Myles Zyblock, Chief Investment Strategist of Scotia Global Asset Management – which manages over $200 billion* for millions of investors in Canada and around the world – shares his latest market and investing insights.

This month, Zyblock analyzes why Canadian equities are underperforming and the case it makes for diversification.

Canada’s S&P/TSX Composite has returned 4.1% this year to date, compared to global equities, which have delivered just over 12%. As a result, Canada’s primary benchmark index, the S&P/TSX Composite, ranks 60th among the 92 “primary equity indexes" tracked and ranked by Bloomberg. This might be considered a disappointing year, at least so far, for a Canadian focused equity investor.

Why is Canada’s benchmark index lagging? The performance of market capitalization weighted indexes (where securities are weighted by their overall value rather than their price) can depend, often materially, on how they are structured.

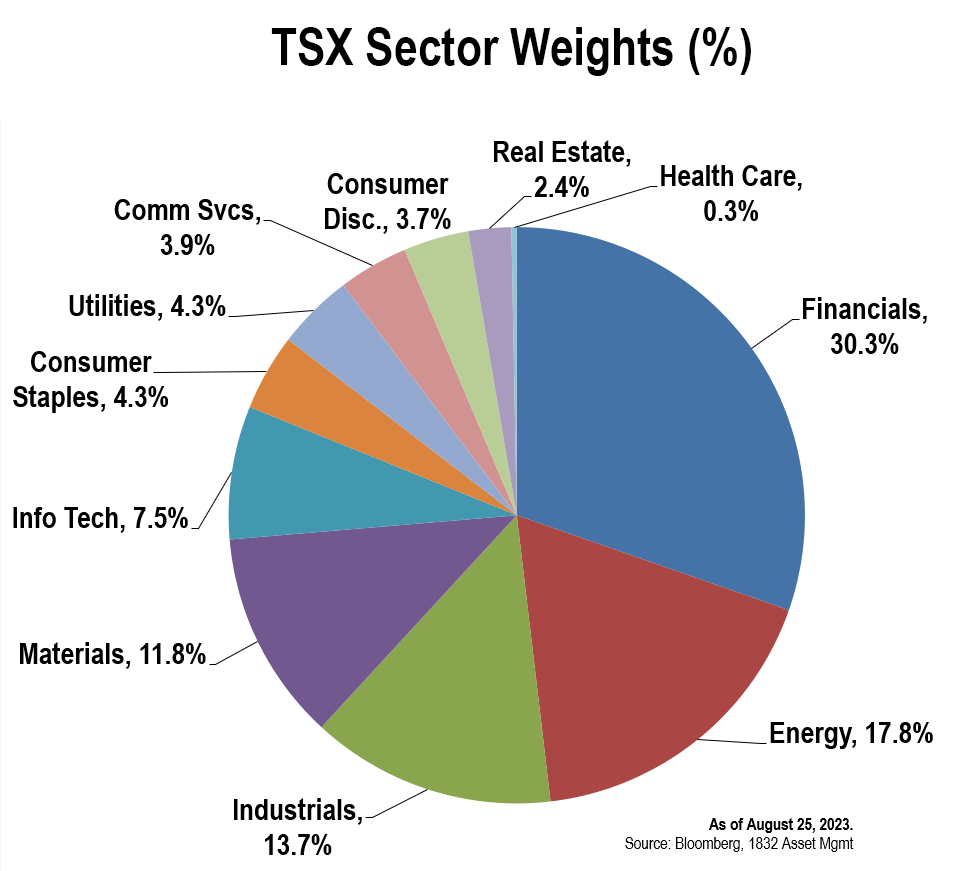

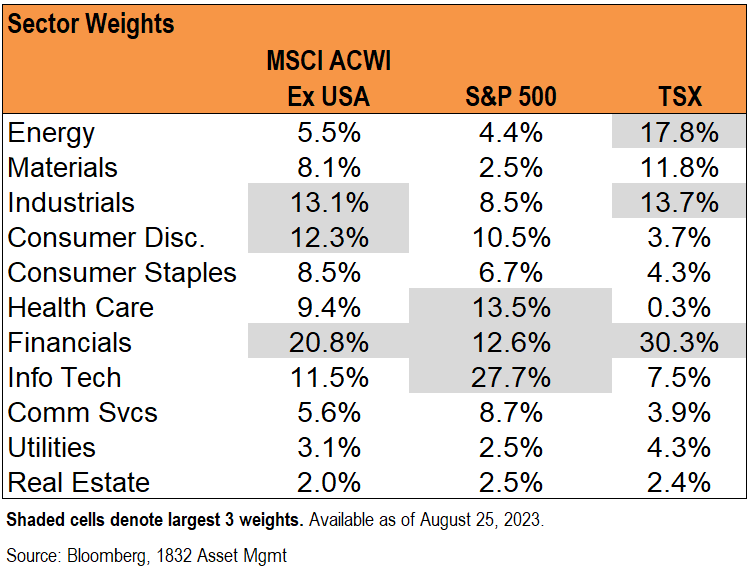

For the S&P/TSX Composite Index, 60% of its market capitalization is skewed towards Financials and Resources (i.e., Energy and Materials), which have been out of favour with global investors. Only 15% of the market capitalization is geared towards Information Technology, Consumer Discretionary and Communication Services, which have been this year’s global equity performance leaders.

For Canada to compete on returns, it probably not only needs its U.S. counterpart (the S&P 500) to continue rising, but it also needs commodity prices to behave much better than they have been.

Canada and the U.S. – a close-knit relationship

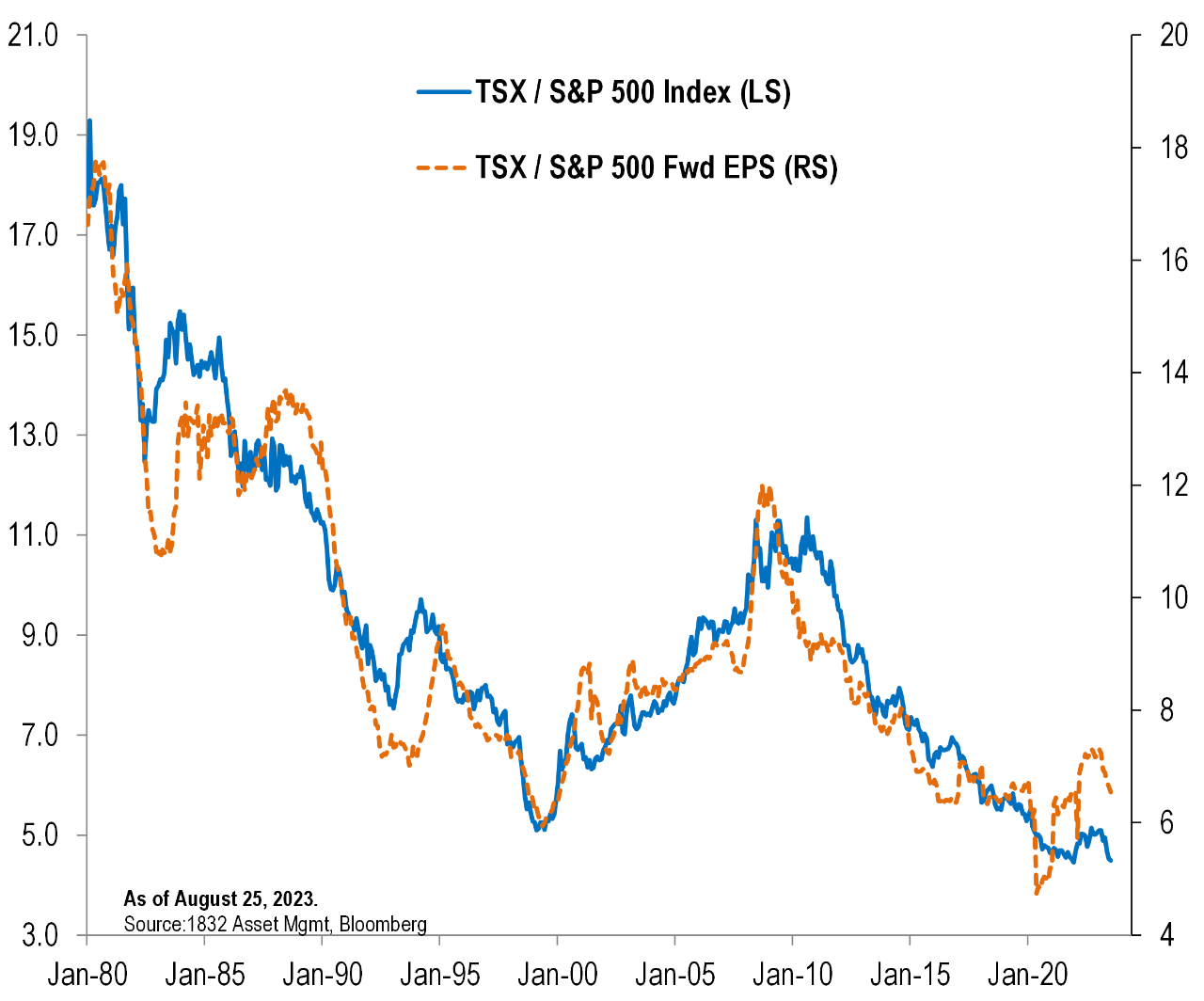

Over time, the performance of the TSX versus the S&P 500 has closely tracked the performance of TSX corporate earnings against S&P 500 earnings.

The Canadian equity market has underperformed its U.S. counterpart for the better part of the past 15 years largely because TSX earnings have not kept pace with those delivered by the S&P 500.

TSX earnings growth, like market capitalization, depends on the earnings progress of financial and resource companies.

While analysts are often concerned about corporate earnings, investors are focused on equity price returns. These two ideas are often in agreement, but the relationship between earnings and stock price returns is far from perfect.

We find that the variation in annual TSX returns can largely be explained by two variables: (1) The annual pace of gains in commodity prices and (2) the rolling one-year returns for the S&P 500. The best environment for the TSX has been when both the S&P 500 and commodity prices rally together. While the S&P 500 has done well this year, most broad-based commodity price indexes have declined by between 5% and 9%.

Canada’s banks and commodity prices

Canada's banks are diversified across business lines and geographies. However, a key part of their business is domestic mortgage lending. The boom in housing activity over the past 20+ years has been a major contributor for earnings. This is unlikely to be repeated over the next 20 years, barring high immigration rates or a return to near-zero percent borrowing rates.

As for commodity prices, China, the world's largest commodity consumer, might be an important curb on future demand. It could take time, measured in years, for the overcapacity in their real estate sector and capital spending programs to normalize. This probably represents an anchor on the pace of future commodity demand growth.

In hindsight, it is always obvious what could have been done to get a higher return. In practice, however, this is extremely difficult. In the end, we recommend a diversified approach to long-term investing, across asset classes, geographies, and sectors.

Myles Zyblock is a recognized North American strategist, regarded for his investment insights that blend finance and psychology to capture major inflection points in financial markets. Myles has over 25 years of experience in guiding and advising on asset allocation for a diverse set of institutional and retail advisors globally. Myles joined the firm in 2013 as the Chief Investment Strategist, working closely with the Investment Team. His experience spans multiple asset classes and geographic regions.

*Total assets managed by 1832 Asset Management registered investment professionals. Scotia Global Asset Management includes 1832 Asset Management L.P., a limited partnership, the general partner of which is wholly owned by Scotiabank.

Commissions, trailing commissions, management fees and expenses all may be associated with mutual fund investments. Please read the prospectus before investing. Mutual funds are not guaranteed, their values change frequently and past performance may not be repeated.

Views expressed regarding a particular company, security, industry or market sector are the views of the writer and should not be considered an indication of trading intent of any investment funds managed by 1832 Asset Management L.P. These views should not be considered investment advice nor should they be considered a recommendation to buy or sell. These views are subject to change at any time based upon markets and other conditions, and we disclaim any responsibility to update such views. © Copyright 2022 1832 Asset Management L.P. All rights reserved.