KEY POINTS:

- Landing on Santa’s naughty list reins in equity shorts

- And other more boring alternative explanations...

- …like Brexit and fish, US stimulus, WHO reassurances

- Ontario shuts down economy again

- US Q3 GDP revisions could slightly inform the hand-off to Q4

- US consumer confidence might have edged higher

- US home resales, Richmond on tap

TODAY’S NORTH AMERICAN MARKETS

Maybe fear of landing on Santa’s naughty list reined in equity shorts as the day went on. What started off as a bigger round of equity losses this morning when the S&P500 was down 2% from Friday’s close began to turn around by about 10:30amET such that the S&P500 ended only modestly lower. European exchanges generally followed a similar pattern but closed down by more than the S&P.

Catalysts for the diminished selling over the day may have included possible movement on the fishy issues holding up Brexit talks, the finalization of the US stimulus bill’s text and when the WHO came in and said there are no clear signs that virus mutations will cause a more severe disease or changed diagnostics or vaccine efficacy as testing trials set out to test this.

- The S&P500 ended down 0.4% with Toronto off by under ¼%. European exchanges closed down by between 1 ¾% (London) and about 3% (Spain). Recall that when this morning’s note was put out US, Canadian and European stocks were generally tracking bigger sell-offs.

- Ditto for sovereign bonds as they still rallied on the day, but generally reined in the magnitudes. For example, US 10s ended about 1bp lower (instead of 5bps this morning).

- The USD offered a similar picture. After hitting peak weakness with a decline of 1.2% on a DXY basis by around 5:30amET, the dollar then rallied to close only ¼% lower.

- And the same logic spills over into oil markets as the earlier 4% sell-off slightly diminished into the close with losses in Brent and WTI of about 3%. Gold still treaded water.

The Ontario government is the latest to extend aggressive lockdowns (details here). The widening in 10 year spreads today was comparable to Quebec and consistent with a general global risk-off tone (chart 1). At home and abroad, it’s unfortunate that with the better part of a full year for individuals to take preventative measures and governments to plan for second and potentially subsequent waves that it has come to this again notwithstanding heroic front-line and stimulus measures. Key this time around is that schools will be shut again as elementary schools will close for at least one week until January 11th and secondary schools will shut for a month. That is much less of a shock to the job market than back in the Spring when the kids were sent to on-line learning from March through June, but it is still going to carry negative consequences for the December and January job markets and especially for mothers given the experience to date. Parents with younger children may be able to adapt to a short-lived closure of in-person learning at elementary schools, but the risk of extensions to this guidance—given the pattern to date—is going to magnify uncertainty with respect to the ability to retain employment or hire new employees. Ditto for the closure of before—and after-school programs. The impact of shutting secondary schools depends on many individual considerations but a full month won’t be costless. Those who have already shifted to work from home may adapt easier than those for whom this option is not possible.

At this tentative stage, the lock downs and school closures will add downside to the way Q4 GDP ends as an offset to the positive tracking to date and set up a poor start to Q1 and the full-year GDP math. With the information we have to go by so far, the effects are likely to be transitory as activity picks up again in subsequent periods. They should be far less severe than in Q2 if the lock downs are more transitory and given the growth in work from home options, heavy tech spending, a more aggressive push into on-line sales, greater experience with curbside pick-up and home delivery and established support programs to replace a part of lost income especially for lower wage earners. There may be brought-forward price discounting into the final holiday shopping season and through more aggressive discounting ahead of Boxing Day when stores will now have to shut other than for on-line and curbside sales.

OVERNIGHT MARKETS

Nothing material to global markets is due out overnight, just Australian retail sales for November (7:30pmET). Brexit negotiations will continue with possible movement on the fish dispute that is holding thing's up.

TOMORROW’S NORTH AMERICAN MARKETS

A sprinkling of US releases will provide a bit of variety. The US House and Senate votes on stimulus and funding bills face uncertain timing into this evening before they go to outgoing President Trump’s desk for his signatures (they only just released the full 5½ thousand pages of text by about mid-afternoon).

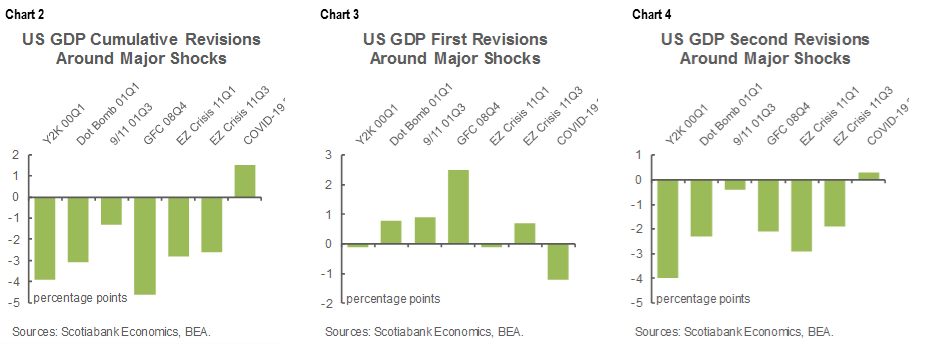

No material revision is expected to US Q3 GDP (8:30amET) as the final services spending tally gets incorporated into the final revision. Remember that the US releases advance, then second and then final quarterly GDP estimates. Tomorrow’s is the final. That doesn’t mean there will not be a further revision as they are pretty common around major shocks and in general. Chart 2 shows the cumulative revisions to US GDP growth from initial print to final around major recent shocks. Chart 3 shows the magnitude of the first revisions around these shocks. Chart 4 is the one that is pertinent to tomorrow’s release and it shows that revisions can still be material in the final round. Of course revision risk in percentage terms should perhaps be viewed in proportionate terms given the magnitude of the shock this year.

The Conference Board’s consumer confidence measure for December (10amET) might get a lift from vaccines like the UofM sentiment gauge did, but near-term forward-looking risks may discount its relevance. Existing home sales during November probably slipped on the basis of softer tracking of pending home sales that show up as completed resales within 30–90 days. The Richmond Fed’s manufacturing gauge will probably follow the Philly and Empire metrics lower (10amET).

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.