ON DECK FOR THURSDAY, JANUARY 21

KEY POINTS:

- Euro takes ECB in stride

- ECB repeats guidance that PEPP may not be fully utilized

- A$ shakes off on-consensus Australian job gain

- Norges continues to guide toward a rate hike in early 2022

- BoJ, BI, Turkey, SARB all stay on hold as expected

- US readings point to resilience amid rising COVID-19 cases

- Further insights from Macklem’s interview

INTERNATIONAL

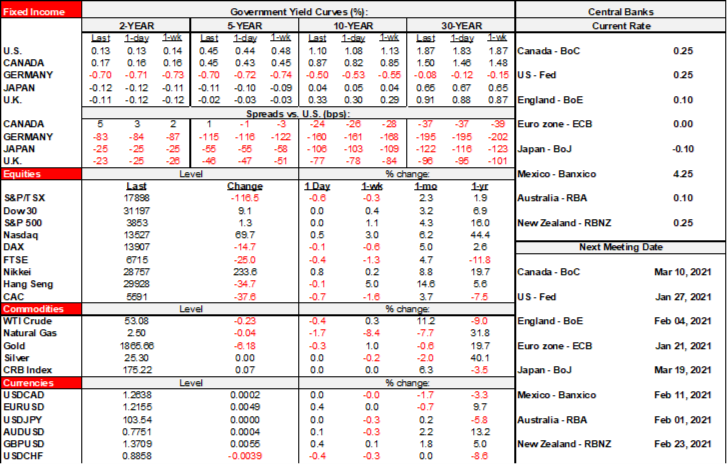

Absent major catalysts for substantial moves, the S&P500 is flat, the TSX is down by ¾% and European cash markets closed slightly lower on balance. The USD is softer against several currencies this morning, but CAD is flat because it was in the spotlight yesterday. Sovereign curves are steeper with 10 year yields up by 3bps in the US and UK, a little more in Canada, and 7bps cheaper in Italy where spreads are widening over bunds.

The ECB left all policy variables intact as expected this morning. The statement (here) merely codified what President Lagarde said during the December press conference about potentially not using all of the room in the Pandemic Emergency Purchase Program (PEPP) and so there was nothing new and the euro shook it off. Recall that the ECB expanded the PEPP at the December 10th meeting and then Lagarde spiked the euro during the press conference when she said the following that was codified in today’s statement:

“If favourable financing conditions can be maintained with purchase flows that do not exhaust the envelope over the net purchase horizon of the PEPP, the envelope need not be used in full. Equally, the enveloped can be recalibrated if required to maintain favourable financing conditions to help counter the negative pandemic shock to the path of inflation.”

The A$ shook off an on-consensus Australian jobs report that posted a 50k increase last month that was primarily driven by full-time jobs. The unemployment rate continues to drop from a peak of 7.5% in July to 6.6% now which should encourage the RBA.

Each of the Bank of Japan, Bank Indonesia, Turkey’s central bank and the South African Reserve Bank held policy unchanged as expected. Norges Bank also held at 0% and continues to guide toward a first hike in early 2022. The BoJ offered very minor forecast revisions that, to the surprise of few, show inflation going nowhere fast.

UNITED STATES

US macro reports were rather strong this morning and indicated greater resilience than one might have expected in the face of rising COVID-19 cases.

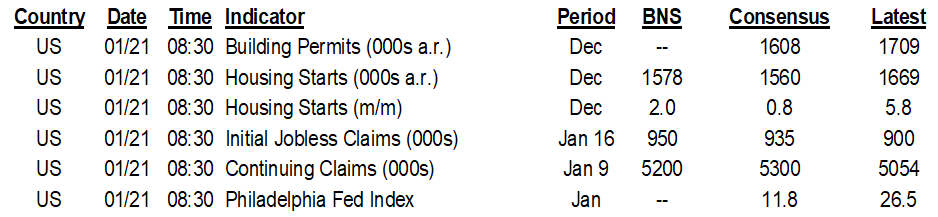

- Housing starts were up 5.8% m/m in December (0.8% consensus) and revised up to a 3.1% gain the prior month from a 1.2% initial print. Building permits suggest there is more to come as they soared by another 4.5%.

- The Philly Fed’s metric far surpassed the brave few who attempt to forecast this random number generator. The headline gauge climbed to 26.5 (11.1 prior). New orders soared to a reading of 30 (1.9 prior) which indicates rapid expansion. Employment picked up to 22.5 (5.6 prior) which indicates accelerated hiring activity. Prices paid (45.4 from 24.9) and received (36.6, 16.1 prior) suggest more cost pressures and pricing power.

- Jobless claims also fell back to a still elevated weekly initial claims reading of 900k with downward revisions to the prior week that is now marked at 926k (from 965k). Continuing claims also fell to 5.054 million from a downwardly revised 5.181 million (5.271 million initially).

US earnings will grind on. Intel in the after-market is perhaps the highest profile company.

CANADA

Governor Macklem’s virtual print interview with Bloomberg is available here or on your terminal. My recap of the BoC’s actions yesterday is available here. I thought it was a useful interview that shed more light on additional topics. I’ll try to capture the essence of what Macklem said and add some interpretations to consider along the way.

1. Quantitative Easing

The taper hints that were in yesterday’s statement, Macklem’s opening remarks to his press conference and during the press conference itself were reinforced in the Bloomberg transcript where Macklem said:

“If the economy plays out in line or stronger with our outlook, then the economy is not going to need as much QE stimulus over time. If things play out largely broadly as we expect, we are not going to need as much QE over time”

This quote reinforces the bias in favour of additional steps toward tapering purchases, but the issue is how to interpret what Macklem means by “over time.” One immediate inference is that it reinforces the natural expectation it will be a gradual process rather than a sudden one, but timing the steps is the key.

I think that if the BoC’s assumption that lockdowns end next month is proven correct and that rebound evidence is beginning to shine at the same time vaccine roll outs are rapidly accelerating then they may find that they have the conditions for further tapering to occur starting as soon as this Spring and maybe as soon as around the April MPR. The BoC continues to encounter supply challenges further up the shorter end of the curve as Roger Quick has been emphasizing and that was what motivated their first decision to successfully taper and extend purchases late last year. Also recall that Macklem has said the BoC would end QE before the output gap shuts; our forecasts show the gap shutting by mid-2022. That being the case, ending QE, say, 6 months in advance may be appropriate. If so, then perhaps multiple tapering steps to the present C$16 billion per month or more of GoC purchases may be appropriate and starting sooner rather than later instead of turning off the taps more suddenly later in the year or early next year.

I also think that as part of this the BoC should consider ending its other main bond buying program (the Provincial Bond Purchase Program) when it is presently slated to expire at the end of May anyway. The goal of the QE programs was to add other forms of stimulus when at the lower bound on the policy rate and to offset a liquidity drain from a shock-induced surge of issuance. Today, the improved outlook offers less motivation for such programs that should be the first to roll off well ahead of hiking the policy rate and liquidity has been vastly enhanced by the enormous expansion of global central bank balance sheets. It is not the business of central banks to, instead, enact measures that prevent bond yields from adjusting in an improved outlook independent of a very good reason for doing so. Provincial bond yields are low but still relatively attractive compared to multiple other jurisdictions (chart 2).

I’d also like to remind the reader that from what I recall, there were many arguing against our recommendation that the BoC would buy provincial bonds when they first rolled out the program. Their main opposing argument was that the market was functioning and issuance was occurring so why have the central bank potentially court market dysfunction by stomping all over the provincial bond market. They can’t now have it both ways by pleading for such programs to continue when some never wanted them in the first place. Besides, the program is barely being utilized with only about $15 billion of provincial bonds purchased in a $50 billion facility.

2. CAD

I have to admit that I’m unclear about what the BoC is trying to say on the currency. Put another way, I see it very differently. First, here is what Macklem did say this morning.

“To the extent that is weighing on our forecast and dampening growth in Canada, everything else equal, we’d need more monetary stimulus to get back to our inflation target”

“Particularly in a a situation where our Canada-U.S. exchange rate is moving largely because of made-in-U.S. developments as opposed to made-in-Canada developments. So in this situation where we’ve seen this broad-based US dollar deprecation that doesn’t reflect some positive development in Canada that the exchange rate is absorbing”

“In that situation, the exchange rate is starting to create a material headwind for the Canadian economy”

Macklem is basically implying that the BoC sees CAD strength as a reflection of US dollar weakness in such fashion as to risk imposing unwanted tightening on Canada's economy.

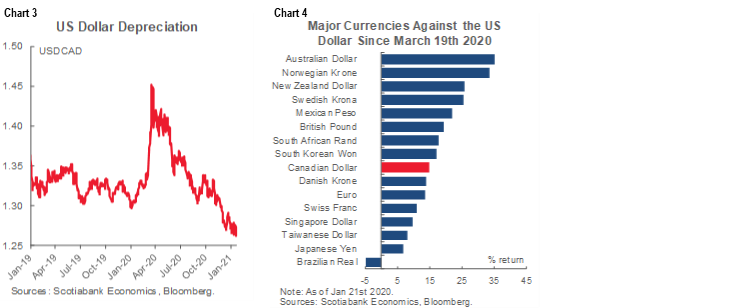

Now consider charts 3–4. My issue is with the portrayal of what has happened to the currency and the implied points about the drivers. Chart 3 makes it clear that the currency is only a handful of pennies (about 3%) firmer than it was before the pandemic struck. While it depreciated massively into the March–April pandemic shock, it has since only recouped all of that and a few cents more. Chart 4 shows that this movement since March has been uneven against other crosses such that on a full trade-weighted basis the C$ has not appreciated by as much as it has against the USD. I don’t think the Governor should be worried about a currency that is just a few cents firmer than it was before the pandemic with the kind of growth outlook they and we are forecasting, but that’s roughly the right time frame to utilize. Long lagging movements in the currency along a 1+ year timeline are generally viewed by most as required in order to materially impact forecasts for things like inflation or trade and when judged in that time frame the currency has barely moved. For inflation pass-through purposes, tracking begins to be worthwhile when it’s a sustained 10% trade-weighted appreciation, and even those pass-through estimates have fallen over time and are more likely to be dominated by other drivers of inflation going forward. To even begin to get toward that point in a pre-pandemic versus now sense would require the currency to punch below 1.20 USDCAD (1.264 now).

Second, why has it moved? The BoC no longer talks of type 1 and type 2 drivers of currency movements and certainly no longer speaks to the monetary conditions index of old. But there is nevertheless strong merit to consider the drivers of currency movements when judging whether they impose net tightening on the economy. The reason the USD has dropped so sharply since March is likely first and foremost a reflection of the recovery in global risk appetite that also benefited higher beta crosses like CAD. That oil prices have risen is another reflection of this and of pertinence to a currency that is part of a basket of FX crosses perceived to be petro-currencies. I wouldn’t call that unwanted appreciation that imposes aggregate tightening.

Even if it were tightening on net of the improvement in risk appetite toward a better outlook, shouldn’t that too be alright? My bias is that policy is overly loose in the face of where we are going in future so the currency should be imposing net tightening on the nation’s terms of trade. The BoC can’t have it both ways by hoping trade competitiveness doesn’t suffer a price offset to the expected pull-effect from growth abroad, while it jacks up the domestic interest sensitive sectors that play a dominant role in driving its forecast for strong growth.

3. Effective Lower Bound

What does Macklem mean by the following quote?

“When we set the effective lower bound at 25 basis points back in March and April, markets were disrupted. Today, markets are working much better, market functioning is much improved and I think that does make the possibility of lowering the effective lower bound to something that is still positive and lower than it is today. That is a more viable possibility.”

I think his point is that they didn't want to maintain the pre-pandemic guidance that they thought the ELB was -0.5% as the pandemic struck because the time to experiment wasn't when financial markets were already in a state of upheaval. They feared being pushed by markets in that direction right away if they indeed indicated openness toward going negative and that in the context of financial market disruptions they didn't think it would be appropriate to add uncertainty over the financial system's ability to absorb negative rates. So they drew a line in the sand.

Now, he's saying that absent such strained conditions in financial markets, the worries about testing the lower bound are not as acute and so if the fundamentals were to require a lower bound than 0.25% absent a disrupted financial system then they could consider it. But it's still not part of their base case and he still isn't signalling a willingness to go back to negative on the ELB.

4. When to Hike & the Strategic Review

Governor Macklem’s quotes could be taken as indicative of a willingness to let inflation overshoot and have the policy rate lag the pick-up in inflation..

“That reflects our risk management framework, where we are taking out a little bit of insurance that we really don’t want to see inflation go any lower. We are aiming for 2% but we are going to use the band and we are going to use the risk management framework to get there as quickly as possible.”

One discussion I have with clients is that even if the Governor is implying a make-up and work-the-band strategic approach, that is not incompatible with starting to raise the policy rate next year when the output gap is likely to close and inflation returns to 2% or slightly above. They can still have a bias toward working the bands that may include a willingness to overshoot for a time in order to make up for past shortfalls because the issue that would govern the starting point to tightening should be inflation risk, not actual inflation per se.

Inflation risk will likely be perceived differently by the BoC when they are on 2% than when below and that's what could well motivate them to hike even if they want an overshoot. Inflation risk would be more balanced at that point versus the present bias to be more worried about staying below the inflation target. If that's the case, then you start to transition away from emergency stimulus because inflation risk has gone down. That was former Governor Carney's playbook from 2010 when he went up 75bps to 1% and stayed there as it turned out for years through a bunch of other problems like the Eurozone debt crisis. This time around the BoC could still argue that there may be merit to staying cautiously below the neutral policy rate that they peg in a 1.75%–2.75% range for a time in order to err more on the side of ensuring that inflation stays on target with or without a make-up bias. If after one or two hikes in 2022 the policy rate is still set below the BoC's estimated neutral rate then the BoC would still be erring in the direction of being open to an overshoot but it would begin the process of transitioning away from emergency conditions.

Nevertheless, the catch is that while the BoC has said similar things for years (ie: symmetrical target around 2% with +/-1% bands), they've always implemented the framework in an asymmetric fashion by tightening the minute they think they are at 2% or on the path. That's why they've fallen below target two-thirds of the months since 2010 on headline inflation and 94% of the months since 2010 on avg core. It's also why inflation expectations are moored below the 2% target and have been for ages (RRB b/e and surveys). Markets expect them to operationalize the bands by treating 2% as the ceiling and so naturally it would average out somewhere beneath. So, I doubt they change the framework per se and I'm skeptical that they will fundamentally alter how they operationalize it if/when we get to 2% or a tad beyond (which we have in 2022H2).

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.