ON DECK FOR TUESDAY, DECEMBER 23

KEY POINTS:

- Risk-on sentiment cherry-picks developments

- Brexit deal done for Christmas?

- Canada posts solid growth in October and November…

- …which gives a running start into renewed lockdowns…

- …ahead of vaccine effects…

- …with the BoC’s output gap still forecast to shut in 2022

- US jobless claims decline…

- …but consumers spent and earned less last month…

- …reinforcing stimulus requirements...

- …while Trump diverts attention from pardons…

- …by throwing the stimulus and funding bill into doubt

- US investment continues to rise strongly…

- …as housing slips

INTERNATIONAL

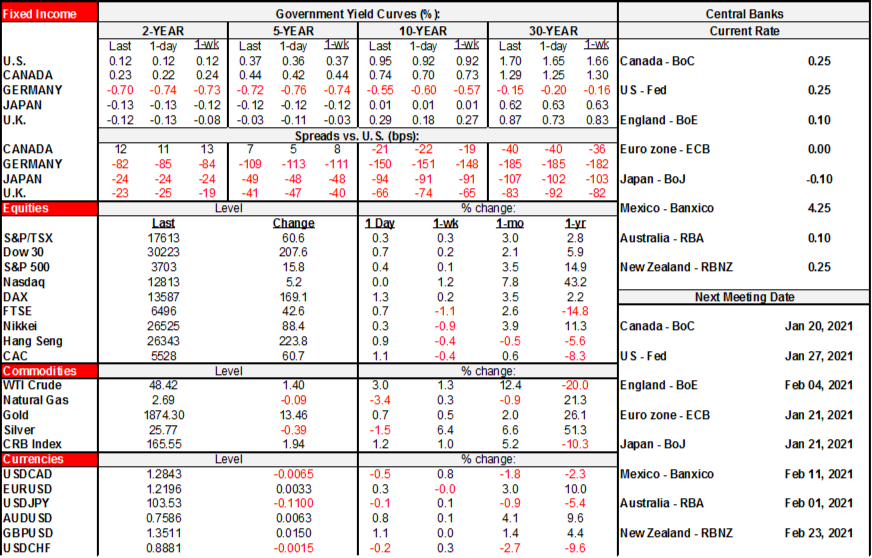

Risk-on sentiment is guiding markets so far today and it appears to be weighted more toward possible optimism toward a Brexit deal and the cherry-picked parts of US releases, rather than Trump’s reckless antics over signing the stimulus and funding bill as well as the weaker parts of the US macro releases. Bonds are getting hammered by the Brexit developments that may be striking a deal once and for all today, but with appropriate caution remaining. US releases favoured jobless claims and business investment over consumer spending and incomes as well as softer home sales. Canada’s economy beat expectations…again; see below for what it may mean to the BoC.

- Stocks are broadly higher. The S&P500 is up by around ½% along with the TSX’s slightly milder performance. European exchanges are up by between ½% and 1¾%.

- Sovereign bond prices are sharply cheaper. The yields on 10s are up by about 3–5bps across the US, Canada and across EGBs while the 10 year gilts yield is up 11bps and the 30 year UK bond yield is up 13bps. Brexit optimism is proving to be a major catalyst for a potentially violent bond move.

- Oil is up 3% across Brent and WTI.

- The USD is broadly weaker. Sterling is the strongest performer and is up by over 1% to the USD.

Trump sought to divert attention from pardoning sundry unsavoury types by suddenly showing interest in the stimulus negotiations. Good timing! Not. His protests risk tossing a lump of coal into American stockings. With the bill requiring his signature to fund the government and apply stimulus on his desk, he says he wants bigger stimulus cheques and less waste elsewhere in the bill. Everyone knows that waste is only good when it’s your pals that benefit from it. He didn’t explicitly guide whether he would veto the bill. Trump’s proposal to seek $2k/person cheques instead of $600 would increase the cost from $160B to $500B. There is some merit to that as downside risks mount in the near-term before vaccines and the economic impact would likely see some of it being spent, but much of it horded such that the saving rate would spike again into the new year. Pelosi—never one to pass up an opportunity to spend more—supports it and said the House would seek a standalone measure. McConnell and the GOP haven’t spoken out but I suspect they’d balk which is kind of funny because they’ve tended to previously think that steps like these pay for themselves…. Trump’s motives are never pure, so this could simply be an effort to front-run additional stimulus plans under a Biden administration and take credit before he gets deleted from the search criteria behind my automated rolling headline feeds, or he could be trying to rock the boat in the January 6th Georgia Senate run-offs. All one can say is grab another coffee and stay tuned…

Brexit talks are ongoing and headline volatility has been rather extreme this morning. While headlines have oscillated back and forth between a deal has been struck and advising caution, it seems that at the point of publishing the headlines and guidance from officials lean toward a decent chance of striking a formal agreement today.

CANADA

Canada GDP, m/m % change, October, SA :

Actual: 0.4

Scotia: 0.2

Consensus: 0.3

Prior: 0.8

November guidance: 0.4

Canada’s economy solidly beat expectations not only for the month of October but also in terms of preliminary guidance for November. There is obvious downside risk that is emerging from December through the winter months as lockdowns and restrictions bite once again, but it’s important to acknowledge that a) the economy has continued to perform better than many had thought possible right up to November, and b) the earlier than expected arrival of vaccines should lend greater confidence toward expecting a more sustained expansion.

GDP grew by 0.4% m/m and that doubled StatsCan’s initial guidance that had indicated an advance of 0.2% m/m. Preliminary guidance for November indicates the economy grew by another 0.4% m/m. We had advised that the tone of the data was looking solid on balance including hours worked as an offset to the late month lockdown in the Toronto area and restrictions elsewhere.

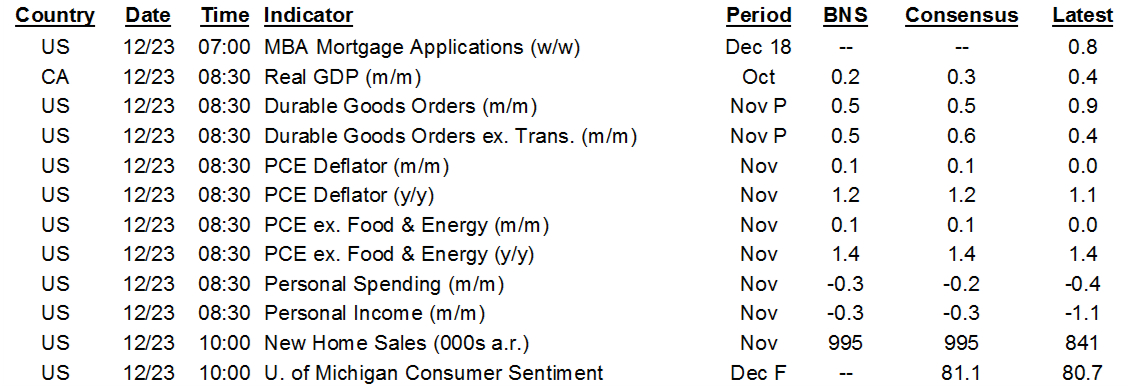

Current tracking for Q4 indicates GDP growth of 6.3% q/q at an annualized rate following 42% growth in Q3 using the monthly GDP figures. After contracting by 18% from February to April, the economy has now recovered 98% of the initial pandemic hit and it took just seven months to do so. We’ll see weaker figures going forward through at least December and January, but put this in perspective by noting that the portion of consensus that believed this would be a deflationary depression that would take a decade to recover from while walloping stocks has been absolutely dead wrong to date. The economy has rebounded faster than anticipated and core inflation remains sticky and just a few tenths beneath the BoC’s target.

Chart 1 shows the progress to date. Chart 2 shows where individual sectors of the economy now stand in relation to their output back in February in order to provide a depiction of the unevenness of the recovery. Some sectors like agriculture, finance, retail and real estate have more than recovered. Some barely remain in contraction like wholesale, public administration, info/culture, utilities, professional services and education. About a half dozen sectors are where the recovery still has a long way to go and particularly arts and recreation, accommodation and food services and transportation/warehousing.

So what does it mean to the BoC? On balance I still think Canada is on track to close spare capacity earlier than the BoC forecast in its October MPR as the tracking risks to their forecasts generally land on the more optimistic side of the picture on balance (chart 3).

For starters, Q4 is blowing the barn doors off the BoC’s projection, so far. The BoC had forecast 1% annualized Q4 GDP growth on an expenditure basis and at this point tracking is pointing toward over 6% using the monthlies. There are various reasons why the two GDP concepts may not line up, but they still leave us tracking a material overshoot of the BoC’s expectations.

Second, the arrival of renewed lockdowns will take at least some of that tracking for Q4 downward and set up a weaker start to Q1 which involves taking a step backward. What makes it more like ‘lockdown lite’ this time, however, include considerations like greater adoption of work-from-home practices, heavy tech investment, an accelerated shift to on-line sales and curbside pick-up alongside a vastly different stimulus backdrop both in terms of cheap financing and extended income supports.

Thereafter, however, the earlier than expected arrival of vaccines should buoy optimism as 2021 gradually unfolds. We obviously didn’t have that during the initial lock downs. Overall, vaccines and better Q4 tracking generally offset the resumption of downside risk in between the two effects.

UNITED STATES

US macro data was a bit of a mixed bag this morning. The state of the job market was a bit better than expected, but that was offset by weaker than expected income and spending figures. Big ticket business investment remains robust.

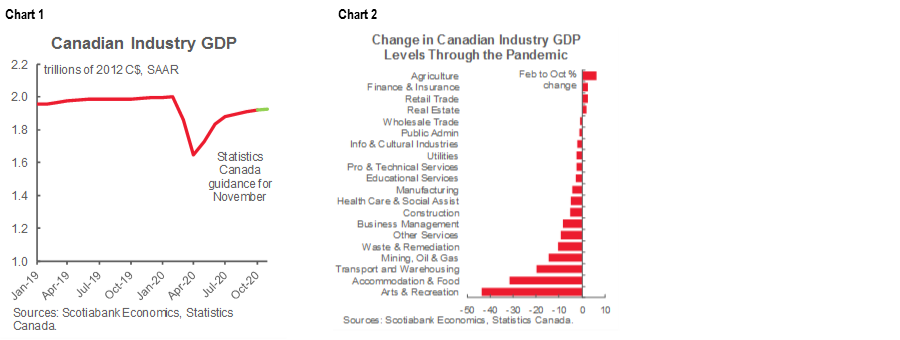

Weekly jobless claims were better than expected. Last week’s tally landed at 803k, down from a slightly upwardly revised 892k the prior week. Claims had risen for two consecutive weeks before reverting lower last week. Still, the pace of progress in initial jobless claims has definitely slowed between nonfarm reference periods which is the pay period including the 12th day of each month (chart 4). Even as jobless claims have seen flat lining trend performance, however, nonfarm payrolls have continued to expand.

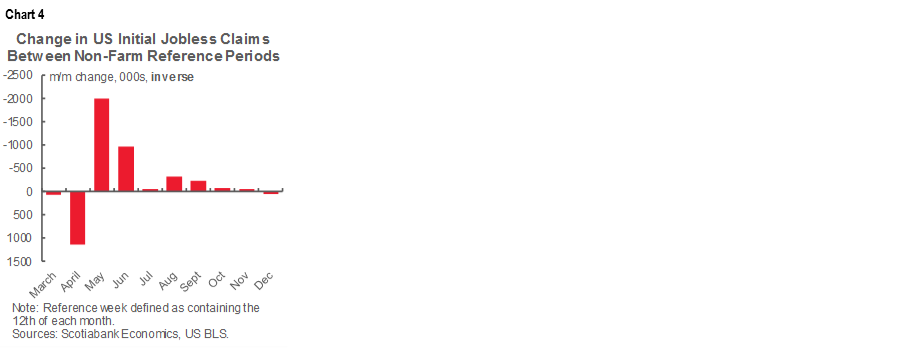

Big ticket durable goods orders also beat expectations last month. Core capital goods orders excluding defence and air are a proxy for broad investment in machinery and equipment and they were up another 0.4% m/m but more importantly the prior month’s 0.8% m/m rise was doubled after revisions. Core capital goods orders have risen for seven straight months now (trend in chart 5). The level of core orders (ex-defence and air) is at an all-time high as pent-up demand from trade wars and the pandemic is being unleashed (chart 6).

Alright apparently that’s enough of all this warm fuzzy holiday cheer, as it’s time for some sobering perspectives on how the consumer sector disappointed. November’s tally for incomes fell 1.1% m/m (consensus -0.3%) and the prior month was little changed at -0.6% m/m (from -0.7% initially). Incomes have fallen in three of the past four months as a portion of jobless benefit transfers ended in July. Dear Mr. President: Sign here. The impact on consumption was felt through a 0.4% m/m drop in November and downward revision to a 0.3% m/m rise in October (from 0.5%). In inflation adjusted terms, personal disposable income is tracking a 9% q/q annualized drop in Q4 while consumption is up 4¼%. The means the personal saving rate continues to decline from a peak of 33.7% in April to 12.9% last month.

The Fed’s preferred inflation readings were also a touch softer than estimated at 0% m/m for headline PCE inflation and 0% m/m for core PCE. That dropped headline inflation to 1.1% y/y while core held steady at 1.4% y/y.

Despite the fact that model home foot traffic held up as COVID-19 cases climbed, fewer than expected new home sales contracts were signed last month. A caution is that new home sales are often heavily revised. Sales fell 11% m/m to 841,000 homes last month. The Midwest saw a drop of over 40% m/m, the west census region fell by about 17% m/m, the south fell 2% and the northeast fell 2%. Months’ supply increased by half a month to 4.1 and has risen for a couple of months now off the lowest inventory position since 1998.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.