ON DECK FOR WEDNESDAY, JULY 22

KEY POINTS:

- Equities slightly weaker on stalled US stimulus, China tensions

- US home resales soar, but fresher housing readings are ahead

- Canadian inflation firmer than expected…

- …amid multiple reasons to ignore it

- Reaffirming the Canadian retail recovery

- Don’t expect much out of next week’s FOMC

INTERNATIONAL

Global markets are in mild risk-off mode so far. There may be two catalysts in addition to simple noise that defies the quest to always have an explanation at the ready.

US stocks began slipping into the close yesterday when more negative headlines began to hit on how US stimulus discussions were in disarray. Some of this renewed concern over US stimulus plans spilled over into the overnight Asian and European sessions including through US equity futures. Selling pressure recommenced in two bouts during the Asian overnight session and before the headlines hit on how the US apparently told China to shut its consulate in Houston “to protect American intellectual property and Americans’ private information.” The order followed mysterious fires to burn papers outside the consulate yesterday. China vows to retaliate but was silent on how and when.

I’d place the disarray that appears to govern the US fiscal stimulus plans as a more important driver of today’s market movements. Maybe a WSJ piece on how the Fed might sit on its hands through the rest of the summer isn’t helping either.

US home resales were strong, but reflect decisions made before rising covid cases in some parts of the US. Canadian CPI was a bit firmer than expected, but with little cause for paying much attention.

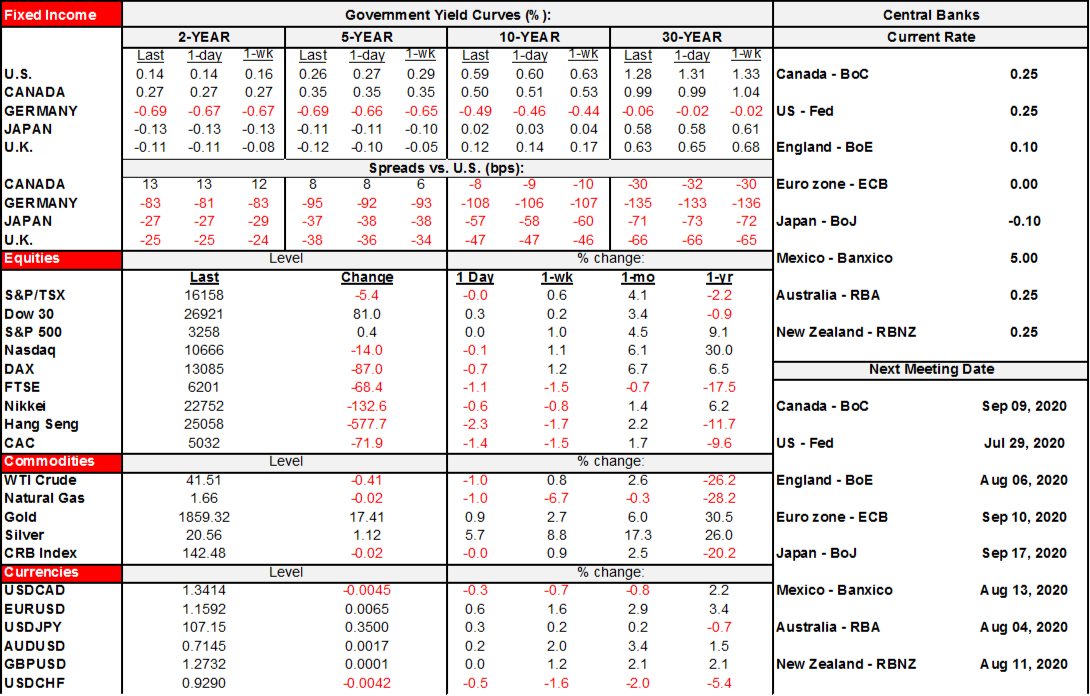

- Stocks are somewhat mixed. European equities are down by ½% to 1½%. They are probably catching up to the sell off in North American equities into the final hour yesterday when markets reined in assumptions about progress toward achieving another US fiscal stimulus bill. Ditto for Asian equities that saw HK down 2 ¼%, a mild decline in Tokyo and a mild gain across mainland China’s exchanges. US and Canadian equities are little changed this morning.

- Sovereign curves are slightly bull flattening. Ten year yields are down by 2–6bps across The US, Canada and Europe with Italy continuing to lead the decline after the EU achieved its stimulus agreement.

- Oil prices are off by just over 1%.

- The USD is little changed on balance as the euro rises along with lesser appreciation in CAD and the A$ versus flat sterling and mild depreciation in the yen.

UNITED STATES

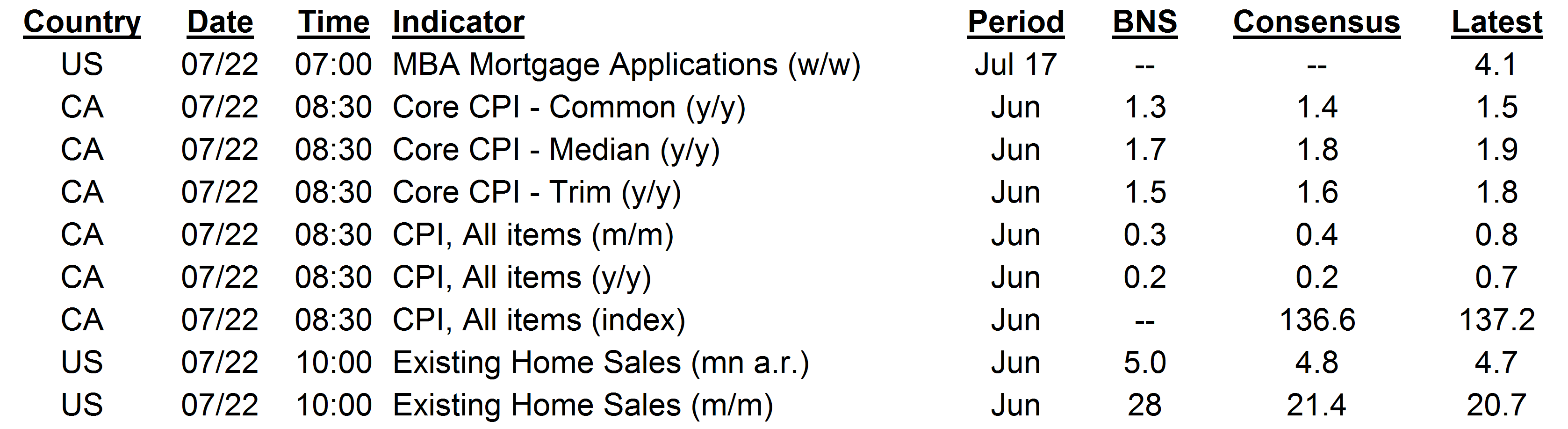

US home resales climbed in line with expectations. Sales were up by +20.7% m/m (21.4% consensus). I was a little higher at 28% m/m. The uncertainty was over the exact distribution of the huge gain in pending home sales during May that close 1–3 months later. It will be the gift that keeps on giving next month when the rest of the sales close. Single family homes sold were up 20% m/m and multiples were up 29%. Months supply fell to 4 which is fairly tight.

How housing is holding up in the face of covid-19 cases will be better informed by Friday's new home sales. Contract signings, so fresher take on current sentiment rather than lags in when resales close months later. Next week we also get June pending home sales that will also be a bit fresher than what we got today.

This WSJ piece on the Fed may also be of interest. It basically says not to expect any material changes at next week’s FOMC meeting. That includes no changes yet to forward guidance or alterations to purchase plans just yet versus potentially later in the year once the Fed has more evidence on the virus and the recovery. In other words, the Fed is like the rest of us in the markets! What’s unwritten may also be that they want to see if Washington can pull a rabbit out of its hat with another stimulus bill that averts cliff effects.

CANADA

Canada registered a slightly firmer set of inflation readings than expected that were largely ignored. In one sense it’s dicey to ignore fresh evidence, but in this case there may be legitimate reason for doing so as explained below. It is less legitimate to dismiss yesterday’s massive strength in retail sales during May and June (recap here). We all know there are forward looking risks. But when the evidence points to a stronger and faster than expected recovery, it’s called confirmation bias to reject it in favour of one’s prior that it simply cannot happen.

Canada, CPI (m/m % NSA ; y/y % NSA), June:

Actual: 0.8 / 0.7

Scotia: 0.3 / +0.2

Consensus: +0.4 / +0.2

Prior: Unrevised from 0.3 / -0.4

Canada, Core Inflation, y/y %, June:

Average: 1.7 (prior 1.6)

Weighted Median: 1.8 (prior 1.9)

Common Component: 1.5 (prior 1.4)

Trimmed Mean: 1.8 (prior 1.6 revised from 1.7)

The C$ and short-term market rates rightly ignored a modest upside to expectations for inflation readings for the month of June as the Bank of Canada is likely to do so as well and with considerable justification for doing so.

Headline inflation climbed by more than anticipated and core inflation edged up a tick to 1.7% from a slightly revised average of 1.6% in May (chart 1).

The main reason the BoC would ignore the release is that it’s too soon to expect most of the adjustment lower in the core measures. As spare capacity has ballooned, more of this lagging effect is likely to come with a 3–5 quarter lag which is one reason behind why we expect the average ‘core’ measure to dip below 1% y/y toward year-end into early 2021. The BoC is likely to remain anchored to this longer run view and dismiss short-term readings. If we have firm—let alone higher—core inflation along that time frame then that would obviously be material information, but we don’t have that today.

There also remain data quality issues that provide ongoing reason to be skeptical toward the exact estimates. For example, prices for suspended flights are still being excluded and replaced by imputed readings for some parts of the air transportation index. Alcohol prices are being imputed with several regions still restricting access (bars etc). Out-of-stock items continue to have their prices imputed. Prices at temporarily shut businesses continue to be imputed. This series of points isn’t meant to imply that StatsCan isn’t doing its best to adapt to unique challenges, but judgement in the face of such question marks surrounding data quality should lead markets to put a filter on the estimates.

With these caveats in mind, here were the drivers in the short-term:

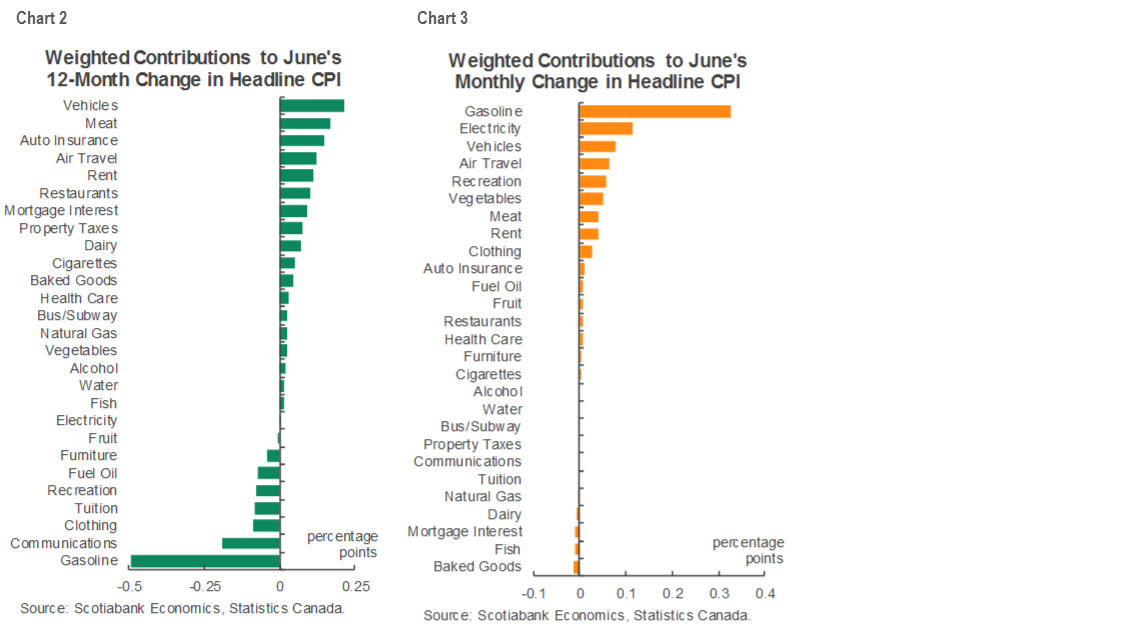

· Charts 2 and 3 break down the weighted contributions to year-over-year and month-ago inflation to give a sense of where the pressures to the upside and downside are coming from.

· Electricity prices spiked higher because they increased by 17% y/y in Ontario for the biggest rise since May 2003 as a result of higher prices that were introduced on June 1st. In month-ago terms this driver should drop out in July but will continue to impact the year-over-year readings until June 2021 barring further policy changes. Chart 4 shows electricity price inflation along with what at times have been other transitory drivers. For instance, mortgage interest cost is finally turning lower and with more to come given the lags to policy rate and market rate changes.

· Gasoline prices rose in month-ago terms and fell at a slower pace in year-ago terms, in line with our tracking based upon market prices (chart 5).

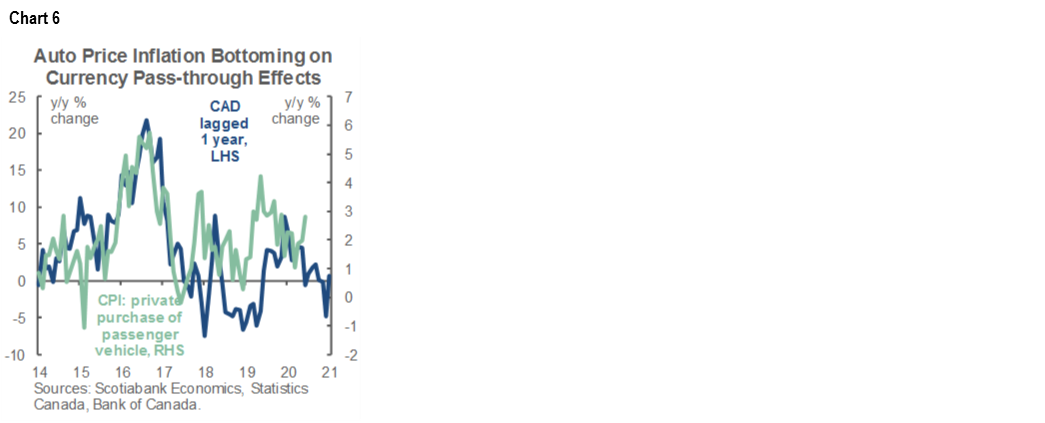

· I’m a little surprised by auto prices and had not factored a mild positive contribution to higher inflation from that part of the basket. As chart 6 shows, auto prices should follow the currency with a lag over time and yet they increased this time. It’s not an airtight relationship mind you. Strong sales momentum during May and June during the initial phase of the recovery was likely a driver of pricing power, but the relationship between sticker prices and USDCAD could reassert itself to the downside with a lag.

· Prices for clothing and accessories as well as the recreation/reading/education category posted less of a decline than previously.

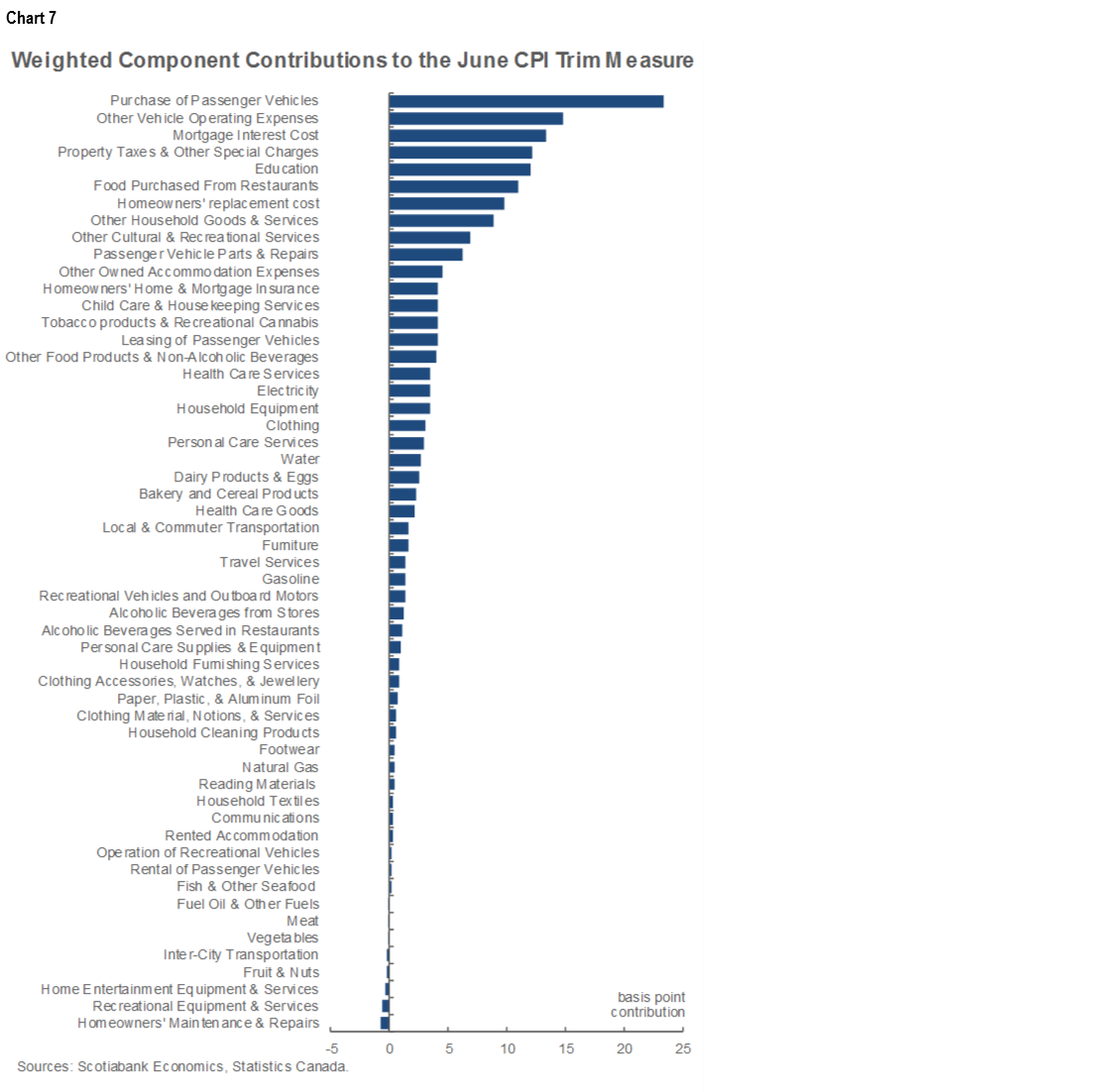

· Chart 7 shows the breakdown of what got included in the trimmed mean CPI core measure in June. The biggest outlier moves were excluded such that components like gas and electricity prices did not impact the core measure.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including, Scotiabanc Inc.; Citadel Hill Advisors L.L.C.; The Bank of Nova Scotia Trust Company of New York; Scotiabank Europe plc; Scotiabank (Ireland) Limited; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Scotia Inverlat Casa de Bolsa S.A. de C.V., Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorised by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorised by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V., and Scotia Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.