ECONOMIC OVERVIEW

- November is coming to an end with a deluge of key data in Latam and the G20 and an uncertain (delayed) OPEC decision ready to challenge a very strong month in markets that saw large gains in equity, rates, and currency markets driven by traders’ hopes that key central banks are done hiking—and may even begin cuts sooner.

- A collection of Chile macro data, inflation figures in Peru and Brazil, and some second-tier data in Mexico and Colombia await in Latam, while US PCE inflation is on tap ahead of the start of the Fed’s communications blackout next Saturday. Chinese PMIs, Canadian jobs and GDP, and Eurozone CPI will also influence trading.

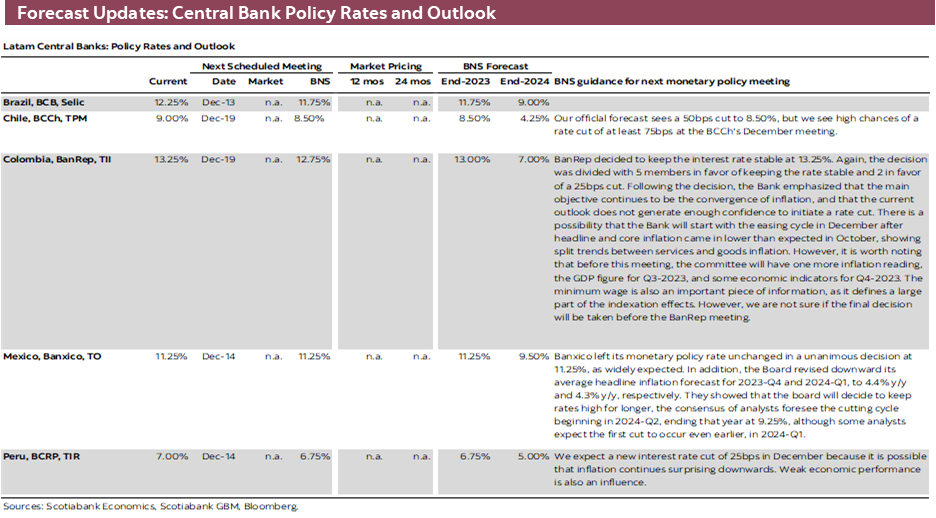

- Inflation in Peru is expected to fall below 4% in next week’s release, comfortably allowing another BCRP cut on the 14th; we see 25bps some think it could be 50bps. Chile’s economy may have grown in year-on-year terms in October after registering no change in September, but a sequential decline (if large enough) would reaffirm our view of a 75bps or greater BCCh cut next month.

- Unemployment data out of Colombia and Mexico and respective releases of current account and international trade/remittances data should mostly come and go (barring huge surprises). Banxico’s quarterly report and BanRep’s non-policy meeting are worth monitoring. Brazil also publishes mid-month inflation data, but the near-term path for the BCB already looks very clear.

PACIFIC ALLIANCE COUNTRY UPDATES

- We assess key insights from the last week, with highlights on the main issues to watch over the coming fortnight in the Pacific Alliance countries: Chile and Peru.

MARKET EVENTS & INDICATORS

- A comprehensive risk calendar with selected highlights for the period November 25–December 8 across the Pacific Alliance countries and Brazil.

ECONOMIC OVERVIEW: CHILE MACRO, PERU INFLATION; KEY G20 DATA

Juan Manuel Herrera, Senior Economist/Strategist

Scotiabank GBM

+44.207.826.5654

juanmanuel.herrera@scotiabank.com

- November is coming to an end with a deluge of key data in Latam and the G20 and an uncertain (delayed) OPEC decision ready to challenge a very strong month in markets that saw large gains in equity, rates, and currency markets driven by traders’ hopes that key central banks are done hiking—and may even begin cuts sooner.

- A collection of Chile macro data, inflation figures in Peru and Brazil, and some second-tier data in Mexico and Colombia await in Latam, while US PCE inflation is on tap ahead of the start of the Fed’s communications blackout next Saturday. Chinese PMIs, Canadian jobs and GDP, and Eurozone CPI will also influence trading.

- Inflation in Peru is expected to fall below 4% in next week’s release, comfortably allowing another BCRP cut on the 14th; we see 25bps some think it could be 50bps. Chile’s economy may have grown in year-on-year terms in October after registering no change in September, but a sequential decline (if large enough) would reaffirm our view of a 75bps or greater BCCh cut next month.

- Unemployment data out of Colombia and Mexico and respective releases of current account and international trade/remittances data should mostly come and go (barring huge surprises). Banxico’s quarterly report and BanRep’s non-policy meeting are worth monitoring. Brazil also publishes mid-month inflation data, but the near-term path for the BCB already looks very clear.

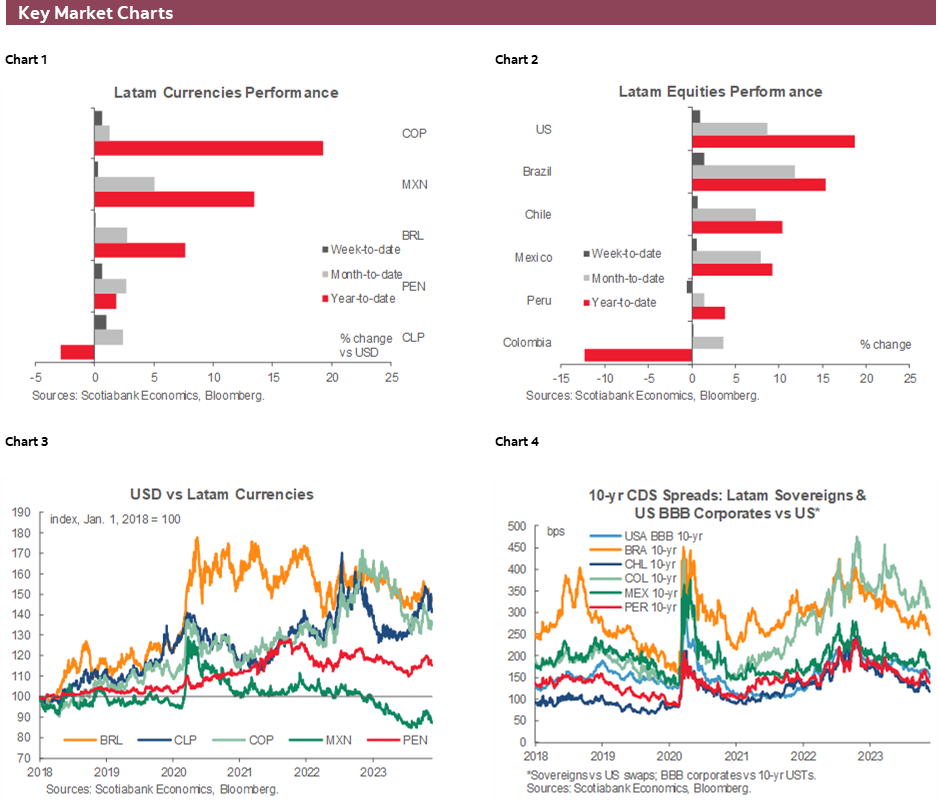

Next week, traders will say goodbye to one of the market’s best months of the year, eyeing the final round of central bank decisions before activity quiets down to close out 2023. Since end-October, on net, we’ve seen a half-point or so drop in US 10yr yields, an 8–10% rally in global equity aggregates, a 2.5–3.0% depreciation of the US dollar on a broad basis (including a 5% MXN rise), and a 5%+ fall in WTI oil vs 3%+ and 10%+ gains in copper and iron ore, respectively.

But, before we can cash in these moves for the month, a busy calendar in Latam and abroad over the next few days stands to challenge or confirm views on expected policy easing in coming quarters that was a crucial tailwind for the positive mood in November. A collection of Chile macro data, inflation figures in Peru and Brazil, and some second-tier data in Mexico and Colombia await in Latam. Around the globe, the last round of Fedspeak before the pre-meeting communications blackout, US PCE inflation, and an uncertain OPEC+ virtual meeting—among other key G20 data and decisions—also figure as top items to monitor.

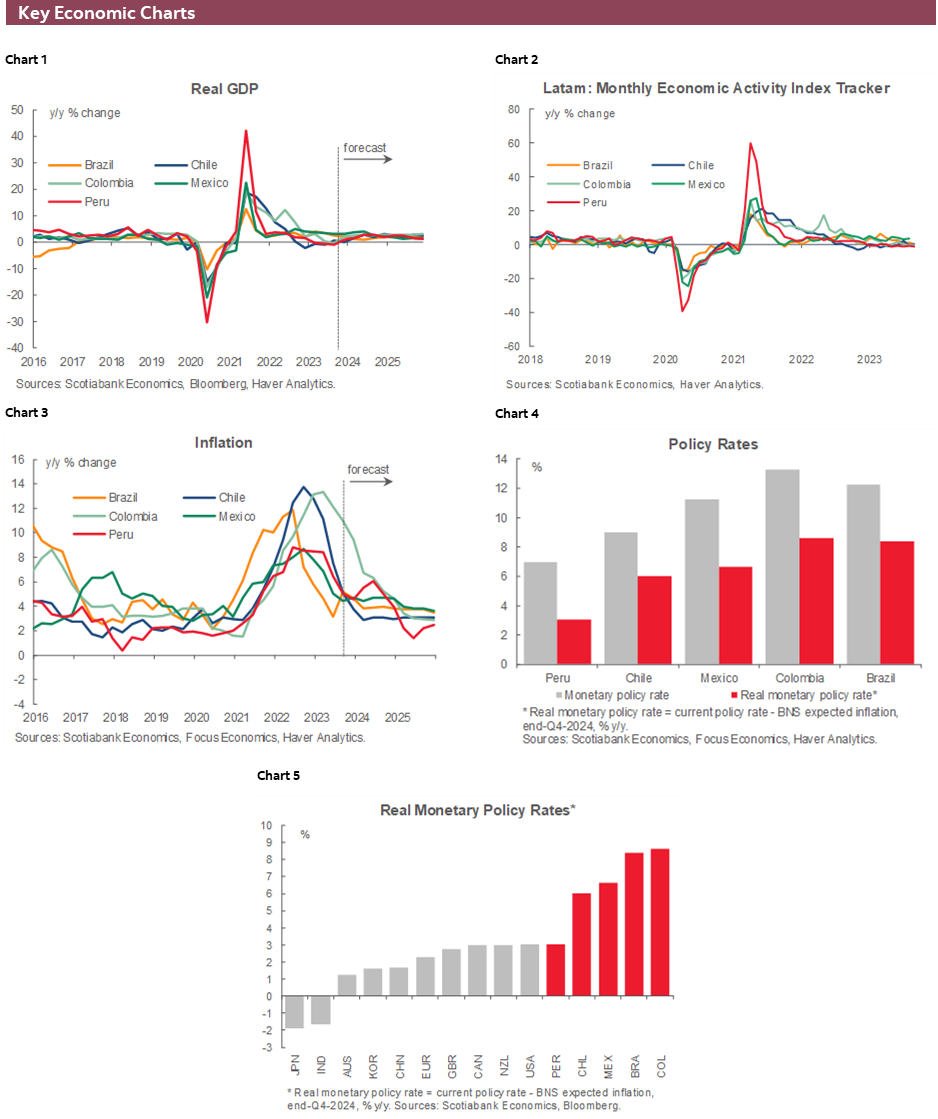

Of the Latam data due next week, perhaps the most important release for the respective local market will be Peru’s November inflation print out on Friday. The BCRP is very likely on track to reduce its reference rate for a fourth consecutive time in mid-December, but there’s still the question of whether it will be a 25bps or 50bps cut then, or even if a January cut or skip will follow. GDP data for Q3 released this week showed that the economy contracted 1.0% y/y with sizeable drags from public and private investment. In today’s report, our economists in Lima detail their projection for inflation to fall just below 4% y/y for the first time in two years. Both GDP and inflation data give the BCRP the green light to continue cuts. The team also highlight encouraging trends in severe El Niño odds, with the phenomenon an important inflation risk for the BCRP’s calculus, and congressional items on the horizon: the approval of the 2024 budget and a bill on a seventh private pension funds withdrawal.

Chile’s release calendar is the busiest of all in Latam, including unemployment, manufacturing/ industrial production, retail sales, and economic activity data during the second half of the week. The industry-level data out on Thursday will be a strong guide for the Imacec print on Friday; we project an 8.5% y/y drop in retail sales. In today’s weekly, our colleagues in Chile outline their expectation of a soft 0.4% y/y output expansion after zero change in September. This reflects a more favourable base of comparison rather than an improvement in fortunes, as we anticipate a month-on-month contraction in activity.

The flood of data should play an important role in the BCCh’s thinking on the cut size to be rolled out next month. Like in the case of the BCRP, the BCCh may also consider a larger reduction than their latest 50bps. But unlike the BCRP, Chilean policymakers will study a return to a larger cut (75bps or more) cut after preferring a smaller, more cautious, move that owed to external conditions—these have turned more favourable. Next week’s data should show a sluggish economy in need of less restrictive settings, with markets already tilted towards 75bps cuts at each of the next two decisions.

Mexico and Colombia schedules have a few bits and pieces to watch, but none are likely to move markets all that much. Both publish unemployment data, Mexico has international trade and remittances data, and Colombia releases current account figures. On the central bank front, Banxico’s quarterly inflation and economy report will outline in greater detail the bank’s outlook—and may reinforce their recent less hawkish guidance. BanRep’s board gather on Thursday for a non-monetary policy meeting, so no changes to the 13.25% overnight rate are due, but the discussion may build a consensus for cuts to begin in December (25 or 50bps).

Elsewhere in the region, Brazil releases mid-Nov CPI data where a sub-5% headline inflation print is seen on a 0.3% m/m rise. This monthly gain would be below the average in the decade before the pandemic, while the y/y deceleration from 5.1% reflects a more a favourable base than that which lifted y/y prints in Aug–Oct. There’s a bit of a lull in terms of adjusting near-term expectations for the BCB as, this week, Gov Campos Neto reinforced their view that the bank has “space to lower rates and still be in the restrictive camp”, with markets seeing at least two more 50bps reductions at the next two decisions. The BCB is already a total of 150bps cuts into its easing cycle to a target rate that sits at 12.25% or 7–7.5ppts above current annual inflation; for comparison BanRep has a 13.25% overnight rate but inflation last printed 10.5%. Fiscal developments remain a focus of Brazilian markets amid upward revisions to deficit figures that highlight the rising odds that Min Fin Haddad will be unable to deliver on his zero-deficit target in 2024, as loose spending by Lula does not find an offset via tax increases (and other revenue-raising measures). Brazilian unemployment data should come and go as far as markets are concerned.

Outside of the region, Canadian employment and Q3 GDP data are unlikely to move the needle as far as BoC December hikes pricing goes (those are extremely low odds) but could influence views around how long the peak at 5.00% will be. Thursday’s US PCE inflation (the Fed’s preferred measure) and a second run at Q3 GDP figures on Wednesday, among other data, will accompany the last speaking engagements of Fed officials ahead of the pre-meeting blackout next Saturday. Global markets will also be highly sensitive to Eurozone CPI releases that begin on Thursday in Germany and Spain, to be followed by the Eurozone, France, and Italy on Friday. In Asia Pacific, Chinese official PMIs on Thursday stand as an important driver of global sentiment (and the commodity prices that impact Latam assets) while we continue to fish for headlines and developments on the fiscal support front. Australian CPI on Wednesday, and policy decisions in New Zealand and Korea (hold expected for both) round out the economic week. Possible OPEC+ leaks ahead of the cartel’s November 30th meeting are bound to inject volatility in crude oil prices (and petro-currencies).

PACIFIC ALLIANCE COUNTRY UPDATES

Chile—Slight Y/Y GDP Growth Forecast for October, but Decline at the Margin

Anibal Alarcón, Senior Economist

+56.2.2619.5465 (Chile)

anibal.alarcon@scotiabank.cl

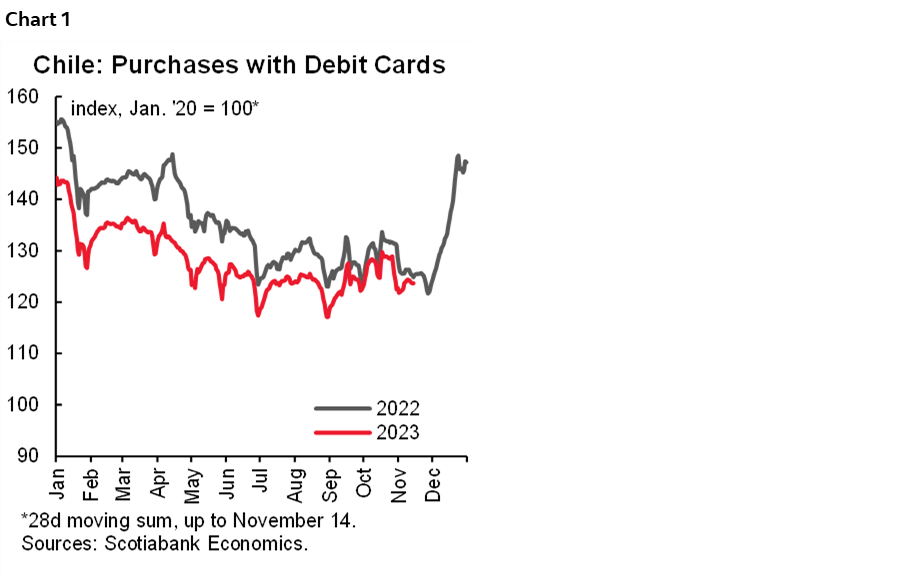

Recent BCCh GDP data for Q3-23 revealed a stabilization of consumption at low levels (see our Latam Daily), as expected. In Q3, durable goods consumption rebounded slightly from the previous quarter, although it remained at low levels. On the other hand, non-durable goods consumption (42% of total private consumption), remained stable, so private consumption did not show dynamism and stabilized close to its lowest level. Based on our high-frequency indicators, with information as of November 14th, goods consumption continues to show no dynamism in the Q4, both at the durable and non-durable goods levels (chart 1).

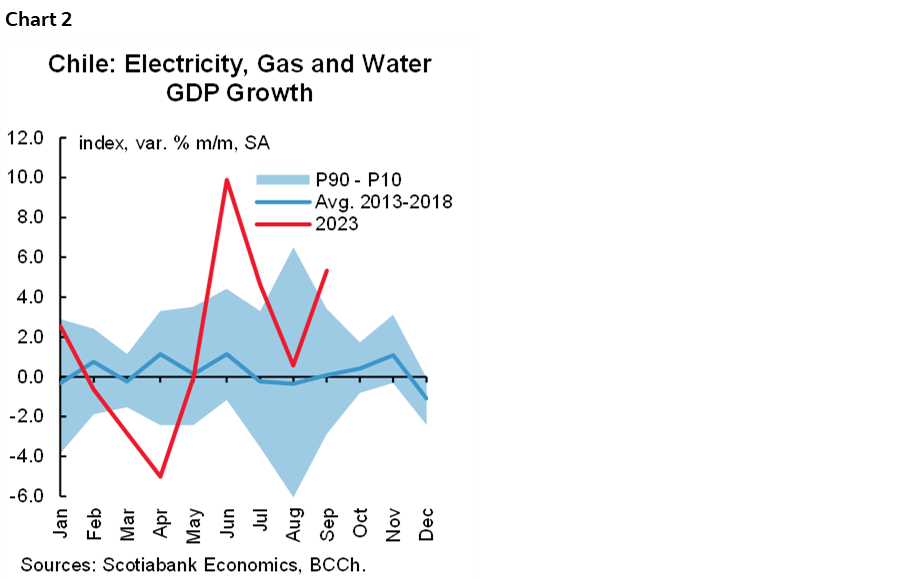

On Friday, December 1st, the BCCh will publish October GDP, for which we project a y/y growth between 0% and 1%, favoured by the basis of comparison, as it would show a drop when compared to the previous month. In this sense, we project m/m contraction in non-mining GDP, which would be driven by a drop both in commerce and in services. Based on our high frequency data of debit card purchases, we project an 8.5% y/y decline for Retail Sales in October. In addition, we do not see dynamism in the electricity sector after the high contribution in Q3 thanks to the rains (chart 2).

Finally, we project a seasonal decrease in the unemployment rate to 8.8%, which would be explained by higher job creation compared to the expected increase in the labour force. However, our view is that the Chilean labour market shows relatively loose conditions according to a broad set of indicators that we monitor on an ongoing basis (see our Latam Weekly).

Peru—Inflation to Continue Falling, but Beware of Congressional Changes to the Budget

Guillermo Arbe, Head Economist, Peru

+51.1.211.6052 (Peru)

guillermo.arbe@scotiabank.com.pe

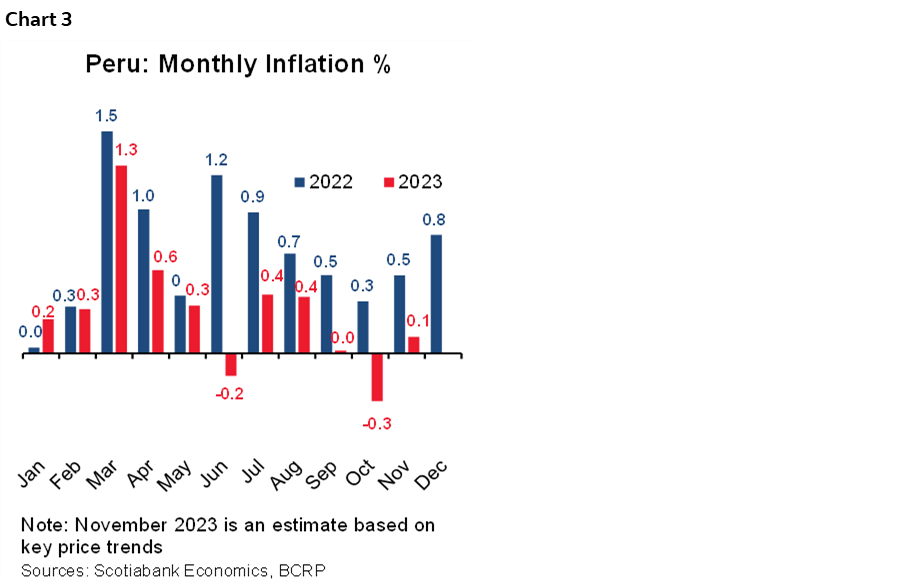

We finally have a few positives, albeit very mild and tentative ones, to point to for Peru. According to the key prices that we follow, inflation is trending at 0.11% so far for the month of November. If the trend holds for another week, twelve-month inflation could decline from 4.3% in October, to just under 4.0% when the number is released for November next Friday. Note that in October, key prices pointed to a similar monthly rise, and monthly inflation actually fell, -0.3%, in the end. Given the trend in local gasoline prices, there appears to be a similar downside risk in November.

Even if inflation should surprise us in November and not quite fall below the 4% threshold, it most certainly should do so in December. In December 2022 monthly inflation had been high, 0.8%. Part of the high number is seasonal, monthly inflation is always higher in December, but even so, this year monthly inflation should easily fall below last year’s register.

For inflation to fall under 4% for the first time in over two years gives the BCRP ample room to continue reducing its reference rate in December as we expect. The question is, rather, will the BCRP continue reducing the reference rate in January, given the current downtrend in inflation? Well, that will depend on how El Niño is shaping up. The BCRP will have from now until January 11th to figure that out.

So how is El Niño shaping up? Better. According to Peru’s official El Niño monitoring agency, ENFEN, the likelihood of the 2024 El Niño being strong or worse has fallen from 50% to 43%. This is still high, but the change in trend provides hope. The probability of El Niño being moderate also fell, slightly, from 47% to 42%. What has risen is the likelihood of El Niño being mild, which has risen from 3% to 14%. To add to this, coastal sea temperatures continue falling, and are moving away from the 1997–98 strong-Niño trend, and towards the 2017 moderate Niño trend.

Two items of particular importance are on the congressional agenda over the next two weeks. One is the 2024 budget, the discussion of which is currently underway. The Executive is grappling with Congress over spending initiatives that Congress is seeking to introduce. The budget already calls for a 12% increase in spending. Given that the fiscal deficit is likely to begin 2024 at 3% of GDP, too much additional spending might become an issue. Congress has until the end of the month to approve the budget, but this could occur earlier if an agreement is reached.

The second item is the bill for a seventh withdrawal from the private pension fund system. A Congressional spokesperson has informally mentioned the likelihood that the committee studying the new withdrawal would have the initiative ready for discussion on the floor by November 30th.

| LOCAL MARKET COVERAGE | |

| CHILE | |

| Website: | Click here to be redirected |

| Subscribe: | anibal.alarcon@scotiabank.cl |

| Coverage: | Spanish and English |

| COLOMBIA | |

| Website: | Click here to be redirected |

| Subscribe: | jackeline.pirajan@scotiabankcolptria.com |

| Coverage: | Spanish and English |

| MEXICO | |

| Website: | Click here to be redirected |

| Subscribe: | estudeco@scotiacb.com.mx |

| Coverage: | Spanish |

| PERU | |

| Website: | Click here to be redirected |

| Subscribe: | siee@scotiabank.com.pe |

| Coverage: | Spanish |

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.