Extended pandemic-related spending programs and a weaker-than-budgeted growth outlook together imply larger financing needs for Colombia’s authorities in 2020 and 2021.

We expect Colombia’s authorities to focus on meeting these needs through the substitution of local-market COP-denominated COLTES issuance for foreign FX financing and liability-management operations to reduce immediate debt-service obligations.

As a result, we expect projected fiscal deficits to remain unchanged and we do not see further pressure on the 2020 and 2021 budgets.

A SMALL NOTE ON RECENT FISCAL DEBT MANAGEMENT ANNOUNCEMENTS

Over the course of the last seven months since the pandemic-induced lockdown started, the Ministry of Finance (MoF) has made some announcements of program extensions (see here and here) that have implications for its financing strategy. Some assumptions made in the June Medium Term Fiscal Framework (MTFF) have started to change; the most important shift is that Colombia is now set to continue having extraordinary fiscal expenditures related to the health emergency into 2021.

Additionally, fiscal income and fiscal sustainability challenges are increasing since economic growth is set to be slower than projected in June’s MTFF. While the government has not yet revised its forecast of a -5.5% y/y contraction in real GDP in 2020, we see the Colombian economy on track for a much deeper -7.5% y/y pullback this year (see our forecasts in the October 18 Latam Weekly). Therefore, the MoF has to be creative to find ways to do more countercyclical expenditure while at the same time maintaining consistency with its fiscal targets. For instance, swaps of public debt to reduce debt-service payments in 2020 and 2021 have been particularly popular over the last few months. Shifting issuance between external and domestic debt markets has also played a role in the government’s efforts to borrow as cheaply as possible while ensuring financial stability.

This short note takes stock of the current fiscal stance and clarifies the economic and financial implications of some key aspects of recent official announcements on swap operations and debt issuance. We use the cash flow “sources and uses” statement from the MTFF to analyze the short-run fiscal situation.

USES AND SOURCES: UPDATED SPENDING AND FINANCING FORECASTS

I. The uses: despite relatively low execution of the emergency fund, pandemic-related needs remain large

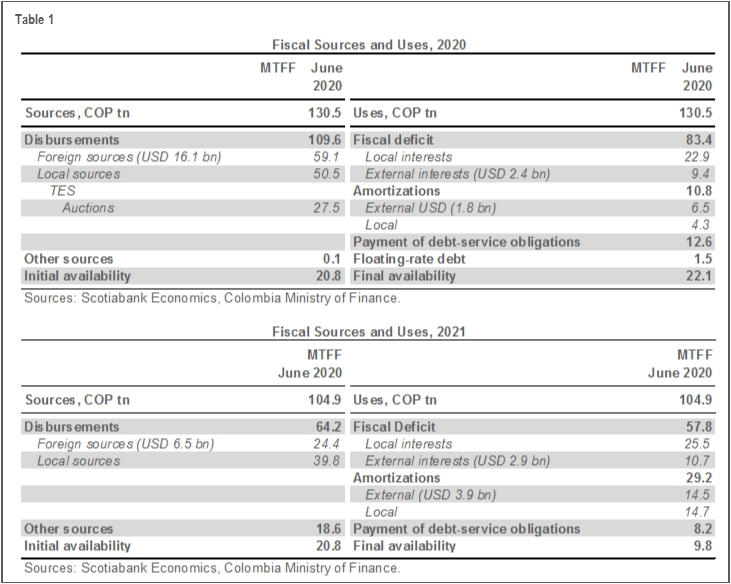

- Up to mid-October, execution of the government’s emergency fund stood at only about 44% of the fund’s total COP 29 tn (its initial COP 25 tn allocation was increased by COP 4 tn). This means that out of the COP 83.4 tn fiscal deficit for 2020 anticipated in the June MTFF (table 1), at least COP 16 tn of the deficit has not yet been realized. As of October 16, 2020, Treasury deposits at the central bank totalled around COP 33 tn, which implies that the MoF has a relatively comfortable liquidity position. However, budget execution typically accelerates in Q4 owing to some seasonality in payments and we expect the deficit to reach the COP 83.4 tn programmed under the MTFF, with full disbursement of the emergency fund before end-2020. Still, the government should close 2020 with a relatively strong liquidity position.

- The government is set to continue executing on emergency spending into 2021 as social programs were extended until the middle of next year, as noted above. Liquidity remaining at the end-2020 will be employed to support emergency spending in 2021.

II. The sources: additional COLTES auctions do not necessarily imply debt stocks would rise

- Under normal circumstances, Colombia’s Treasury prefers to split its annual financing 20% from external sources and 80% from domestic sources, although the share of outstanding external debt has been higher than 30% in recent years (chart 1). In 2020 and 2021, the authorities are likely to modify this balance, with a higher share of local issuance to keep reducing FX exposure.

- In the MTFF, projected external sources of funding for 2020 were established at USD 16.1 bn or COP 59.1 tn (table 1, again); however, as of October, only USD 3.8 bn in foreign bonds had been issued this year, while USD 1.3 bn in financing had been secured from multilateral institutions. If one adds USD 5.3 bn or about 30% of the augmented

USD 17.2 bn IMF Flexible Credit Line (FCL)—the portion of the augmented FCL that the Colombian authorities have indicated they would draw on for budget support—then total external sources sum up to around USD 10.4 bn, well below June’s MTFF target. So far, the MoF has shown no interest in issuing additional external debt or seeking alternate sources of external financing. - Regarding local sources, the COP 27.5 tn of COLTES issuance anticipated for 2020 in the MTFF is already complete; however, the MoF decided on October 5, 2020 to increase its COLTES auctions in 2020 by about COP 5 tn (0.49 % of GDP), which implies that issuance will be extended until the last week of November. Nevertheless, extra local issuance would not necessarily imply that debt levels should go higher than anticipated under the MTFF; likewise, additional local issuance would not automatically be employed to finance a fiscal deficit larger than the -8.2% of GDP currently envisaged by the government. Instead, more local issuance could simply be substituted for anticipated, but untapped, sources of external financing, which currently amount to around COP 19 tn in 2020. We think the MoF will continue to prefer domestic debt issuance to external financing as long as markets continue to show good appetite for COLTES since local financing lowers the country’s FX exposure. In fact, the recent issuance of a 30-year bond was almost entirely bought by offshore agents, which demonstrated the ongoing demand for COLTES despite the debt sustainability concerns recently stressed by Fitch.

- A note on the IMF arrangement. IMF resources are typically meant to boost FX reserves rather than finance government budgets, but recent augmentation in the FCL was specifically intended to meet extra COVID-19-related spending needs. At the time of the augmentation, the Colombian authorities indicated their intent to treat the balance of the approved USD 17.2 bn FCL as precautionary, meaning it would not be immediately drawn. As noted earlier, the MoF currently has a comfortable liquidity position, and it has the option to increase local COLTES issuance rather than tapping external sources for more financing.

DEBT SWAPS: LONGER DURATION AT LOWER COUPON RATES

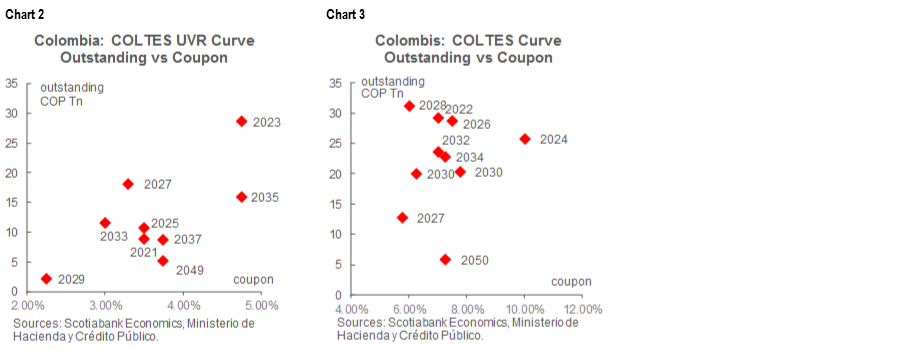

- So far in 2020, the MoF has made seven debt swaps: four with public entities, two with the BanRep (the central bank), and the most recent one last week through market makers. As a result of these swaps, the average maturity of local debt has been increased from 7.14 years to 8 years, while the average coupon has been reduced by 63 bps to 6.814%. The total outstanding stock of the inflation-linked COLTES UVR 2021 issue was reduced by COP 7.2 tn and replaced with expansions in the longer-tenor COLTES 27s, 32s and 34s, as well as in the inflation-linked COLTES UVR 27s, 29s, and 37s (charts 2 and 3). This opens some room for additional 2021 investment expenditures without, necessarily, increasing the fiscal deficit.

- Debt swaps are expected to continue in 2021 and reduce debt service next year by COP 4.7 tn or 0.5% GDP. Two out of the seven debt swaps noted above were made after the initial 2021 budget was presented to Congress in July; they reduced the stock of UVR 2021s outstanding by around COP 1.5 tn, 30% of the total amount needed to achieve the targeted reduction in 2021 debt service. This still leaves a long way to go, and the MoF is likely also to consider additional maturity-extending swaps with its Global and Yankee bonds, which have outstanding stocks of USD 2.5 bn and USD 1.5 bn, respectively.

MAIN TAKEAWAYS: WHAT’S AHEAD

- For now, we don’t see significant pressures on either 2020 or 2021 budget execution, which should mitigate the extent to which Colombia’s authorities will need to tap foreign sources of financing.

- In any event, Colombia’s Treasury is likely to favour local sources of financing so long as COLTES markets remain well supported, which we expect to be the case. Compared with the MTFF, we project the government’s debt composition to shift from 38% in external debt in October 2020 (chart 1, again) to around 35% over time.

- Maturity-extending debt swaps are expected to continue, with a focus on retiring short-term domestic issues with relatively high coupons (e.g., COLTES 2022, COLTES 2024, UVR 2021, UVR 2023) and replacing them with longer-term paper in existing series with lower coupons (e.g., COLTES 2027, UVR 2033, UVR 2037) to ease immediate debt-service requirements. On the external side, debt payments are particularly high on the Global 2021s and Yankee 2021s and these also could be the target of liability-management operations in the coming months.

—Sergio Olarte & Jackeline Piraján

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including, Scotiabanc Inc.; Citadel Hill Advisors L.L.C.; The Bank of Nova Scotia Trust Company of New York; Scotiabank Europe plc; Scotiabank (Ireland) Limited; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Scotia Inverlat Casa de Bolsa S.A. de C.V., Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorised by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorised by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V., and Scotia Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.