ECONOMIC OVERVIEW

- A dozen or so global central banks, including the BCB, the Fed, the BoE, and the BoJ, decide on policy next week, delivering a mix of hikes, holds, and cuts—and ever-important guidance.

- The BCB will likely cut by 50bps again, supported by a softening pace of economic growth and progress in inflation (including in services prices). The Fed looks set to hold at 5.50%, but Powell and co should leave the door open to further tightening.

- Colombian and Mexican monthly economic activity is also on tap, due to show a weak rate of growth in Colombia against another strong print in Mexico. Yet, both countries’ central banks are not guiding that rate cuts will start soon. BanRep is battling sticky double-digit inflation alongside a clear slowdown, but Banxico is faced with constructive inflation trends (H1-Sep data out next week) but a highly-resilient economy.

- In today’s weekly, the team in Mexico looks at the challenges that the government's projection for a smaller deficit in 2025 faces—from a massive expected increase in 2024. In Peru, our economists break down the difficulties that El Niño brings about for GDP and inflation forecasts—and, thus, monetary policy.

PACIFIC ALLIANCE COUNTRY UPDATES

- We assess key insights from the last week, with highlights on the main issues to watch over the coming fortnight in the Pacific Alliance countries: Mexico and Peru.

MARKET EVENTS & INDICATORS

- A comprehensive risk calendar with selected highlights for the period September 16–29 across the Pacific Alliance countries and Brazil.

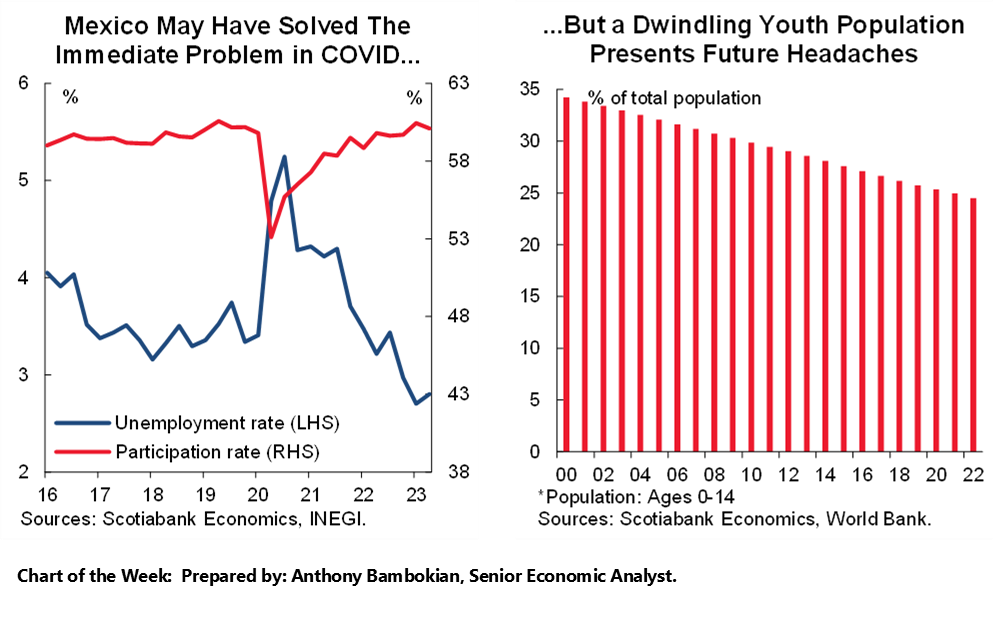

Charts of the Week

ECONOMIC OVERVIEW: BCB ATTENDS GLOBAL CENTRAL BANKS PARTY; LATAM ECON ACTIVITY DATA

Juan Manuel Herrera, Senior Economist/Strategist

Scotiabank GBM

+44.207.826.5654

juanmanuel.herrera@scotiabank.com

- A dozen or so global central banks, including the BCB, the Fed, the BoE, and the BoJ, decide on policy next week, delivering a mix of hikes, holds, and cuts—and ever-important guidance.

- The BCB will likely cut by 50bps again, supported by a softening pace of economic growth and progress in inflation (including in services prices). The Fed looks set to hold at 5.50%, but Powell and co should leave the door open to further tightening.

- Colombian and Mexican monthly economic activity is also on tap, due to show a weak rate of growth in Colombia against another strong print in Mexico. Yet, both countries’ central banks are not guiding that rate cuts will start soon. BanRep is battling sticky double-digit inflation alongside a clear slowdown, but Banxico is faced with constructive inflation trends (H1-Sep data out next week) but a highly-resilient economy.

- In today’s weekly, the team in Mexico looks at the challenges that the government's projection for a smaller deficit in 2025 faces—from a massive expected increase in 2024. In Peru, our economists break down the difficulties that El Niño brings about for GDP and inflation forecasts—and, thus, monetary policy.

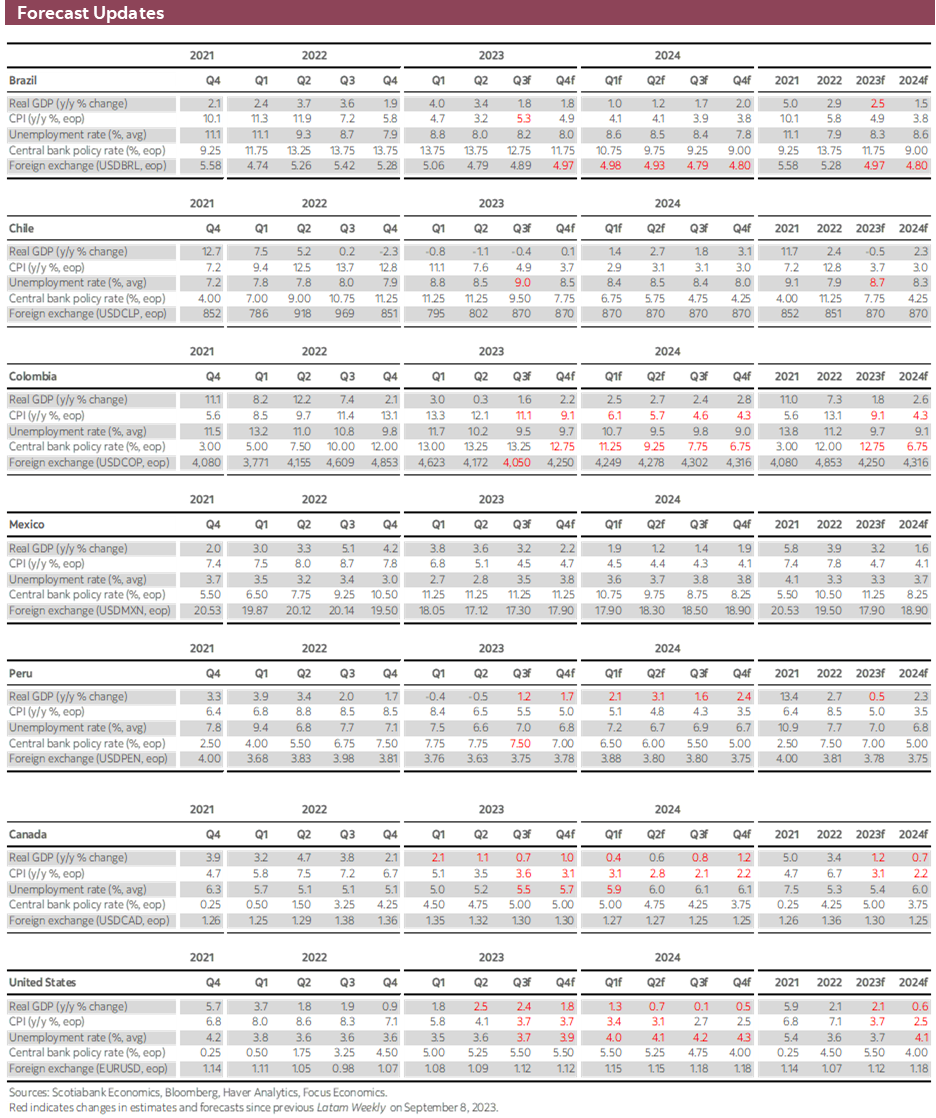

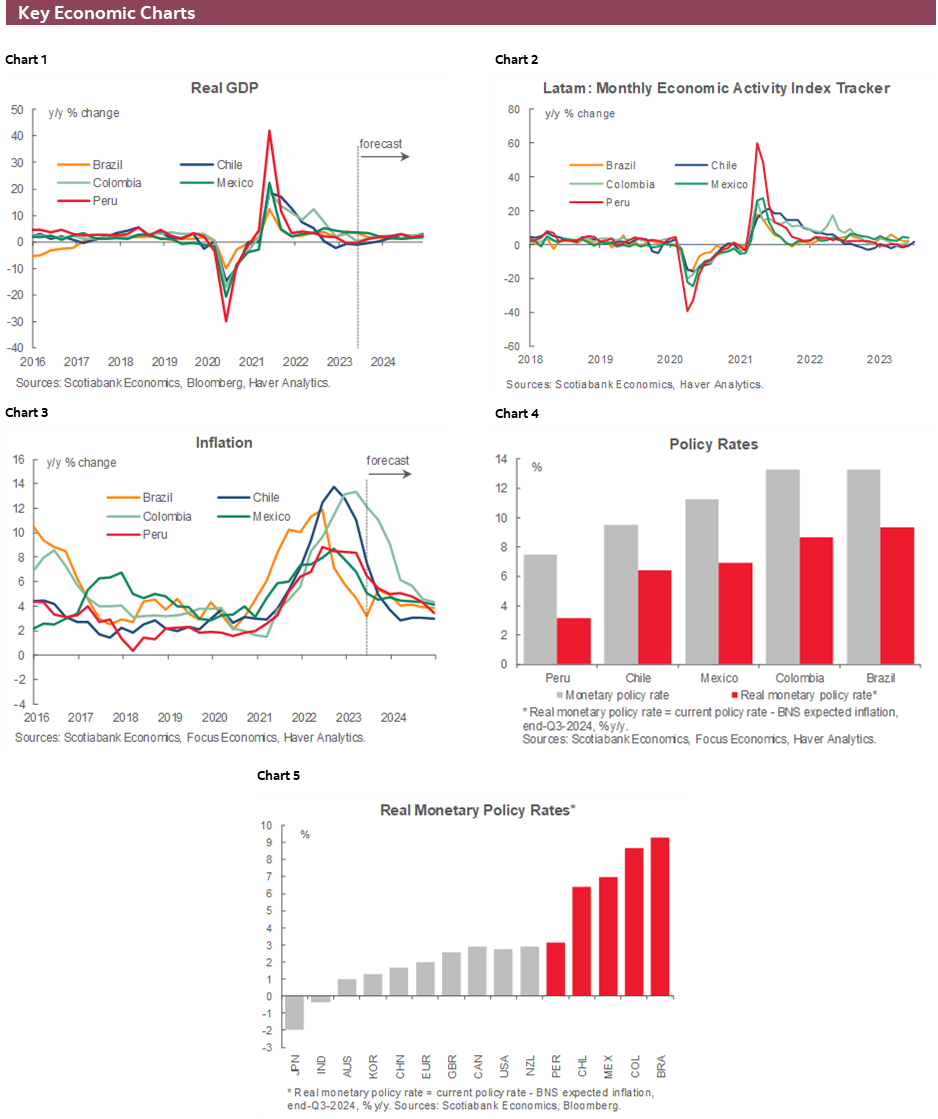

We have a schedule full of global monetary policy decisions next week, with policymakers from a dozen or so noteworthy central banks delivering a mix of rate holds, hikes, and cuts. Among them, the BCB will likely cut 50bps for the second consecutive meeting, the Fed looks set to hold at 5.50%, and the BoE is expected to hike 25bps to 5.50%. Officials in Japan, Switzerland, Norway, Paraguay, Philippines, Indonesia, Turkey, and South Africa will also decide on policy from now until Friday.

On Tuesday, the day before the BCB’s announcement, Brazilian economic activity figures for July are seen showing another moderate, but still acceptable, expansion of 2%+ y/y. Industry/sector level data released over the past few weeks showed a decline in industrial output (-1.1% y/y), strong services volumes growth (+3.5% y/y), and a decent gain in retail sales (+2.4% y/y) that would support this view of steady but slower growth.

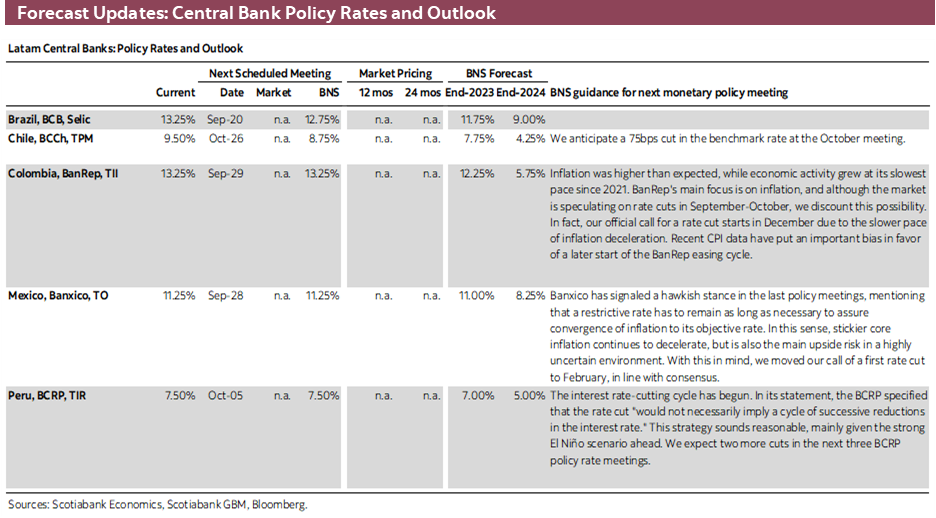

A slowing economy and a slight miss in August inflation data released on the 12th (with encouraging details on the services side of the basket) give the BCB room to cut by half a point again as rate-setters have broadly guided is the currently appropriate pace. The inflation data did act to pull year-end BCB pricing a touch lower (~3bps), suggesting some speculation that at one of the remaining three meetings of 2023 we may see a 75bps reduction.

Colombian and Mexican statistics agencies will also publish July economic activity readings next week, on Monday and Friday, respectively. Our team in Colombia projects a soft 1.3% y/y expansion in July, reflecting economic weakness centred on demand for goods while nonfinancial services hold up a bit better—though the overall pace is far from stellar. BanRep is still facing double-digit inflation in headline and core, however, and some prices (like those of food) remain under pressure, so there is no appetite to cut yet despite the economic slowdown.

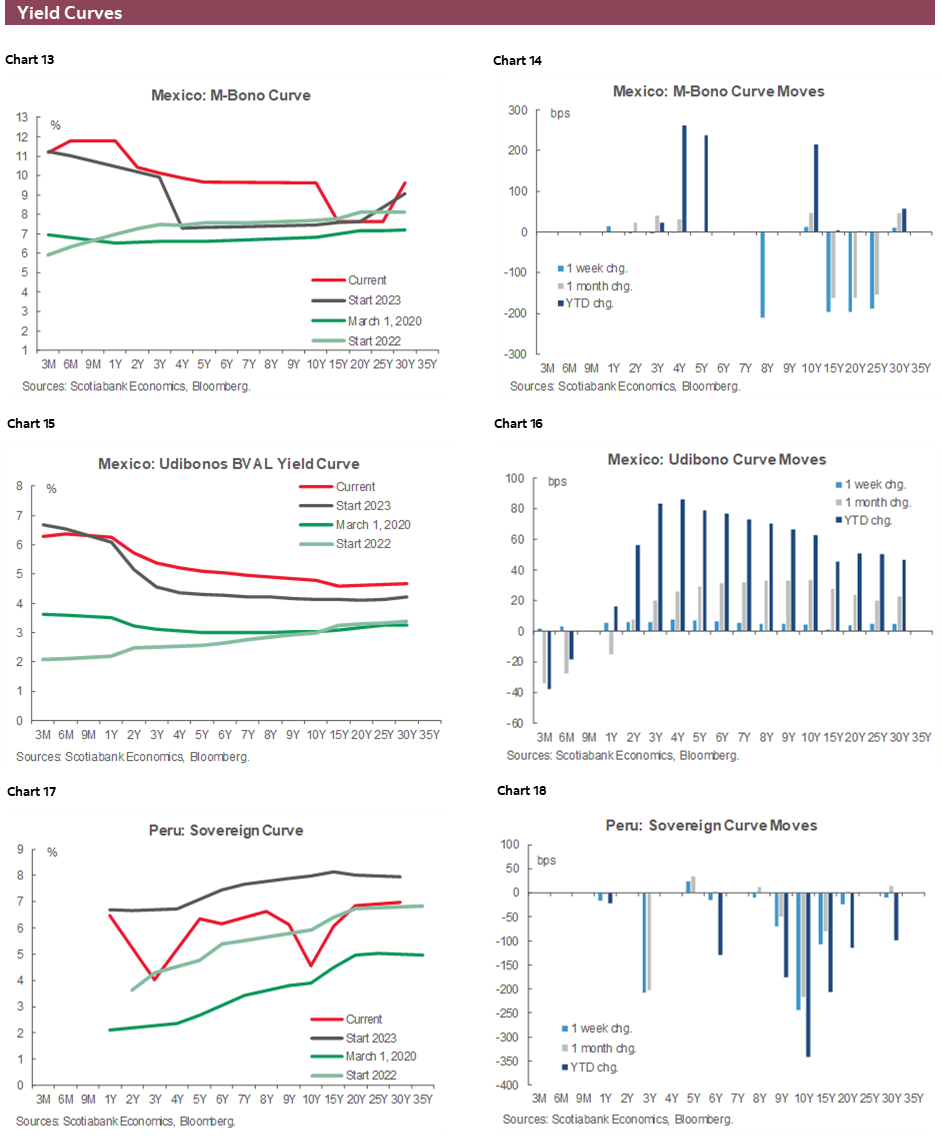

As for Mexico’s IGAE, INEGI’s early estimates of economic activity point to a slight deceleration for the month from 4.1% to the high 3’s in data due Friday. That’s not too much cause for worry considering this is still quite a high pace of growth, seemingly impervious to highly restrictive monetary policy—and the US economy keeps on trucking on. So, as far as Banxico is concerned, economic activity data are far from screaming ‘cut’, and we don’t expect economists surveyed by Citbanamex to feel otherwise in results of the poll out on Wednesday. Retail sales data out the previous day will inform expectations for Friday’s reading.

H1-Sep inflation is due for release at the same time as the IGAE. Bi-weekly core inflation finally fell below 6% y/y in the H2-Aug release, for the first time since late-2021, edging below the low-6’s forecast that the median had pencilled in. On a sequential comparison, the 0.08% increase in core prices of H2-Aug was the smallest since a November 2021 decline (due to Mexico’s ‘Black Friday’ sales) and one has to go back to late-2020 for the next smallest move. Overall, the trend in core inflation on a period-over-period basis is certainly a positive development for Banxico, but it cannot get comfortable considering the aforementioned economic strength. Next week’s data should show a 5.7/8% y/y core reading, while headline inflation should remain around the mid-4s.

The fiscal backdrop is also a point of concern for Banxico as the government’s recently published 2024 economic package foresees additional spending and support for households that would fuel a longer wait to reach the 2-4% inflation goal. In today’s weekly, the team looks at the difficulties that the Mexican government will face in trying to rein in the wider deficit that they project for 2024 to slightly less than half of that in 2025, as they intend.

There’s not a lot that catches the eye in Chile’s and Peru’s calendars next week. In fact, there’s nothing of note in Peru next week, but in today’s Weekly, our economists discuss the trouble that an uncertain El Nino has caused for forecasts of growth and inflation; agricultural weakness, in particular, shows up as GDP negative and prices positive. It’s already tough to forecast economics, it’s even tougher to forecast economics sensitive to weather, increasing the margin of error for projections and monetary policy decisions. The BCRP nevertheless thought it was appropriate to lower rates at its September decision (see Latam Daily). It’s a short week in Chile, with markets closed on Monday and Tuesday for Independence holidays, and the only items worth watching will be August PPI and the BCCh’s September meeting minutes (where a 75bps cut was rolled out) , both out on Friday morning.

PACIFIC ALLIANCE COUNTRY UPDATES

Mexico—Reining in Deficit Could be A Tough Challenge After 2024

Eduardo Suárez, VP, Latin America Economics

+52.55.9179.5174 (Mexico)

esuarezm@scotiabank.com.mx

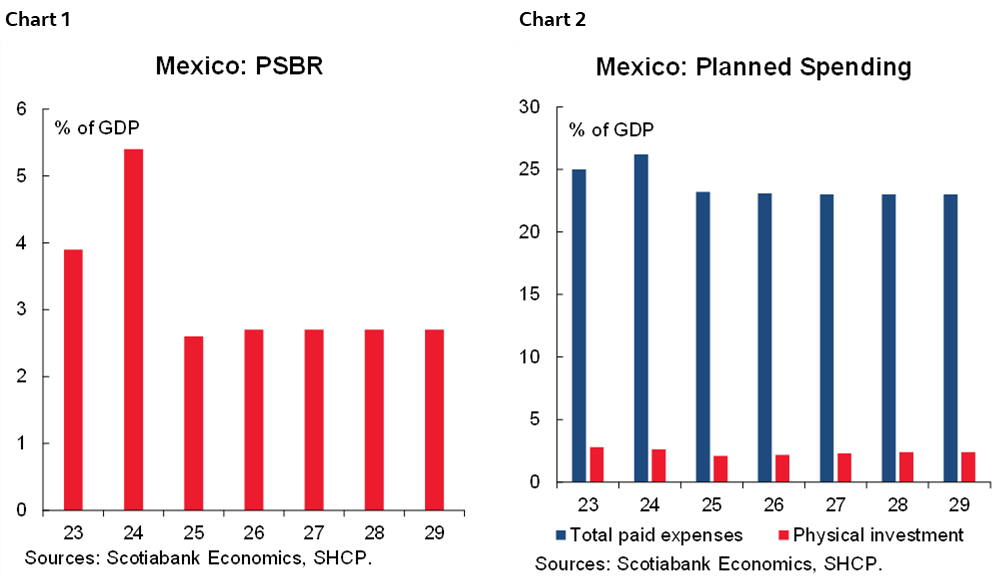

One of the most challenging elements we see in the Economic Package for 2024 is the dynamics of public sector borrowing requirements (the PSBR). The Economic Package envisions a sharp rise in borrowing requirements to 5.4% of GDP (as has been widely discussed, the widest deficit since 1988), and a drop to slightly less than half that amount by 2025 (at which time a new administration should be sitting in the National Palace).

The first challenge with that expected deficit reduction is that we don’t know what the plan for the next administration will be, and even if the new government plans to restore fiscal discipline it will be a tall order to reduce the deficit this much without an ambitious tax reform that would need to increase tax revenues by 2.5 percentage points of GDP.

One of the reasons why believe fiscal healing will likely require a solution on the tax revenues side is that the increase in spending is not a crisis response package where the government is giving one-off transfers to deal with a shock that subsequently expires (and the fiscal backdrop automatically stabilizes). It’s also not a temporary increase in investment that expires when the projects end (as charts 1 and 2 show, planned physical investment is falling). Hence, the larger deficit will likely be very challenging to solve on the spending side.

In addition, if we think about this from a (G–I) perspective, a methodology for estimating long term fiscal sustainability by looking at the trajectory of debt service vs the trajectory of revenues, and estimating the necessary primary surplus necessary to stabilize debt, the world is becoming more challenging for fiscal adjusters. In particular, the growth rate of debt payments is determined by the weighted average of interest rates of public debt. Given that US Treasuries are likely to average about 200bps higher than they did in the 2010–2020 period, the “I” (the growth rate of debt payments), is likely to be at least that much higher for much of the rest of the world. This should also make the fiscal adjustment back to a sub-3% of GDP PSBR challenging.

Peru—El Niño Tantrums Are Wreaking Havoc on Forecasts and Expectations

Guillermo Arbe, Head Economist, Peru

+51.1.211.6052 (Peru)

guillermo.arbe@scotiabank.com.pe

We’re all bracing for it… the tantrums of a two-year El Niño event. Much of the impact of the severe weather has already been felt in 2023. El Niño was the main reason why growth was negative (-0.5% y/y) in Q2-2023. It is also beginning to weigh more heavily on domestic agricultural prices and, therefore, on inflation.

Although the return of Lima’s characteristic winter drab gray skies and humid drizzle this week has finally interrupted the unseasonal sunny skies and warmth seen this winter, providing some hope of a weaker El Niño in 2024, the official forecasts do not seem to validate this, and continue to point to a moderate/strong second round El Niño in 2024.

As El Niño is a two-year event, much of the impact has already been felt. It is mainly because of El Niño that we recently lowered our GDP growth forecasts for 2023 from 1.4% to 0.5%. We are maintaining our GDP forecast at 2.3% for 2024, but note that this is off a much lower base and, thus, represents a lower real GDP level than we expected before. Perhaps the best way to view forecasts given that El Niño is a two-year event is to consider that, without El Niño the country might have been growing about 2.5% per annum, or just over 5.0% for the two year 2023–2024 period. Instead we expect the cumulative growth over the two years to be under 3.0%. Thus, El Niño would be reducing growth by at least two full percentage points over the two-year period.

El Niño, and severe weather in general, had a much greater impact on the economy, especially on agriculture and fishing, in Q2 than we had expected, and initial data suggest that this will be true for Q3 as well. At the time of this writing, the official figure for July GDP growth has not been released, but early partial data suggest a very weak number. The issue is that El Niño’s hand was once again evident in fishing, down 48%, and agriculture, which fell 0.7% y/y.

August GDP will be telling. Fishing GDP growth will actually be strong, but this will be nonconsequential, as 1. August is not a main fishing month (thus both weight and base comparisons are low) and 2. The only reason for strong fishing growth in August is that monitored fishing took place to test conditions for future reference.

Outside of fishing, there will be three sectors to keep a keen eye on, namely, agriculture, construction and industrial manufacturing. All three sectors fell strongly in the first half of 2023 (agriculture -4.6%; construction -9.0% and industrial manufacturing -7.7%).

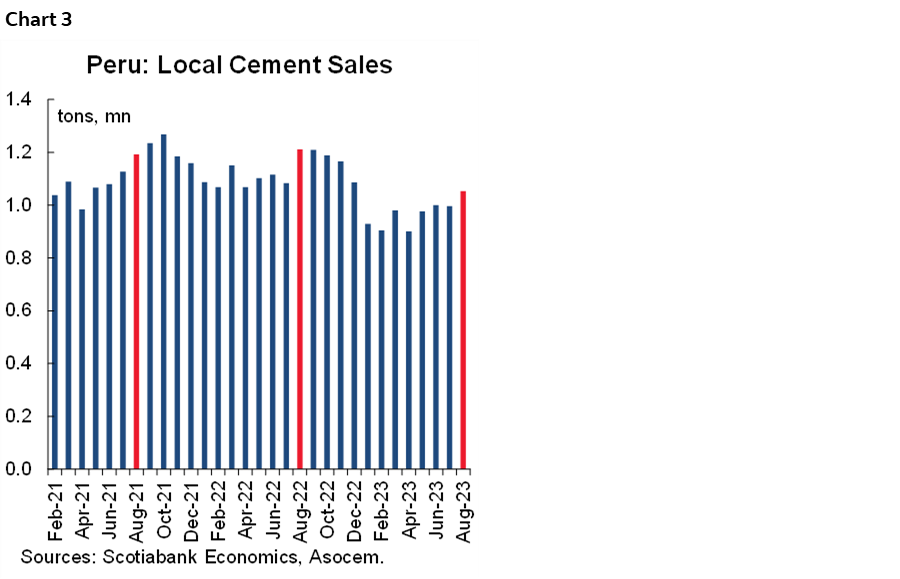

We can get a bit of a preview of construction for July and August by looking at cement demand figures, which have already been released. The glass is more half empty than half full. Although cement sales have increased month-over-month since May, they are broadly still materially below 2022 and 2021 levels (chart 3). Thus, y/y growth figures are quite disappointing. We can only hope that the magnitude of the y/y decline will decrease after August, as there appears to be a bit of a revival in both residential and infrastructure construction.

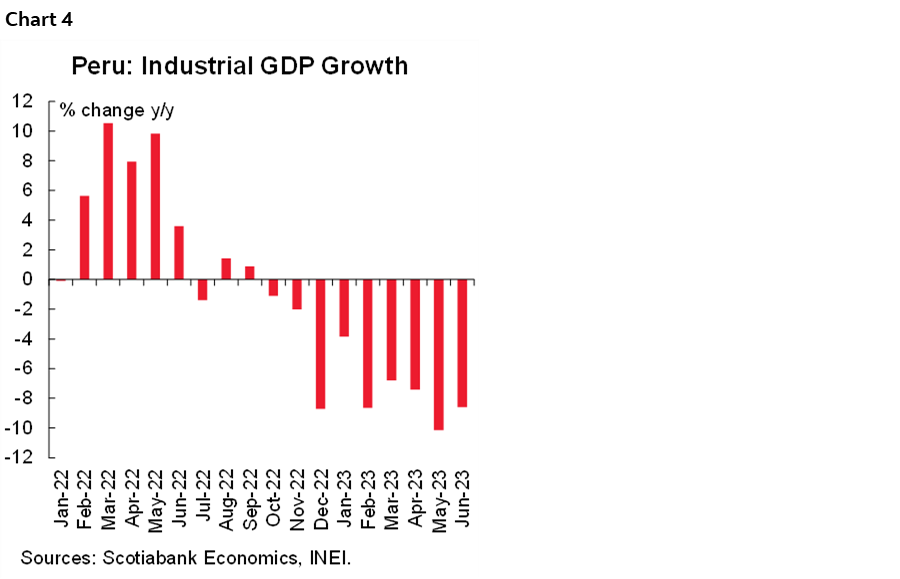

The speed of decline for industrial manufacturing is not slowing, however, which registered very high negative growth rates in April to June. In the case of industrial manufacturing, it is not clear to what extent the sector is feeling an indirect impact from El Niño and to what extent something more structural is at play. We’re not very hopeful for the sector’s growth in July, but hopefully August will be more revealing as to whether we are nearing a point of inflection in the downtrend (chart 4).

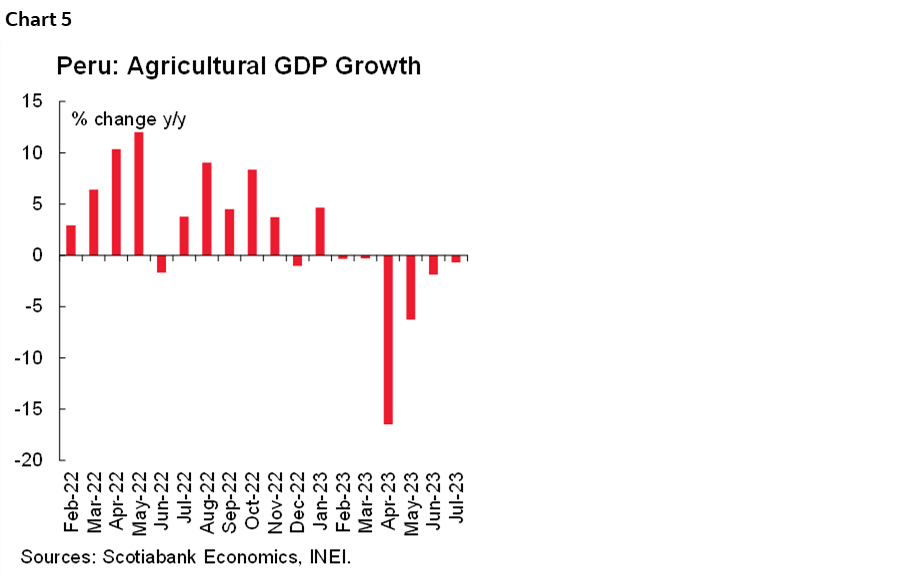

Agriculture is the third key sector to monitor. Whereas negative construction and industrial manufacturing growth are indicative of low domestic demand and, therefore, are at least helpful in deterring inflation, negative agriculture growth is a supply restraint and harmful for inflation. Agriculture GDP growth has been negative for six consecutive months, from February to July (chart 5). The main factor is the weather and its impact on productivity. This could easily continue for the next three quarters, although starting in early 2024 growth will be assisted by a low base due to the impact of El Niño in 2023. But the same will not be true for production levels going forward, which will continue to be battered by a second-round El Niño event.

Agriculture production is key not only for what it means for GDP growth, but also for inflation and monetary policy. The BCRP is certainly wary of the impact of El Niño on inflation, and is likely to pace its reference rate decisions more carefully than otherwise. It is true that agriculture prices will impact headline inflation directly, but not core inflation, and that low domestic demand will provide pressure to the down on core inflation, but it is also apparent that the BCRP is more sensitive to inflation expectations than to core inflation. Inflation expectations tend to be aligned more with headline inflation than with core inflation. Thus, agricultural prices are likely to be a factor affecting monetary policy.

The bottom line is that the El Niño has degrees of uncertainty attached to it which increase the margin of error for growth, inflation and monetary policy.

| LOCAL MARKET COVERAGE | |

| CHILE | |

| Website: | Click here to be redirected |

| Subscribe: | anibal.alarcon@scotiabank.cl |

| Coverage: | Spanish and English |

| COLOMBIA | |

| Website: | Click here to be redirected |

| Subscribe: | jackeline.pirajan@scotiabankcolptria.com |

| Coverage: | Spanish and English |

| MEXICO | |

| Website: | Click here to be redirected |

| Subscribe: | estudeco@scotiacb.com.mx |

| Coverage: | Spanish |

| PERU | |

| Website: | Click here to be redirected |

| Subscribe: | siee@scotiabank.com.pe |

| Coverage: | Spanish |

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.