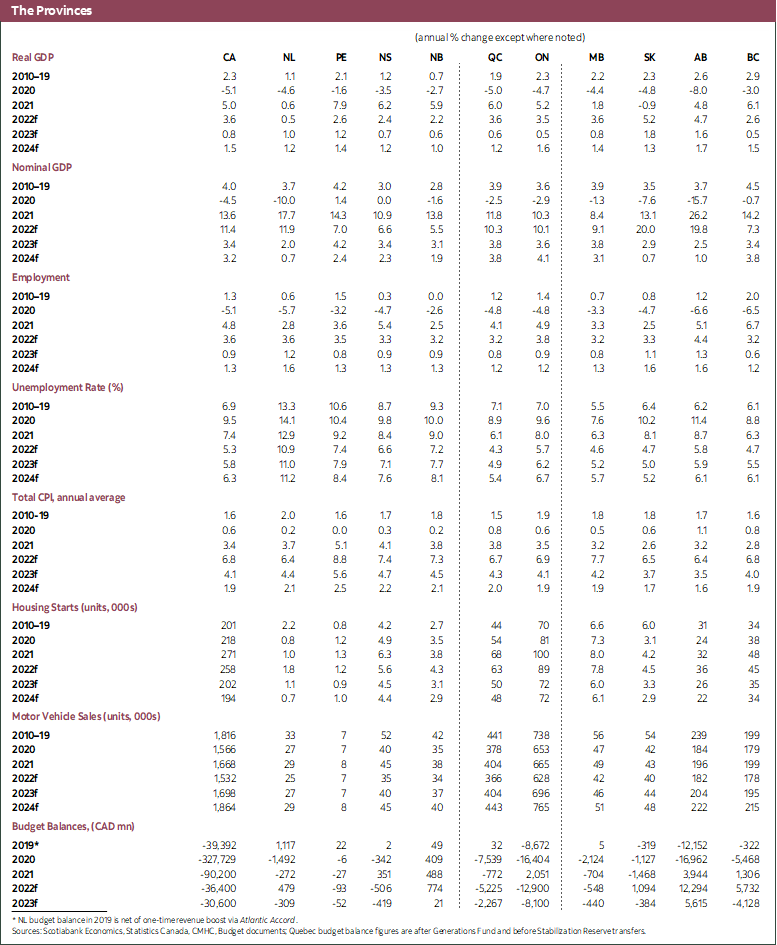

HIGHLIGHTS

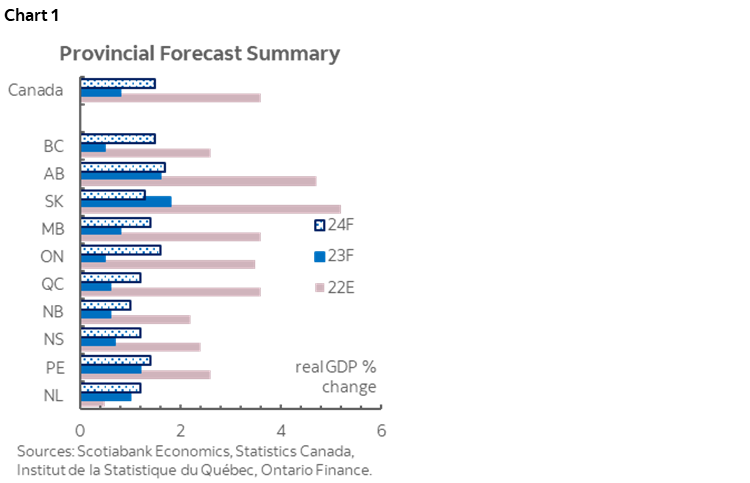

After seeing strong broad-based growth in the first three quarters of 2022, the tide is turning quickly as all provinces are feeling the pinch of rising interest rates and dimmed global outlook (chart 1). With high levels of uncertainty regarding inflation and monetary policy actions, growth should continue to slow well into 2023, and we now expect national growth to stall in the first half of next year. Alberta and the Prairie Provinces face fewer headwinds relative to the rest of the country, whereas Ontario and BC brace for a sharper slowdown.

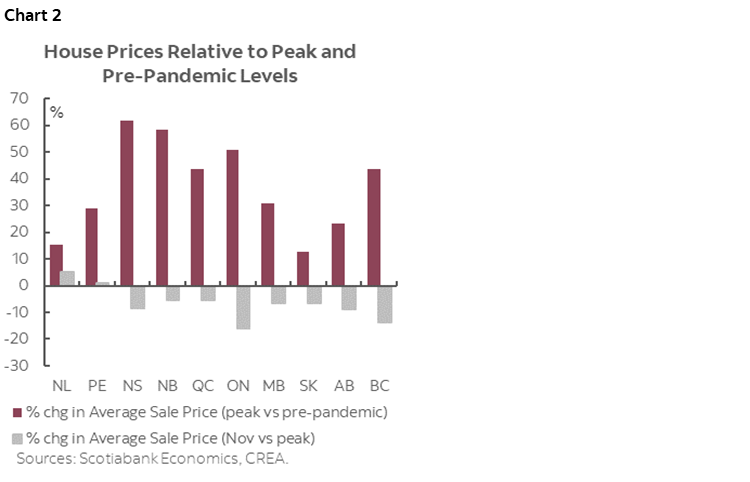

An interest-rate-induced housing slowdown weighs on growth across the board, with the impact most pronounced in Ontario and BC via high exposure to housing-related sectors. Although the pace of decline seems to be moderating as of November, our baseline forecasts assume the downward trend will continue into 2023, with large uncertainty around homebuyer sentiment and central bank actions. The Bank of Canada’s 400 bps rate hikes have driven the slowdown so far this year, facilitated by other factors—as pointed out in our latest Housing News Flash (see here), the softness this year is also partly the outcome of an advancement in purchases front-loaded to 2021. Hence, with house prices still well above pre-pandemic levels, the Atlantic provinces (particularly Nova Scotia and New Brunswick) could see further rebalancing in sales activities next year. Housing markets in Saskatchewan and Alberta are more shielded by their smaller price appreciation during the past two years (chart 2).

The cooling effect of restrictive interest rates is also felt in the consumer sector, compounding headwinds in Ontario and BC while adding pressure to Alberta. Households in these provinces have higher debt relative to income and will see their debt servicing costs increase more as interest rates rise, weighing on spending. The continued decline in property valuation could also erode spending through the wealth effect.

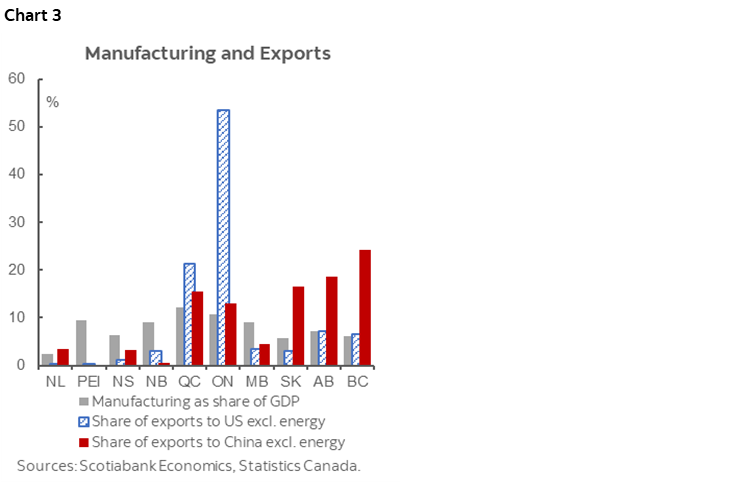

Provinces are also facing strong headwinds from abroad, mainly through weaker demand for exports (chart 3). As we flagged in the latest forecast tables, a global recession is assured and largely driven by dramatic slowdowns in China and Western Europe. Meanwhile, we are also seeing the US entering a technical recession with output falling modestly in 2022Q4 and 2023Q1 as a result of aggressive monetary policy tightening and an equity market correction. Weaker demand from the US disproportionally affects Ontario and Quebec, particularly weighing on manufacturing in Ontario. Non-energy exports from BC and Alberta should also see sizable declines driven by the US and China. On the flip side, Manitoba, Nova Scotia, and PEI are relatively shielded from a global slowdown as over half of their exports are interprovincial.

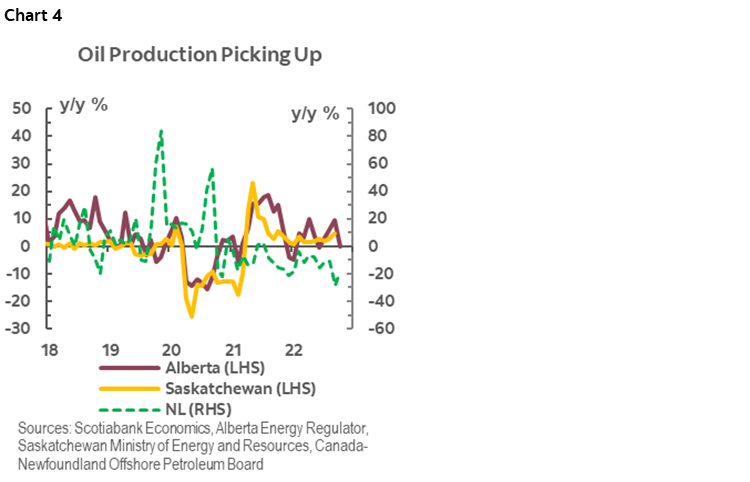

Alberta and the Prairie Provinces should continue to benefit from well-supported commodity prices and agriculture production recovery. Although pulled back from the peak levels this summer, oil prices are expected to average well above US$90/bbl this year and next despite recession fears against tight supply. Oil production is picking up in Alberta and Saskatchewan (chart 4). Looking forward, even an average harvest could support growth next year—prices of main crops are expected to remain strong as the Russia-Ukraine war continues.

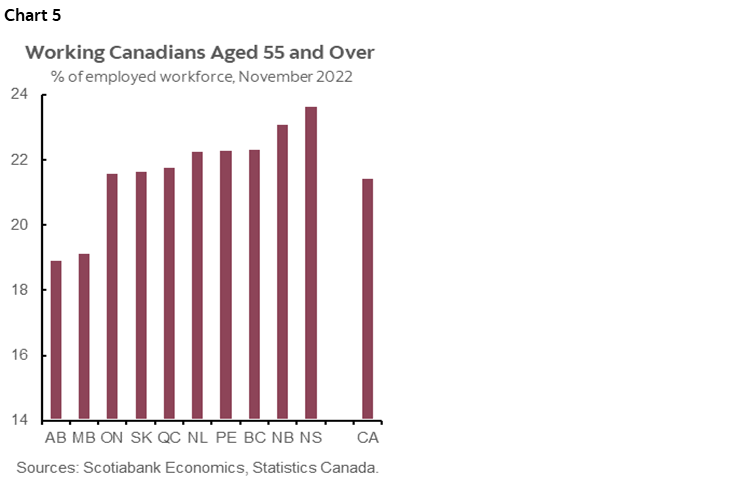

Tight labour markets across the country, but particularly pronounced in BC and Quebec, could be a double-edged sword—low unemployment rates provide a buffer in a slowdown, while continued labour shortages could weigh on growth next year. Job vacancies have doubled compared to pre-pandemic levels across Canada, owing to the strong economic rebound that has seen an additional half-million jobs created since the onset of the pandemic. Shortages have been exacerbated by a temporary dip in immigration and a surge in retirements. Record-level immigration targets in the next three years could help fill some of these positions, but the mismatch of skills will likely keep vacancies materially higher in some occupations, constraining capacity expansion in key sectors such as construction, health care, agriculture, accommodation, and food services. BC and Quebec have had the highest vacancy rates among all provinces since 2019 and should continue to see high vacancies with over 20% of workers reaching retirement age in the next 5 years in both provinces. Alberta’s vacancy rate doubled relative to pre-pandemic but is still lower than that of most of its peers, thanks to the province’s younger workforce (chart 5).

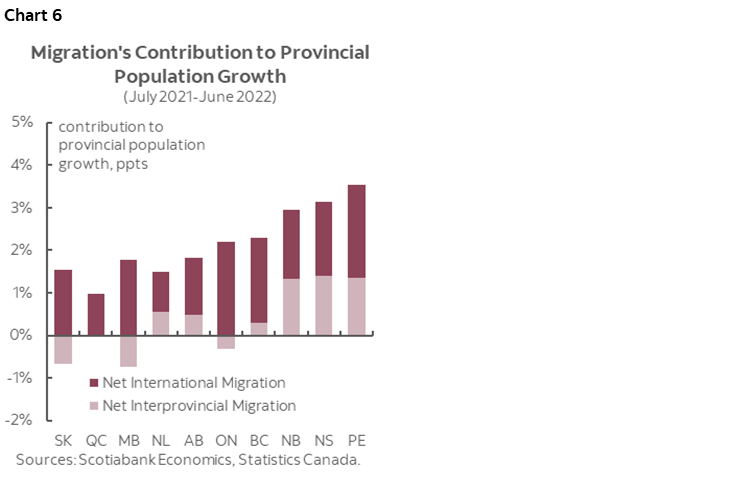

Benefitting from the rise in net interprovincial migration in the past two years, the Atlantic provinces should continue to see strong population growth as international migration picks up. Canada is currently on track to beat the upper range of its 2022 target to welcome 445k new permanent residents, which would be close to another 10% increase from last year’s record-level immigration. The Government of Canada also increased its immigration targets for the coming two years, planning to receive 447k immigrants in 2023 and 451k in 2024. The influx of international immigration should also give Ontario and BC a boost—from July 2021 to June 2022, international migration contributed to over 2% of population growth in these two provinces. Quebec will likely continue the trend of weak population growth, but saw the largest surge in non-permanent residents among all provinces. Population growth is still lagging in Saskatchewan and Manitoba despite strong contributions from immigration—residents moving out of these two provinces reduced their respective populations by 0.7% (chart 6).

Global and national drivers should continue to dominate provincial growth paths ahead with some regional differences. Looking beyond the slowdown in the first half of 2023, the Bank of Canada could begin rate cuts in the back half of next year and into 2024 given the expected slowing in inflation, hence we could expect some rebound to take hold (see here for our latest national forecast) in most provinces.

BRITISH COLUMBIA

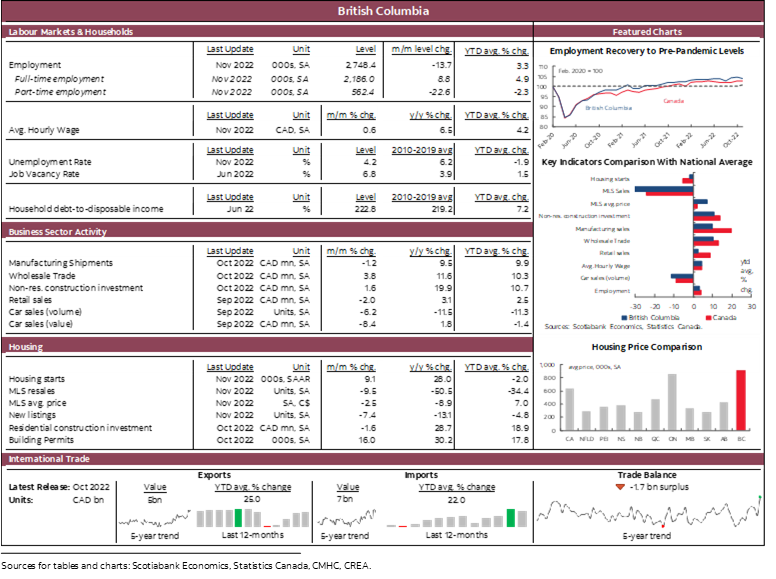

Following a strong recovery of 6.1% real growth last year, we expect more downside to BC’s economy this year, with weaknesses continuing into 2023. BC is more affected by an interest-rate-induced slowdown compared to its peers through larger exposure to the housing sector and reliance on household consumption. The housing market is cooling faster in the province than its peers—reflected in resale activity where year-to-date sales plunged -34% relative to last year—the largest drop among all provinces. This contraction affects the province disproportionally—over 23% of BC’s real GDP is contributed by real estate and residential construction, compared to 17% in Ontario and 14% in the rest of the country. BC’s economy also skews towards household consumption of goods and services, which could see a sharper slowdown than the rest of the country due to high household indebtedness and the wealth effect from the depreciation of house prices.

The province saw strong growth in exports so far this year, but the tide is likely turning given reduced demand from BC’s trading partners. We expect weaker growth from exports for the rest of this year and next, driven by the province’s key commodities—lower lumber demand associated with continued declines in US homebuilder sentiment, as well as weak copper prices resulting from a slowdown in China. Robust prices of energy products (natural gas and coal) should continue to support the province’s export values.

ALBERTA

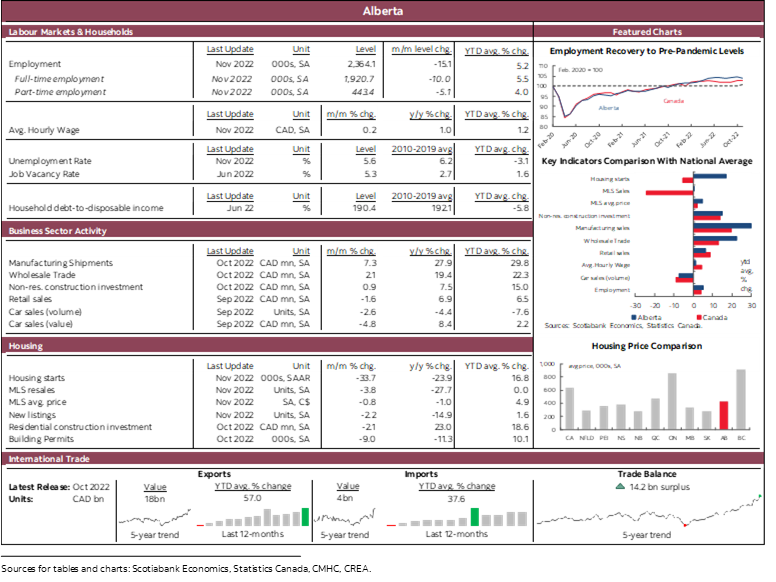

We expect Alberta to continue to lead growth this year and next. Although pulled back from the peak in June of around US$120 per barrel, crude oil prices remain favourable. Drilling is ramping up—the Alberta Energy Regulator expects oil and gas capital spending to increase by 56% this year and remain around levels higher than in years preceding the pandemic, yet still well below 2014 peak levels. The completion of the TransMountain pipeline expansion next year will increase the transportation capacity and should narrow price discounts between the Western Canada Select (WCS) and West Texas Intermediate (WTI), giving the sector more advantage moving forward.

Employment growth in Alberta outpaced the national average this year, mainly driven by broad-based gains in the service sector. The province is having a strong year in housing starts as of the third quarter, bringing the year-to-date total to 21.2% higher than in the same period last year. But the province’s housing market has been cooling fast as interest rates rose—sales contracted -46% since the peak in February, and the average sales price declined by -8.9% during the same period. Nevertheless, as the province experienced less price appreciation during the pandemic than the national average, housing remains relatively affordable in Alberta—especially after accounting for income levels.

Alberta has been diversifying business investments into non-energy sectors—capital outlay in sectors such as petrochemical manufacturing has been ramping up, but the benefits are likely to be seen only after some time.

SASKATCHEWAN

Saskatchewan is better positioned to weather the monetary-policy-induced downturn than most provinces. We expect a rebound in agricultural production and favourable commodity prices to support growth momentum in Saskatchewan well into next year. Prices of potash and wheat have pulled back from their May peaks following Russia’s invasion of Ukraine, but are expected to remain strong for as long as the conflict continues. Benefitting from the steep price appreciation of crude oil this year, oil production in the province increased modestly by 2.1% relative to the same period last year, while year-to-date oil and gas exports jumped by nearly 70% in value as of September.

Outside the commodity sectors, Saskatchewan has also been leading in wholesale trade, manufacturing, and construction investments so far this year. The province faces more modest headwinds compared to its peers in an environment of monetary policy tightening. Household consumption contributes to a smaller share of real GDP than the national average. The housing markets are more insulated from the large adjustments we have witnessed in most parts of the country—mainly thanks to smaller price appreciation during the past two years.

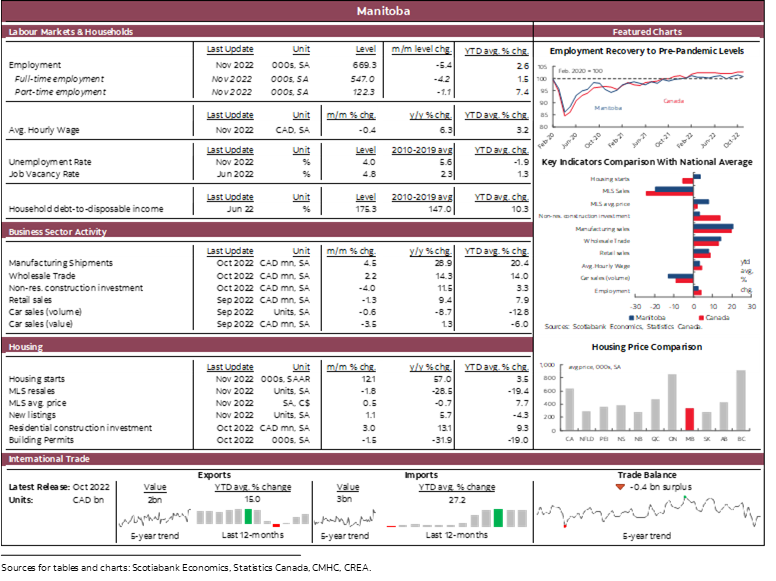

MANITOBA

Manitoba’s economic growth has been tracking strong this year, with its key indicators very close to the national average on a year-over-year basis. The strong growth was mainly due to the recovery from the drought last year, which affects the economy in two folds: the first one is through the loss of crop production, which has fully recouped this year. The second one is through electricity exports. Last year, Manitoba didn’t generate enough hydroelectricity and had to import from the US to compensate for drought conditions. This year, electricity generation in Manitoba picked up and rose over 80% year over year in September, which gave the economy a sizable boost through exports.

We expect Manitoba to continue its middle-of-the-pack performance next year. The province is exposed to the same factors that drive the national slowdown, but with some differentiators. The province’s housing sector should see more downside in sales next year. Average sale prices rose over 30% during the pandemic, much higher than the price appreciation seen in Saskatchewan and Alberta, and only declined by under 7% since the February peak this year. Sales dropped -26.2% year-to-date relative to last year, and should continue to slow with interest rates remaining in restrictive territory. Housing is still relatively affordable in Manitoba, but the province has a lower share of private dwellings per capita than the national average—not much higher than Ontario. Immigration should continue boosting the province’s population, but inter-provincial migration removes some of that gain.

Elevated commodity prices should continue to provide a lift to the regional outlook next year, as prices of the province’s key exports remain favourable with the ongoing global geopolitical conflict. As an export province, Manitoba could face some headwinds from weaker US demand next year but is also more insulated than other export provinces since half of its exports are towards other jurisdictions in Canada. Domestic demand should remain relatively strong in Canada compared to most of its trading partners.

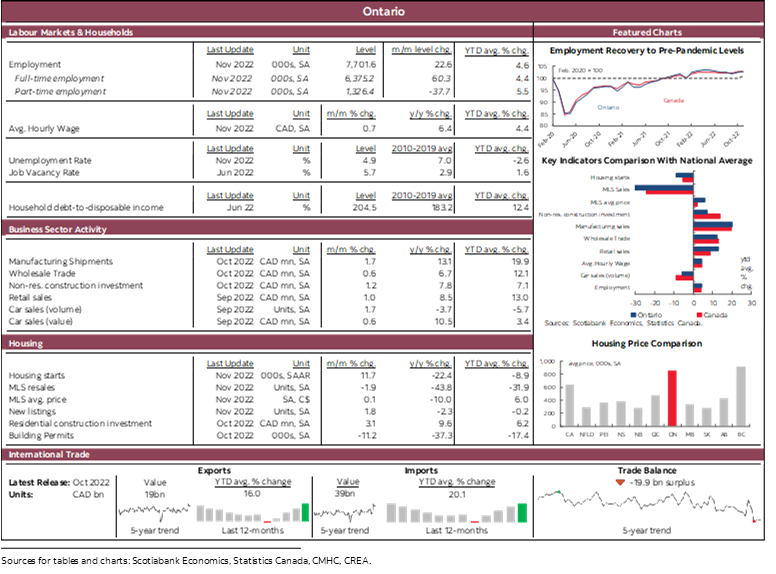

ONTARIO

Ontario’s real growth held up firmly in the second quarter, led by strong household spending and exports. We see the momentum slow rapidly as the impact of rising interest rates disproportionally affects the province, where minimal real growth is expected next year (0.5% in our current forecast). The province has seen the largest housing market correction in the country as average sale prices plunged by -16.2% since February’s peak, and sales contracted by -36%. The secondary effect of a housing market slowdown is weaker construction activity—residential investment fell at twice the speed as the national average in real terms—further weighing on growth. Slowing economic activity will also likely weigh on the finance and insurance sectors, which make up over 10% of Ontario’s real output.

Manufacturing output growth will likely face more headwinds as the year progresses, owing to persistent supply disruptions, higher input costs, and labour shortages in the industry, but an improved auto sector outlook next year provides some upside. The province’s critical auto sector saw slower-than-anticipated production recovery in the first half of the year as chip shortages remained the bottleneck. The rebound in auto production will nevertheless contribute to the province’s economic growth—Wards Automotive forecasts a 13% growth in Canadian light vehicle production in 2022 and a further 17% in 2023.

On the flip side, sizable public investments in infrastructure will offset falling residential investments and give growth a boost. In the mid-year fiscal update, the provincial government pledged over $20 bn in infrastructure spending each year for the next two years. Major investments have been flowing in the province’s electric vehicle industry, including $12.5 bn in EV and EV battery-related manufacturing investments in the past two years, with the first production operations scheduled to begin in 2024.

On the fiscal front, the rollout of childcare rebates that started this fall provides a near-term stimulus of $1.1 bn in 2022 and should improve labour participation and productivity in the long run.

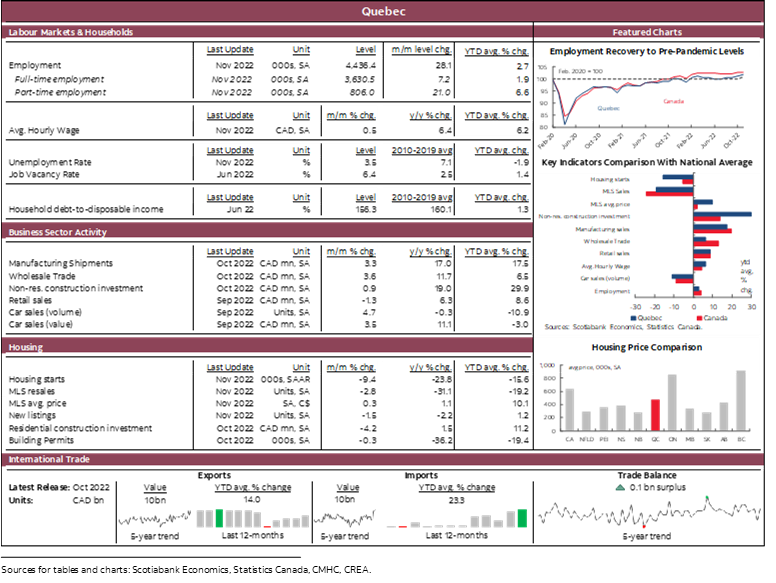

QUEBEC

The economic expansion continues to slow in Quebec after a sharp decline of real growth in Q2 to +0.3% q/q from +1.4% q/q in Q1. We expect an expansion of around 3% in Quebec this year on the back of strong real growth in the first half of the year, with a much softer growth projection of around 0.6% in 2023. Weaker US demand poses strong headwinds to exports and manufacturing in the province, but a softer CAD could act as a buffer.

Household consumption will likely remain more resilient in Quebec compared to its peers, with the household saving rate well above the national average since 2016, and a lower household debt burden proportional to disposable income than in other large provinces. The large fiscal stimulus announced by the province should help support consumption but may slow the deceleration of inflation.

Quebec has one of the highest job vacancy rates in the country while the unemployment rate remains historically low. Labour shortages stemming from an aging workforce, the low employment rate among older workers, and slow population growth will likely remain a major constraint on growth—especially in industries such as construction and manufacturing where vacancy rates are the highest. The province plans to make up for the labour supply gap with a record immigration target this year (71k, including 15k carry-over from 2021).

Quebec should see a more modest slowdown in residential investment—the province’s housing market has been adjusting in response to rising interest rates and declining affordability, but to a lesser extent than the national average. Government infrastructure spending, including the $80 bn investments planned in the next five years under the 2022–2032 Québec Infrastructure Plan (QIP), will contribute to growth in the medium term.

NEW BRUNSWICK

Highly dependent on trade, declining exports due to weaker demand from the US and Europe will no doubt be a major drag to New Brunswick’s economy next year, but the province has some advantages that keep growth close to the national average next year. The province witnessed soaring house prices during the pandemic and only saw a slight decline in prices since the February peak. Average sales prices are still close to 50% above pre-pandemic levels—the highest among all provinces. Resale activity mostly normalized from last year’s unsustainable growth and was down -19.6% year-to-date. Housing starts held up firmly and rose by 20.7% so far this year compared to the same period last year. As high interest rates work through the system, we should continue to see slowdowns in sales activities and further drops in prices. But demand for housing should remain strong given the province’s growing population and put a floor on the scope of decline.

Although New Brunswick’s economy will not be spared from a slowdown in consumption as the result of restrictive interest rates and the broader erosion of purchasing power from high inflation, consumer demand should be more resilient than the rest of the country. The province has the lowest debt-to-disposable income ratio in the country, which helps support consumption in a high-interest-rate environment. Housing is still very affordable in the province, providing some relief against the rising cost of living. The growing population should continue to help contribute to the consumption of both goods and services.

NOVA SCOTIA

Nova Scotia saw its population surge by over 3% so far in 2022 to 1.03 mn, bringing robust growth to the housing sector. Average sale prices rose by a whopping 62% during the pandemic up until the February peak—the highest among all provinces—and even with the -8.5% pullback since then, prices are still 48% higher than pre-pandemic levels. Resale activities slowed by -21.1% so far this year compared to the same period last year—other than the impact of rising mortgage rates, this could also be the result of the rebalancing of font-loaded purchases during the pandemic. Hence, demand should remain firm on the back of strong population growth and put a floor to the slowdown. So far in the ongoing housing downturn, the province’s housing starts dropped slightly, but residential construction investment is still tracking strong growth—both well above the national average. With solid demand from the growing population and still-high prices, construction activity in the province should continue its momentum next year.

Aiming to double the population by 2060, Nova Scotia would need to sustain at least 1.8% population growth every year. Efforts will be needed to achieve that goal—the average pace of population growth is 1.2% since the province started to see consistent population gains in 2016. Overall, we expect further decline in the housing sector to drag growth next year, offset by the impact of continued population growth.

PRINCE EDWARD ISLAND

The Island’s economy was lifted by its population boom this year, which grew by 3.8% year-over-year as of November—the highest in the country. Close to two-thirds of the increases resulted from newcomers to the country, with the rest mostly contributed by soaring interprovincial migration to the island that started in 2019. We expect strong growth to continue here as the record-level population gain continues to bring strong demand for goods, services, and housing.

The labour market churned out some strong job gains despite the impact of Hurricane Fiona in September. Employment was up 6.7% this year as of November, much higher than the 3.9% national average. Wage growth in PEI also outpaced all other provinces except New Brunswick. Employment has started to soften in recent months as growth slows, and we expect the trend to continue into next year until economic conditions stabilize.

The province tables its largest capital budget in history on November 2nd, pledging to spend $1.2 bn in the next five years (2.7% of nominal GDP each year), with $308 mn planned for FY23 on health care, highways, schools, and publicly-owned housing units, up 24% from the fiscal year prior. This could bring material upside to growth next year.

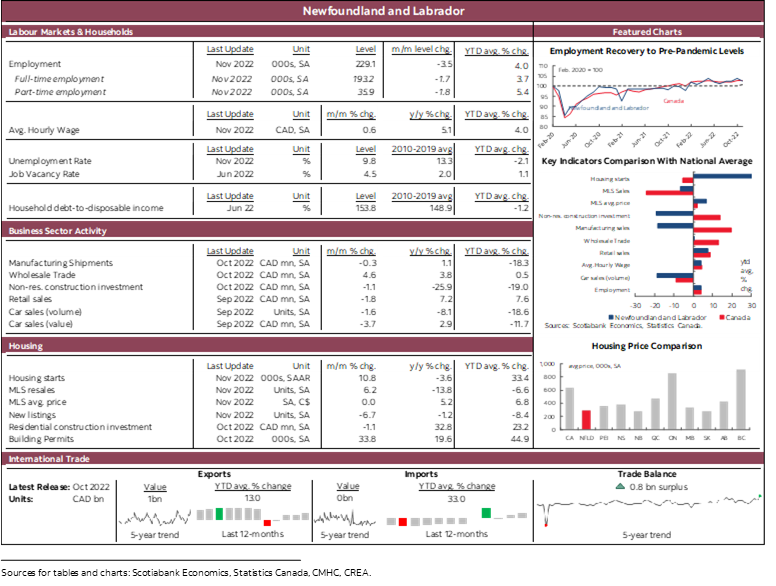

NEWFOUNDLAND AND LABRADOR

We expect higher growth in Newfoundland and Labrador in 2023 compared to 2022, underpinned by an improved outlook in the province’s oil and gas industry. Despite favourable oil prices, the economic growth in Newfoundland and Labrador this year has inevitably been held back by falling oil production. Crude oil production was down -26% compared to last year as the Terra Nova site remained shut down. 2023 growth should get a boost with the planned reopening of the Terra Nova site later this year and the conversion of the Come By Chance Refinery. The progression of major projects such as The Bay du Nord project could provide additional employment opportunities down the line.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.