Argentina: Capacity utilization back to pre-pandemic levels; leading indicators point to further recovery ahead

Chile: Bill on second withdrawal of pension assets moves forward

Peru: The Sagasti Government’s new cabinet looks capable

ARGENTINA: CAPACITY UTILIZATION BACK TO PRE-PANDEMIC LEVELS; LEADING INDICATORS POINT TO FURTHER RECOVERY AHEAD

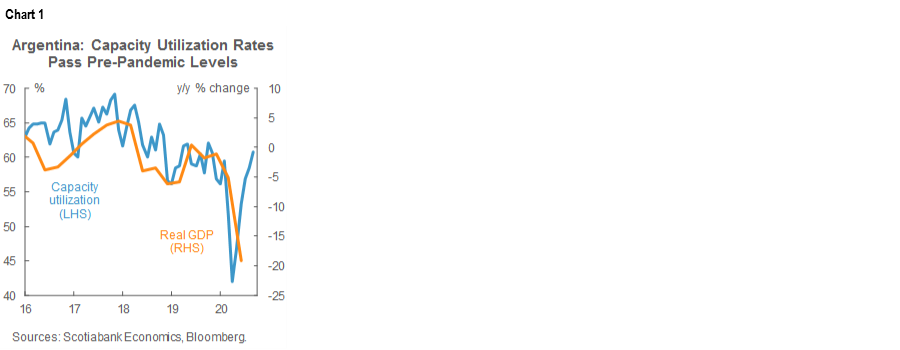

Industrial capacity utilization rose to 60.8% in September, according to data released by INDEC on Monday, November 16 (chart 1). This took capacity utilization up from 58.4% in August and put it well above the 42% level recorded during April’s comprehensive lockdowns and higher than the 57.7% recorded in September 2019. Given that industrial production accounts for about a fifth of GDP, this bodes well for Q3 GDP growth, whose data are due for publication by INDEC on December 16, about a month behind the rest of the region.

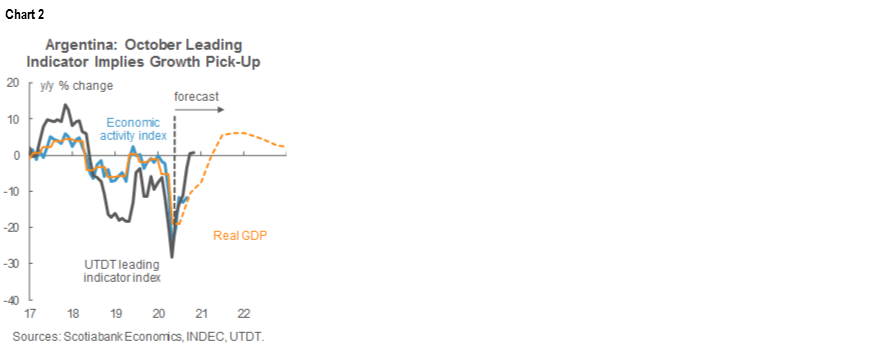

October’s UTDT leading indicator notched up a second month where it came in higher than a year ago, with annual growth in the index rising slightly from 1.59% y/y in September to 1.64% y/y in October (chart 2). The leading indicator’s recent prints align with our estimate that the September economic activity index is likely to show an improvement from being down -11.6% y/y in August to -6.0% y/y in September, on the back of a mild acceleration in seasonally-adjusted sequential month-on-month growth. This would pare annual GDP losses from -19.1% y/y in Q2 to -10.4% y/y in Q3, and keep Argentina on track for a -10.8% y/y contraction in 2020, as we forecast in the November 14 Latam Weekly. In a mix of sometimes conflicting data points and a still-serious surge in COVID-19, Argentina’s recovery continues to unfold in line with our expectations and close to market consensus.

—Brett House

CHILE: BILL ON SECOND WITHDRAWAL OF PENSION ASSETS MOVES FORWARD

After several hours of discussion on Wednesday, November 18, the Constitutional Committee finally dispatched to the full Senate the bill that would allow a second set of withdrawals of 10% of individuals’ assets at the AFP pension funds. The bill would maintain the same conditions that applied to the first withdrawal of pension assets: most importantly, there would be universal access to withdrawals (i.e., there would not be any targeting of certain income groups or other demographics) and taxes would not apply to withdrawals by relatively high-income earners. The bill also states that the AFPs would have 15 working days following a request to transfer funds to their account holders.

The President of the Central Bank, Mario Marcel, was invited to testify at the Committee. He expressed the BCCh’s concerns that a second set of withdrawals would not only generate liquidity pressures for the AFPs, which would be forced to sell assets, but would also generate operational problems in the entire process that would follow a withdrawal request. Withdrawals would generate a series of logistical challenges related to the transfer of funds to the banks, the availability of funds for contributors, and cash access, among others—all of which would require some time to operate effectively. Pres. Marcel noted that some flexibility on the time required to deliver larger amounts would help to mitigate some of these challenges.

The BCCh President also warned that new withdrawals from the AFPs could affect their institutional credibility. Marcel noted that, “By breaking the logic of a one-time withdrawal on retirement, this bill could affect institutional credibility, it could raise the risk premium on Chile, AFPs could tend to hold more liquid and take less profitable positions in order to be ready for future withdrawals; the central bank's space to offset this will be more limited in the future.” Pres. Marcel indicated that total drawings under the second withdrawal bill would likely be between a quarter and a third less than what we saw under the first bill, where around USD 19 bn in assets were withdrawn from the AFPs.

President Sebastián Piñera warned on Tuesday, November 17, in an event with businesspeople, that he would go to the Constitutional Court if the proposed second withdrawal of pension assets is approved. According to the President, the approval of the measure in the Senate “would not only be deeply unconstitutional, it is a path that would lead to the destruction of these institutions, and all of us who hold public office, including parliamentarians and, by the way, this President, when we take office we swear to comply and enforce the constitution”.

At the end of the discussion in the Senate, the Minister of the Presidency announced that the bill implied a constitutional conflict because it would violate several rules under Chile’s constitution.

All in all, we think there is only a low probability that this bill will be passed into law. The Government’s opposition is opening up the entire process around the bill to scrutiny. Given that the Constitutional Court will likely have to rule on the bill’s legality, we do not foresee the bill being approved.

—Carlos Muñoz

PERU: THE SAGASTI GOVERNMENT’S NEW CABINET LOOKS CAPABLE

Violeta Bermúdez, a constitutional lawyer, has been designated to lead the new cabinet of the Sagasti Government. Bermúdez was briefly Vice-Minister of Women’s Affairs and Human Rights in 2002 during the Toledo Government. In 2003 she was appointed to head the Advisory Council to the cabinet. Aside from constitutional law, she has been involved in gender issues. Since 2018 she has been part of the Honours Tribunal, an official institution dedicated to ensuring fair elections. Her appointment underscores the importance that President Sagasti places on ensuring that the 2021 elections take place as scheduled and without incident.

Waldo Mendoza has been chosen to lead the key Ministry of Finance. Mendoza is a prestigious economist who is known for his very vocal newspaper columns. He is mostly an academic at the Universidad Católica, but he also has experience in fiscal management, albeit perhaps not as recently as one would like. He was Vice-Minister of Treasury during 2005–06 and directed the Office of Economic and Social Affairs from 2002 to 2005. He was also on the Board of Directors of the BCRP in 2015–16. Mendoza’s most recent experience has been as President of the Fiscal Council, an official institution that monitors compliance with the fiscal rules and regulations and acts as a steward and sounding board for government fiscal policy. As such, Mendoza has made a name for himself as a hawk on fiscal matters. His designation ratifies statements made by President Sagasti that his government would follow a policy of fiscal prudence.

Mendoza has a strong personality, and his designation should make it more difficult for any Congressional initiative that adds to the fiscal burden to be approved by the Executive. However, it is not clear if the same criteria will be used for those initiatives (such as pension fund withdrawals) that do not imply a direct fiscal cost.

Finally, Mendoza also happens to be a member of the directive council for the University Superintendency, Sunedu, which has been a great bone of contention between Congress and the Executive. His appointment reinforces President Sagasti’s message that the educational reform will not be reversed.

Other highlights include:

- Pilar Mazzetti, the Minister of Health during the Vizcarra regime, was reinstated. She is well appreciated by large segments of the population for the determination with which she dealt with COVID-19. However, she had come under a bit of fire more recently since her policies do not seem to have been successful in curbing the pandemic. The main message in her appointment is that Sagasti values her expertise and that continuity is better than change;

- Other members of the Vizcarra Government who are being reappointed include Alejandro Neyra at the Ministry of Culture and Ricardo Palacios at Labour. To appoint Mazzetti at Health could be seen as a move driven by common sense, but to draw on three members of the Vizcarra Government is also freighted with other messages; and

- Another appointment that is making headlines is that of Nuria Sparch as Head of the Ministry of Defense. Following in the of footsteps of Bachelet in Chile, this is the first time in Peru’s history that a woman has been appointed Head of Defense.

Sagasti has populated his cabinet mostly with specialists in their fields. Many, but not all, have experience in public office. Some have participated prominently in past governments, but mostly as outside independents. Overall, this is a serious cabinet. It is significantly apolitical and not one that seems designed for dealing with Congress. One wonders if Sagasti is planning to deal politically with Congress himself. One difficulty this cabinet may face—with the exception of Health Minister Mazzetti—is to hit the floor running. The makeup of the cabinet implies that it will require time to acquire the operational knowledge it needs for proper policy implementation. However, the cabinet does seem capable enough to fulfill effectively its role as a caretaker government.

—Guillermo Arbe

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.