ECONOMIC OVERVIEW

- Another week, another broad-based rally across most asset classes. Next week, markets will get more clues to help refine expectations on when key G10 central banks may begin their easing cycles. The Fed’s meeting minutes, global PMIs, and Canadian and Japanese CPI are the highlights in a week that may see reduced volumes with US and Japanese holidays on Thursday.

- Next week in Latam, Chile, Peru, and Mexico all publish Q3 GDP data. But, there’s some staleness to these figures. In the case of Chile and Peru, monthly economic activity data have already given us a good idea of where the quarterly prints will land; +0.2% and –1.0% y/y, respectively, is our forecast. Chile’s BCCh is justified in continuing their large-cuts easing cycle, as the team outlines the looseness of local labour markets in today’s report.

- Mexico’s release is just a revision of a preliminary 3.3% y/y rise in GDP, so H1-Nov CPI out on Thursday is the data highlight. More importantly, however, Banxico’s meeting minutes will be key to judge how likely it is that officials may want to start rate cuts as soon as the February gathering. At the early-November decision, Banxico surprised with a guidance tweak to language regarding the time that will be spent at the current peak rate of 11.25%. Public comments by officials since the decision suggest a decently-sized group in the board may be eyeing a rate cut at the first meeting of 2024.

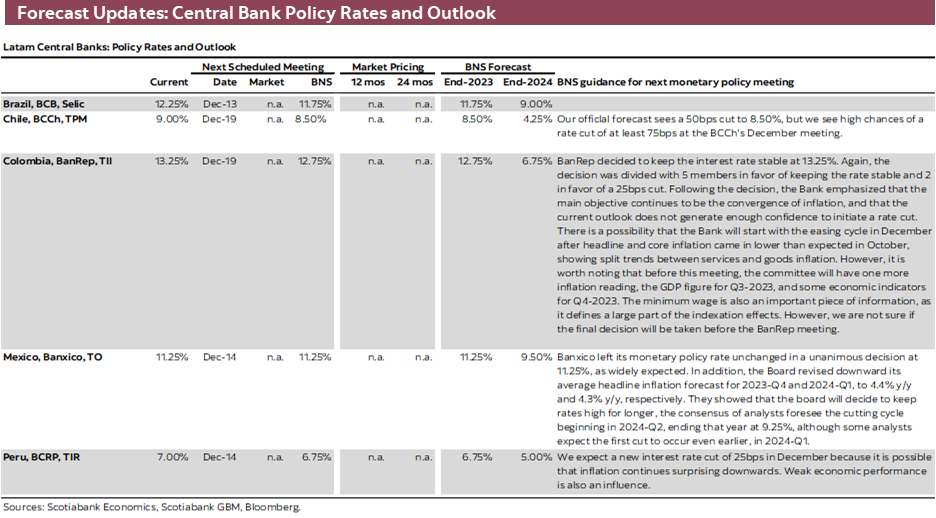

- Policymakers in Colombia could be more and more considering a December start to the easing cycle, especially on the back of a highly disappointing Q3 GDP print, versus still-high inflation prints and upside risks, that the team in Bogota break down in today’s weekly.

PACIFIC ALLIANCE COUNTRY UPDATES

- We assess key insights from the last week, with highlights on the main issues to watch over the coming fortnight in the Pacific Alliance countries: Chile and Colombia

MARKET EVENTS & INDICATORS

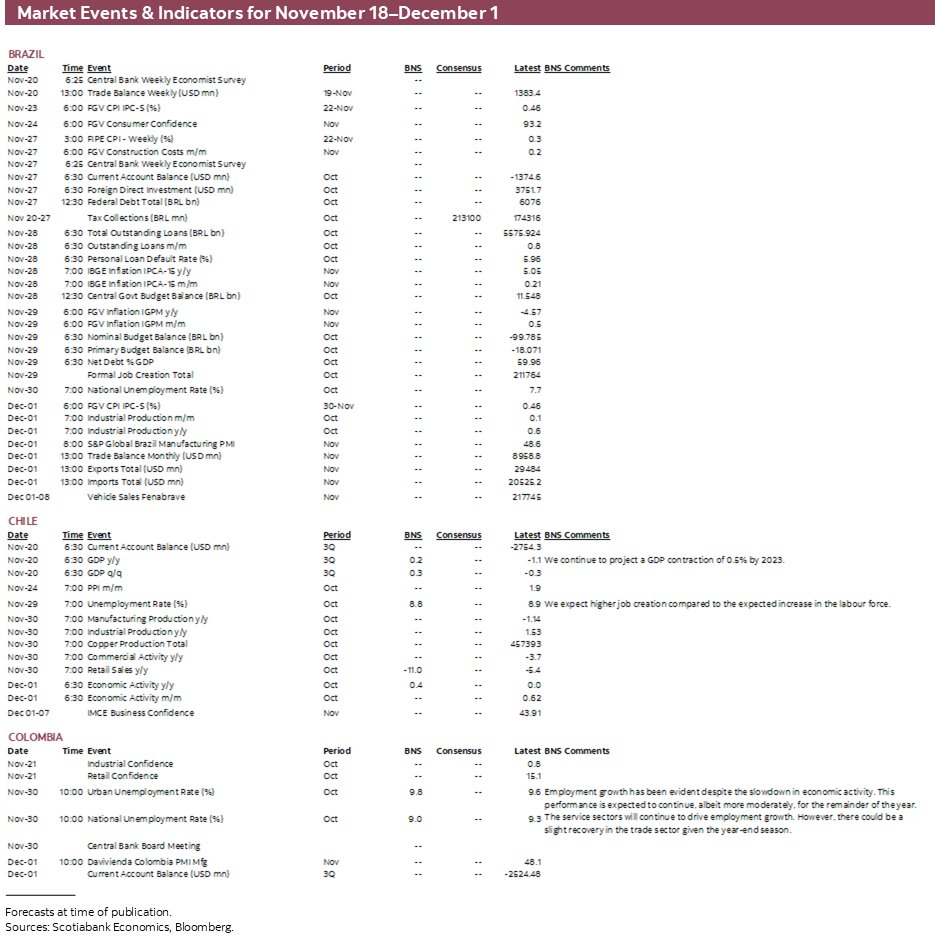

A comprehensive risk calendar with selected highlights for the period November 18–December 1 across the Pacific Alliance countries and Brazil.

ECONOMIC OVERVIEW: CHILE, PERU, AND MEXICO GDP; BANXICO, FED, AND ECB MINUTES; GLOBAL PMIS

Juan Manuel Herrera, Senior Economist/Strategist

Scotiabank GBM

+44.207.826.5654

juanmanuel.herrera@scotiabank.com

- Another week, another broad-based rally across most asset classes. Next week, markets will get more clues to help refine expectations on when key G10 central banks may begin their easing cycles. The Fed’s meeting minutes, global PMIs, and Canadian and Japanese CPI are the highlights in a week that may see reduced volumes with US and Japanese holidays on Thursday.

- Next week in Latam, Chile, Peru, and Mexico all publish Q3 GDP data. But, there’s some staleness to these figures. In the case of Chile and Peru, monthly economic activity data have already given us a good idea of where the quarterly prints will land; +0.2% and –1.0% y/y, respectively, is our forecast. Chile’s BCCh is justified in continuing their large-cuts easing cycle, as the team outlines the looseness of local labour markets in today’s report.

- Mexico’s release is just a revision of a preliminary 3.3% y/y rise in GDP, so H1-Nov CPI out on Thursday is the data highlight. More importantly, however, Banxico’s meeting minutes will be key to judge how likely it is that officials may want to start rate cuts as soon as the February gathering. At the early-November decision, Banxico surprised with a guidance tweak to language regarding the time that will be spent at the current peak rate of 11.25%. Public comments by officials since the decision suggest a decently-sized group in the board may be eyeing a rate cut at the first meeting of 2024.

- Policymakers in Colombia could be more and more considering a December start to the easing cycle, especially on the back of a highly disappointing Q3 GDP print, versus still-high inflation prints and upside risks, that the team in Bogota break down in today’s weekly.

The November rally in global markets kept going this week, as a smaller than expected US inflation reading, a PBoC liquidity injection, and a continued moderation of geopolitical risks, among other developments, contributed to a more upbeat trading mood. Rates markets are becoming more confident that we are at the peak of central bank rates and are adding to expectations of mid-2024 cuts—which, in some cases, may be a bit overdone.

So, G10 policymakers may be done hiking, but that doesn’t mean they are looking to cut anytime soon, unlike most in Latam among which Colombian and Peruvian central bankers may have found more reasons to ease policy in disappointing Q3/September GDP data released on the 15th. G10 officials will watch key figures out next week to gauge how long peak rates will last, where the highlights are PMIs across the globe and Canadian and Japanese CPI. The Fed, ECB, and RBA meeting minutes, and Canadian and UK fiscal updates are also on tap.

Activity may be somewhat subdued, however, as the week starts with closed markets in Mexico for Revolution Day, followed by trading suspensions in the US and Japan on Thursday. Argentinean markets are also shut on Monday, a day after the second-round vote for the country’s presidency that remains too close to call. Final polls ahead of blackout were tilted slightly in favour of libertarian Milei over economy minister Massa; radical change with goals of dollarization or more of the same that resulted in 140%+ inflation in October? The answer will not be obvious right away.

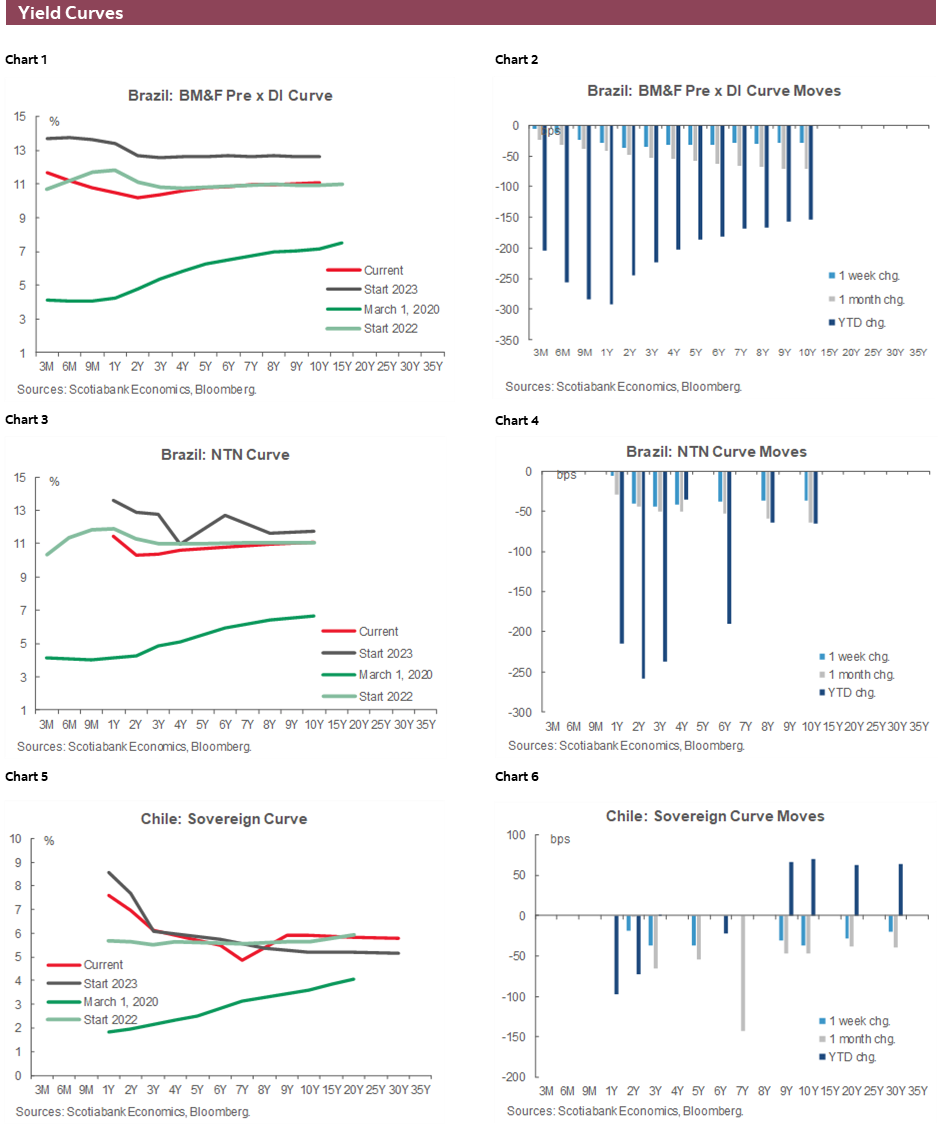

Next week in Latam, Chile, Peru, and Mexico all publish Q3 GDP data. But, there’s some staleness to these figures. In early-November, Chile released economic activity data for September that showed no year-on-year change in output against expectations of a 0.5% contraction, but this was thanks to the performance of the mining sector against sluggish services output (see Latam Daily). Excluding mining, Chile’s economy contracted 0.4% y/y in Q3-23 based on the monthly data. For next week’s full-quarter reading the team in Chile project a 0.2% y/y rise in GDP, roughly aligned with the average of the monthly economic activity numbers. We’ll also dissect Q3 current account balance figures due at the same time. In today’s Weekly, the team focuses on the looseness of domestic labour markets, a development that supports continued large cuts by the BCCh.

It’s a similar story for Peru’s Q3 GDP release in terms of stale data. Output fell a surprisingly large 1.3% y/y in September (see Latam Daily), exceeding our already more negative than consensus forecast of a 0.8% drop. It was an especially worrying result, considering that weakness was not simply concentrated in El Niño-impacted primary sectors, but spread throughout domestic demand industries, especially manufacturing and construction. With the monthly data at hand, Peru’s economy contracted for a third consecutive quarter, by 1.0% y/y in Q3 according to our economists.

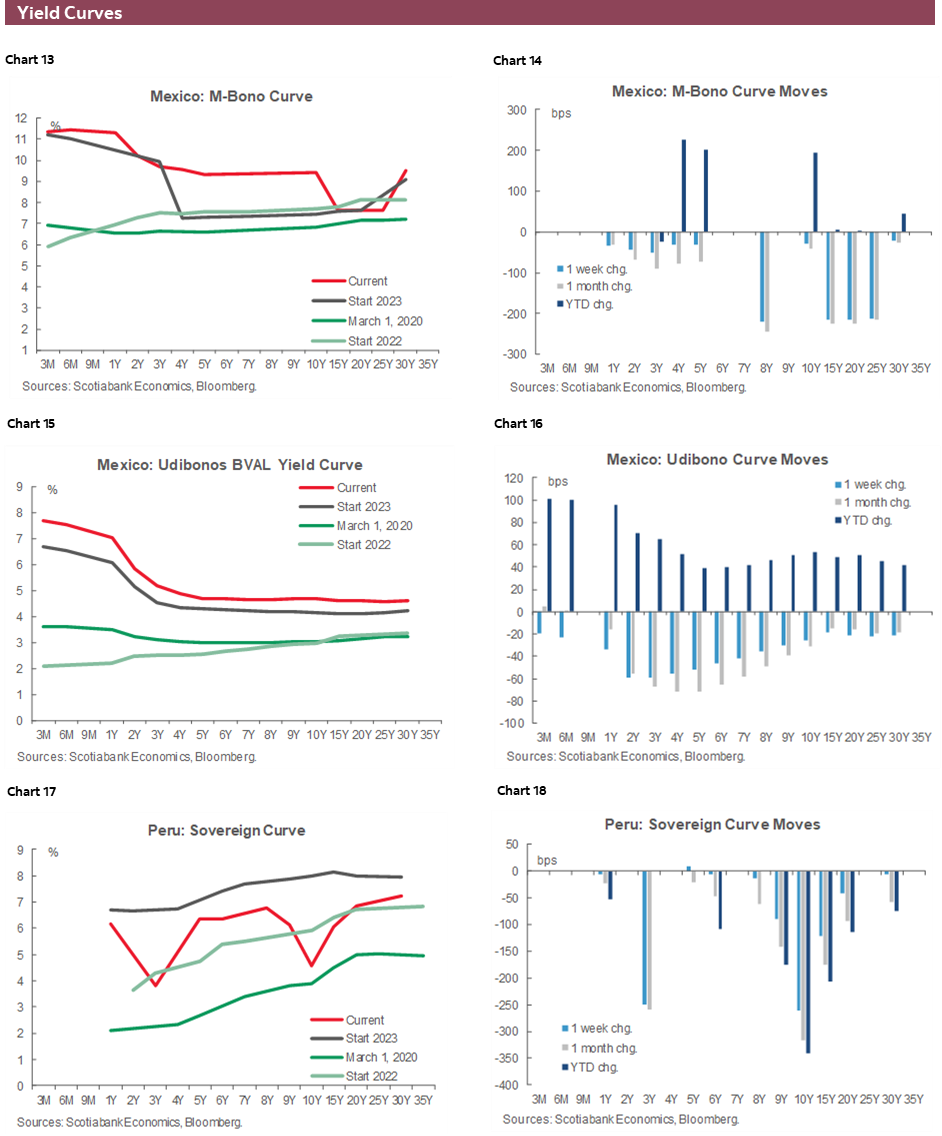

Mexico’s GDP data may be even less exciting as next week’s are a revision of preliminary figures of 3.3% y/y and 0.9% q/q expansions. Data-wise, markets may instead focus on Thursday’s bi-weekly H1-Nov inflation expected to print a roughly unchanged headline around 4.2% but a slight deceleration in core inflation to 5.2/3% from 5.5%. What may be more interesting will be Banxico’s November meeting minutes out a few hours after the CPI data. At this decision, officials surprisingly tweaked guidance on the time that will be spent at the rates peak, switching from the overnight rate having to remain at 11.25% “for an extended period” to “for some time”. Economists and markets went into Banxico’s announcement expecting no surprises and a maintenance of a well-articulated hawkish tone, with little data in between meetings to suggest a guidance change was warranted. Next week’s minutes may shed some light on why officials favoured this language tweak which has raised the odds of a Q1 rate cut versus those of a Q2 cuts start. In recent days, a handful of Banxico officials have spoken publicly, seemingly expressing a unified view that suggests the easing cycle will begin in Q1.

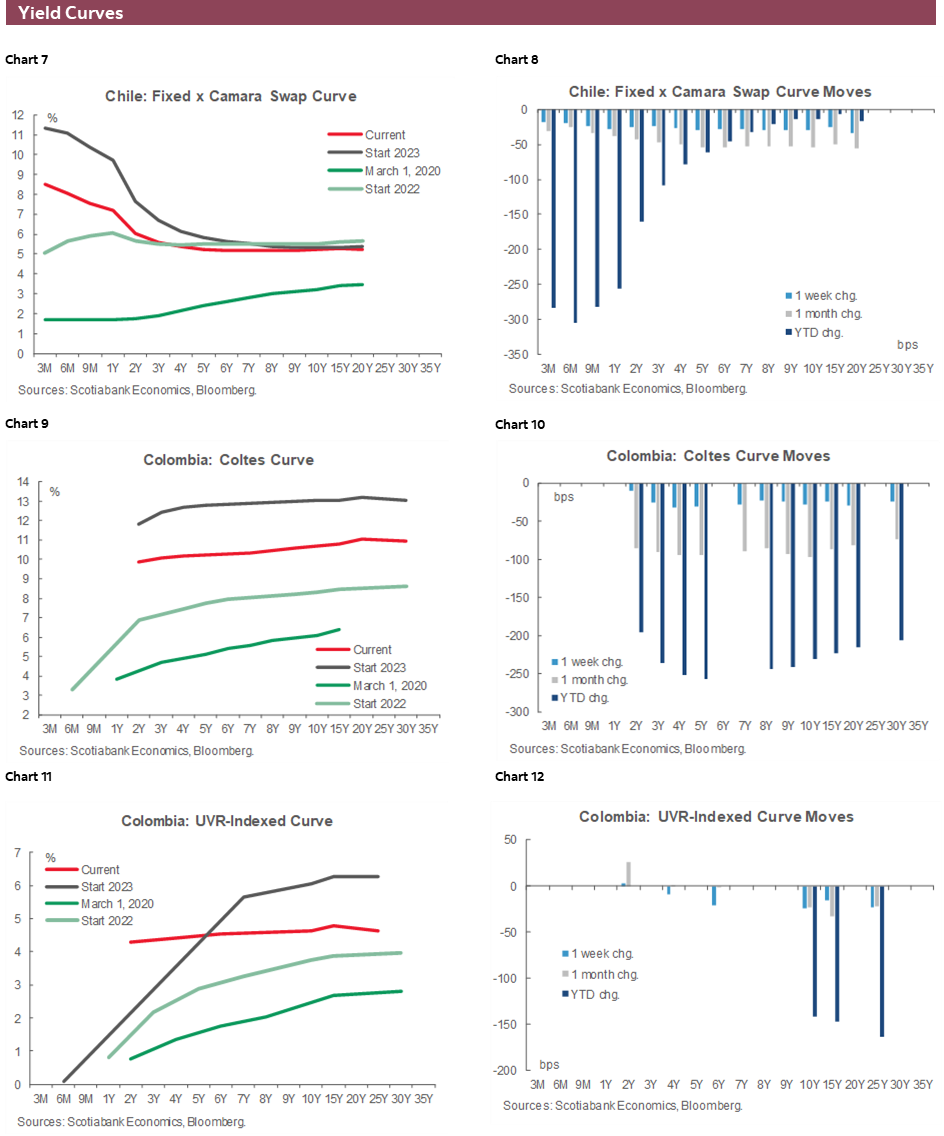

Colombia’s calendar is empty of key data, but we’ll be keeping an eye on political and monetary policy headlines. Earlier this week, President Petro again shook local markets with a call to overturn the country’s fiscal rule, in part to allow an increase in public spending to support the economy. Fin Min Bonilla chimed in, saying that it would be good to start a discussion on whether to keep the rule, though he did concede that this would require Congressional support—which we don’t expect. Q3 GDP data released on the 15th widely missed forecasts, printing a 0.2% q/q expansion (Scotiabank: 0.4%, Bloomberg median: 0.7%), tilting the balance in favour of a BanRep cut at the December decision—a move clearly backed by Bonilla who also sits on the board. In today’s report, our economists in Colombia give their take on the state of the country’s economy and the slow progress made in inflation moving towards target.

PACIFIC ALLIANCE COUNTRY UPDATES

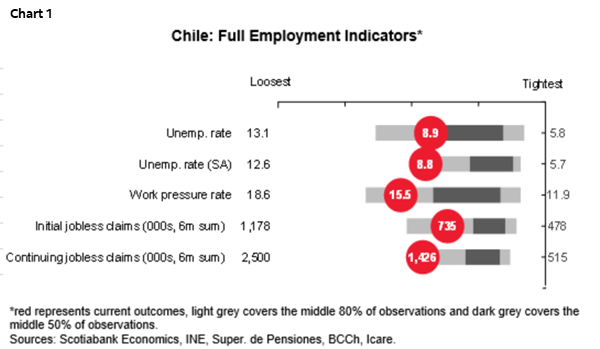

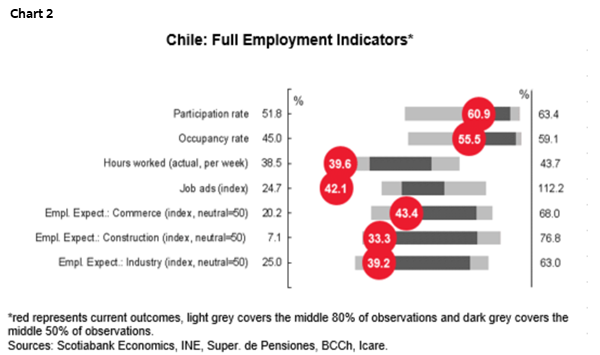

Chile—Loose Labour Market Conditions According to A Broad Set of Indicators

Anibal Alarcón, Senior Economist

+56.2.2619.5465 (Chile)

anibal.alarcon@scotiabank.cl

Chile’s labour market shows relatively loose conditions according to a broad set of indicators that we monitor on an ongoing basis. In charts 1 and 2, each row shows the latest observation of an indicator as a red dot. Greater labour market looseness is associated with red dots further to the left, while the gray shaded area shows the typical range of outcomes since records began. One of these indicators is the unemployment rate, which is near its highest level since 2010 with data as of September 2023. This is probably the reason why initial and continuing jobless claims are at the upper end of their historical range. Likewise, the high level of the unemployment rate is explained by an occupancy rate at the low end of its historical range and a participation rate that reflects the increase in the share of females joining the labour force. Along the same lines, if we add the number of employees looking for a new job and the number of people outside the labour force but willing to work, the result is a work pressure rate close to its maximum levels. Indicators of labour demand, such as job advertisements and firms’ hiring intentions, suggest that the labour market remains quite loose across economic sectors. Looking ahead, we estimate a slight improvement in traditional labour market indicators in the coming months, such as the unemployment rate, labour force and employment, but mainly for seasonal reasons. Looking at the broad set of indicators at seasonally adjusted levels, we expect the labour market to remain relatively weak in the coming months.

Colombia—What Does Recent Macro Data Mean for Colombia’s Monetary Policy? Is the Glass Half Full or Half Empty for Rate Cuts?

Jackeline Piraján, Senior Economist

+57.601.745.6300 Ext. 9400 (Colombia)

jackeline.pirajan@scotiabankcolpatria.com

The monetary policy rate has been at 13.25% (the highest of the century) since April 2023; seven months of rate stability at high levels could be considered a long time. However, it seems stubbornly high inflation has made the “higher for longer” mantra also true in Colombia. In this piece, we will talk about recent economic developments and key things to be aware of to guide expectations about the timing of the easing cycle.

On the economic front, the Q3 GDP print was significantly below expectations, with the first annual contraction since the pandemic episode, which is very unusual by Colombian standards. Although it might seem like a cause for concern, levelheadedness should prevail. After the pandemic, and even during 2022, Colombia showed a very steep recovery, but, unfortunately, it was an unsustainable trend.

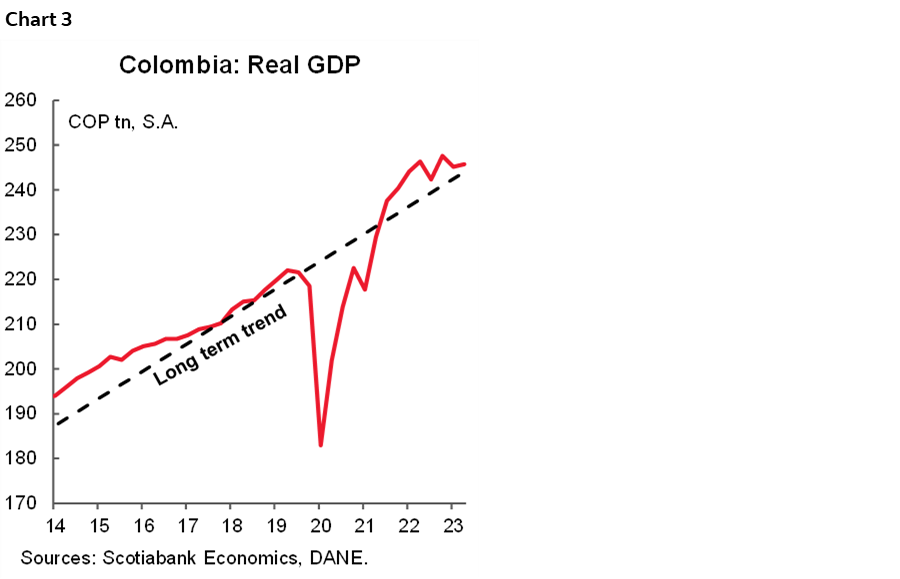

The post-pandemic recovery suddenly created a positive output gap that we are now seeing close at a fast pace (chart 3). At the beginning of the year, central bank projections pointed to GDP growth of 0.2%, assuming a faster closure of the output gap, and the current projection is at 1.2%, which suggests that, in any case, the economy has been doing better than initially expected.

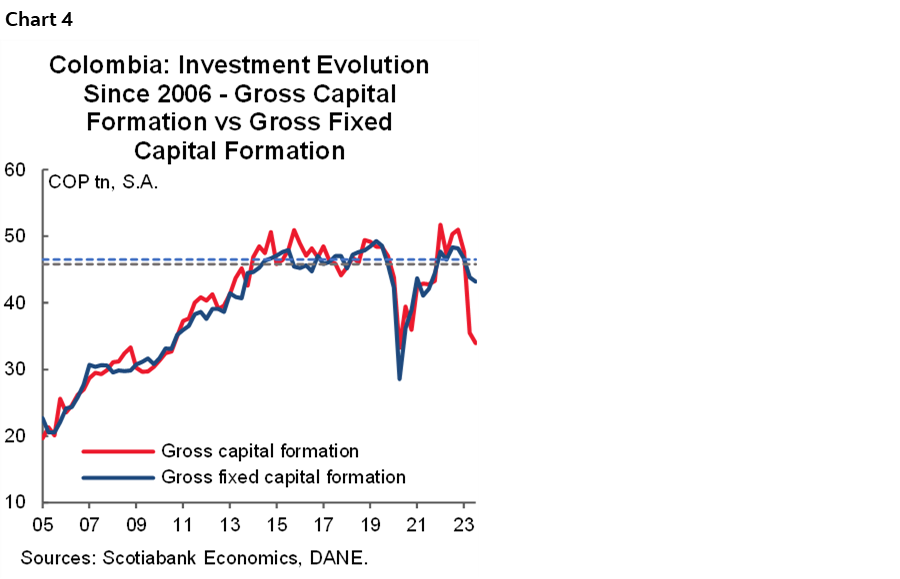

GDP data for Q3-23, released on November 15th, evidenced a consolidation of the private consumption downtrend, which the central bank welcomes. The main question mark is on investments since, in the year-to-September, it has contracted by 22.3% y/y on average; versus pre-pandemic, investment levels are 20% lower, while versus pre-elections, they sit 8% lower (chart 4). A combination of inventory reduction and definitively lower investment in private and public projects has resulted in this deteriorated picture. However, the question is whether it is only an issue that the central bank has to resolve or if other components are behind it.

Traditional theory points out that monetary policy tries to smooth cycles, and their contribution to potential GDP is thought to send a message of responsibility. That said, increasing the installed capacity of the economy (potential GDP) requires additional ingredients such as a stable rules framework and public investment, among others. The recent GDP data could be read as a good result in terms of household demand moderation, so monetary policy is working; but GDP is also a warning sign for the government that should incentivize them to implement their budget strategically.

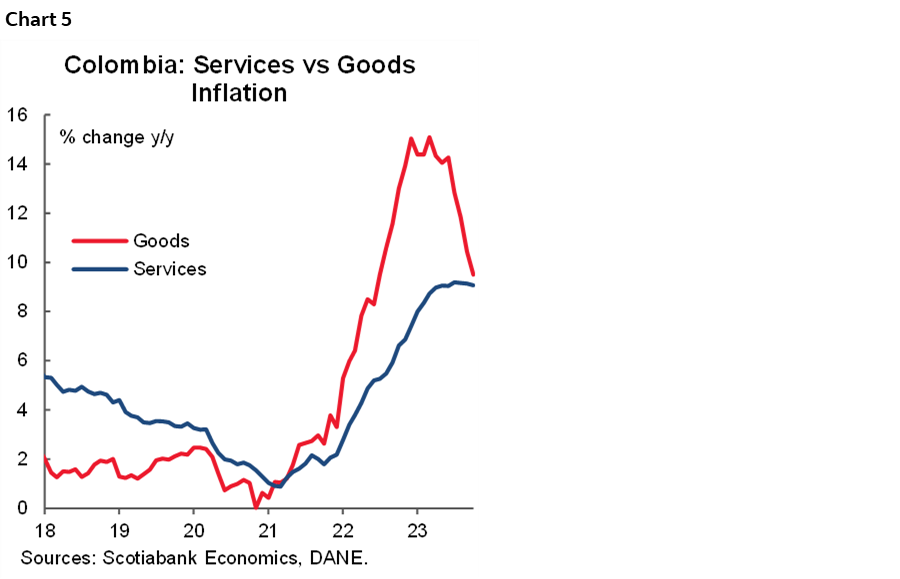

Regarding inflation, the headline figure showing a faster deceleration could put a potential December rate cut on the table. However, it is worth noting that what concerns BanRep are the possible risks ahead of 2024 and the possibility of missing the target again by the end of the following year. In that regard, October’s inflation showed a downside surprise thanks to a more moderate food inflation but also thanks to the vehicle prices contraction; meanwhile, rent fees and service-sector inflation remained sticky (chart 5), reflecting in one part still high indexation effects in the case of rent fees, and a still resilient demand in the case of services prices. Since the peak in Q1-23, headline inflation has passed from 13.3% to 10.5%, while core inflation (ex. food and regulated items) has only decreased from 10.5% to 9.3%. Again, we can see the glass either half empty or half full. But what really matters is whether risks on the horizon could tilt inflation into a slower convergence to the target. In that regard, minimum wage negotiations are key; moves around regulated prices, for instance, diesel prices, toll fees, and utility fees, are also relevant for BanRep’s board. That said, we are only one and a half months away from year-end, and this question hasn’t been resolved. The central bank is probably also feeling this degree of uncertainty.

In the political scenario, things are becoming more challenging for the government, with popularity falling, there is a lack of political support in congress, and weak economic activity highlighted in news headlines. Despite fears that it could trigger some hasty decision from the government, we think that this will not be the case. We are still very confident in Colombia’s institutional framework and the respect that the current government has shown to it. What to do with the fiscal rule is something that can only be defined within a legislative process (ergo, the government needs congress on board). Meanwhile, the main release worth keeping an eye on is the Financing Plan 2024, expected in December, since in the end it should show, with numbers, the respect for the fiscal rule.

Finally, regarding monetary policy, although we think the December meeting is trending towards a rate cut, we think that the central bank probably needs more evidence to see the glass half full. The second best option is waiting for more material evidence and starting decisive cuts, probably at a faster pace. Here, we didn’t talk about the Fed, but what the Fed decides is a big constraint for BanRep.

| LOCAL MARKET COVERAGE | |

| CHILE | |

| Website: | Click here to be redirected |

| Subscribe: | anibal.alarcon@scotiabank.cl |

| Coverage: | Spanish and English |

| COLOMBIA | |

| Website: | Click here to be redirected |

| Subscribe: | jackeline.pirajan@scotiabankcolptria.com |

| Coverage: | Spanish and English |

| MEXICO | |

| Website: | Click here to be redirected |

| Subscribe: | estudeco@scotiacb.com.mx |

| Coverage: | Spanish |

| PERU | |

| Website: | Click here to be redirected |

| Subscribe: | siee@scotiabank.com.pe |

| Coverage: | Spanish |

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.