Countervailing winds

Strong Q4 recovery trend

Metal prices

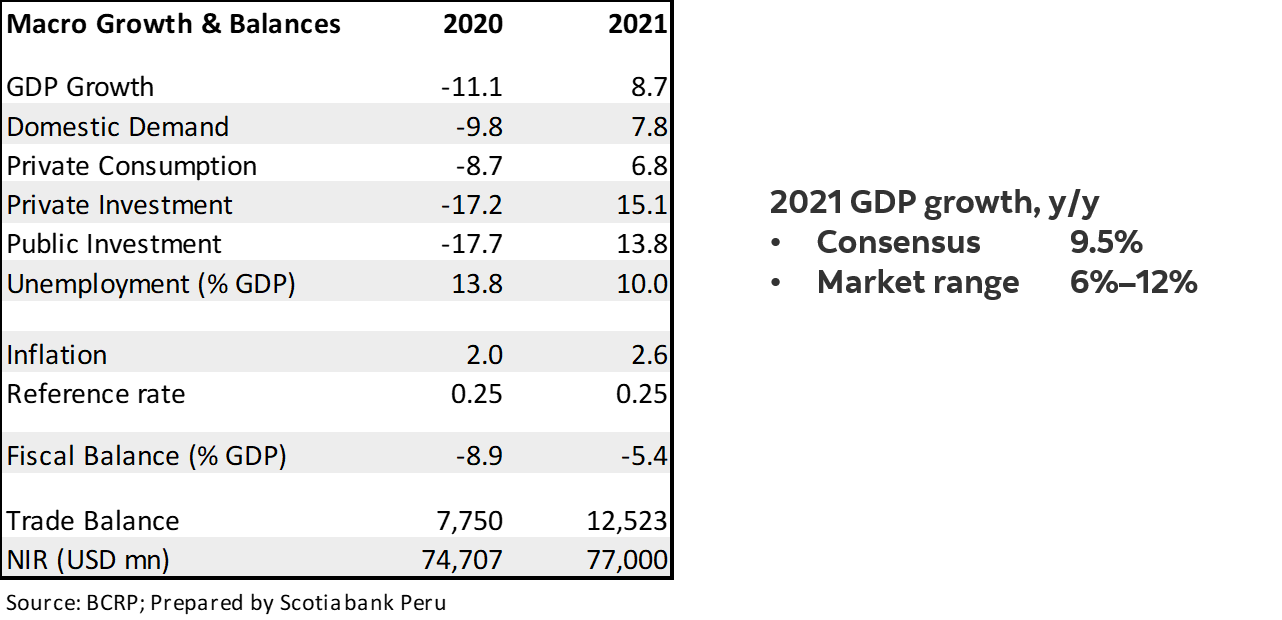

Strong macro balances

Political turbulence

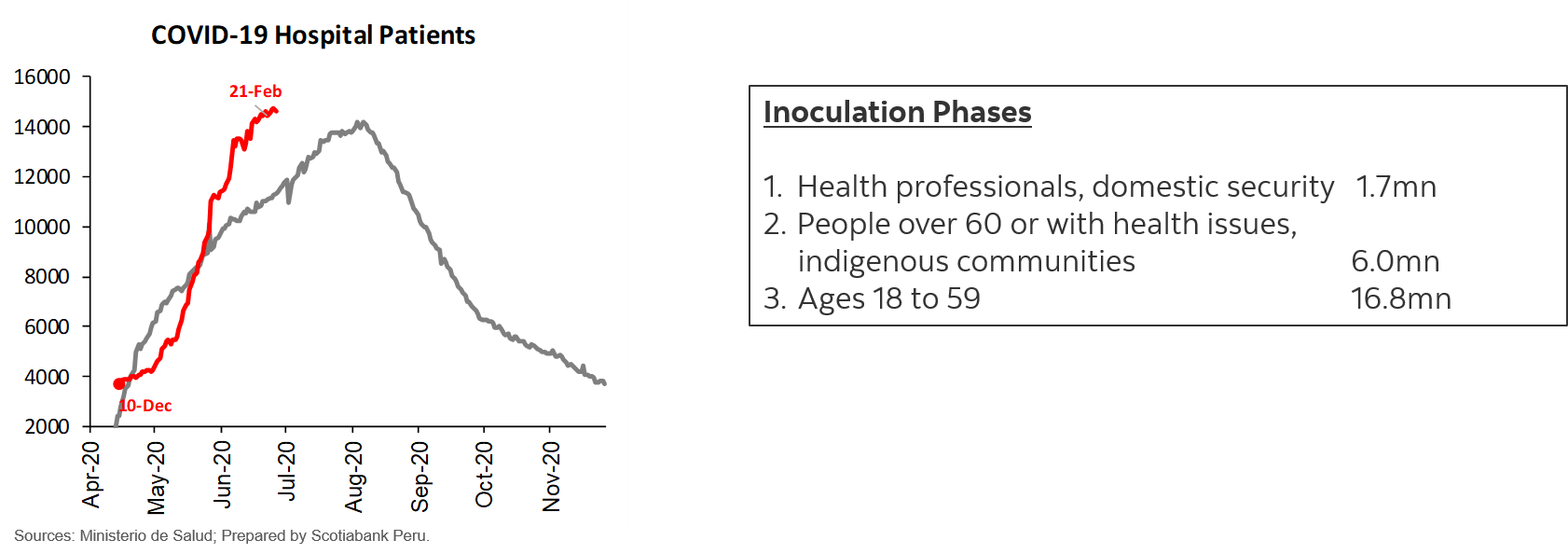

Second COVID-19 wave

Elections

COVID-19 second wave

Mortality per million: 1,200 (the world average is 280 per million).

- Timing of second-wave restrictions much later than in first wave.

Status of vaccines

Procurement of 85 mn doses.

1 mn have arrived, 2 mn in March, 10 mn by June.

Government goal: 15 mn vaccinated by July.

160,000 health professionals have been vaccinated (0.5% of the population).

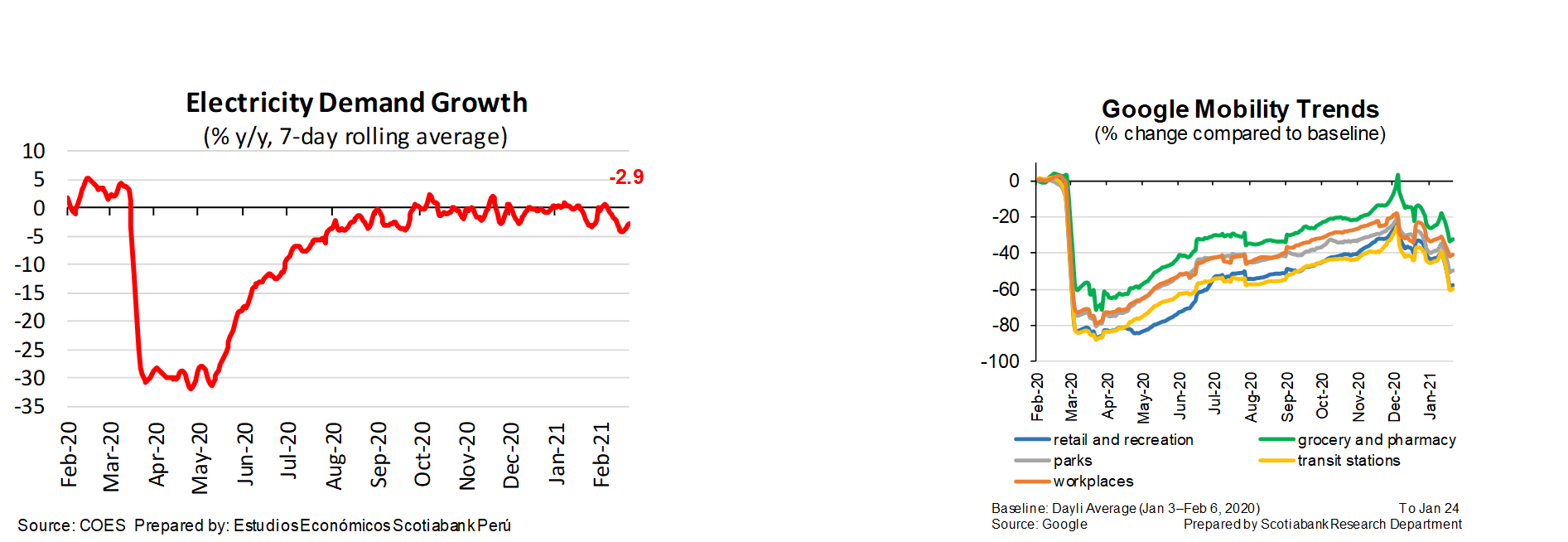

New measures restrict mobility, not production

- 95% of the economy allowed to operate, versus 44% at height of 2020 lockdown.

- Our GDP growth forecast of 8.7% y/y for 2021 in line with 6.8 weeks of restrictions.

- New support measures represent 2.5% of GDP in resources for households.

- Difference between electricity demand and mobility trends: government restrictions have affected mobility, but not production.

Support measures:

- PEN 600 transfer to over four million families.

- One-month postponement on the payment of income, sales, and other taxes.

- PEN 2 bn small-business support program (similar to Reactiva), and a PEN 0.2 bn tourism support program.

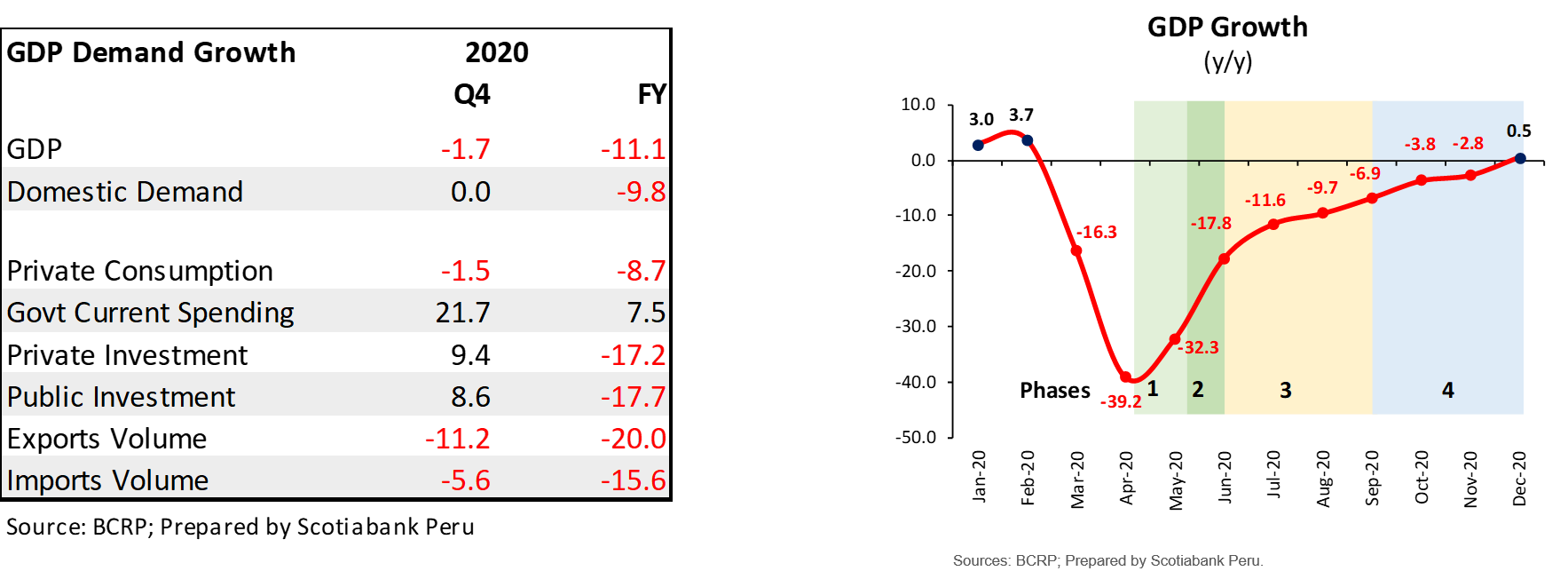

2020: the recovery was better than expected

Q4 especially strong

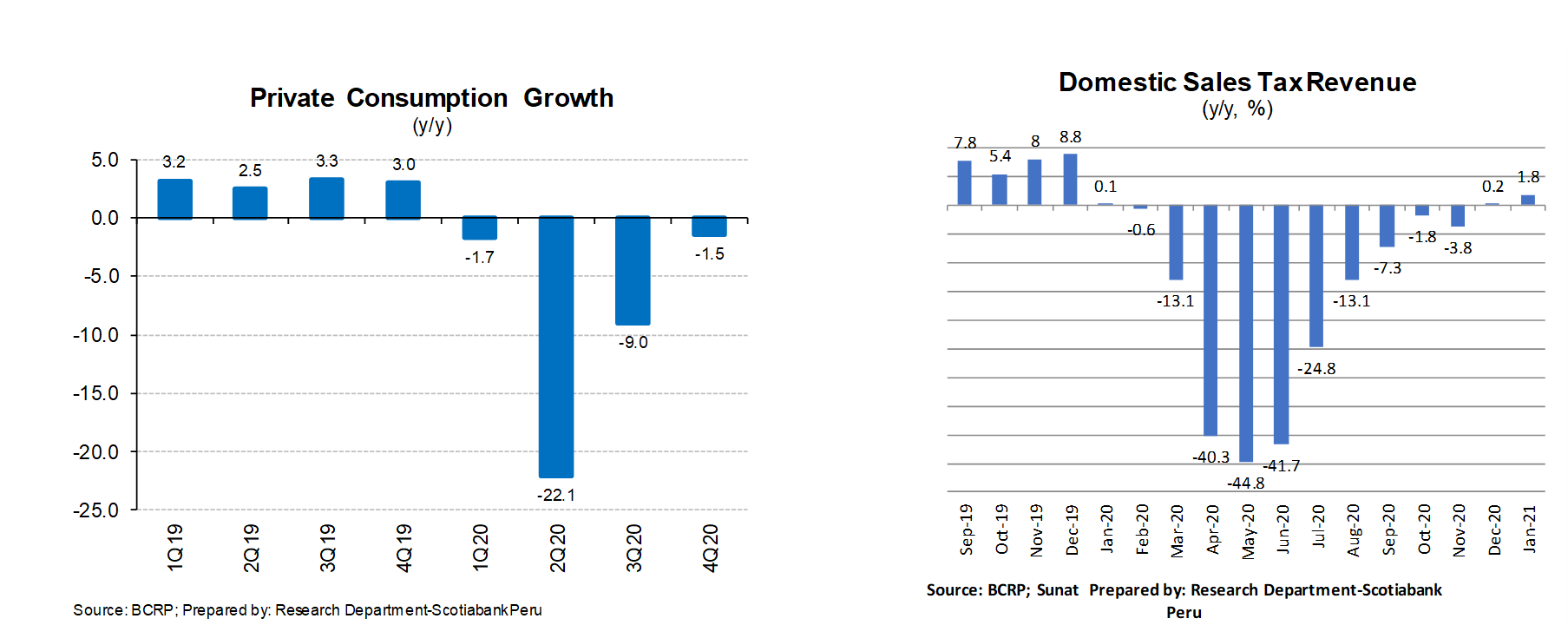

Domestic demand did not contract.

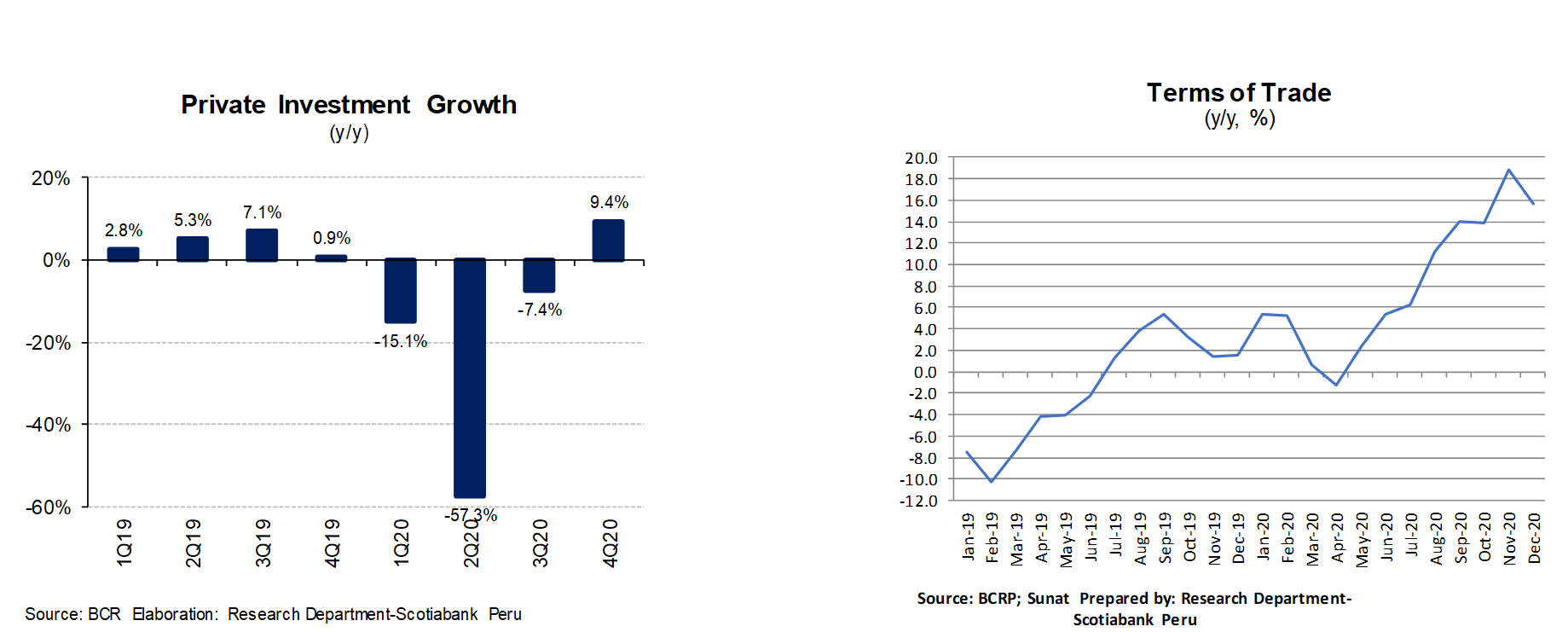

Surprisingly strong private investment turnaround.

December: positive growth ahead of expectations.

6 of 12 major sectors rose (fishing, construction, resource processing, government services, telecom, and financial services).

An encouraging improvement in private demand—investment

Technological transformations.

Booming real estate.

Companies adapting to new consumption patterns.

Terms of trade (high metal prices) have traditionally given strong support to macro accounts and business confidence.

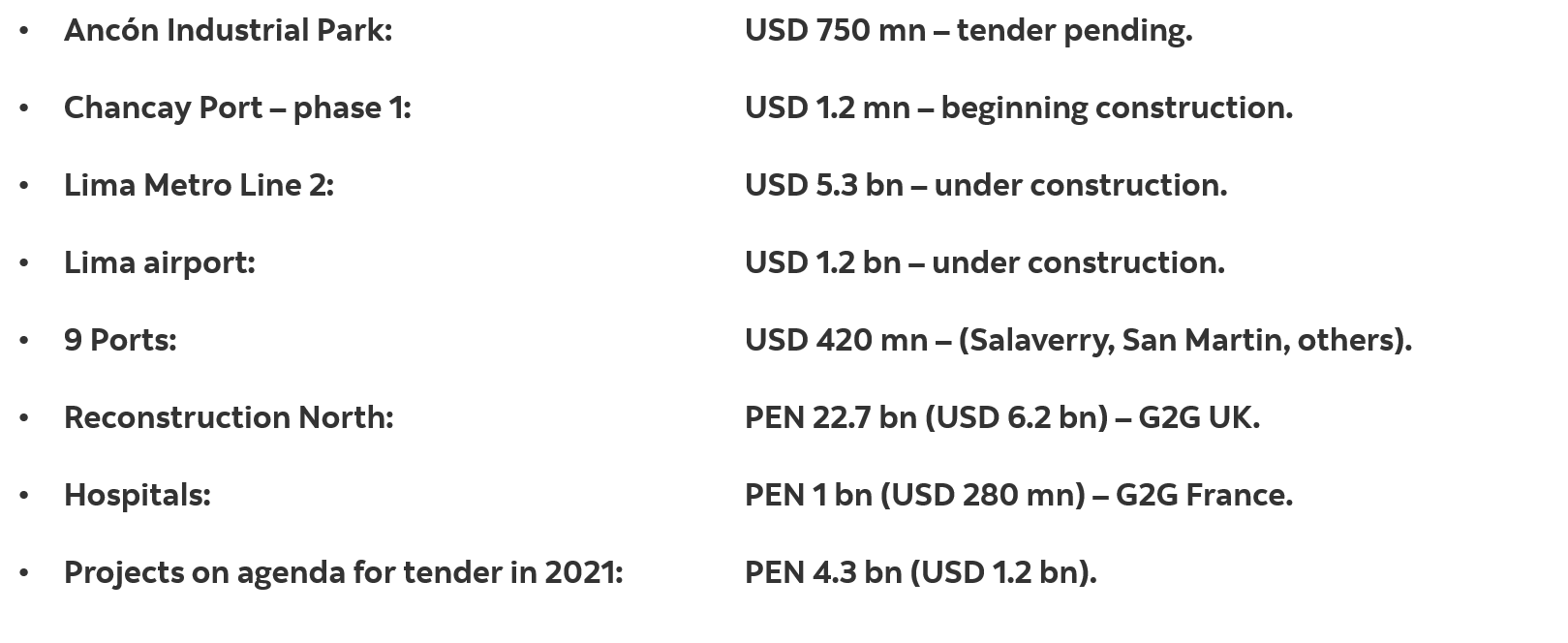

Infrastructure investments are slow, but progressing

An encouraging improvement in private demand—consumption

Government measures (5.5% of GDP).

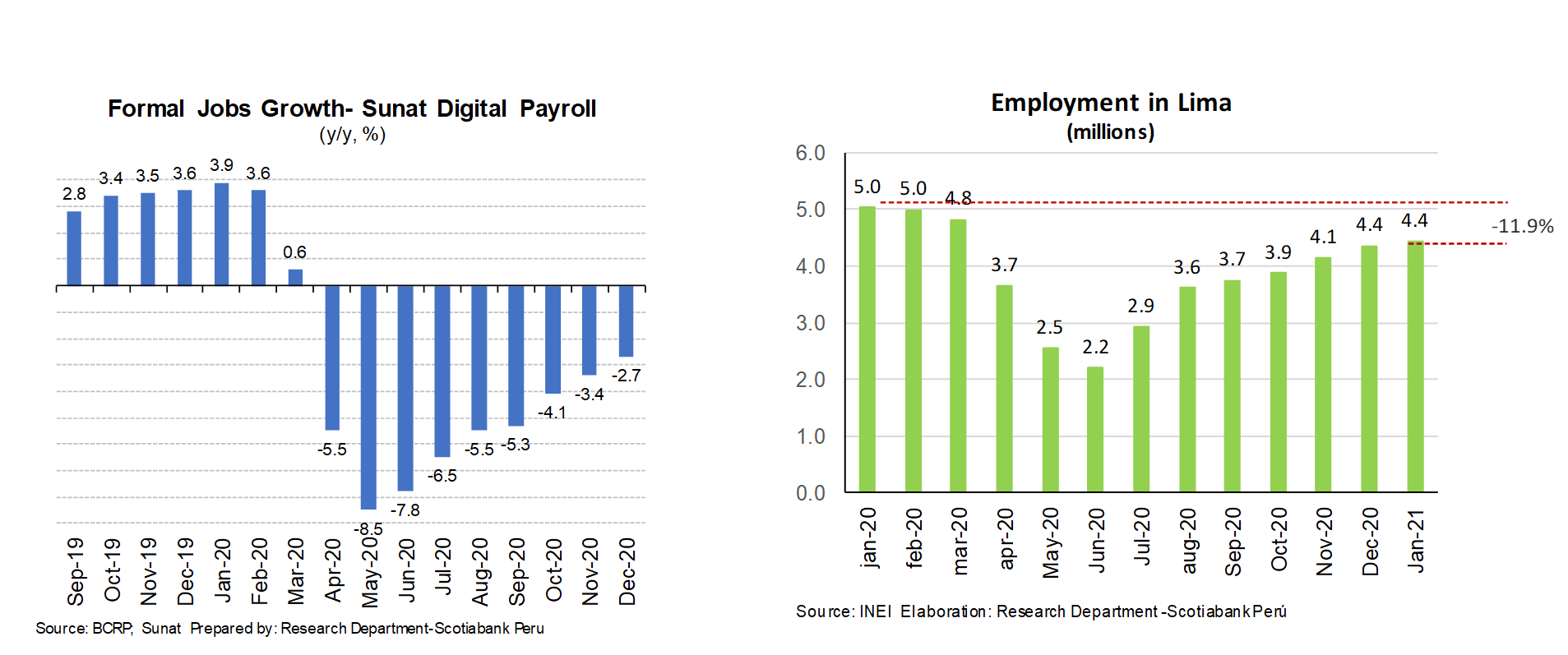

Rebound in employment.

New (virtual) sources of service income.

Sales tax revenue above pre-COVID-19 levels reflects robust sales, but also new activities and the formalization of informal sales through digitalization.

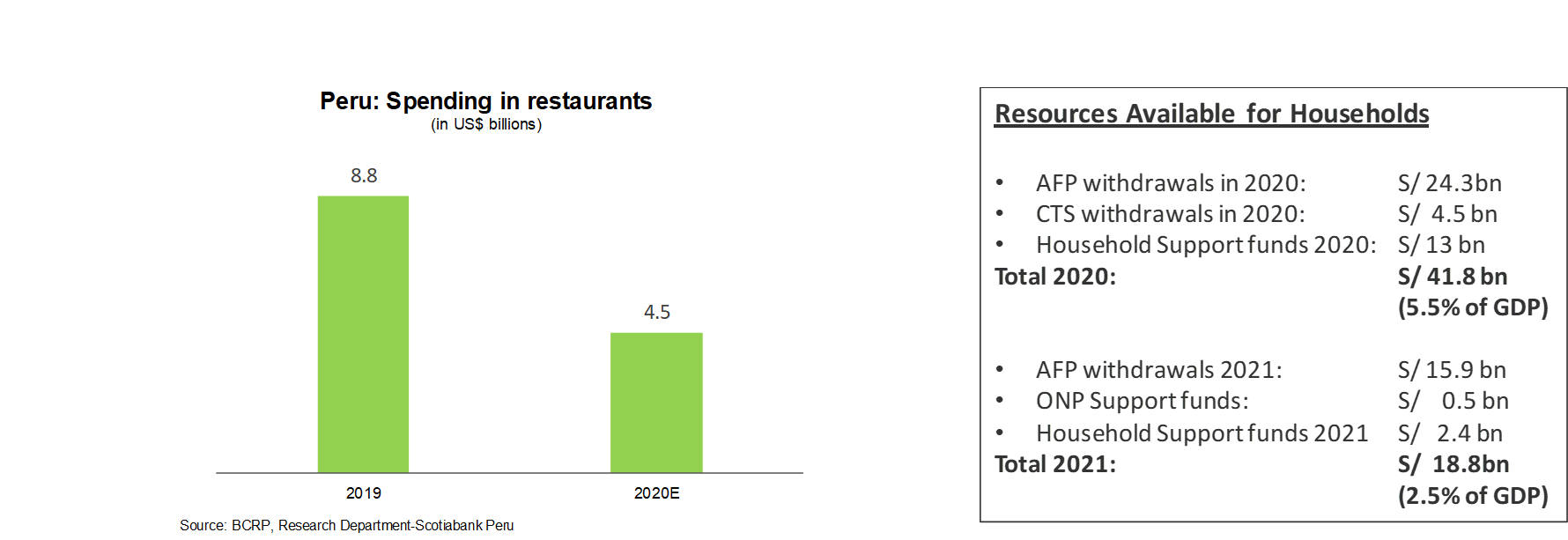

Resources available to boost domestic demand

In 2020, government transfers and access to savings helped sustain consumption.

Resources that will be available in 2021: +5% of GDP.

Household deposits at banks up by PEN 30 bn (15%) between March and December 2020.

lower spending on restricted activities + resources from AFP withdrawals + Reactiva.

Nearly PEN 19 bn in pension withdrawals, government transfers.

Employment is also recovering, albeit still under past levels

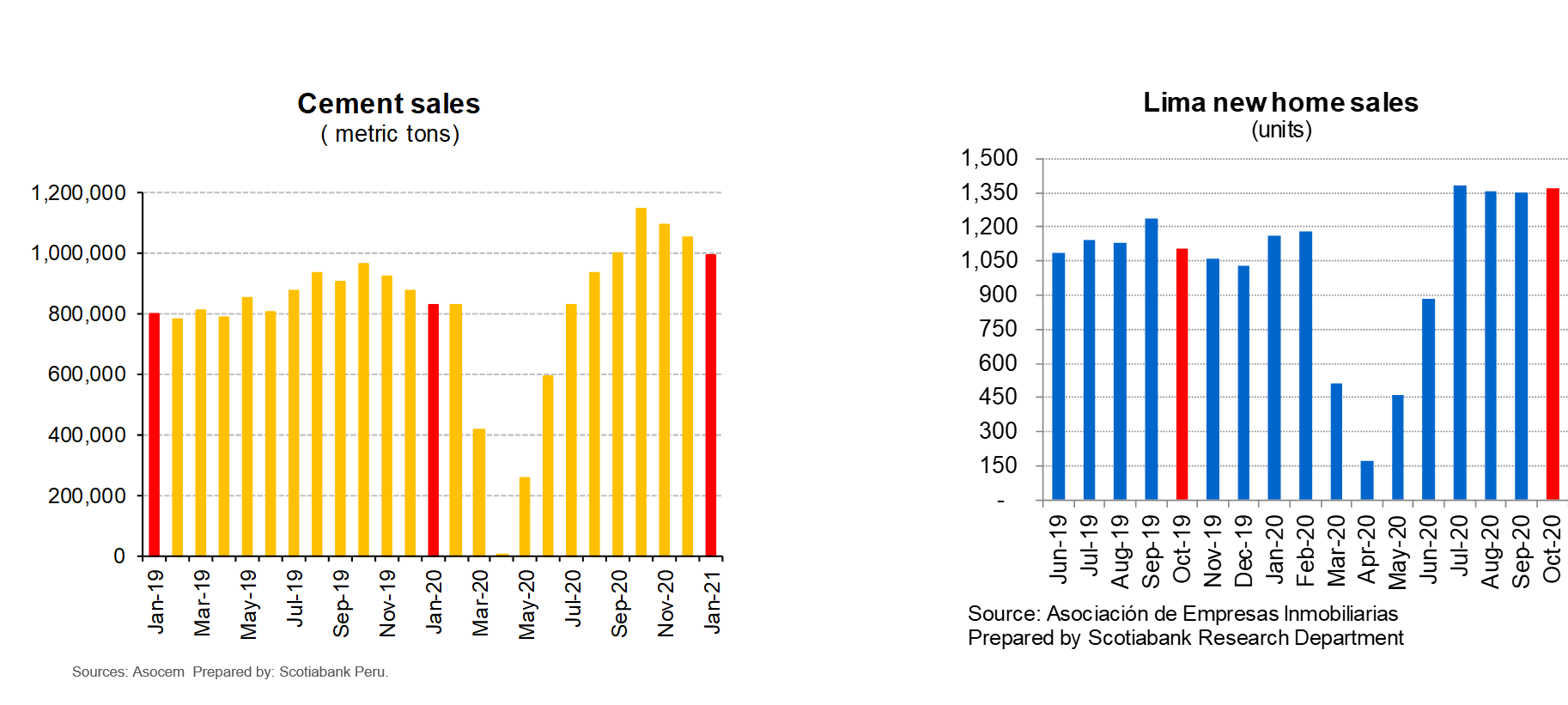

Construction is booming

Cement sales have risen 19%–20% y/y each month from October 2020 to January 2021.

Construction GDP is currently significantly above pre-COVID-19 levels.

Part of construction growth is government spending, but most involves a booming real estate market.

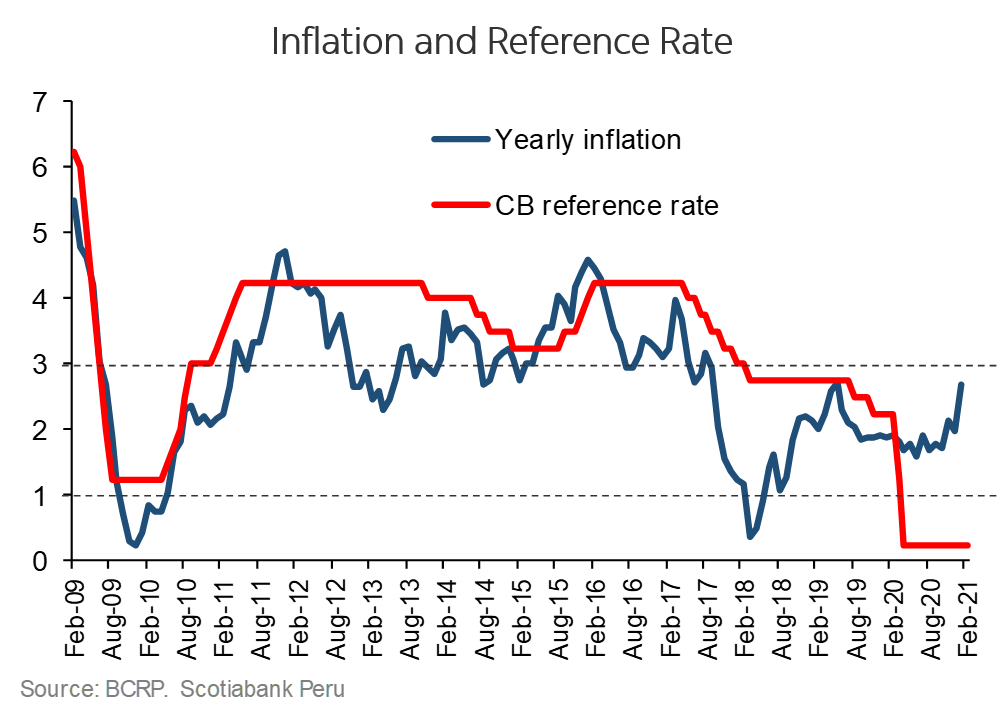

Low interest rates is probably the most likely source

The reference rate will remain low well into 2022, although rising inflation merits monitoring.

Metal prices are changing external outlook

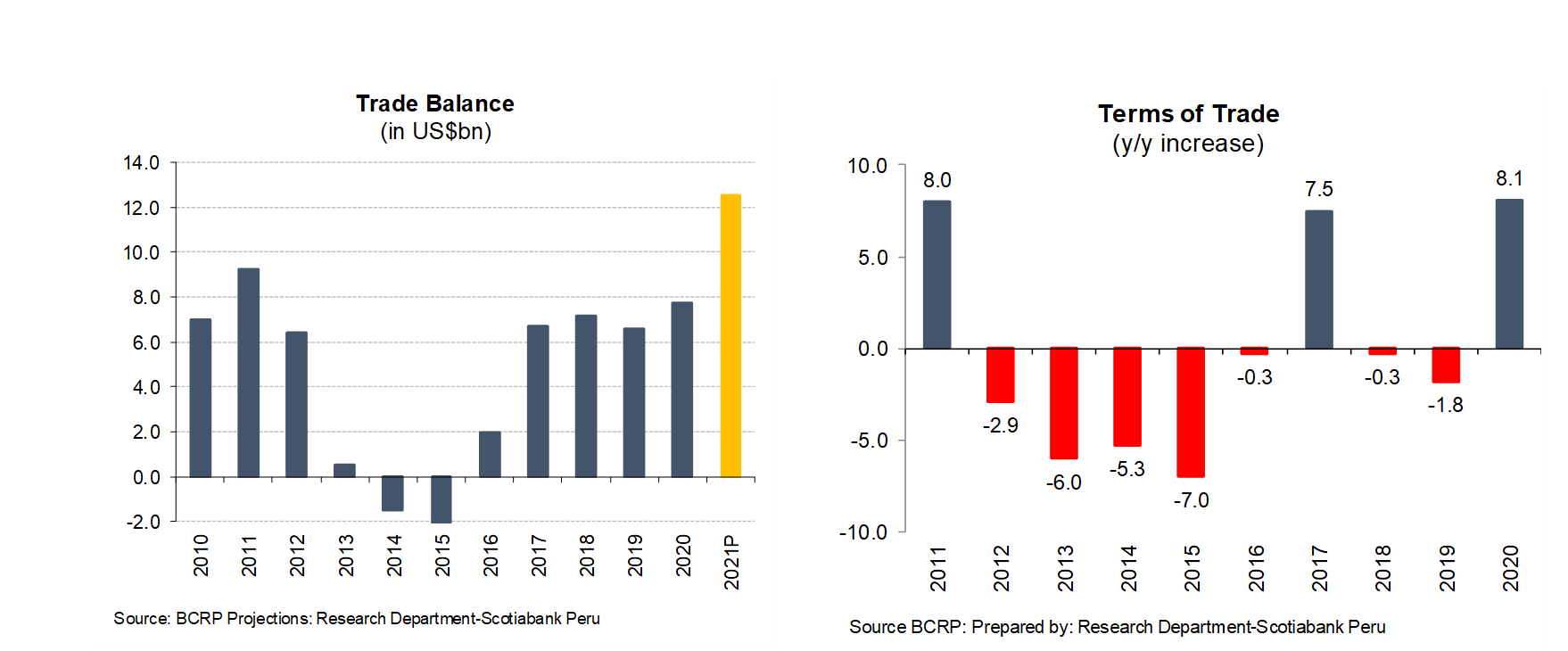

External accounts are very, very strong, and are set to get even stronger in 2021 as metal prices move higher.

2020 Current Account: 0.5% of GDP.

Net international reserves: USD 74.7 bn, or 25 months of imports.

Every one cent increase raises exports by USD 50 mn.

A copper price of USD 4.00/lb would increase exports by over USD 3 bn.

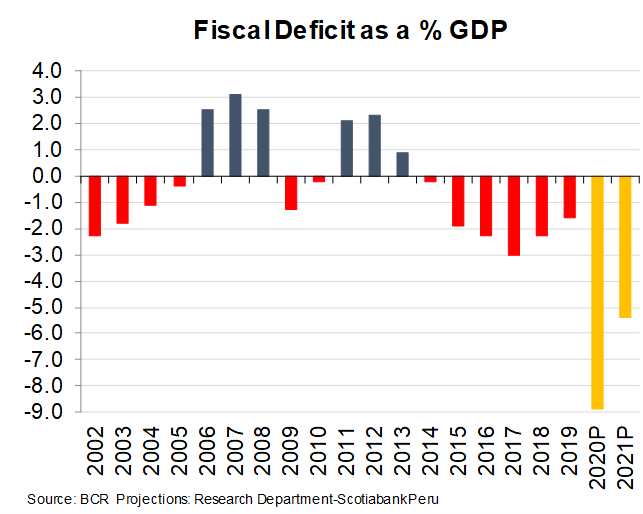

Metal prices could lower 2021 fiscal deficit

Current 2021 forecast: -5.4% GDP, with avg copper price of USD 3.35/lb.

Every one cent increase raises income tax revenue by USD 10 mn.

A copper price of USD 4.00/lb would increase income tax revenue by USD 650 mn to USD 800 mn.

This would bring down the fiscal deficit by 0.4 ppts to 0.5 ppts.

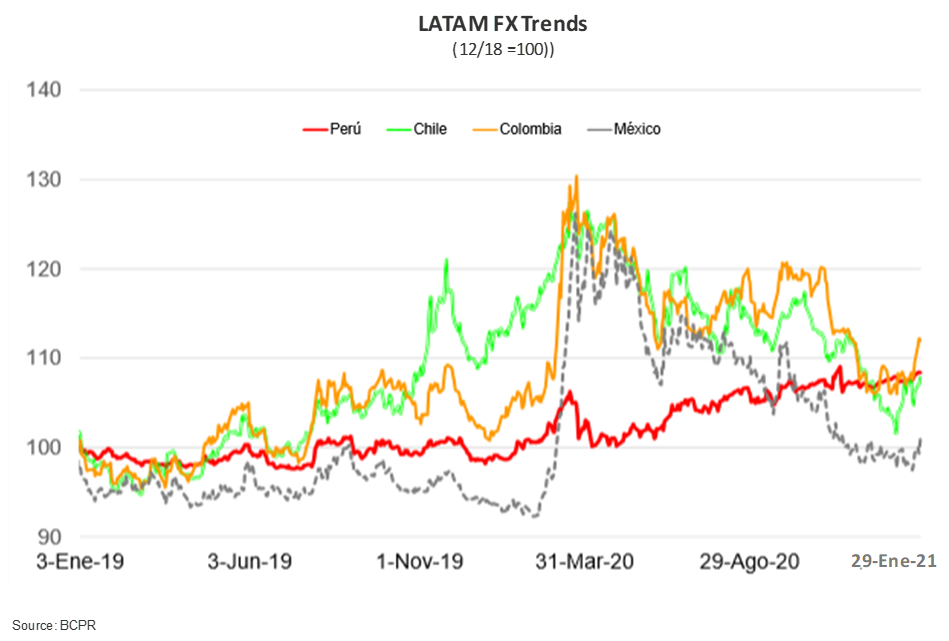

PEN is not aligned with regional peers

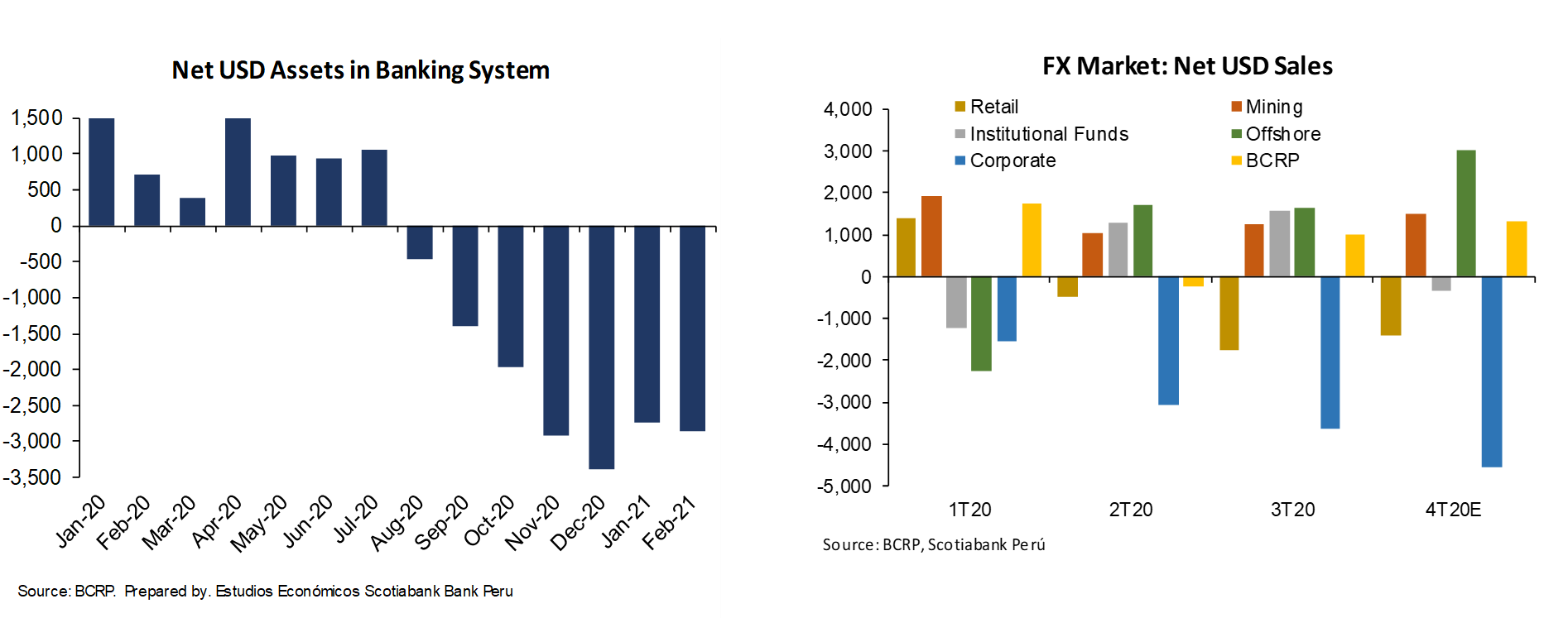

Corporate demand for USD liquidity has shifted from bank loans to FX market

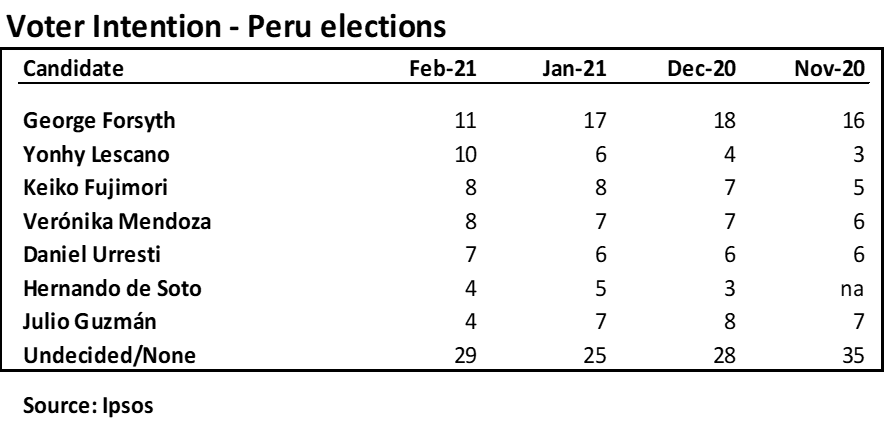

Elections are in seven weeks

Health crisis + credibility crisis + political crisis + economic crisis may bolster anti-establishment vote.

A quarter of voters are undecided.

Votes will shift from lagging to leading candidates as elections near.

Key issues regarding new authorities

Forsyth no party; city mayor.

Lescano no executive experience; Congress.

Fujimori political experience; no executive experience.

Mendoza no party; no executive experience.

Urresti no party; no executive experience.

Guzmán new party; no government experience.

No candidate has significant governing experience or proven management capacity.

New cabinet head: will define political priorities and governance.

New finance minister: will define policy quality and continuity.

New BCRP Board: will define monetary solvency and confidence.

The new Congress will include many members with little experience (new law prohibits re-election).

Governability is at issue (again!)

Vacunagate has renewed governability risk—the risk of an empowered Congress

Exceptional times: health crisis + credibility crisis + economic crisis.

Why is Peru in a state of seemingly perpetual political turbulence?

The difference between Peru and other countries is the weakness of political institutions and of the rule of law.

Political parties neither represent voters (no constituencies) nor do they develop future leaders.

The application of the law is unpredictable.

State management capabilities have deteriorated.

Economic institutions are strong, but the above puts them at risk.

Legislative legacy

Constitutional Court has struck down:

1. road tolls elimination;

2. reimbursement of public pension funds; and

3. automatic worker promotion in State institutions.

Pension fund reform

Mining law

Interest rate caps

Possible future initiatives:

Wealth tax

Education reform

The bright spot

After the Presidential elections are concluded, the economy could soar:

Electoral uncertainty resolved

New authorities with the credibility of having been elected

A vaccinated population in a vaccinated world

Renewal of correlation between metal prices and private investment

Pent-up investment and consumption (high level of savings)

Robust macro accounts

Infrastructure investment already tendered

- A more digitalized world

Key: adequate governance, continuity in economic policy, no sharp decline in metal prices

Estudios Económicos – Scotiabank (Peru)

Guillermo Arbe

51.1.211.6052 (Peru)

Scotiabank Peru

guillermo.arbe@scotiabank.com.pe

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.