In Sunday’s nationwide plebiscite, Chile’s citizens approved by wide margins a re-write of the country’s 1980 constitution through a popularly-elected assembly.

Still, a range of outstanding issues remain to be determined and ratification of a new constitution in a mandatory vote planned for early 2022 is by no means guaranteed.

We do not see the constitutional process that lies ahead as a threat to central bank independence, fiscal responsibility, or the pension system.

SUPPORT FOR REWRITING CONSTITUTION EXCEEDED POLLS

In the plebiscite held on Sunday, October 25, to decide whether to maintain or replace the current constitution, the ‘Approve’ option—to replace the current constitution—obtained 78.3% of the votes, against 21.7% for the ‘Reject’ option. In a peaceful day, 7.5 million citizens went to the polls to vote— the highest number of voters since the return to democracy in 1990—which meant a turnout of 50.9% of eligible voters. On the second question regarding the body that should draft the new constitution, the winning option was the Constitutional Convention/Assembly—i.e., 100% of the members elected through popular vote—with 79% of the votes cast, compared to the Mixed Convention option—50% of members elected by popular vote, 50% of members drawn from Congress—which obtained 21% of the votes.

The high turnout—the highest rate since 2012 when voting became voluntary—occurred in the midst of the pandemic and some suspensions of constitutional rights, including the imposition of curfews. Although the turnout increased compared to recent elections, it was still far from the OECD average, which stands at around 60%.

Support for rewriting the 1980 constitution exceeded expectations based on polls that anticipated a majority closer to 60–70%, with softer support expected for the Constitutional Convention option over the Mixed Assembly.

OUR KEY TAKEAWAYS

The relatively high participation rate at 50.9% was a pleasant surprise. Preliminarily, it appears that there was strong turnout amongst first-time voters, which implies that young people’s interest in politics has increased. However, the overwhelming victory for the Constitutional Assembly versus the Mixed Assembly delivered a message of rejection to Congress and the political class.

Differences in perceptions of inequality stand out. In broad terms, municipalities with the highest concentrations of relatively wealthy citizens tended to vote against constitutional change. Furthermore, the gaps between these municipalities and the national average were greater than those observed in the 1988 plebiscite on the transition from military rule. This would imply that although the results of the 2020 plebiscite indicate a large majority in support of constitutional change which opens doors for political agreements, it may not be easy to reach consensus on a new constitution since there are some social and political groups that maintain less flexible political positions.

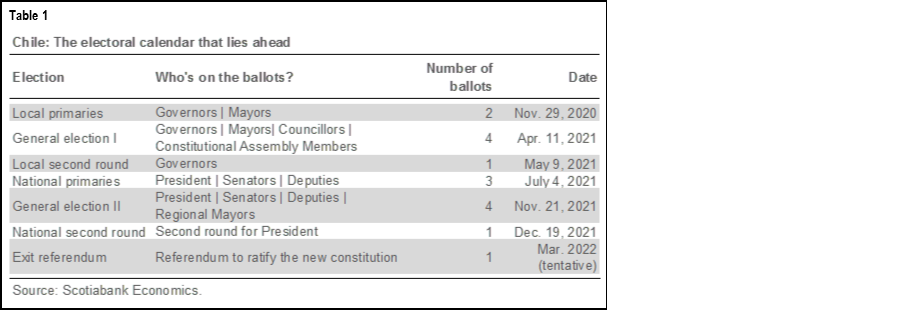

Again on citizen participation, although it was higher than that observed during the last eight elections, it seems to us that it was not high enough to ensure success in the exit plebiscite that will take place in 2022 to ratify a new constitution (table 1). Indeed, given that the exit plebiscite will require a mandatory vote, we could see that many people who did not vote yesterday could reject a proposed new constitution in two years’ time. This will depend crucially on how the constitutional process is conducted and the modifications that are proposed in the re-draft.

The streets should be dramatically calmer after this result, although some small groups of protesters may continue to raise proposals for the constituent process in public demonstrations.

Regarding the constitutional process, it will be important for the authorities to inform the population about the possible reach of a new constitution—that is, what can be done and what cannot—and to provide a reasonable roadmap and timeline for potential modifications. Setting realistic expectations about the process will be crucial to maintain the peace and avoid a resurgence of violent protests.

Among the 78% who chose to reform the constitution and the 79% who voted to do it through a 100% elected convention, a wide diversity of views and groups are represented. This indicates that the election of members to the Constitutional Assembly on April 11, 2021 will be critical in determining whether there is likely to be a set of coalitions that would allow the Convention to reach the two-thirds majority required to approve a new constitutional draft and send it to voters for review in a mandatory plebiscite in early-2022 (table 1, again). If the draft receives more than 50% of votes in the 2022 popular plebiscite, it would become Chile’s new constitution; if not, the 1980 constitution would remain valid.

There are still some outstanding issues to be clarified in the coming weeks on the process for electing members of the Constitutional Assembly. One of the main points concerns the approval of seats reserved for Indigenous peoples. There is still no agreement on whether these seats would be within the 155 already specified for the Constitutional Assembly or whether additional seats would be added.

PERSPECTIVE FOR MARKETS

Market reactions have so far been rather limited. However, political uncertainty could remain elevated for a prolonged period, which would counteract the appreciating effects on the peso of strong copper prices, solid terms of trade, and the ongoing recovery in the economy. Still, we maintain our view that the CLP is set to appreciate mildly over the coming quarters. With respect to interest rates, we think the implications of the vote are likely to be minor. Although political uncertainty could add some risk premium, we continue to see a possibility that the central bank will consider adding additional stimulus at the BCCh Board’s next monetary policy meeting on December 7.

Could the independence of the central bank be put into question? This issue may be discussed, but no leftist politician has expressed interest in changing the independence or autonomy of the central bank. There has been some interest in adjusting the organic law (i.e., foundational statutes) of the BCCh from strict inflation targeting toward a Fed-style dual mandate focused on both inflation and employment. There is also some interest in creating a constitutional process by which BCCh Board members could be reviewed and dismissed, though this power is already to a large extent implicit in the current organic law of the central bank. Hence, we do not foresee relevant risks of material changes in the fabric of the central bank that could affect the BCCh’s success in controlling inflation.

Is fiscal responsibility likely to be loosened? This will depend on how strongly certain social rights are guaranteed in a new draft constitution. Indeed, we could see relevant fiscal pressure coming from adjustments in the coverage of the public health and pension systems. However, we must also consider that pressure to modify the Fiscal Rule—from the OECD and the Autonomous Fiscal Council—has increased in recent times. This could result in changes that would manage to contain excessively high levels of indebtedness and, thus, prevent an increase in spending greater than that which could be financed with taxes. Along the same lines, the government is already working on a new tax reform to promote fiscal sustainability. Overall, although we see important fiscal pressures, we also detect some relevant mitigating factors.

Is the structure of the pension system under risk? The pension system could be modified, but this would proceed on a path parallel to any constitutional changes. In effect, Chile is already close to an agreement to modify the pension system to provide for an increase in contributions by account holders (i.e., up 6 ppts) and other changes. If broad political agreement on such reforms is reached prior to April 2021, it is unlikely that the system would be altered further (e.g., from an individually-funded system to a pay-as-you-go format) at a later date in the constitutional process.

—Jorge Selaive, Carlos Muñoz, & Waldo Riveras

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including, Scotiabanc Inc.; Citadel Hill Advisors L.L.C.; The Bank of Nova Scotia Trust Company of New York; Scotiabank Europe plc; Scotiabank (Ireland) Limited; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Scotia Inverlat Casa de Bolsa S.A. de C.V., Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorised by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorised by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V., and Scotia Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.