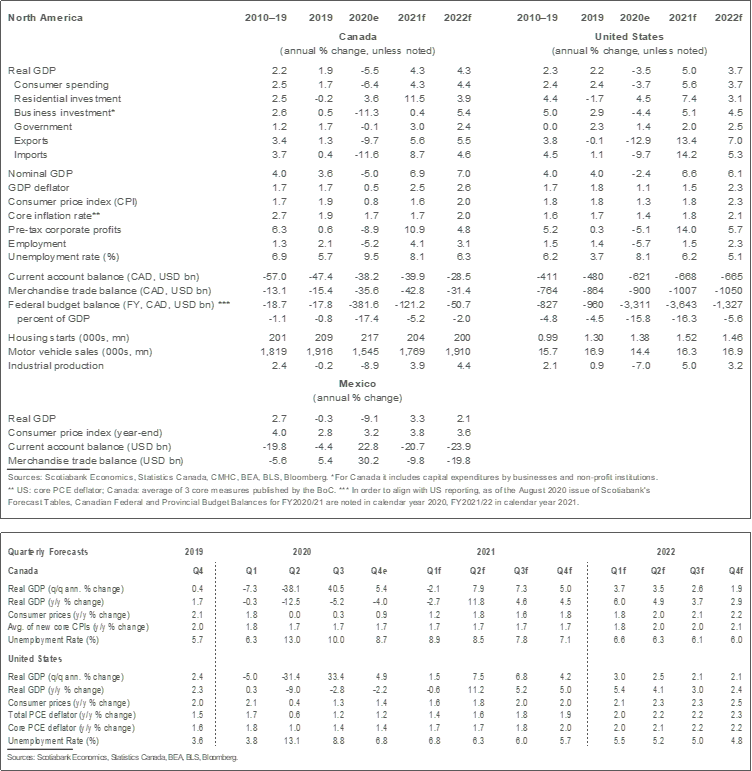

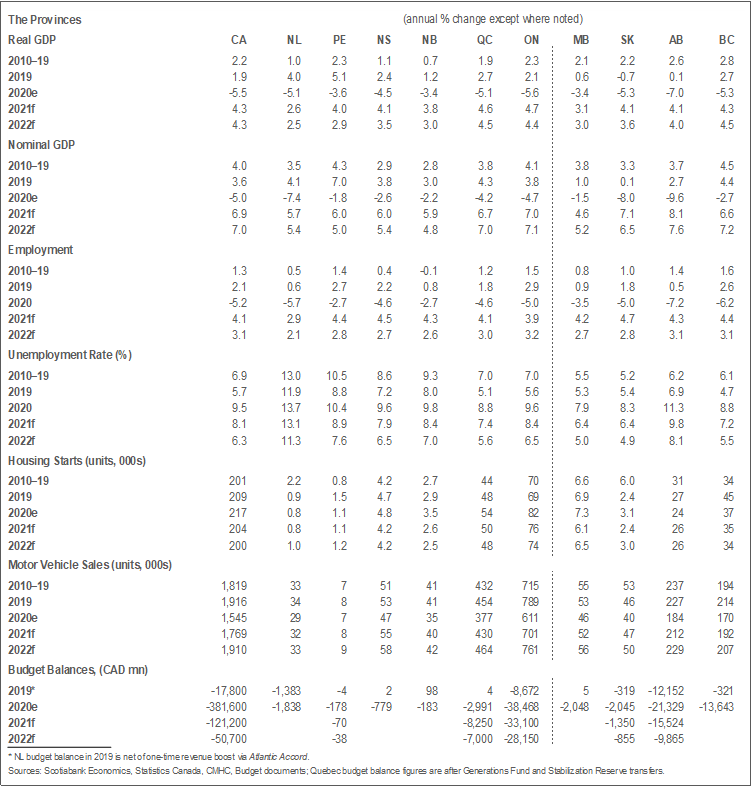

An explosion of COVID cases is leading to a sharp reduction to forecasted GDP growth for 21Q1 in Canada, but very solid growth is expected as restrictions on activity are lifted by the end of the first quarter. We expect growth of 4.3% in 2021 and 2022.

The near-term outlook in the US is more positive than it is in Canada, as fewer COVID restrictions are implemented south of the border so far despite an increased prevalence of the virus. For the remainder of the year, a ramping-up of fiscal support under President Biden is expected to lift US growth to roughly 5% in 2021, falling to 3.7% in 2022.

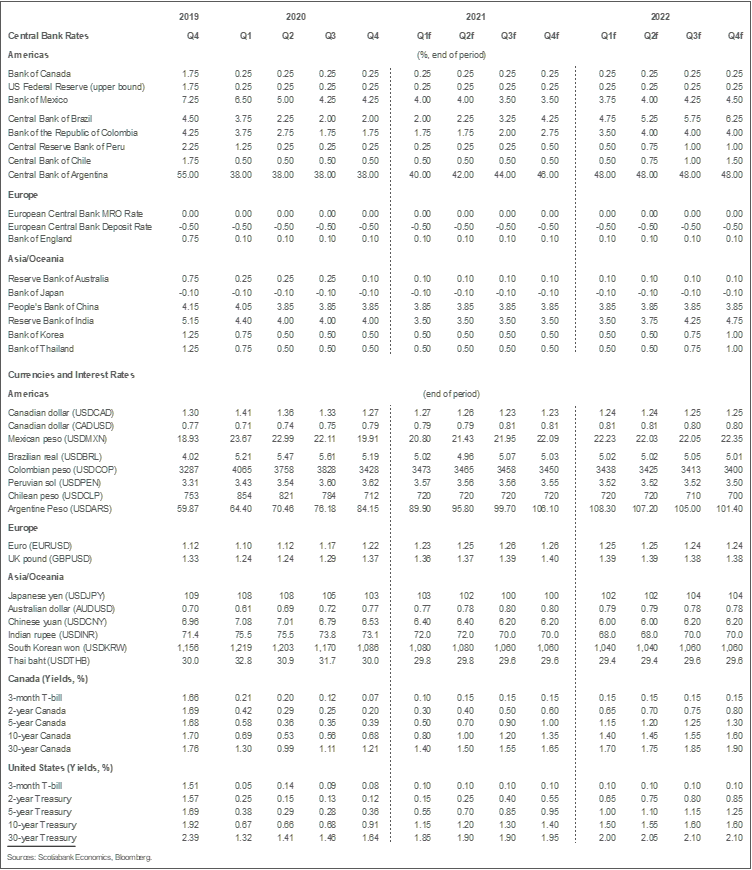

Excess slack will persist, with unemployment rates coming down only gradually and remaining well above pre-COVID levels for much of the next two years even as the output gap will close mid-2022. Policy rates in Canada and the US will remain at current levels for the foreseeable future, but there is a risk that both central banks raise rates well before their currently communicated horizon. We will update our rates call once we have more clarity on the post-COVID recovery.

The COVID storm is raging. The number of infected is climbing exponentially in many countries and provinces. Despite the vaccine roll-out, and possibly because of it, measures to slow the spread of the virus appear, thus far, to be having a limited impact on virus containment. Virus fatigue, the holiday period, the heads-up given that more restrictive measures would be forthcoming, and the evolution of much more contagious strains of COVID have all contributed to the worrisome acceleration in cases and hospitalizations seen so far this year.

This nasty storm should pass. Owing to the vaccine roll-out, the uncertainty at this point is now focused on the duration of the storm rather than whether or not it will pass, as was the case when the pandemic first struck last year and severe restrictions on social engagement were put in place. For the purposes of our forecast, we assume the bulk of Canadian restrictions remain in place until the end of March.

A strong rebound is expected after that. Part of that will reflect the re-opening of the economy in Q2, but we expect a powerful recovery to take us through at least the end of 2022. In Canada, that is driven by a number of factors:

- Considerable pent-up demand for a range of goods and services that could be financed by elevated cash balances. As households become less worried about the impact of the virus on their finances, we anticipate some of these cash balances will be drawn down.

- Strong underlying momentum in a number of industries prior to lockdowns. Monthly GDP for October and Statistics Canada’s estimate for November suggested much stronger-than-anticipated economic activity at a time when some virus control measures were being strengthened. The momentum at the end of 2020 is raising 2021 growth in this forecast, but it is important to remember that a number of industries and their workers continue to struggle. The K-shaped recovery is still very much in play.

- Substantial wealth effects. Equity markets have responded very positively to the vaccine, the US election, and the associated optimism with respect to economic prospects in 2021 and beyond. A similar dynamic has impacted commodity prices, which have rebounded very sharply in anticipation of a post-COVID economic rebound. Rising house prices are also adding to this wealth effect. We view the housing market as quite undersupplied and therefore believe prices are likely to rise further.

- Immigration should pick up sharply at some point this year, and government targets suggest strong increases will be observed until at least 2023.

- Fiscal support will be ramped-up in Canada by $20–30 billion in the next budget. The exact impact of that support will be assessed as details are announced. In the US, it is clear that the Biden administration will undertake substantially more fiscal support this year and beyond. For the time being, we are reflecting earlier announced fiscal measures in addition to US$2,000 stimulus cheques. More is likely to be done.

- Monetary conditions will remain highly supportive of the recovery given central bank pledges to maintain policy unchanged for an extended period of time. The recent rise in long-term interest rates is consistent with the improved outlook and so should not be viewed as a brake on growth. Likewise with the appreciation of the Canadian dollar, which reflects a more benign global risk environment and stronger commodity prices. At current levels, we do not view the loonie as a headwind to growth and the recovery.

Taken with the current state of COVID dynamics, these fundamentals suggest growth of around 4.3% this year in Canada, followed by roughly the same progression in 2022. We expect, however, that GDP will fall by around 2% in the first quarter of 2021 before activity rebounds in the second quarter. Of course, the path will be a function of success, or lack thereof, in controlling the virus over the next several weeks. A re-opening of the economy in early March instead of at the end of the month would lead to less loss of output in Q1, while imparting stronger momentum in Q2.

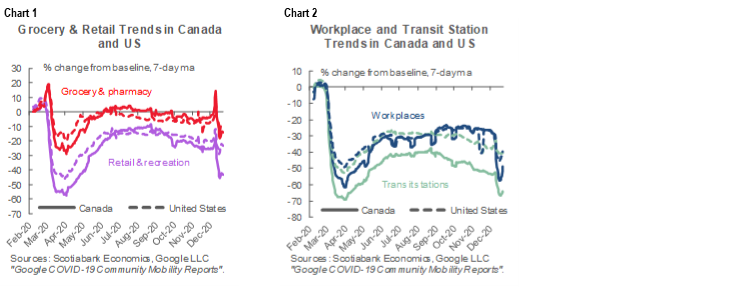

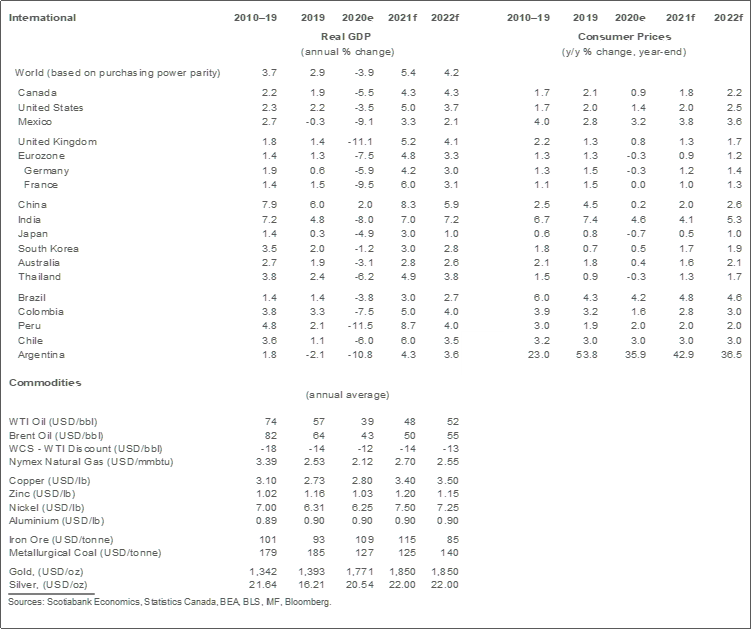

Growth forecasts in Canada stand in sharp contrast to those in the US in the early part of the year. While COVID is more prevalent in the US, restrictions on movements are far less stringent than they are in Canada. As a consequence, the mobility of US residents has remained quite resilient to COVID in the last few weeks. This is not the case in Canada, as can be seen in chart 1. As a result, we expect modest GDP growth in the US in the first quarter, while we expect a fall in economic activity in Canada. The counter to this, obviously, is much worse health outcomes in the US even if vaccine rollout is more rapid south of the border.

For the year as a whole, less COVID-related economic disruptions, combined with a much more substantial increase in fiscal support and more sensitivity to equity market wealth effects in the US in 2021 should lead growth there to be around 5%, more than half a percentage more than the 4.3% expected in Canada. That growth advantage should wane in 2022, with Canada’s 4.3% growth surpassing the 3.7% anticipated in the US.

Risks to the outlook of course remain important. On the downside, slow vaccine rollouts and acceptance can delay the anticipated rebound, as would further evolution of the virus. More positively, it may be that individuals adapt to the current restrictions and resume spending more rapidly than we currently assume. Fiscal policy may also be more supportive than expected. Given the nature of the jobs being affected now and the CERB-like benefits available through the Employment Insurance system, household income might once again benefit as lockdowns are imposed. It is also possible that more fiscal firepower is deployed in Canada in the context of the Spring budget, above the $20–30 billion already planned. This is also possible in the US, where we have only penciled in larger stimulus cheques and not a range of other measures the Biden Administration is likely to pursue.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.