With the increased attention on Canada’s trade relationship with the United States and broader questions about how to boost the nation’s economic potential, there is growing interest in tapping into the country’s rich deposits of critical minerals. But what exactly are critical minerals, and which of these minerals can Canada actually produce? And how important will these resources be for the future of the country?

Below is a primer on critical minerals from the Scotiabank Economics team, including Rebekah Young, Vice President, Head of Inclusion and Resilience Economics at Scotiabank, and other sources. Watch the video below or scroll down for the full article.

• What are critical minerals?

• Why are critical minerals so important?

• What critical minerals does Canada have?

• Which countries have the most critical minerals?

• How can tapping critical minerals help Canada’s economy?

What are critical minerals?

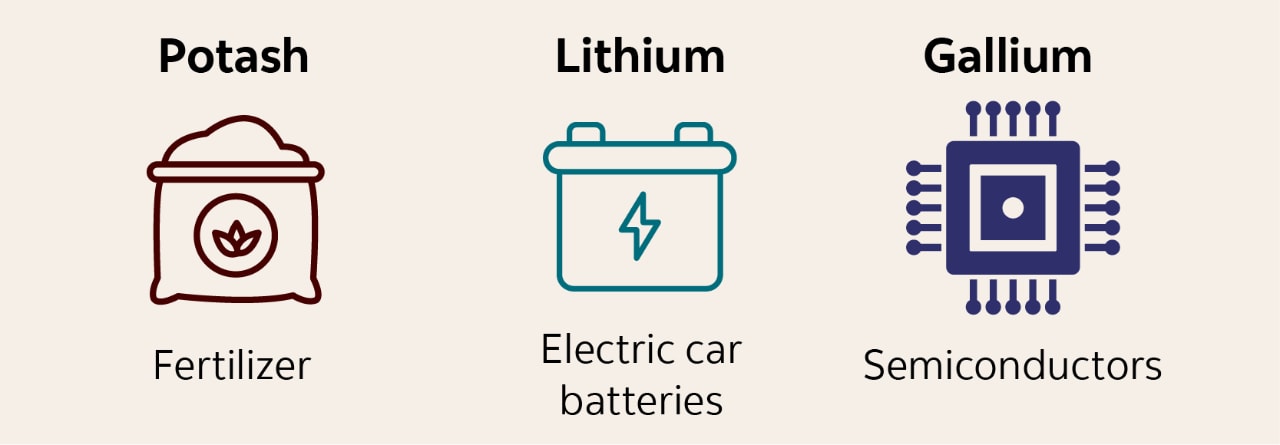

Critical minerals are elements and compounds that are required to create a vast amount of technologies including smartphones, solar panels, electric car batteries, computer chips, jet engines, fertilizer, satellites, and so much more.

Here are some examples of critical minerals found in Canada and some of their uses:

While designations may vary across countries and over time, by definition, critical minerals are “essential” and their supply could be “at risk” when needed.

Critical minerals are typically mined and extracted from ore deposits, but they can also be obtained from secondary sources, including through recycling end-use technologies or as byproducts in the refinement processes of other resources.

Why are critical minerals so important?

Many of the technologies we rely upon today and will rely upon tomorrow — whether for a clean-energy transition or data centres for AI — require critical minerals.

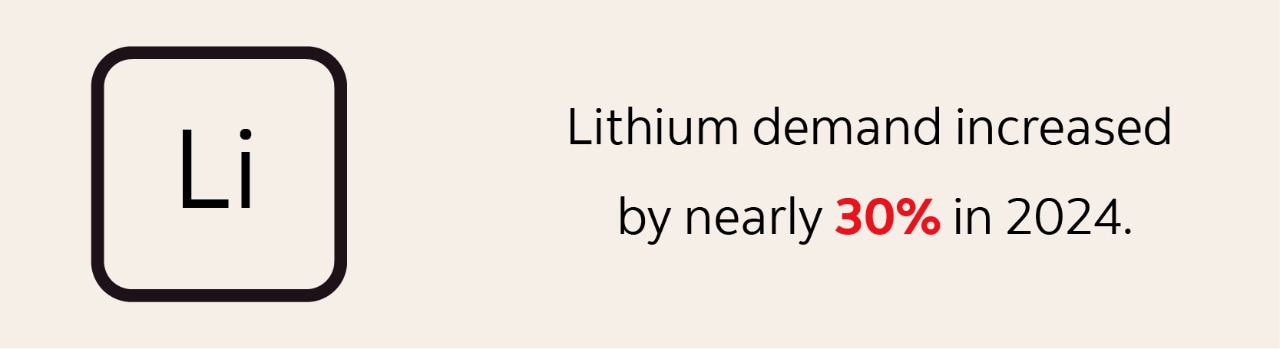

When we look at sectors such as energy, aerospace, tech, defence, transportation, medical devices and more, we’re essentially thinking about technologies that require lots of critical minerals. The demand for critical minerals will continue to grow. In its projection based just on current stated policies, the International Energy Agency predicts lithium to grow fivefold by 2040, graphite and nickel to double, cobalt and rare earth to grow 50-60% and copper to grow 30%.

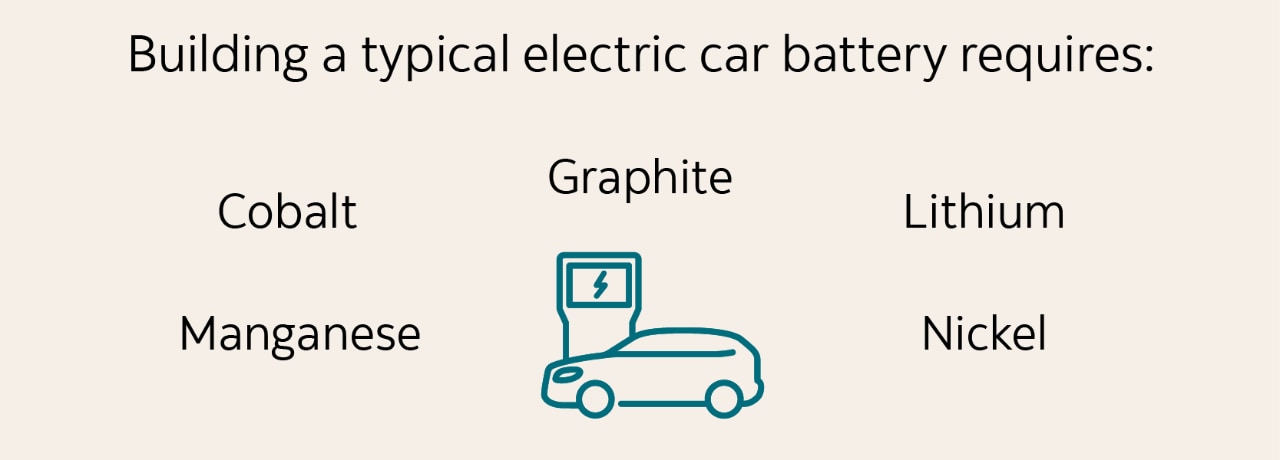

Take electric car batteries as an example. In 2024, electric vehicles represented 20% of the global car market and this is projected to reach 40% by 2030, according to the International Energy Agency.

Because of the need for critical minerals in so many important technologies, a country’s access to these resources can also affect its ability to ensure secure and affordable energy supply as demand for electrification could double by the end of the decade including from emerging pressures from AI data centres.

“The wiring, the solar panels, the turbines, the batteries for storing energy, the grids for moving energy around is another category for which we have a high need for critical minerals,” Young says.

Critical minerals are also important to national security because of their use in military and security technologies.

Many countries are upscaling both the extraction and refinement of critical minerals available within their borders or are strengthening their relationships with countries boasting these capabilities.

What critical minerals does Canada have?

In Canada, the federal government has an official list of 34 critical minerals, but has identified six as key: lithium, graphite, nickel, cobalt, copper and rare earth elements. Many provinces also maintain their owns lists of those key to their regions.

To be included in Canada’s overall list, a mineral must be both accessible for production in Canada and have its supply chain threatened. It must also meet one of the following criteria:

- essential to Canada’s economic or national security

- required for the national transition to a sustainable low-carbon and digital economy

- position Canada as a sustainable and strategic partner within global supply chains

As well, Canada is the world’s largest producer of potash, used primarily in fertilizers, with 21.9 million tonnes in 2023 or 32.4% of global production. It’s also in the top five global producers for indium, niobium, platinum group metals, titanium concentrate, uranium and primary aluminum.

These rankings represent what’s currently produced, but much of Canada’s critical mineral resources are untapped. For years, Canada has been investing more heavily in exploration to survey what we have and what can be mined. AI models are increasingly being used to predict the location of critical minerals, Young says.

It’s important to recognize there’s a difference between how much of a critical mineral a country has and how much is economically feasible to extract. Canada has a rich critical mineral endowment but unlocking its full potential will require great effort. And, as one House of Commons committee report noted, challenges to critical mineral extraction include lack of infrastructure in remote locations and environmental considerations. Those economics can change fairly quickly, Young notes, for example if governments create a more stable (and timely) investment environment or, unfortunately, if once-reliable cross-border supply is suddenly restricted.

Which countries have the most critical minerals?

Many critical minerals are heavily concentrated in a small number of countries, both in terms of mining and refining. In fact, a report by the IEA found that supply concentration has increased in recent years, raising concerns over economic and energy security.

Source: The International Energy Agency

China controls the lion’s share of the world’s critical minerals because of its domestic reserves, longstanding strategic investments abroad, massive domestic subsidization, and extensive refining capabilities. Amid trade disputes with the United States, China recently placed export controls on some of its critical minerals. It is not just China: export restrictions around the world have increased five-fold over the past 15 years, according to the OECD. Currently over half of energy-related critical minerals are subject to some form of control.

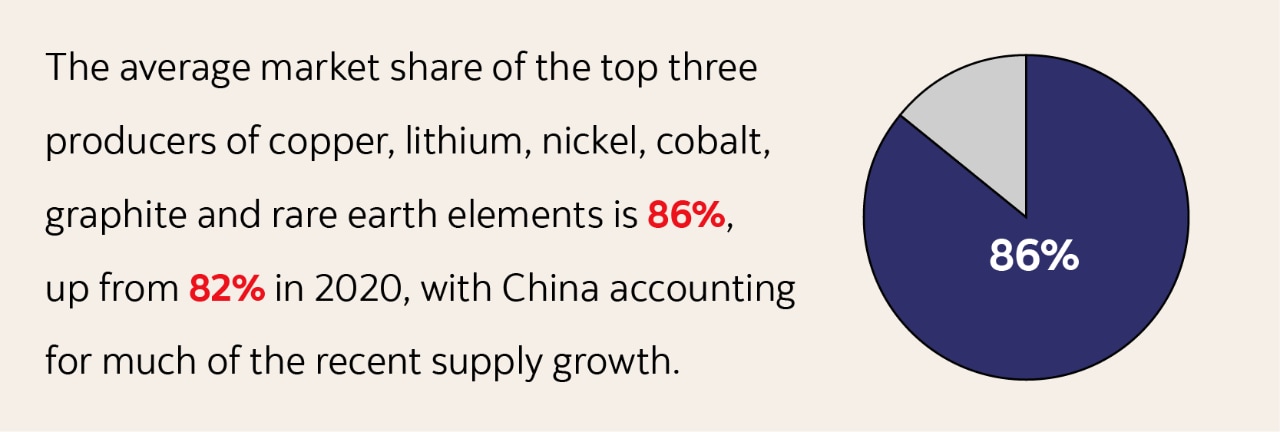

In recent years, the United States and other countries have been making strategic attempts to secure critical mineral supply chains. While increased attention on critical minerals around the world will lead to more diversified refining supply chain over time, the IEA projects only moderate progress by 2035 with the top three refined material suppliers expected to hold an 82% market share.

How can tapping critical minerals help Canada’s economy?

In Canada, there are hopes that extracting and refining our critical mineral endowments could generate jobs and prosperity in the country. For example, northern Ontario’s so-called Ring of Fire, with large amounts of nickel, chromite, zinc, platinum, copper, and other critical minerals, is being eyed for production. The mining sector already accounts for around 5% of Canadian GDP, and global demand for these resources could double that over time, Young says.

All five of the critical minerals needed for an electric battery, for example, are on Canada’s critical mineral list and therefore could be produced in the country. If Canada developed a domestic EV battery supply chain, it could support up to 250,000 jobs by 2030 and add $48 billion to the Canadian economy each year, according to a report by Clean Energy Canada.

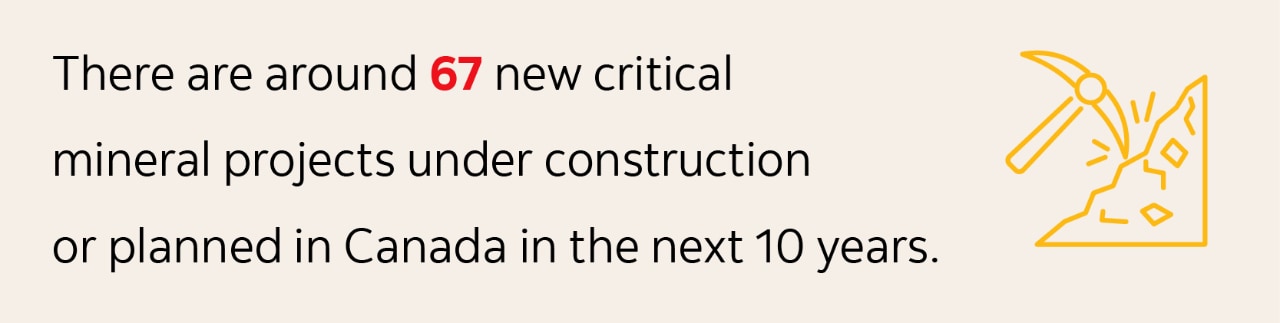

“It’s very difficult to put a number and even a timeline on the potential [of critical minerals in Canada]. The best estimate that we can put would be around the federal government’s tracking of major project activity,” Young says. Beyond current production, there are around 67 critical mineral mining projects under construction or planned in the next 10 years in Canada, amounting to $72.4B in potential investment.

However, Young says if the federal and provincial governments are smart about policy and the onerous regulatory process is streamlined, we could see far more projects enter development given the demand for critical minerals. She also notes progress on advancing partnerships with Indigenous communities, not only through employee and supply chain channels but increasingly through equity partnerships.

Source: Natural Resources Canada

Beyond extraction, Young says Canada could become a prominent player in the refining stage as well. The potential benefits are further amplified through indirect channels, not just the jobs and businesses in the local communities, but also the sector’s outsized contribution to the country’s intellectual property.

“Processing of critical minerals is more mobile and tends to go to countries that have high skilled labour, higher academic institutions, more research going on because of the higher sophistication that’s involved and it also requires higher capital intensity. Canada has all those factors.”