The government has unveiled its long-anticipated proposals to increase fiscal revenue by 2% of GDP and maintain social programs created during the pandemic

On Thursday, April 15, the Colombian government presented to Congress its long-awaited fiscal reform proposals. We lay out their key features below.

In 2020, Colombia faced significant challenges amid the COVID-19 outbreak—tax revenues fell by 11.2% y/y versus 2019, while fiscal expenditures increased by 21% y/y in response to the health and social crisis. Together, these developments led to a widening in the central government’s fiscal deficit from -2.5% of GDP in 2019 to -7.8% in 2020; it is projected to widen even further in 2021 to -8.6% of GDP. Gross central government debt rose from 50.3% to 64.8% of GDP. The country’s fiscal rule was suspended under commitments to resume compliance with it by 2022.

KEY FEATURES OF THE PROPOSALS

With these developments in mind and with a broad goal of ensuring fiscal sustainability, the government committed to the development of a fiscal reform package that would also consolidate a more equitable social infrastructure framework. The set of proposals announced on Thursday cover four key elements: (I) redefinition of the fiscal rule; (II) strengthening social programs; (III) redistribution of fiscal burdens (tax reform); and (IV) other items.

I. Fiscal rule changes

The Ministry of Finance (MoF) proposed the adoption of more easily observable variables to define the fiscal rule.

- The proposal would change the definition of “government” from “central government” to “general government”. This is a more ample definition and standard in international metrics. The move would bring in the performance of regions and municipalities in the rule’s fiscal metrics.

- The calculation of the fiscal rule would be augmented to include a ceiling on the stock of net liabilities exclusive of pension obligations. The new rule would feature two parts: a maximum limit on the general government’s primary balance, and an upper bound on the stock of general government debt net of pension liabilities.

In our view, these changes are positive: the new parameters and calculations would give the authorities some added flexibility. Additionally, the key fiscal metrics would be more transparent and better reflect Colombia’s public finances by encompassing data on general government developments.

It is important to note that the new fiscal rule wouldn’t be comparable with its previous incarnation. Both the definition of the rule and its target level would change. Under the newly proposed revised fiscal rule, the initial primary deficit would be limited to -1.8% of GDP for 2022, -0.7 % of GDP in 2023, and -0.2% of GDP in 2024. The primary balance in 2019 was 0.4% of GDP, -4.1% of GDP in 2020, and it is projected to hit -4.8% of GDP in 2021.

II. Strengthening social programs

At the beginning of the pandemic, the government created a new pool of social assistance programs, some of which it wishes to maintain after the public-health crisis has passed. In particular, the government wants to preserve the Ingreso solidario program, which consists of direct and periodic payments to low-income populations, specifically households living in poverty and extreme poverty. Additionally, it wants to continue with a program that reduces labour costs to promote employment for young people, older people who can’t be pensioned, women over 40-years old, and people with disabilities. Lastly, the government seeks to provide ongoing subsidies for undergraduate studies to low-income people and to support culturally-related sectors.

III. Redistribution of fiscal burdens via tax reform

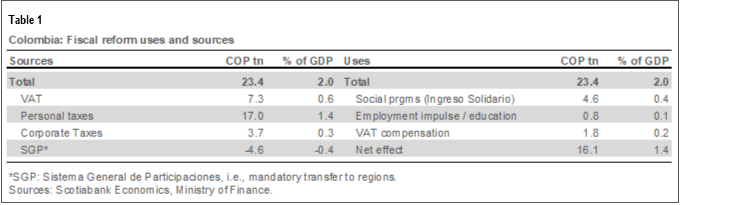

Proposed tax changes would increase levies on wealthy people while adjusting some taxes to enhance the promotion of productive sectors (table 1).

- VAT changes (would generate 26.1% of potential new fiscal revenue). Despite the MoF’s earlier intentions to add essential goods, mainly foodstuffs, to the VAT base, this initiative was dropped from the final draft of the reform package due to its unpopularity. Other items would be taxed with a VAT rate of 19%, while the government would extend low tax rates for capital goods and some essential services.

- Personal taxes (to account for 60.7% of potential new fiscal revenue). High-income people would face increases on taxes applied to salaries, dividends, and wealth under the proposed reforms. The package includes a one-time levy on monthly wages that exceed COP 10 mn (USD 2,700), to be introduced in H2-2021; a wealth tax on assets greater than COP 4.5 bn; and a 15% tax on high incomes from dividends. The proposals also aim to reduce some exemptions to income taxes and bring down tax thresholds to capture more middle-income payers. Under the reform package, gradually more people would be taxed over time. At present, receipts stemming from personal tax collection represent only 6.2% of total fiscal revenue, well below the OECD standard of 24%. These ambitious changes would aim to close this gap.

- Corporate taxes (13.2% of potential new fiscal revenue). The government wants to keep corporate taxes competitive; according to OECD statistics, corporate taxes represent 24.5% of fiscal revenue in Colombia, while in OECD countries, the standard average is 9.6%. Still, in the proposal, the government plans to reduce exemptions and postpone some tax reductions planned for 2022. Additionally, the proposed initiatives would preserve some stimulus for the creative sectors of Colombia’s so-called “Orange economy” and tourism.

- General Participation System (Sistema General de Participaciones in Spanish). By law, the central government must transfer to the regions part of any extra revenues and this would subtract -0.4% of GDP in new fiscal revenues from the MoF’s coffers.

IV. Other items proposed in the fiscal-reform package

Other proposals include some green taxes, most of which are charges on fossil fuels and a tax on single-use plastics.

More importantly for markets, the proposals would also reduce the withholding tax from 5% to 0% for foreign holders of public debt instruments and related derivatives. It is worth noting that the withholding tax reduction was included in previous reform proposals and didn’t pass. In this case, the elimination of the withholding tax on foreigners could be a potential bargaining chip that could be sacrificed in negotiations with Congress.

SUMMING UP

The proposed fiscal reforms aim to generate new revenue and savings equivalent to over 2% of GDP from the beginning of 2022 (table 1, again) and reduce Colombia’s Gini coefficient by 2.3 points (from 51.3 in 2019, which is at the higher end of Latam’s 38 to 58 range in World Bank data). The proposal looks unrealistically ambitious since tax reform initiatives in Colombia, on average, tend to raise fiscal revenues by around 0.6% of GDP. The MoF has indicated that the government needs around 1.5% of GDP in new revenues to ensure long-run fiscal sustainability; therefore, we expect Congress to water down these proposed reforms at their margins. Still, even after any modifications, we expect that the Colombian government will be able to raise the roughly 1.5% of GDP in resources needed and send a message of fiscal responsibility to international credit-rating agencies and markets. This should allow Colombia to keep its investment-grade status.

Looking ahead, the government expects to gain approval of the fiscal-reform package before mid-June when the first legislative session ends. The authorities already emphasized that social programs currently set to expire in June will be made permanent, which increases the government’s incentive to negotiate with Congress in an expeditious fashion.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.