ON DECK FOR TUESDAY, DECEMBER 22

KEY POINTS:

- Markets calm down

- Brexit talks hit a new level of apparent pettiness

- US stimulus and funding bill awaits Trump’s signature

- US consumer confidence hints at nonfarm downside

- US home resales weaken

- US regional surveys are divided over ISM-mfrg risks

- US Q3 GDP left unrevised

- Canada: high health spending, few acute care beds

INTERNATIONAL

Markets are somewhat more stable so far this morning. Sterling is on the run again after the EU rejected the latest offer from the UK on how to manage access to fisheries (see below). The US stimulus and funding bill was passed by both chambers in Congress last night and it’s on its way to Trump’s desk with White House guidance he’ll sign it on a TBD schedule. Mixed in the middle was a medley of US releases that generally disappointed and reaffirm downside risk to the next nonfarm payrolls report.

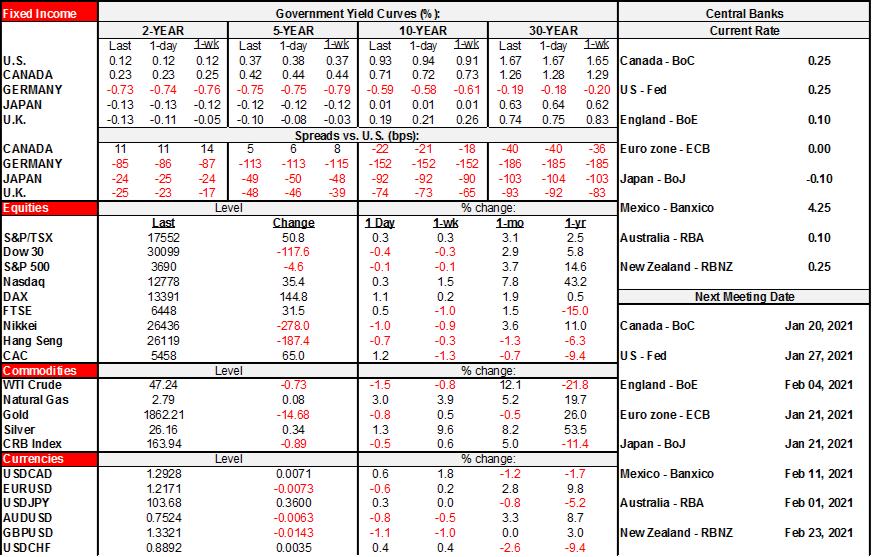

- Equities are in a generally more stable place so far this morning. The S&P500 is down a touch, while the TSX is up by under ¼%. European exchanges are up by as little as 0.4% in London to generally over 1% elsewhere.

- Sovereign bond yields are mildly lower across major markets. UK and Canadian 10s are outperforming by rallying by about 2bps with US Treasuries and core EGBs rallying a touch less.

- The dollar is rallying again. Sterling is the weakest cross with the A$/NZ$ close behind.

- Oil is down another 1½% and gold is flat.

5%. Just when you thought Brexit negotiations couldn’t get any pettier. The UK went all the way from insisting that the EU reduce its catch in UK waters by 60% over three years down to 30% over five years with yesterday’s proposal. The EU still rejected that offer this morning because it was higher than their demand that no more than a 25% reduction be imposed over seven years (down from 10 previously). Sterling sold off on the headline that dashed optimism that the UK offer could reignite talks. If 5% and a few years winds up in a hard Brexit on January 1st then businesses and households on both sides of the English channel should direct their anger at both London and Brussels for not simply sweeping 5% away and getting on with the business of avoiding a tariff wall in the middle of a pandemic in a little over a week from now. Of course there are other unresolved issues and as argued in the Global Week Ahead (here) there are legitimate reasons for the UK to defend access to its fishing rights, but getting this one out of the way would remove a major impediment to inking a final deal. An 11amET briefing call to be held by EU negotiator Barnier may further inform negotiations as well as other side negotiations and calls during the day.

UNITED STATES

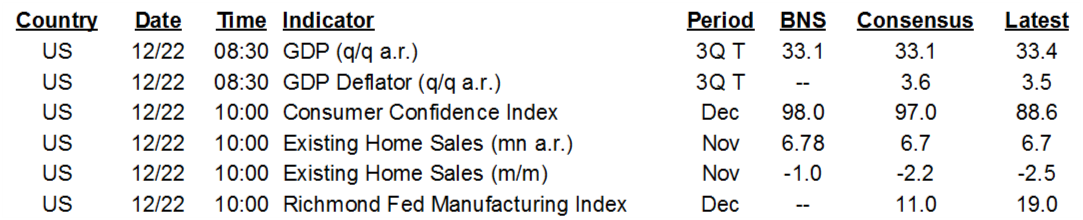

A series of low impact macro releases were largely pushed aside by markets.

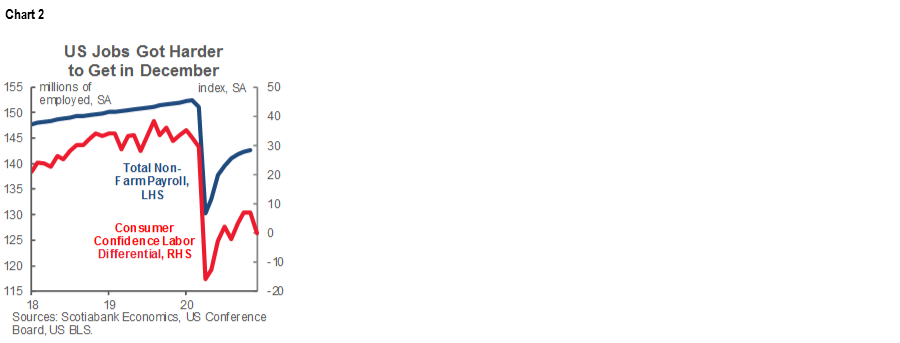

Consumer confidence unexpectedly fell in December according to the Conference Board. Well, unexpectedly at least given that expectations had been driven by the rise in the University of Michigan’s consumer sentiment reading as the second most watch gauge for consumer confidence. Instead, the two measures went in opposite directions during December (chart 1) which may speak to revision risk to the UofM gauge’s final estimate but might also speak to the greater weighting on labour market conditions in the Conference Board’s methodology. One wouldn’t, however, say that a decline in consumer confidence in an environment of rising COVID-19 cases and restrictions is particularly shocking. Each of the headline and present situation components fell, while the expectations component only increased because the prior month was revised down by about five points.

Note that the jobs plentiful subcomponent to the CB’s confidence measure points to downside risk to nonfarm payrolls in the December reading on January 8th (chart 2).

Existing home sales during November fell by 2.5% m/m which was in line with expectations given tracking of pending home sales that show up as completed resales when the paperwork settles within 30–90 days after the ink dries. Pending home sales for November arrive on December 30th and will inform expectations for the December resales print.

A positive sign shone through the Richmond Fed’s manufacturing index that unexpectedly climbed to 19 (15 prior) on the strength of a gain in new orders. That goes against the deterioration in other regional manufacturing surveys like the Philly and Empire gauges, but is consistent with the improvement in the KC Fed’s gauge. All four readings advance our understanding of manufacturing conditions on the path to the next ISM-manufacturing national print on January 5th that is set up to face possibly modest downside risk. Next week’s Dallas Fed reading will complete the regional surveys and I’ll firm up an ISM estimate afterward.

US Q3 GDP growth was essentially left unchanged at 33.4% (33.1% prior estimate). The break down of changes in weighted contributions to growth across the GDP components was uninteresting.

CANADA

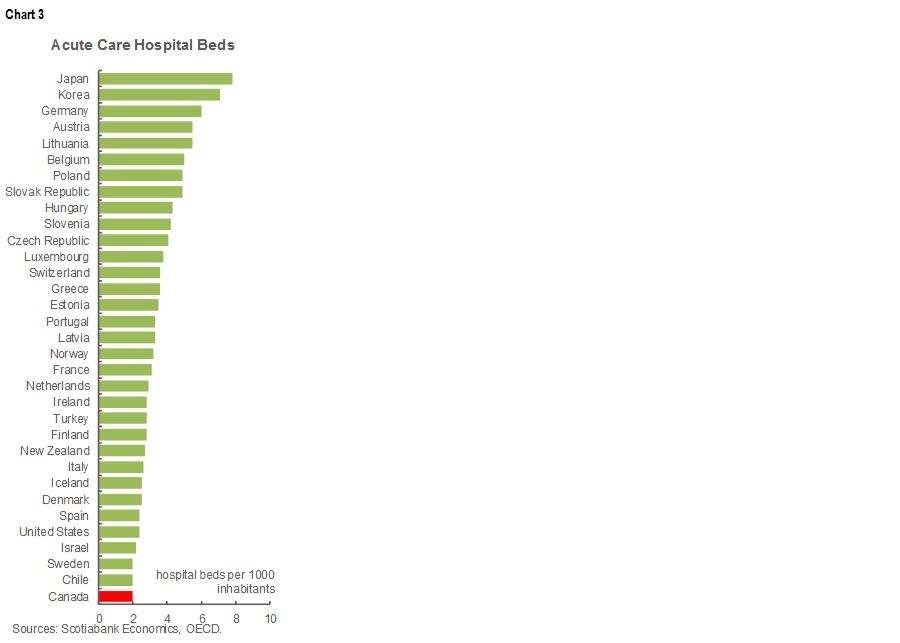

As for Canadians facing lockdowns starting this Saturday, I leave you with chart 3. It shows Canada ranked dead last in the OECD for acute care beds per capita. Take Ontario, for instance, with its population of almost 15 million people, yet only just under 2,200 ICU beds throughout the whole province of which 265 are occupied by COVID-19 patients. This isn’t because of a shortage of government funding to the overall health sector — or low taxes! — as Canada ranks above average on government/compulsory spending on health care as a share of GDP according to the OECD (here).

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.