KEY POINTS:

- Risk trade looks through the Fed

- On guard for Brexit & US stimulus headlines

- BoE, Norges expected to stand pat

- Can Australia follow up a blow-out jobs report with another gain?

- US: Claims, Philly, starts

- Canada’s third jobs report

TODAY’S NORTH AMERICAN MARKETS

The risk trade generally looked through disappointing US retail sales figures this morning and shook off the FOMC’s effects as rapidly as they occurred. That returns the focus to monitoring potential progress in US stimulus and Brexit talks.

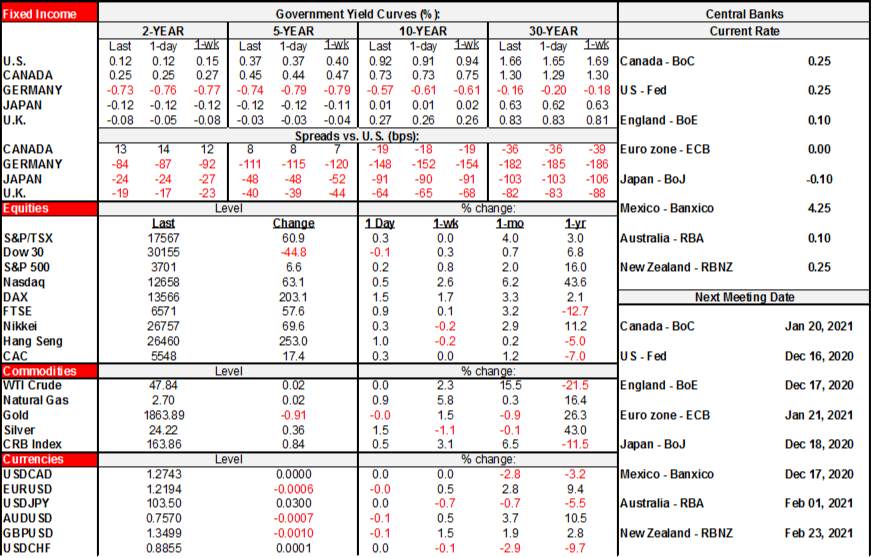

- Stocks held onto gains into the close. The S&P500 was up by less than ¼%. Toronto was up by just over ¼%. European markets closed higher by ¼% to 1 ½% except for a small loss in Spain.

- The USD initially appreciated following the FOMC communications but subsequently lost ground to close weaker on the day. Most currencies appreciated against the USD—except CAD. I don’t have a great explanation for CAD’s depreciation. BoC Governor Macklem’s remark about the C$ being on the BoC’s radar was nevertheless followed by CAD appreciation to the USD yesterday perhaps as he sounded generally more upbeat. Today’s unwind of yesterday’s CAD rise started well before inflation figures registered a bit firmer than expected headline but a touch softer core including revisions.

- Oil was up ½%. Gold was flat.

- Sovereign debt curves remained little changed in the US and Canada following the FOMC and Canadian inflation.

OVERNIGHT MARKETS

Overnight developments are likely to primarily affect regional markets but guidance from the Bank of England will be a focal point.

Both the content and tone of the Bank of England’s policy announcement at 7amET will ultimately depend partly on Brexit talks. No changes are expected tomorrow. While the increased asset purchase target announced at last month’s meeting suggests the bank will hold monetary conditions as is, there is a potential the bank announces more accommodation should Brexit talks ultimately collapse. At the moment, however, they appear to be achieving notable progress by narrowing the issues down to one—what to do with fisheries—which is likely to keep policy monetary policy unchanged for now.

The November Australian jobs report will be released at 7:30pmET. This is a volatile report which reported 179k jobs added in the month of October. It may be challenged to post a further gain. The RBA has stated that its policy will be aimed at improving labour market conditions as a way of stoking inflationary pressure. We expect hours worked to rise as spare capacity is alienated.

Norges Bank is expected to hold its Deposit Rate at 0% at 4amET. Despite higher than expected inflation, the Bank is unlikely to revise forward their guidance of holding rates until the end of 2022. We expect the bank will wait until the economic recovery has matured before signaling a tightening in monetary conditions.

TOMORROW’S NORTH AMERICAN MARKETS

Nothing should carry material surprises on the macro docket tomorrow which means that tape bombs on Brexit and US stimulus negotiations will likely carry the most potential to impact markets if anything.

Banxico is expected by most including our Mexican economists to hold at 4.25% tomorrow afternoon, but a minority think they might have another cut up their sleeves (2pmET).

Canada’s ADP payrolls report for November is usually good for a giggle (8:30amET).

US releases will include jobless claims (8:30amET), the US Philly Fed’s metric (8:30amET) and housing starts for November (8:30amET).

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.