KEY POINTS:

- Markets enter final sprint to the holiday break

- Overnight: Brexit, BoT hold

- CDN GDP: October up, November uncertain

- US on tap: claims, durables, PCE, new home sales

TODAY’S NORTH AMERICAN MARKETS

Global calendars will go dead quiet after tomorrow, but in the meantime, Brexit negotiations will groan on and continue to combine with COVID-19 headlines to guide markets. Today brought more of the same after the morning developments. The US will fire off another salvo of macro releases in the morning that could impact markets—especially job market signals—and then its calendar goes pretty much silent until the new year. Failing achievement of a Brexit agreement could bring out defensive positioning before the Christmas break.

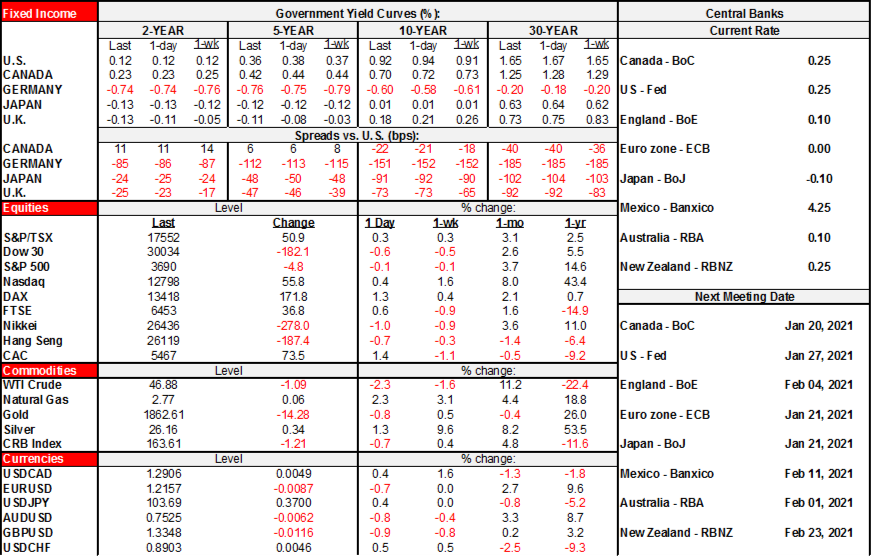

- The US S&P500 fell by about ½% along with the DJIA but the Nasdaq closed up ½%. Toronto closed higher, but with little breadth as Shopify singlehandedly added ½% to the index today. European stocks closed up by 1–2% except for a ½% rise in London.

- Sovereign bonds rallied across North American and European markets. The gilts front-end led the rally as the 2s10s curve steepened a little. US and Canadian sovereign yields fell by about 2bps in 10s by the time of publishing.

- The dollar climbed again with gains of just under ½% to over 1% across major currencies.

- Oil fell by about 2%.

OVERNIGHT MARKETS

Overnight markets will continue to monitor Brexit negotiations. The only release on tap will be the policy decision by the Bank of Thailand and they are expected to hold at 0.5% (2:05amET).

TOMORROW’S NORTH AMERICAN MARKETS

The US and Canada will update a series of macroeconomic readings tomorrow morning.

Canada releases October GDP and provides guidance for November GDP (8:30amET). StatsCan previously guided that growth would be 0.2% m/m in October based upon preliminary estimates.

The bigger uncertainty surrounds the preliminary reading for November GDP. There are two forces at play in driving expectations for November. One is that November data has been pretty solid thus far. Hours worked were up by a robust 1.2% m/m for the reference week including the 15th of the month. Since GDP is hours worked times labour productivity the gain in hours worked is a good sign. True, the estimate is for the middle of the month before Toronto and some of its surrounding ‘burbs went into lock down the following week, but that might not get fully captured in the preliminary estimates as opposed to revisions. We also know that housing starts were up 14% m/m. Retail sales were “relatively unchanged” which seems to be StatsCan code language for a decent gain given the pattern of late. Wholesale trade was up by a strong 1% m/m but existing home sales slipped by 1.6% m/m.

Secondly, we need to consider the lock down effect itself. It’s likely to be much smaller at least for November than when lock downs started in March. For one thing the whole country went into lock down around mid-March whereas the experiences this November were more uneven. For another, the most affected sectors—like accommodation and food services, or arts and entertainment—are only about 73% and 54% of what they were back in February and their weights in GDP are lower. On-line sales, curbside shopping, work from home and income supports should also make this experience less negative through the narrow lens of GDP growth.

A wave of US releases will get crammed into tomorrow morning again before the global calendar goes empty.

- US durable goods orders during November are expected to rise by ½% m/m for headline and core orders ex-defence and aircraft (8:30amET). Core orders have risen for six straight months.

- US weekly claims may further inform nonfarm payroll expectations for December as tomorrow’s figure pushes right through the reference period (8:30amET). The consensus guesstimate is for little change around 880k; three weeks prior to that the figure was down around 716k so markets will be sensitive to further deterioration.

- US consumer spending & incomes during November are likely to post an income drop on continued roll-off of benefits and a spending decline given what we already know happened to retail sales (8:30amET).

- US PCE inflation during November should be little changed both in terms of headline and core based in part on earlier CPI figures (8:30amET).

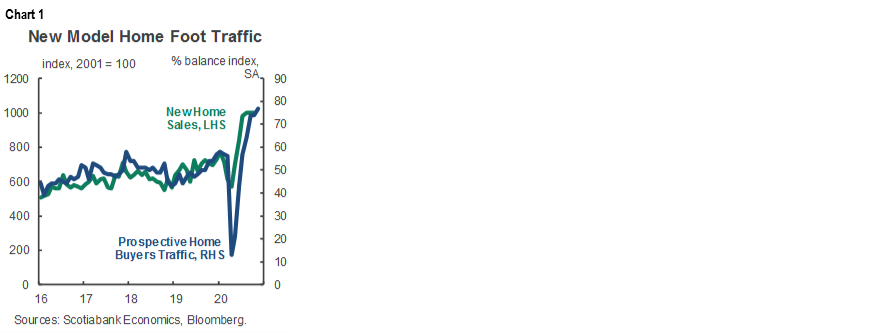

- US new home sales during November are expected to be little changed, notwithstanding still elevated foot traffic through model homes as shown in chart 1 (10amET).

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.