Argentina: Inflation accelerated in October, BCRA raises benchmark rate

Colombia: September imports fell by -17.2% y/y, YTD trade deficit narrowed by 11% y/y

Mexico: Banxico holds at 4.25%; job gains in October

Peru: New cabinet appointed as the BCRP stays on hold

ARGENTINA: INFLATION ACCELERATED IN OCTOBER, BCRA RAISES BENCHMARK RATE

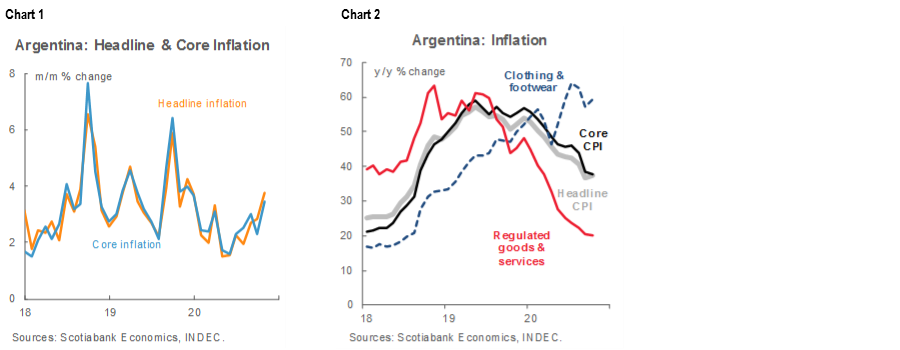

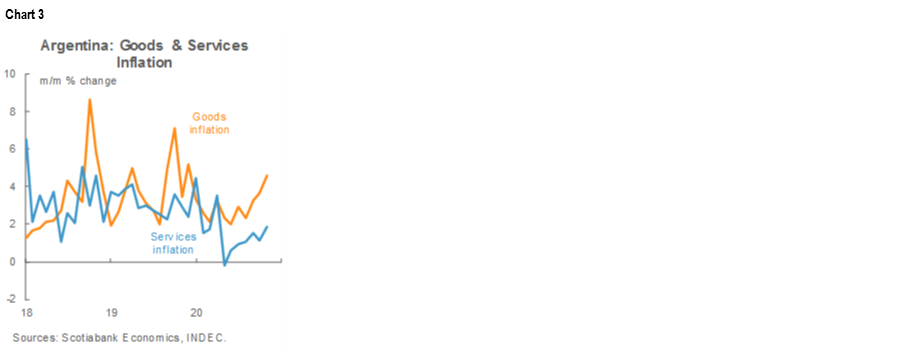

October inflation, according to data released by INDEC on Thursday, November 12, accelerated from 2.8% m/m in September to 3.8% m/m in October (chart 1). This was well above our 3.0% m/m forecast from two weeks ago; it also exceeded the market consensus, which drifted up from 2.8% m/m at end-October to 3.1% m/m by the time of yesterday’s print. October’s numbers took headline inflation up from 36.6% y/y in September to 37.2% y/y, the first rise in annual inflation so far in 2020 (chart 2). We have long forecast that annual inflation would begin rising in Q1-2021 on the back of monthly inflation at 3% m/m or faster; October’s print simply brings this projection forward by a few months.

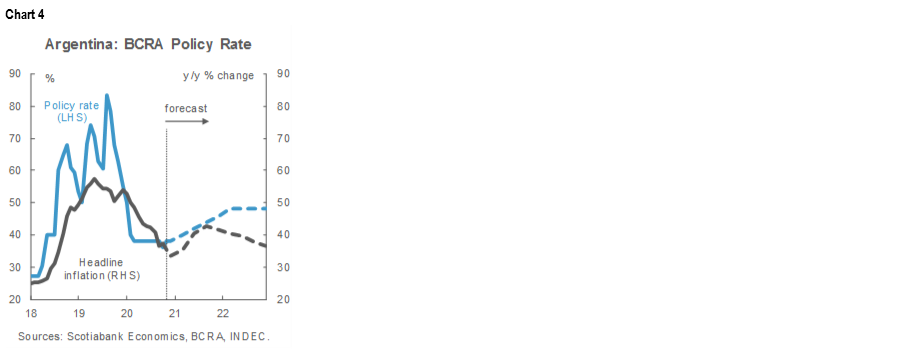

In the details, core inflation also picked up from 2.3% m/m in September to 3.5% m/m in October (chart 1, again), but this still allowed annual core inflation to come down from 38.3% y/y in September to 37.9% y/y in October (chart 2, again). Inflation in goods prices came in at 4.6% m/m, well above the 1.9% m/m increase in services (chart 3), which likely reflects intensifying pass-through effects from the weak ARS and what may be tactical efforts to bring forward goods imports to access relatively cheaper US dollars through the official market. Amongst specific sectors, clothing, food, and consumer durables prices led October’s gains, while communications and educational fees were close to unchanged.

Inflation is unlikely to slow down much in the coming months as FX pass-through effects, some loosening in price controls, and this year’s massive expansion in Argentina’s monetary base continue feeding through into price increases. Any rollback of price controls is set to reduce the artificial dampening effect regulated prices have had on headline inflation for over a year (chart 2, again).

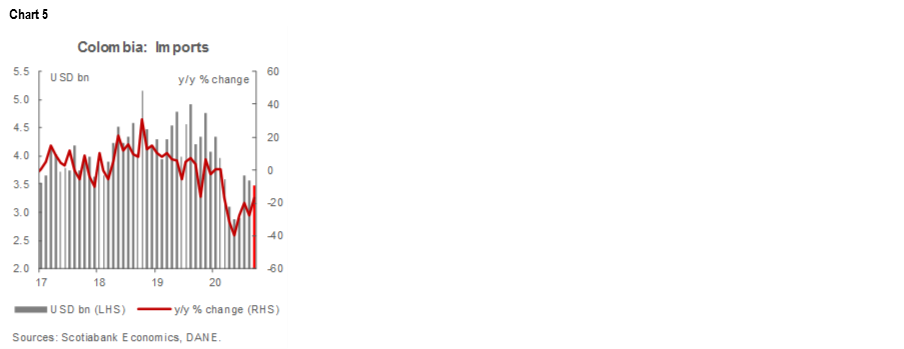

At least partially driven by October’s pick-up in inflation, on Thursday, November 12, the BCRA reversed recent cuts in its benchmark Leliq rate and raised it by 200 bps from 36.0% to 38.0% (chart 4). While the increase begins what we forecast will be a steady effort to take the real policy rate back into positive territory, it won’t be sufficient to stabilize the ARS: we continue to project more hikes ahead. Nevertheless, the BCRA’s rate increase was helpful in tandem with the Ministry of Economy’s commitment not to request any further transfers from the BCRA this year to finance its deficits.

—Brett House

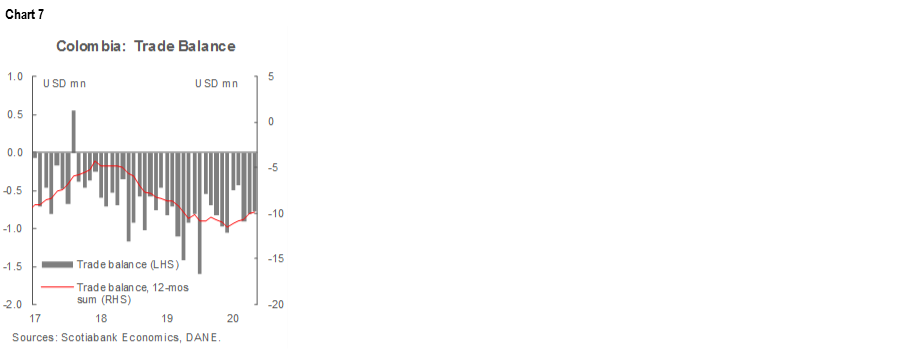

COLOMBIA: SEPTEMBER IMPORTS FELL BY -17.2% Y/Y, YTD TRADE DEFICIT NARROWED BY 11% Y/Y

September’s imports, released on Thursday, November 12, came in at USD 3.48 bn, down -17.2% y/y and slightly lower than August’s exports of USD 3.57 bn (chart 5). Manufacturing-related imports were off by -15.1% y/y and accounted for most of the year-on-year decline. Year-to-date, imports were still down by -20.4% y/y. The trade deficit narrowed by 16.7% y/y in September and 11% y/y YTD on the back of weak economic activity compared with 2019’s levels.

From the perspective of imports by use, there were declines in all three major segments (chart 6).

- Capital-goods imports were down -11.1% y/y due to contractions in construction-related sub-sectors (-46% y/y) and the agricultural sector (-17.7% y/y).

- Consumption-goods imports fell by -18.95% y/y, owing mainly to a significant decline in durable goods imports (-23.1% y/y), especially vehicles (-25.9% y/y); meanwhile, non-durable goods imports contracted by a more modest -15.56% y/y.

- Raw-materials imports were down by -20% y/y, mainly due to a drop in fuel oil imports (-48.6 % y/y) and imports for the industrial sector (-13.8% y/y) owing to weaker imports for mining industries (-21.5% y/y).

The trade deficit came in at USD -771 mn in September (chart 7), a 16.7% y/y narrowing that took the YTD deficit to USD -6.95 bn, down -11% y/y.

All in all, despite the fact that imports were down less in annual terms than in the previous month, import volumes remain at levels similar to those from five years ago, which is a clear testament to how much further the recovery has to go. The narrowing in the YTD trade deficit compared with last year was in line with domestic demand weakness and reflected the fact that September’s softness in imports offset the deterioration in export dynamics. All of these factors should help maintain the current account deficit at around -3.2% of GDP for 2020 as a whole.

—Sergio Olarte & Jackeline Piraján

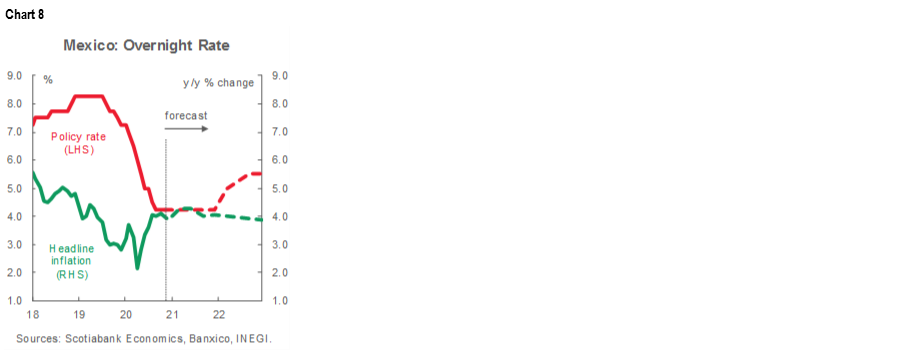

MEXICO: BANXICO HOLDS AT 4.25%; JOB GAINS IN OCTOBER

I. Banxico pauses easing cycle at 4.25%; we expect an extended hold

In its regularly scheduled meeting on Thursday, November 12, Banxico’s Board kept the Bank’s target rate unchanged at 4.25% in a split 4-1 decision (chart 8). Although the hold was aligned with our expectations, it cut against consensus views where about three-quarters of market analysts surveyed expected another -25 bps cut to 4.00%. In the end, one Board member did vote for a cut while the others elected, as the statement indicated, to “pause” the easing cycle.

The Board highlighted in its statement that market expectations for end-2020 inflation have risen, while medium- and long-term expectations have remained stable at levels above the 3% y/y target. Similarly, the Board noted that recent trends in headline and core inflation, and the factors that affect them, imply slight increases in its expected trajectories for inflation over the forecast horizon, although it is anticipated that during the next 12 to 24 months inflation will settle around 3% y/y. Still, the Board noted that the balance of risks for inflation remains uncertain, with factors implying both faster and slower price increases.

Taking all of this into account, we maintain our forecast that the Banxico Board shall keep its target rate on hold at 4.25% through end-2020 and onward through the end of 2021. Although the Board referred to its decision yesterday as a “pause”, it noted that this hold was intended to give Banxico the space it needs to confirm that inflation is on a trajectory to converge with the 3% y/y target. Given that we forecast headline inflation remaining at or above the 4% y/y of the target range through 2021, we believe the Board’s “pause” is, in fact, a longer-term hold.

Looking ahead, the minutes of yesterday's meeting will be published on November 26 and the next monetary policy decision is scheduled for December 17. In addition, the July–September 2020 Quarterly Report will be published on November 25 and will update the Bank of Mexico's quarterly inflation forecasts.

II. Formal job creation rose for the third month in October, in line with Banxico’s most recent survey of expectations

In data released on Thursday, November 12, by the Mexican Institute for Social Security (IMSS), formal job creation rose in October for the third straight month. The month saw a gain of 200,641 new jobs, the largest increase for any October since current records began in 1998. That said, October’s gains mark only another partial step in recovering losses from earlier in the year. The first ten months of 2020 saw the elimination of -518,609 positions while an even greater -824,591 jobs were lost over the last twelve months—the biggest losses on record (chart 9). As a result, job creation remained down -4.0% y/y in October, the seventh straight month in which employment gains were below those of the same month a year ago. This marks the longest run of annual declines since 2008–09. On the bright side, the number of employers affiliated to the social-security system (1,003 million) increased by 1,208 employers in October, but this still left the total down -0.1% y/y compared with October 2019.

IMSS also reported a nominal increase of 7.7% y/y in the salaries of workers who contribute to the social-security system. This was little changed from September’s 7.6% y/y nominal gains, but it made for the strongest nominal salary increases in the month of October since 2010. In real teams, annual salary growth remained stable at 3.4% y/y.

In line with October’s positive evolution in the labour market, the Banxico survey of economic expectations for the month showed an improvement in analysts’ outlook for jobs. Survey respondents now expect a loss of -900,000 jobs in 2020 versus -950,000 in the September survey; similarly, analysts now expect the end-2020 unemployment rate to be 5.54%, down from the previous consensus of 6.11%. Regarding 2021 forecasts, analysts’ expectations of an upturn in job creation remained unchanged at a gain of 350,000 positions and the projected end-2021 unemployment rate came down from 5.07% to 4.87%.

—Miguel Saldaña

PERU: NEW CABINET APPOINTED AS THE BCRP STAYS ON HOLD

I. Experienced new cabinet may help the government gain economic, but not political, credibility

The new Merino government’s cabinet was sworn in yesterday, Thursday, November 12. The cabinet is headed by Ántero Flores-Aráoz (sworn in on November 11). His experience during five stints as a member of Congress makes him a capable politician. He is a conservative in terms of his social and political views, but his grasp of economic issues is, perhaps, less reliable.

José Arista was appointed Minister of Finance. Arista has considerable experience in public office, having been Minister of Agriculture during the Kuczynski administration, Governor of the Amazonas region (2011–14), and Director of the Treasury at the Ministry of Finance at one point, in addition to holding different directorship positions at the Central Bank (BCRP), the Inter-American Development Bank (IADB), the CAF (Corporación Andina de Fomento), among other institutions. He has a decently solid economic background, including a master’s degree from UCLA. Judging from his past performance, his economic thinking appears to be broadly pro-market, but with liberal (as opposed to conservative) tendencies. His strength is in day-to-day management: he understands how to run a large organization and operationalize policy. But he will need to demonstrate a willingness to take strong stances against populist initiatives emanating from Congress, especially as he may not always have the backing of cabinet chief Flores-Aráoz or of President Merino in this regard.

Another key position that has been filled by someone who is largely viewed as adequate is Abel Salinas at the Ministry of Health. Salinas was previously Health Minister in 2018 during the Kuczynski government, albeit for a short four months. However, he has also been a member of the National Health Council and advisor to the Ministry of Health.

Viewing the Flores-Aráoz cabinet as a whole, its main strength is that it’s quite experienced. Thirteen of the 19 members of the cabinet have held high executive positions in public office and others have held advisory positions. This bodes well for operational management. In particular, the period of slackened fiscal spending and delays in decision-making that typically occurs after a change in government may be shorter than feared, especially at the Ministry of Finance.

Another plus of the new cabinet is that there appears to be very little linking it to current members of Congress. In short, this is not an overly political cabinet: few of its members belong to a party and many are more clearly linked to past administrations than to the parties that dominate the current Congress. Hopefully, this will mean that the Merino government will be less beholden to Congress than we have feared.

On the other hand, this is not the broadly-based cabinet that President Merino had promised. The impression one gets is that this is a second-best collection of appointments and that Flores-Aráoz, having failed to attract the ideal Ministers he would have preferred, looked back in time to see which veteran policymakers were both competent and available.

The bottom line is that this new cabinet appears to be fairly reasonable. But, it is unlikely that this will be enough to award the Merino government the credibility or sheen of legitimacy that it needs. Where the cabinet could possibly gain some luster more quickly is in its handling of the economy. The Ministry of Finance under Arista is not likely to be a source of populist, unorthodox, or otherwise questionable economic policy; but, prospects for the rest of the cabinet are a bit less clear. The big question that remains is how this cabinet—and the Ministry of Finance in particular—will behave when faced with difficult initiatives emanating from Congress.

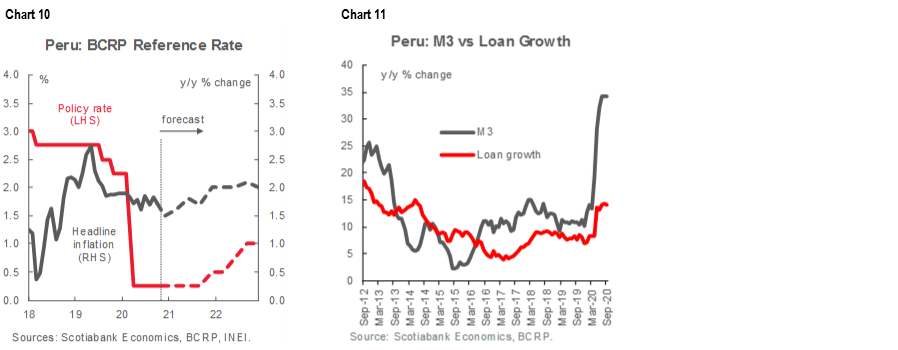

II. Peru’s BCRP kept its reference interest rate unchanged at 0.25% for a seventh consecutive month, in line with market expectations

In its scheduled monetary-policy meeting on Thursday, November 12, the BCRP’s Board decided to keep its benchmark policy rate on hold at 0.25% (chart 10), as expected by the market consensus. In its statement, the BCRP maintained the tenor of its communications following its October 7 meeting, with its focus on the provision of liquidity. However, recent increases have so far been marginal and the BCRP made no mention of additional new measures to boost liquidity further. Total injections reached PEN 61.7 bn (8.1% GDP) as of November 11, a level similar to the PEN 60.5 bn recorded a month ago. Within November’s total, state-guaranteed lending operations amounted PEN 50.2 bn, up from the PEN 47.8 bn level reported a month ago. During the last two months, the pace by which Reactiva funds have been allocated has slowed down significantly. Nevertheless, credit to the private sector still grew by 14.1% y/y in September (chart 11).

Regarding inflation, the BCRP’s Board continued to adjust its outlook upward. The Board now believes that inflation in 2020 and 2021 will land in the lower part of the 1% y/y to 3% y/y range around the 2% y/y target, rather than at the lower limit of the range, as the Board had anticipated in its October statement. This is in line with our forecast of 1.5% y/y with an upward bias for end-2020.

Still, the Board kept its forward guidance and related signals unchanged. It continued to note that a strongly expansive monetary stance will be appropriate for a prolonged period while the effects of the pandemic continue to weigh on inflation and its determinants. The Board remained ready to expand the monetary stimulus it is providing to the economy using diverse instruments, if necessary. We continue to see the Board maintaining its key policy rate at 0.25% until Q4-2021.

In the near term, we see the BCRP being very active in managing pressures on the PEN derived from the current period of political uncertainty.

—Guillermo Arbe & Mario Guerrero

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.