- Peru: No more doubts, BCRP begins rate cuts cycle

A beat in Chinese retail sales/industrial production data and a large PBoC cash injection had Asia markets trading with a positive mood before European hours brought a selloff in rates markets that also chipped away at overnight progress in US equity futures. After the China-led jump, SPX futures have fallen to sit roughly unchanged, while crude oil follows a similar path but is still holding on to a 0.3% increase after trading above $91/bbl in WTI. Iron ore is up 2% and copper is down 0.3%. USTs and EGBs are bear steepening. US industrial production and U Mich inflation expectations are the G10 highlight today.

The USD is sitting mixed to weaker, flat against the MXN, and on track for its first weekly drop on a BBDXY basis since mid-July (tracking down 0.5%) due to the stronger CNY and high-beta currencies over the week—well offsetting EUR and GBP losses. The MXN, with a 2.8% gain, is the best performing major currency this week, reversing a decent share of its losses on Banxico’s late-August announcement that it would scale back its currency hedge program.

Colombian and Brazilian retail sales and Peruvian GDP data are the main releases to watch today in Latam. While in Brazil, retail volumes are expected to rise 2% y/y , the median economist estimates that Colombian retail sales contracted steeply, again, by 7.8% y/y after a 11.9% drop in June (our Bogota team projects an 8.5% decline). The weak retail data may see some emboldened in their view that BanRep could cut rates in October, or even September, but we think a December cut is more likely. On that note, the results of BanRep’s economists survey are also due today.

Peruvian GDP figures for July are expected to show no growth, which sounds terrible but is at least an improvement from the 0.6% y/y negative reading and in comparison to the four out of six months of year-on-year declines in monthly data for H1-2023. Wherever it comes in (we are forecasting a small expansion of 0.3% y/y), it can only materially chip away at weakness in the first half of the year (-0.4% and –0.5% y/y in Q1 and Q2, respectively) that, in combination with expectations of a harsher El Niño, has led us to revise our 2023 GDP growth forecast to 0.5% (see Latam Daily). At 11ET, we hear from BCRP head Velarde who will likely expand on yesterday’s rate cut (see below), at the same time as the release of unemployment data for August.

—Juan Manuel Herrera

PERU: NO MORE DOUBTS, BCRP BEGINS RATE CUTS CYCLE

The board of Peru’s Central Bank (BCRP) provided a key signal by deciding to cut its reference interest rate this Thursday by 25bps, to 7.50%. The interest rate cutting cycle has begun. There was strong no conviction going into the decision, but it is not surprising. The Bloomberg survey, with the majority of participation being foreign banks and analysts, pointed to a cut of 25bps. However, in surveys of locals, the possibility of not making changes predominated.

The technical conditions for an interest rate cut were in place. The doubt came from the weight of the precautionary criterion in the decision, given the increasing probability of a strong El Niño scenario. In its statement, the BCRP specified that the rate cut “would not necessarily imply a cycle of successive reductions in the interest rate.” We discussed this strategy in a previous report (see Latam Daily) because at least in the two previous episodes of rate cuts, the BCRP has opted for staggered cuts, combined with months of pauses. In the face of the uncertainty associated with the impacts of El Niño, it makes sense to use this strategy as in the past. Inflation has remained outside the target range for 27 months, a record period. Expectations for 3 month sales prices increased in August, for the second consecutive month, remaining in “bullish” territory, according to a BCRP survey.

The BCRP expressed concern by noting that the transitory effects on inflation have begun to dissipate in only some foods since June, and a general reversal has not been observed. Along these lines, it reiterated that there are risks associated with weather factors (El Niño). However, it also reiterated its view that inflation will reach the target range (between 1% and 3%) at the beginning of next year.

The statement also provided three dovish signals. The first by emphasizing that the headline and core trend inflation both have been decreasing since the beginning of 2023. The second, highlighting that 12 month inflation expectations—which decreased from 3.6% to 3.4%—are approaching the range goal (between 1% and 3%). Additionally, 24 month inflation expectations decreased from 2.8% to 2.7%, within the target range for the third consecutive month. The third, cutting the rate for overnight deposits by 50bps, from 5.25% to 4.75%.

The beginning of the rate cuts cycle also occurs in a context in which the BCRP remained concerned about economic weakness, reiterating that "the shocks derived from social unrest and the El Niño have had a greater impact than expected in economic activity and domestic demand". In August, the MoF reduced its economic growth forecast for this year from 1.5% to 1.1%, and the market consensus reduced it from 1.3% to 1.0% according to the latest BCRP survey. We expect a similar change in the BCRP macroeconomic forecast released today. In its view of the international economy, the BCRP highlighted lower economic growth in China.

Our monitoring of key prices suggests that the inflation trend would continue to decline in September, although at a slow pace, between 5.5% and 5.4%. So far in September there has been an increase in the average prices of perishable foods, offset by lower prices for poultry. We expect a similar decrease for core inflation, which would go from 3.8% to 3.7% in September. Our inflation forecast of 5.00% for the 2023-end is biased downward based on available data, but we maintain our forecast due to the increased probability of a strong El Niño scenario in the coming months.

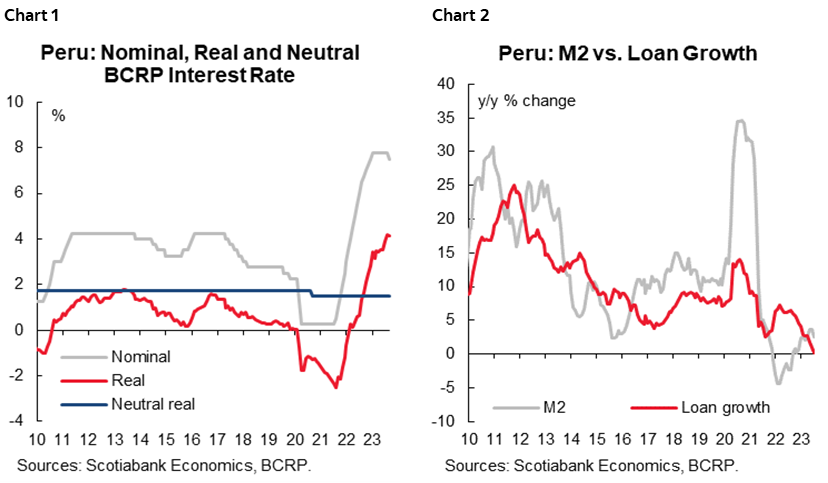

By cutting its policy rate to 7.50%, the real interest rate fell from 4.2% to 4.1% (chart 1), practically maintaining the monetary policy stance, and still well above the neutral level (1.50%), accumulating 13 months in contractionary territory. We believe that from now on BCRP decisions will be more data dependent than ever. The policy stance became more dovish by adding that, if necessary, it will consider “additional” modifications to monetary policy. Our key rate forecast of 7.00% for the year end includes the possibility of a pause down the road. For 2024 we maintain 200bps in rate cuts, taking the policy rate to 5.00%, assigning an upward bias, depending on the intensity and persistence of El Niño on inflation and its expectations. Financial conditions remain tight, characterized by weak credit expansion, which went from 1.0% y/y in June to 0.2% in July, the lowest performance in 19 years, in line with the weakness of the economy and the contractionary stance of monetary policy. The growth of liquidity in soles (M2, chart 2) slowed, from 3.7% in June to 2.6% in August, but remains in expansionary territory for 11 consecutive months.

—Mario Guerrero

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.