCOP 3,678 by the end of 2020 and USDCOP 3,583 in 2021.

—Sergio Olarte & Jackeline Piraján

MEXICO: EARLY-NOVEMBER INFLATION BACK IN TARGET RANGE, LABOUR MARKET KEPT IMPROVING IN OCTOBER

I. Inflation back to target range in the first half of November

Inflation for the first half of November came back into Banxico’s target range, according to data released on Tuesday, November 24. Headline annual inflation came down from 4.09% y/y in late-October to 3.43% y/y in early-November (versus 3.61% y/y consensus), still higher than the 3.10% y/y we saw at this time last year (chart 7). On a sequential basis, inflation slowed from 0.16% 2w/2w in late-October to 0.04% 2w/2w in early-November, below the 0.23% 2w/2w consensus.

By components, both core and non-core prices moderated their growth rate, with core inflation coming down from 3.96% y/y in late-October to 3.68% y/y in early-November (versus 3.66% y/y a year earlier), and non-core inflation falling from 4.50% y/y to 2.67% y/y (compared with 1.45% y/y in the first half of 2019, chart 7 again). Annual inflation in goods prices came down sharply from 5.4% y/y in late-October to 5.0% y/y in early-November, while annual services inflation continued its gradual moderation from 2.35% y/y to 2.25% y/y (chart 8).

Looking at the sequential monthly details:

- Sequential core inflation turned negative, coming down from 0.07% 2w/2w in late-October to -0.11% 2w/2w in early-November versus the 0.09% 2w/2w consensus. The unexpected drop in core inflation may have been driven by promotional sales that took place from November 9 to 20, an effect that we expect to be temporary. Merchandise goods prices came down -0.30% 2w/2w, while the prices of services maintained their pace of the previous two weeks at 0.10% 2w/2w growth; and

- On the other hand, sequential non-core inflation came in at 0.51% 2w/2w, (versus 2.30% 2w/2w a year earlier), with agricultural price inflation turning negative at -0.94% 2w/2w (versus 1.46% previously). Fruit and vegetal prices drove the decline by diving deeply into deflationary territory. In contrast, regulated prices and utility tariffs both rebounded as summer subsidies on electricity rates came to an end.

II. Better labour market conditions in October, yet still below pre-pandemic levels

INEGI also released on Tuesday, November 24, the fourth edition of its new Survey on Jobs and Employment (ENOE), which is mainly based on face-to-face interviews (86% of respondents) with some telephone conversations (14% of respondents). The unemployment rate came down from 5.1% in September to 4.7% in October, “in line with the evolution of the pandemic in the country” (chart 9). Still, INEGI highlighted that the average unemployment rate for January to October was 4.5%, the highest rate for the first 10 months in six years. Some further notable points included:

- The participation rate went up again, from 55.6% in September to 57.4%. The share of informality amongst the total employed population rose from 54.9% in September to 56.0%, while the underemployment rate fell from 15.7% in September to 15.0%;

- In absolute terms, the economically active population increased from 53.8 to 55.6 mn people, an inflow of 1,736 mn; the total employed population rose from 51.1 mn to 53.0 mn (up by 1,865 mn). In the sub-components, the informally employed population went up from 28.1 to 29.7 mn people (an increase of 1,598 mn), while the unemployed population decreased from 2.7 mn, to 2.6 mn (down by -0.129 mn); and

- The service sector led much of the further recovery, driven by increases in the retail, financial, corporate, professional, and hospitality sectors.

Still, even with October’s progress, Mexico’s participation rate remained below its pre-pandemic levels and unemployment rates remained elevated.

—Miguel Saldaña

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.