- Peru: Persistent inflationary pressures lead us to revise our forecasts for key financial variables

PRICE STABILITY INTERRUPTED

We are making significant changes to our 2021–2022 outlook for inflation, the BCRP’s policy interest rate, and our exchange rate forecasts. We are raising our inflation forecast from 3.5% to 6.5% y/y for 2021, and from 3.2% to 4.5% y/y for 2022. In response to higher inflation, we now expect the BCRP to raise its reference rate from 0.50% currently to 1.25% by year-end 2021, and to 2.50 by year-end 2022. We see upside risk to our reference rate forecast. Given persistent political turbulence, and in view that the USDPEN continues to ignore external account fundamentals, we are raising our FX forecast from 3.65 to 4.15 for 2021, and from 3.60 to 4.25 for 2022. We note, however, that uncertainty is high, not only in terms of magnitude of change, but also in terms of direction, and with so many strong countervailing forces in play the risk is on the downside (PEN appreciation).

Inflationary pressures are proving stronger and more persistent than anticipated. In addition to the global pandemic, domestic uncertainty is spurring volatility, with the risk of an incipient feedback loop between inflation and PEN depreciation. The BCRP needs to disrupt this loop quickly, which is why we expect it to be much more aggressive in monetary policy, despite an economy that is still trying to get back on its feet after the 2020 COVID-19 lockdown.

INFLATION

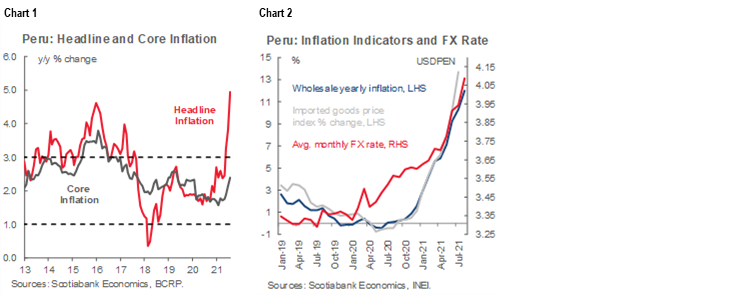

We are raising our inflation forecast to 6.5% for 2021, from 3.5%, and to 4.5% for 2022, from 3.0%. These are hefty changes. The reality of inflation has changed swiftly in the country. Inflation, which ended 2020 at 2.0%, is now trending, in August, at nearly 5%, and rising (chart 1). It’s true that core inflation is at a much more modest 2.6%, yearly, up from 1.7% only four months ago. More significantly, the pass-through from higher import prices (especially energy, and soft commodities such as wheat and maize), higher freight, containers and other transportation costs, and a rising FX rate, has still to be felt fully (chart 2). Wholesale price inflation is soaring at 12% yearly. (A year ago, wholesale inflation was 0.1%, and in April it was still under 6%.) This will be putting pressure on head-line inflation for some time to come, and it will likely take some time before the BCRP’s tighter monetary policy gets inflation back within the bounds of its’ target range. More so, considering that much of inflation reflects global cost factors outside the BCRP’s control.

MONETARY POLICY

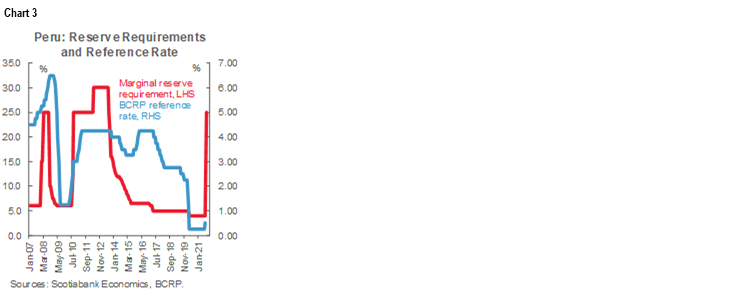

We have brought forward the BCRP tightening schedule. We now see the BCRP raising the reference rate to 1.25% in 2021 (our previous forecast was 0.50%), and to 2.5% in 2022, from 1.0% previously. The BCRP has done more than just signal that this is the intention. In August, the BCRP raised its reference rate from 0.25% to 0.50%. Equally significantly, the BCRP raised the marginal reserve requirement that banks must deliver on PEN deposits (chart 3). Whereas before banks had to withhold PEN 5 out of each PEN 100 in new deposits it received for purposes of meeting BCRP reserve requirements, it will now have to reserve PEN 25 out of each PEN 100 received. This is a huge increase, although not without precedent. The BCRP did something similar in 2010. Note that this occurred at the same time that it raised its reference rate by 300 bps, from 1.25% to 4.25%, over the course of a year. The context is different now, what with the risk of a third wave of COVID-19 looming, and an economy still trying to catch up with 2019 levels. The question is, giving current circumstances, just how quickly the BCRP will move. On the one hand, the BCRP surely recognizes the need to control price instability as soon as possible. On the other, with core inflation still within the target range, at 2.6%, and inflation expectations at a still mild 3.07%, up very little from 3.03% in July, and with the surge in the FX rate having abated somewhat, the case could be made within the BCRP that there is no need to be overly aggressive. We shall know whether that will be the case on not on Thursday, depending on whether the BCRP increases the policy rate by 25 bps or by more.

THE FX RATE

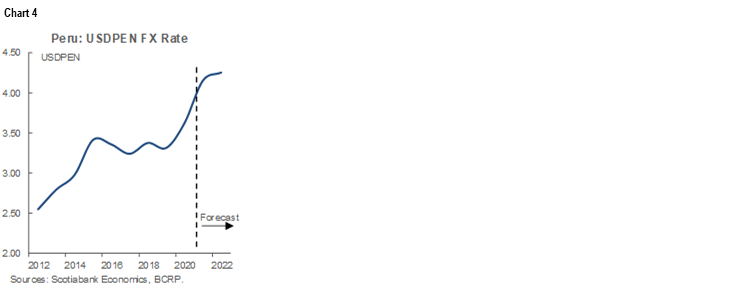

Our new USDPEN forecasts are 4.15 for year-end 2021, and 4.25 for 2022 (chart 4). We had delayed changing our forecasts, as they are out of line with external account fundamentals. Terms of trade are at their best level since 2012. The trade balance is on its way to an all-time high of USD 13.8 bn this year, and then on to USD 16 bn in 2022, according to our estimates. Given this background, the PEN should be strengthening. And yet, it’s not. With inflation rising, and political uncertainty high, both local businesses and households are taking refuge in the USD. There has been a record outflow of nearly USD 10 bn of business and household short-term capital in the first half of 2021, mostly in the second quarter. We understand that this outflow has slowed since, but has not been stemmed. Note, also, that much of the PEN 30 bn from private pension fund withdrawals which Congress has awarded, have yet to be delivered, and typically part of this will flow into USD demand. But, then, on the other hand, and to add to the conflicting factors bearing on the FX market, the withdrawal of monetary stimulus by the BCRP should give support to the PEN. Considering the complexity and degrees of uncertainty of the factors involved, the PEN FX market has become very hard to forecast. Our forecast is somewhat of a compromise: the weakening trend continues, but at a slower pace than in the past. Unlike inflation and the reference rate, the risk here is to the downside (PEN appreciation).

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.