Drop in new COVID 19 cases (Omicron) and ICU-bed occupancy, but still at high levels.

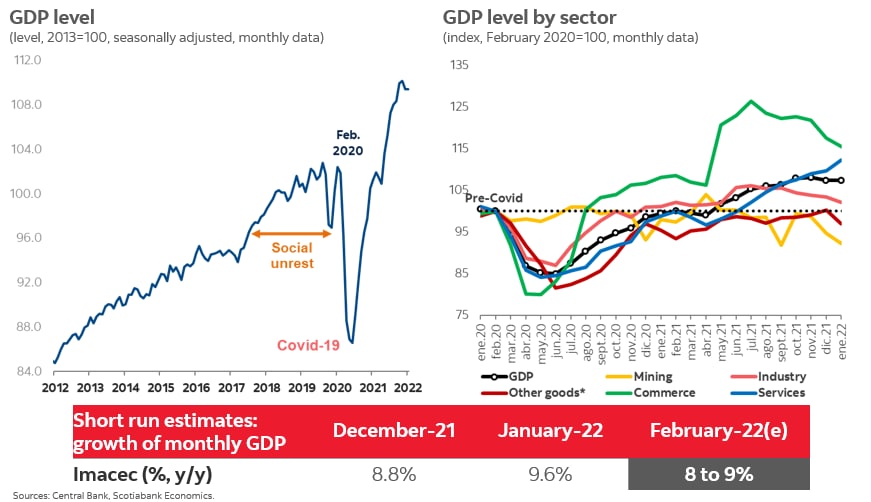

GDP surpassed pre-Covid levels in 2021Q3 led by private consumption and investment. By sector, commerce is the most dynamic sector, followed at the margin by investment-related services and construction.

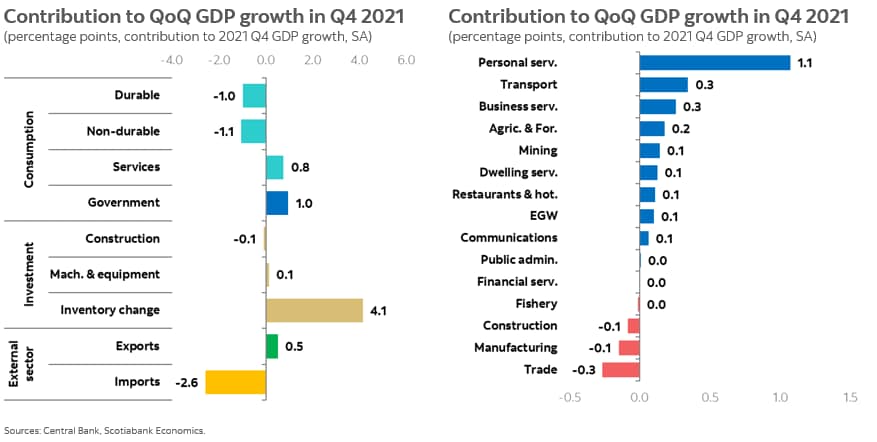

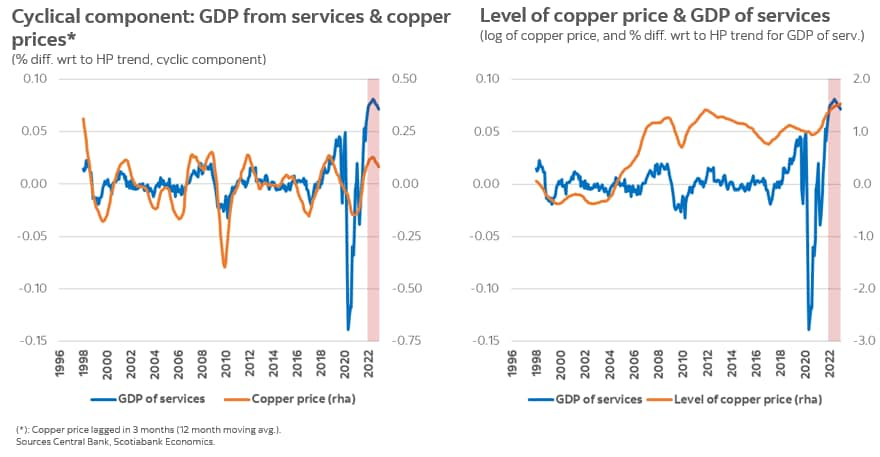

Recovery of GDP in Q4 led by consumption of services, the expansive effect of fiscal policy, and rebuilding of inventories. Service sectors supported GDP in the last quarter.

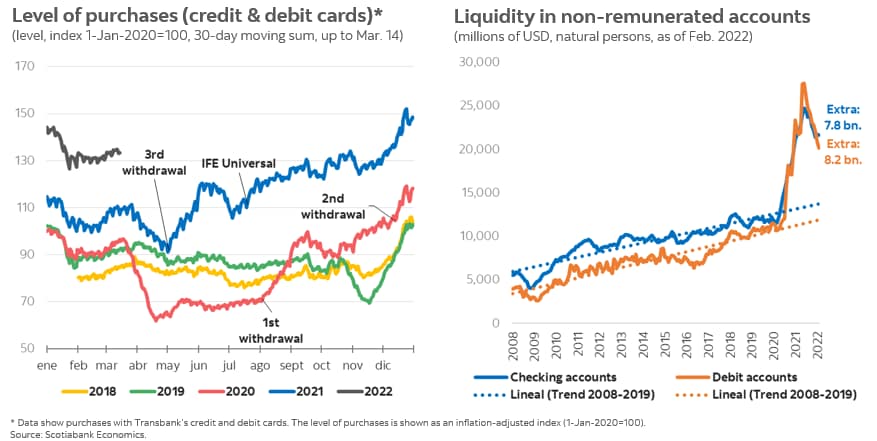

Pres. Boric ruled out new withdrawals from pension funds. There is still USD 16 bn in checking and debit accounts that will support a smooth deceleration of private consumption. On top of this, the Universal Pension will add USD 1.5 bn to high-propensity-to-consume households in 2022.

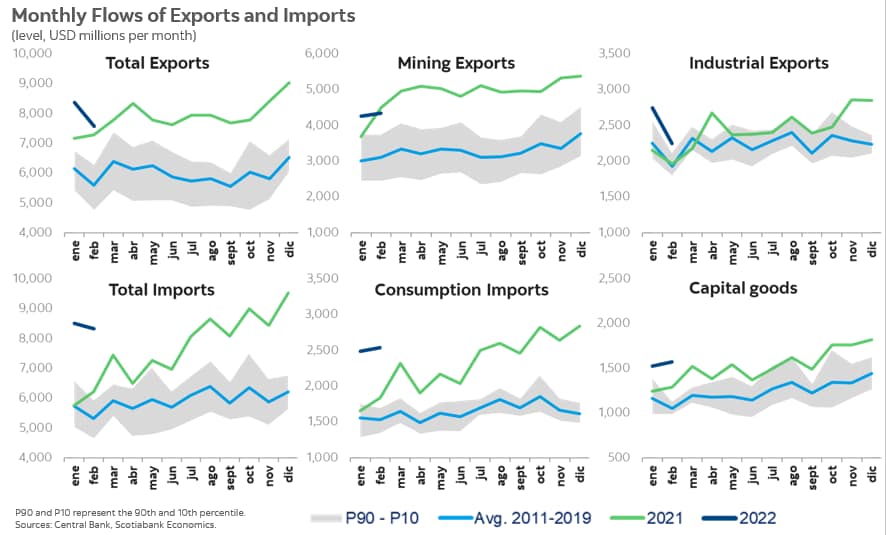

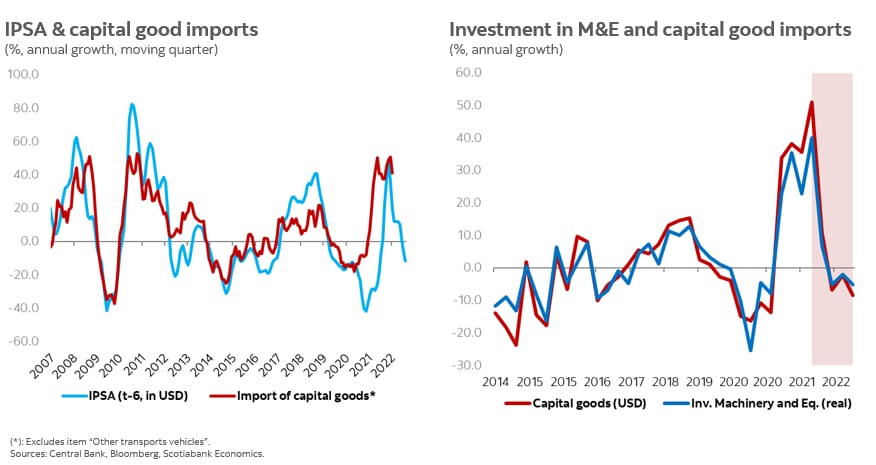

Strong exports. Inventory replenishment continues and capital goods imports remain very solid.

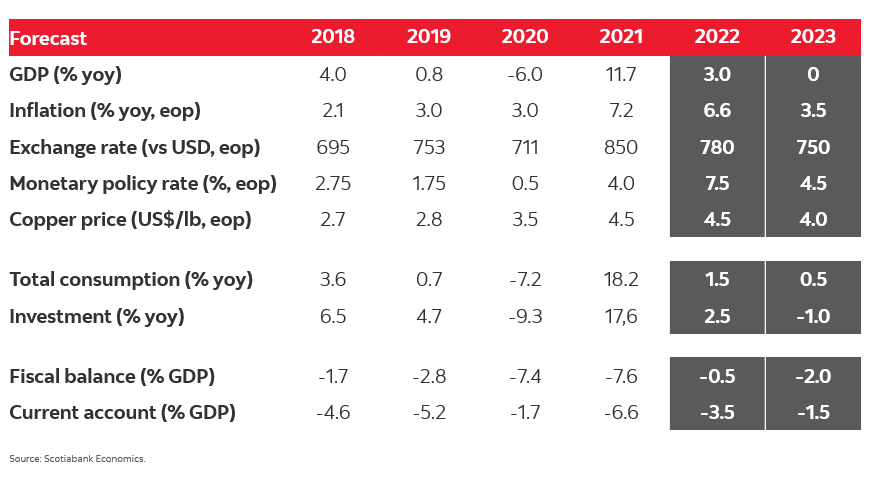

GDP expanded 11.7% y/y in 2021. We forecast GDP growth around 3% y/y in 2022 and 0% y/y in 2023. We estimate Imacec expanded 8 to 9% y/y in February.

High copper prices will give support to services. Representing 47% of the total, services will contribute around 1.4 ppts to GDP growth in 2022.

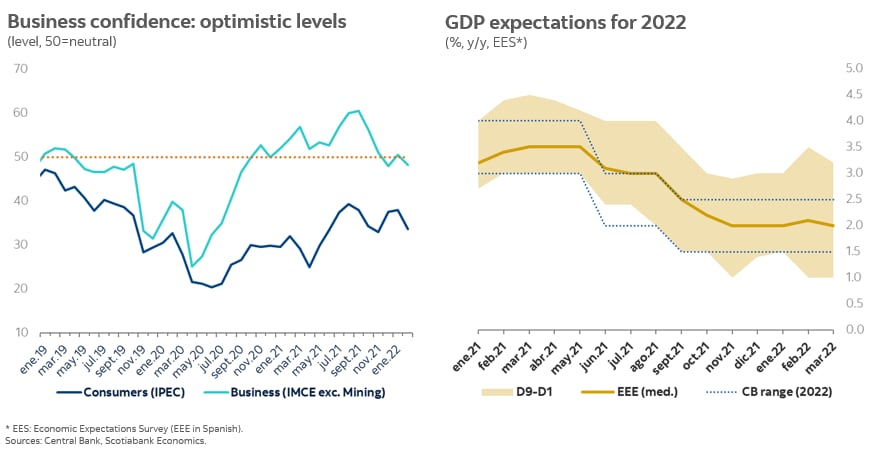

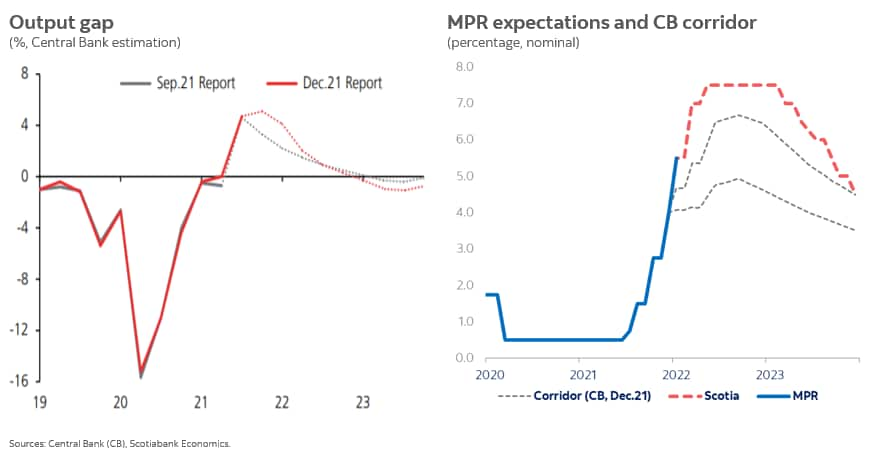

Stabilization in confidence and economic expectations post-elections. Consensus and the central bank anticipate a GDP expansion around 2.0% y/y for 2022.

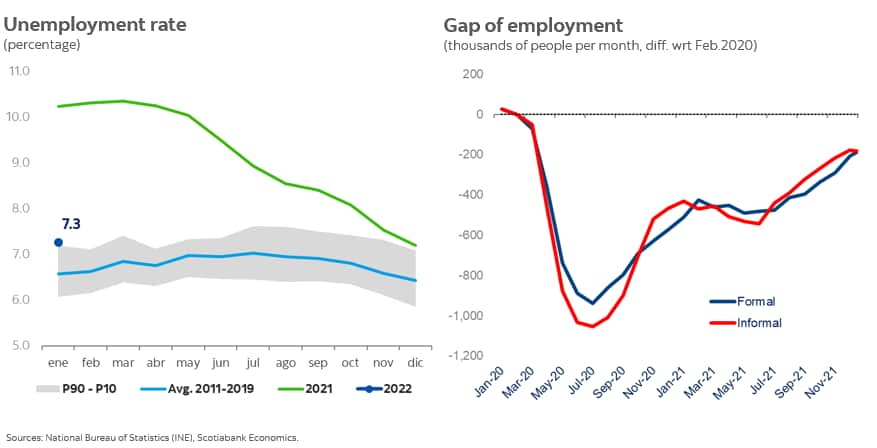

Unemployment rate increased to 7.3% in January due to higher growth in the work force (0.5% y/y) compared to employment (0.4% y/y). The employment gap compared to the pre-pandemic level fell to 350k, of which 160k corresponds to formal jobs and 190k to informal jobs.

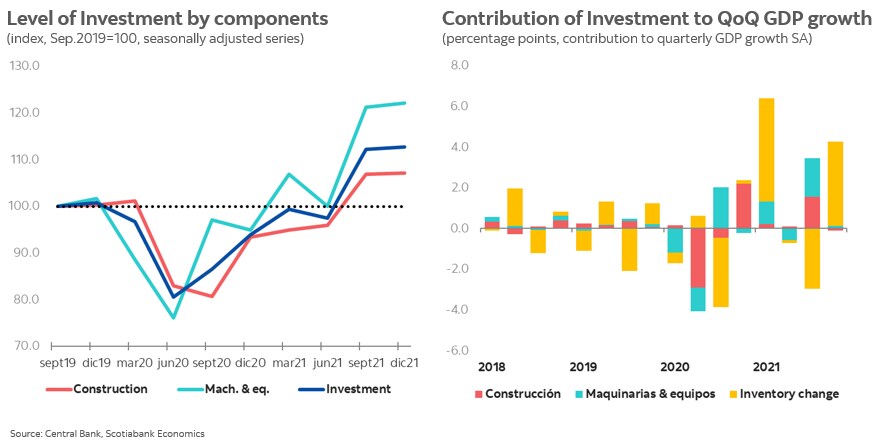

Investment components recovered pre-Covid levels. Rapid recovery of the M&E component and normalization in Construction due to the opening of the economy. Inventory rebuilding supported investment growth in Q4 2021.

As stocks signal, we expect a slowdown in the import of capital goods in coming quarters, and therefore in investment in machinery and equipment (M&E).

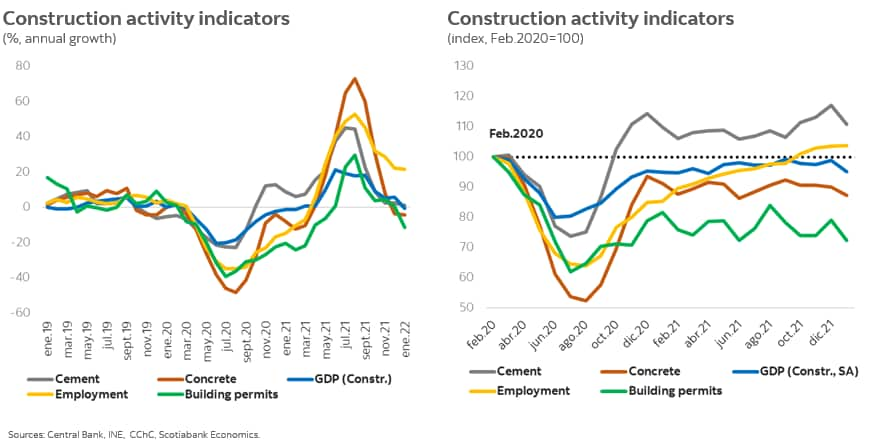

Stabilization of construction activity indicators. Re-opening is favouring the recovery of construction.

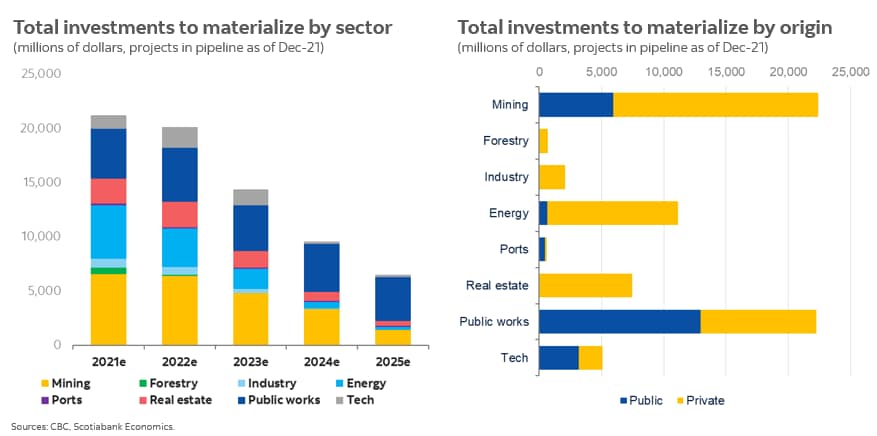

As of December 2021, investment projects in the pipeline for the period 2021-25 reached USD 71.7 bn. Investment was adjusted upward by USD 2 bn (2.8%) for 2021-25, mainly in Energy, Mining and Public works (18% public and 13% concessions).

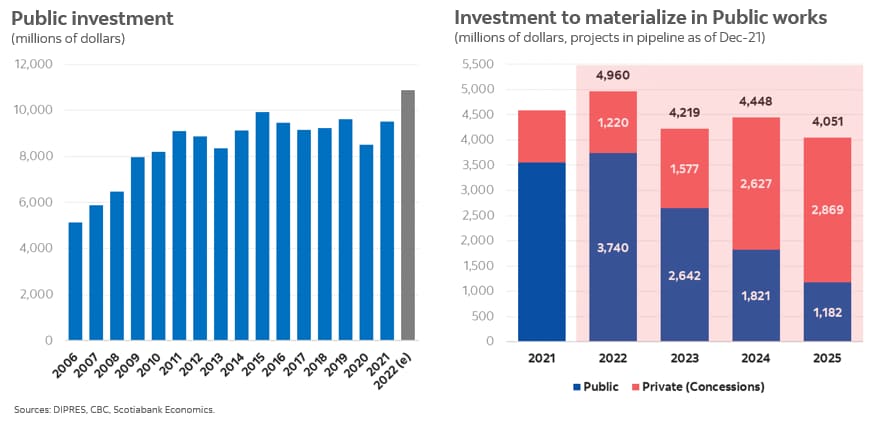

Strong fiscal impulse in public investment in the coming years. Fiscal Budget for 2022 includes an increase of 14.3% in capital expenditures. Projects in pipeline of public works reached USD 17.7 bn for period 2022-25 (public and concessions).

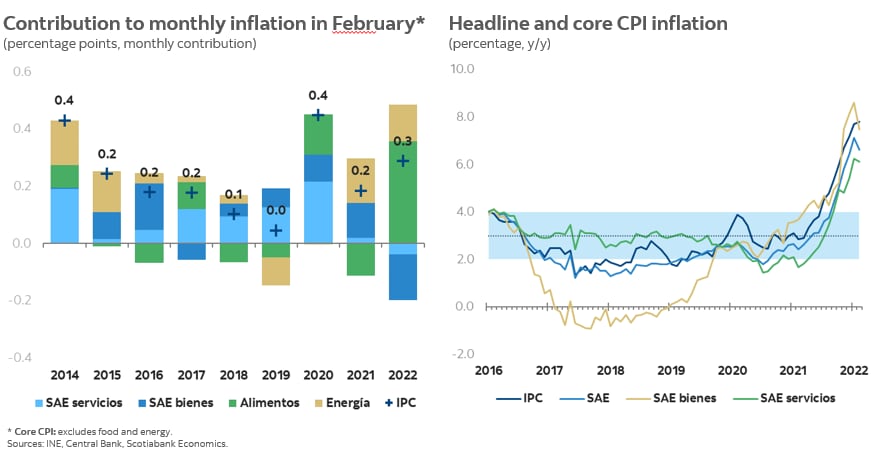

February inflation (0.3% m/m; 7.8% y/y) gives a small break, but inflationary pressures remain.

Inflationary pressures fuel the already worrying de-anchoring of inflation expectations. CB will increase the benchmark rate by 150 bps at March 29 meeting.

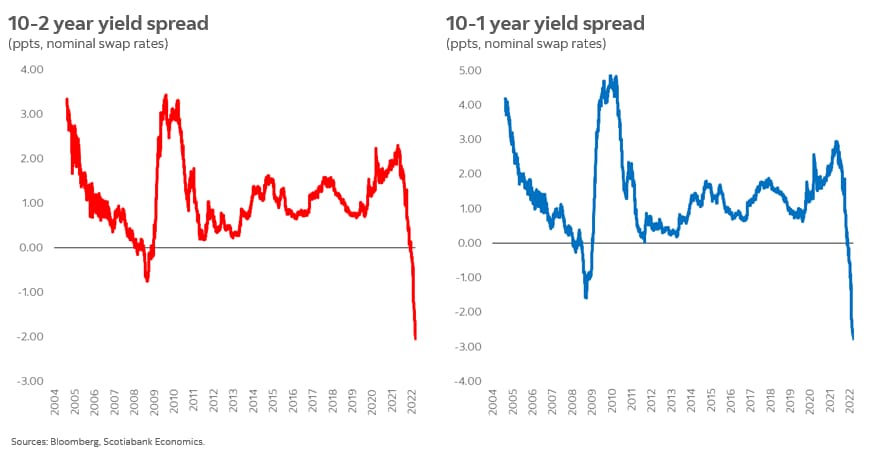

Rise in short-term nominal interest rates and 10-year rates falling and down to negative arena for first time since 2008-09.

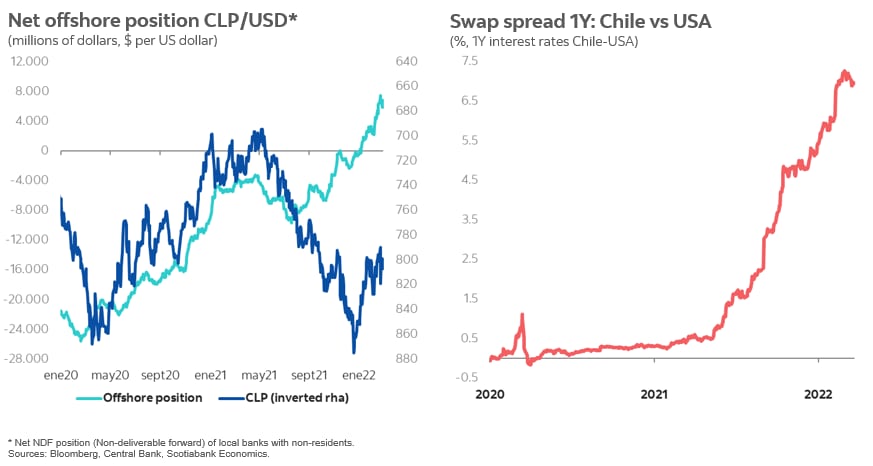

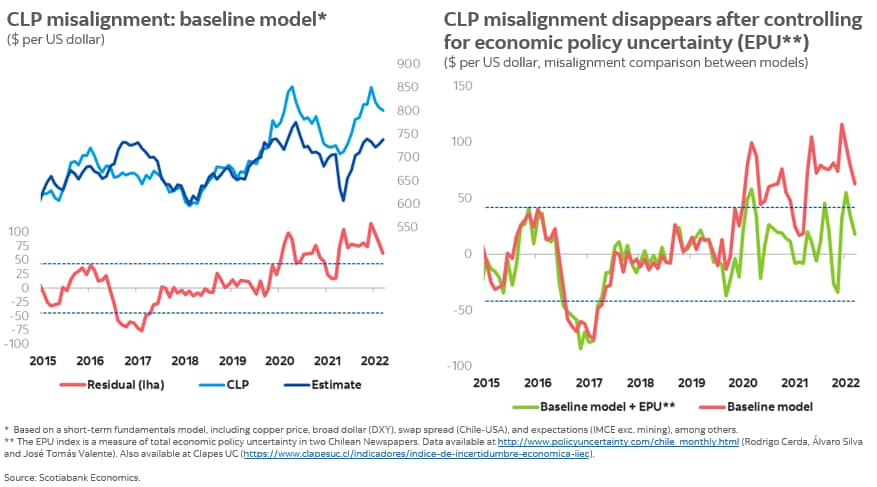

Despite the rise in interest rate differentials, the net offshore position continued rising in favour of the CLP, reaching positive levels for first time since 2010. Any improvements in political perceptions should trigger further CLP appreciation.

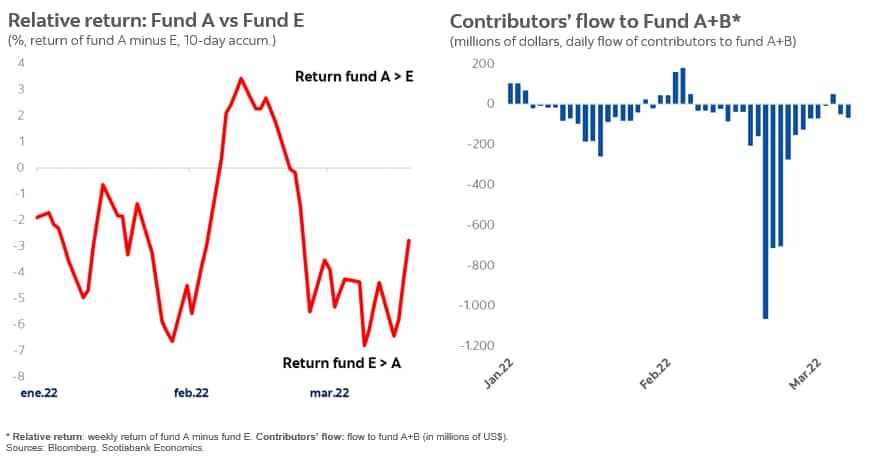

The relatively poor performance of risky funds (A & B) in recent months increased the incentives for contributors to shift their asset allocations in favour of fund E (which has a high share of peso-denominated fixed-income securities)

Our baseline model implies a large misalignment of the CLP compared with its classic fundamentals. However, when we include economic policy uncertainty in our model, the misalignment disappears.

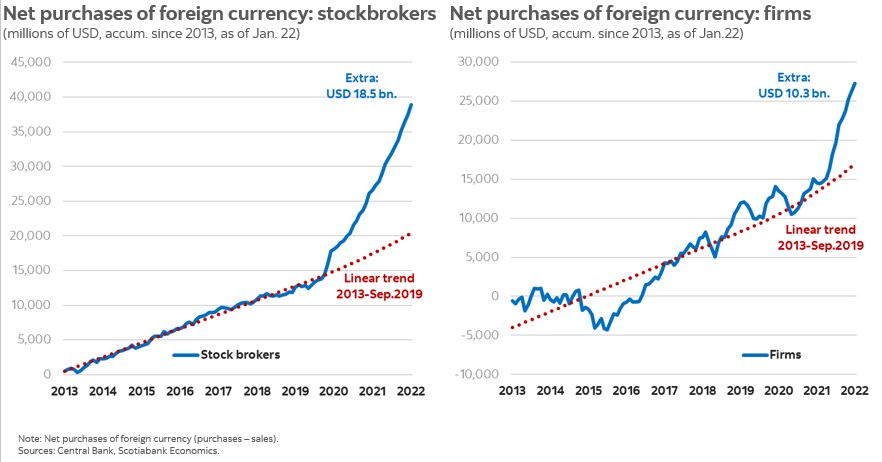

Stock brokers and firms have been increasing their purchases above the trend from before the social unrest.

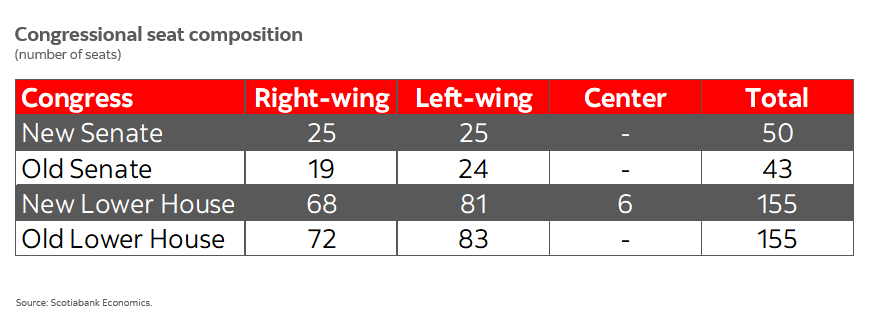

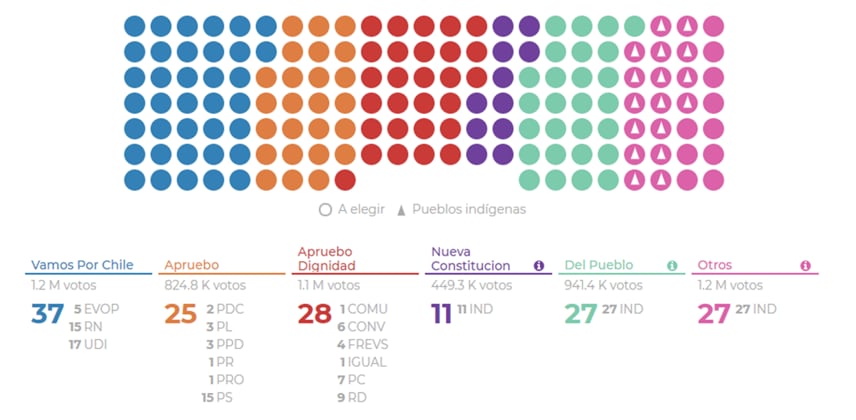

More balanced composition of political forces in Congress from March 2022.

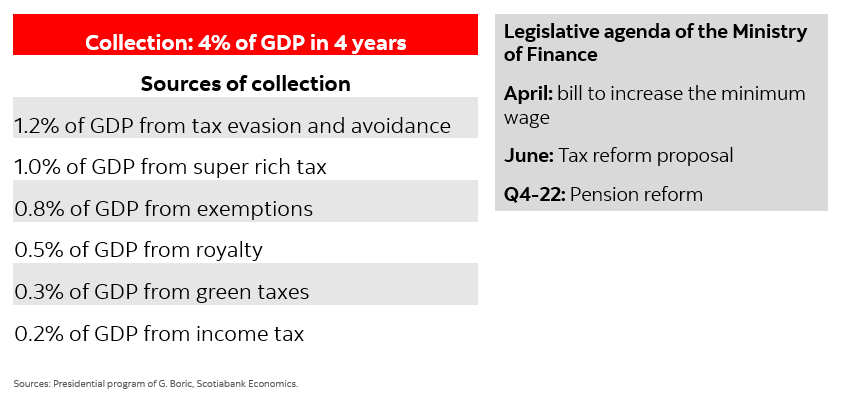

Gabriel Boric’s economic agenda: tax reform will collect around 4% of GDP.

Economic Outlook

Composición de la Convención Constitucional

Quórums:

2/3 = 103 votos.

1/2 = 78 votos.

* Vamos por Chile (37) necesita al menos 14 votos adicionales para bloquear aprobaciones en el pleno

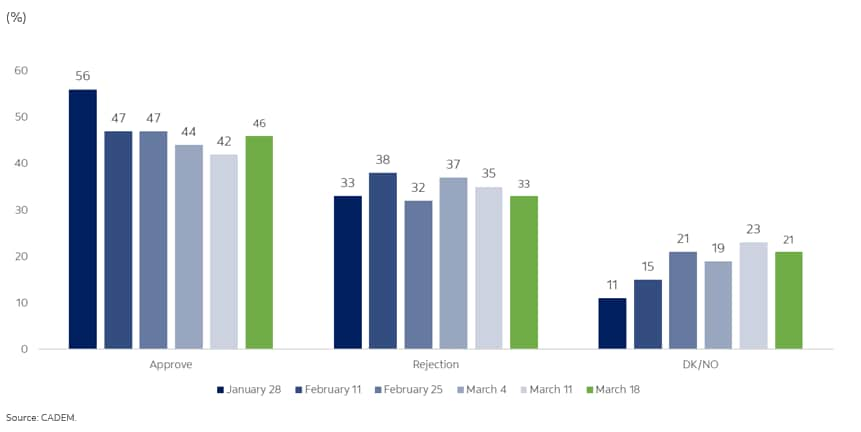

Support for the exit referendum has been falling. More people are undecided.

Exit Referendum: With the information you currently have, would you vote to approve or reject the constitution proposed by the Constitutional Convention in the exit referendum in September this year?

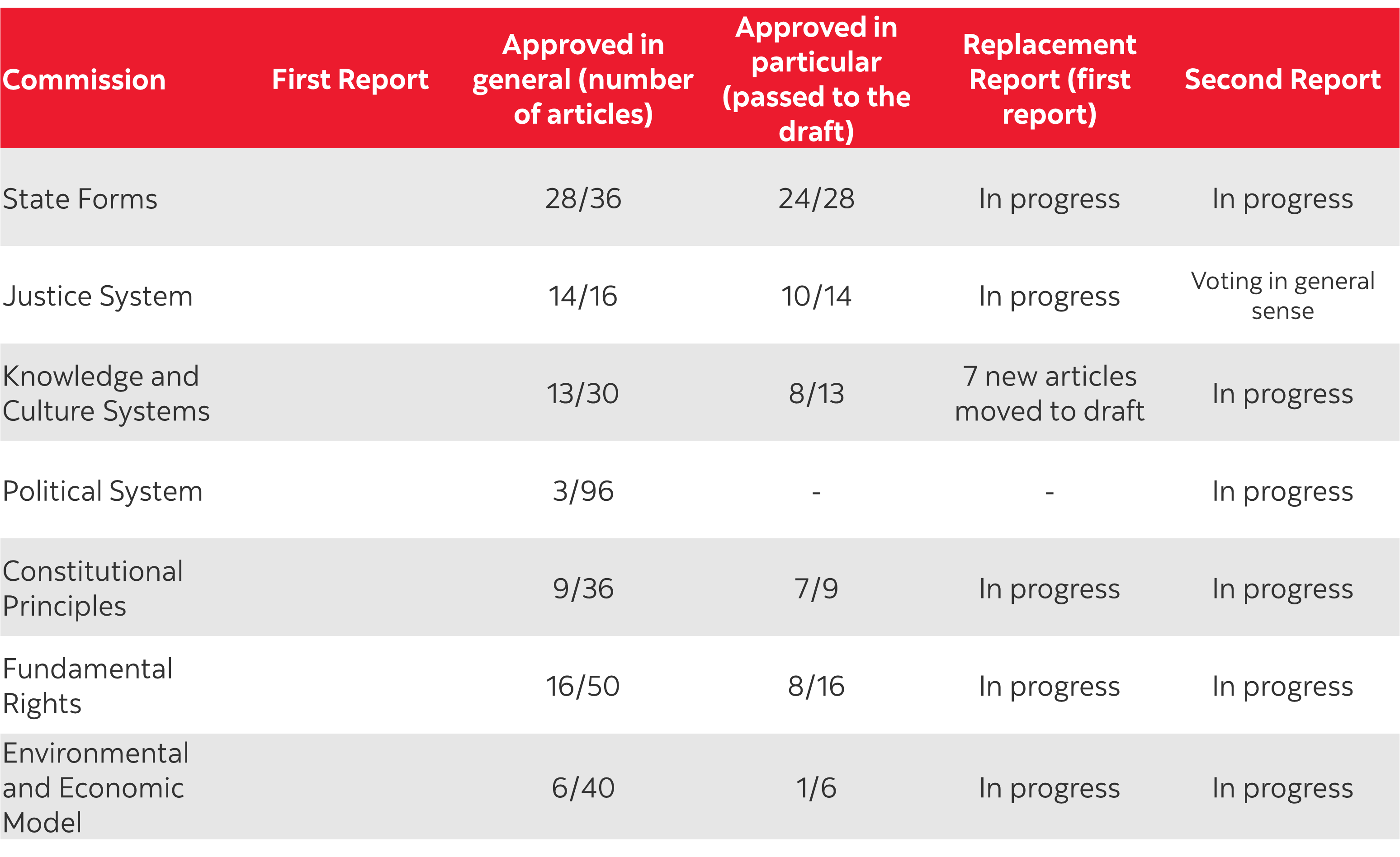

Thematic Commissions

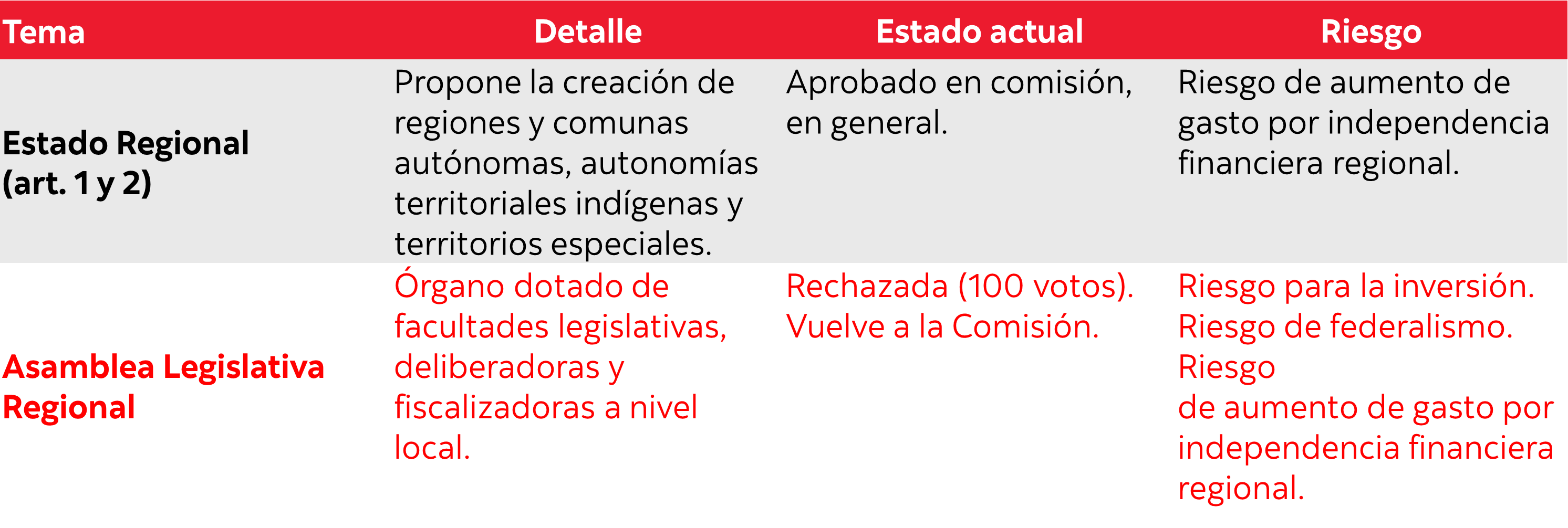

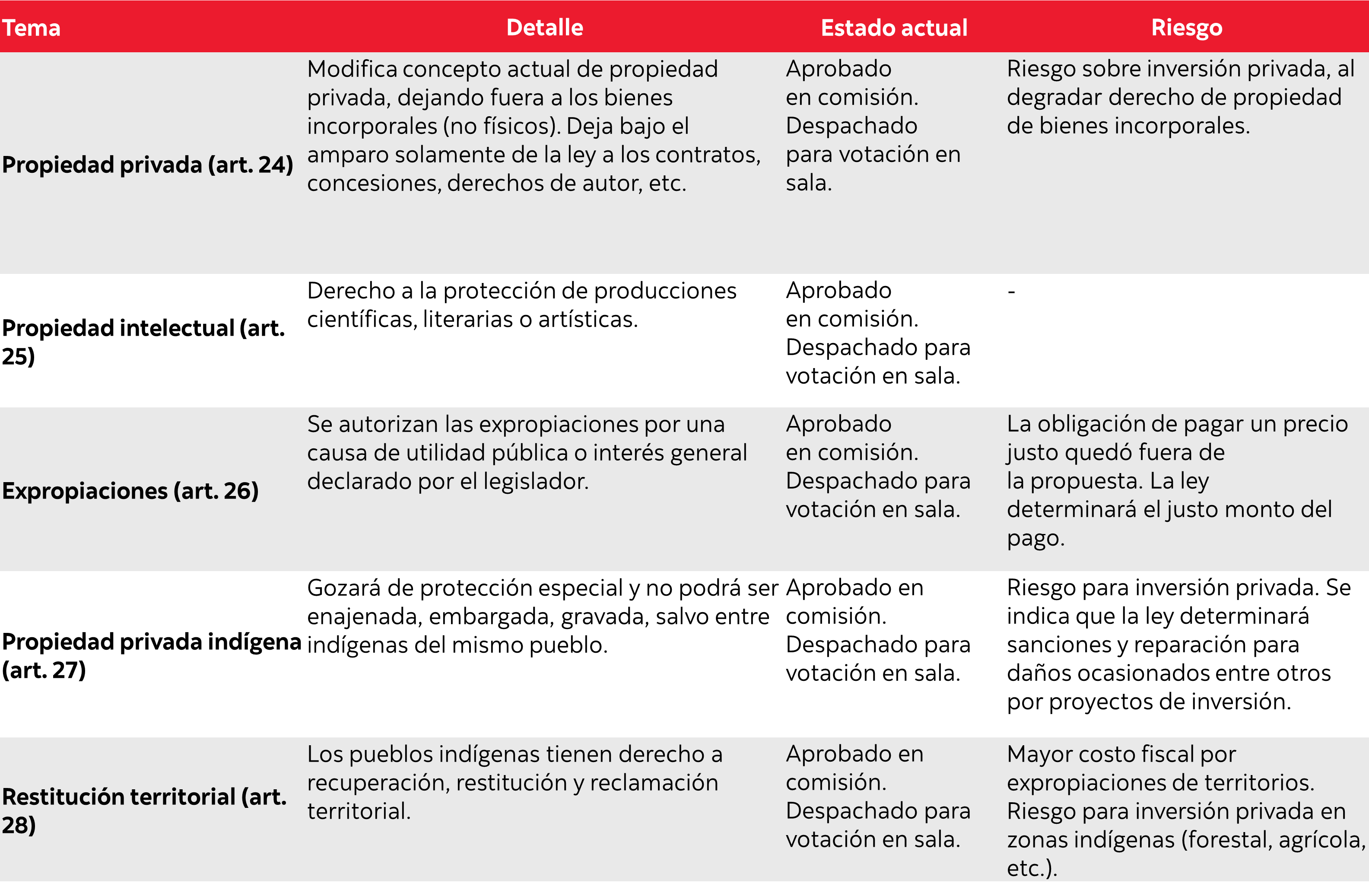

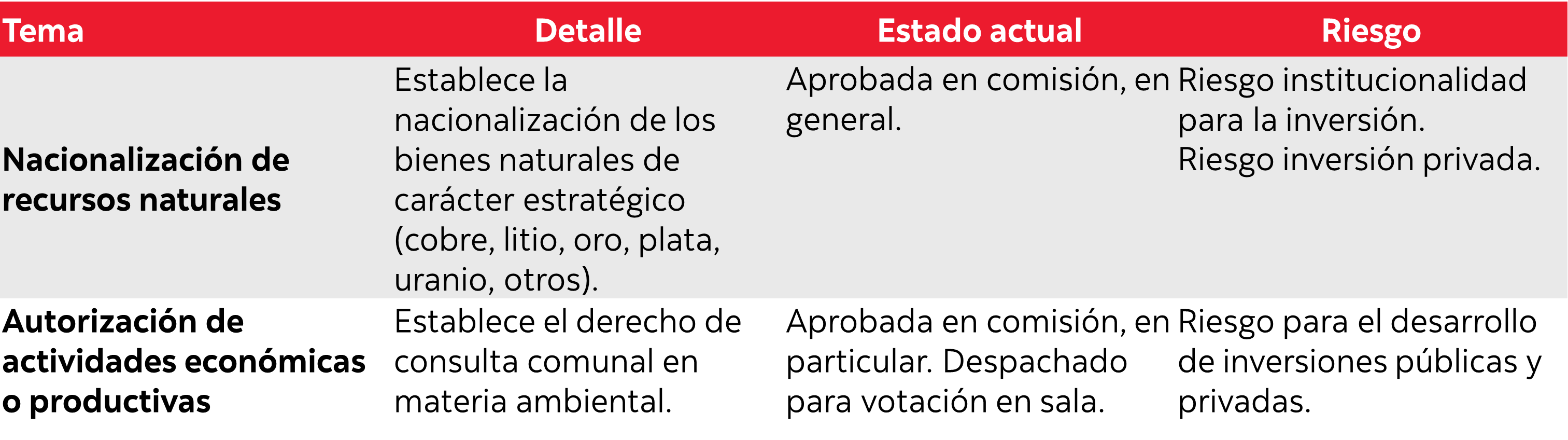

Main risks: Higher government expenditure, lower private investment, increase in labour cost, higher political uncertainty.

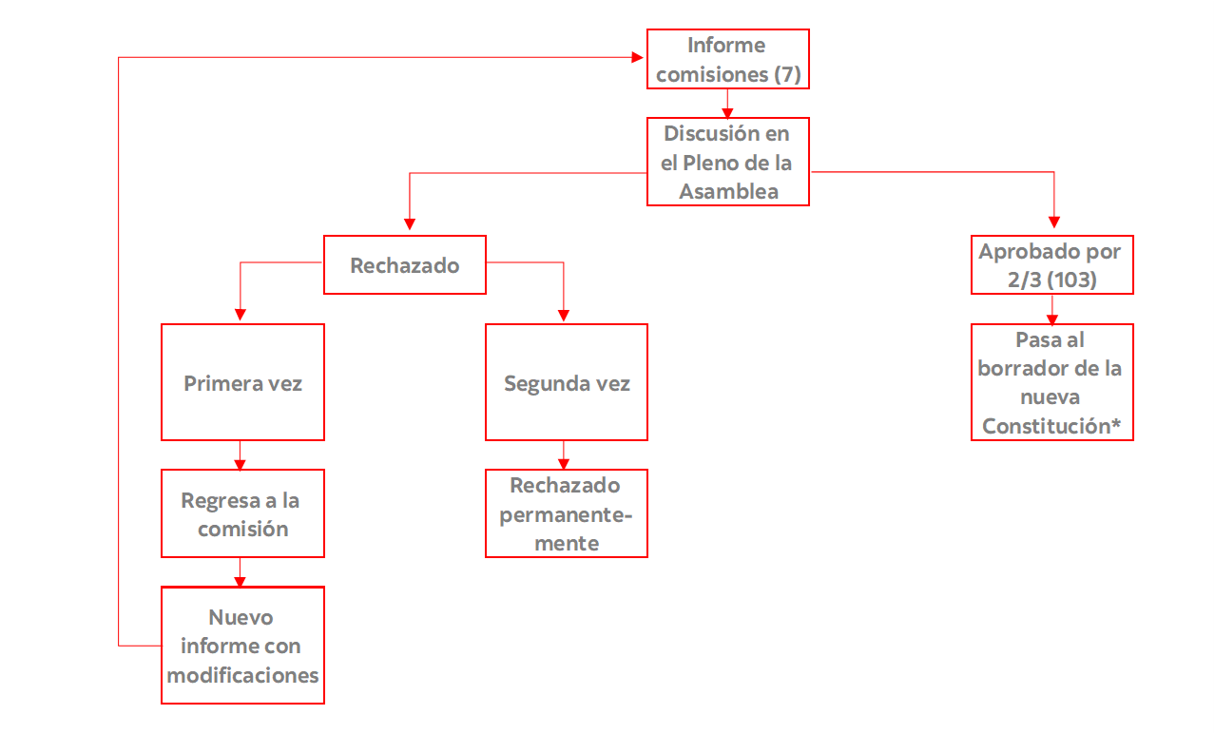

Proceso constitucional

*La Comisión de Armonización asegurará la concordancia y coherencia del Proyecto de Constitución (sesionará desde el 28 de abril al 2 de junio).

2/3 = 103 votos (pasa a borrador para ser armonizada posteriormente). Quórum requerido en el Pleno.

1/2 = 78 votos (se devuelve a la comisión respectiva). Este quorum permite aprobación en general y particular sólo en las comisiones temáticas.

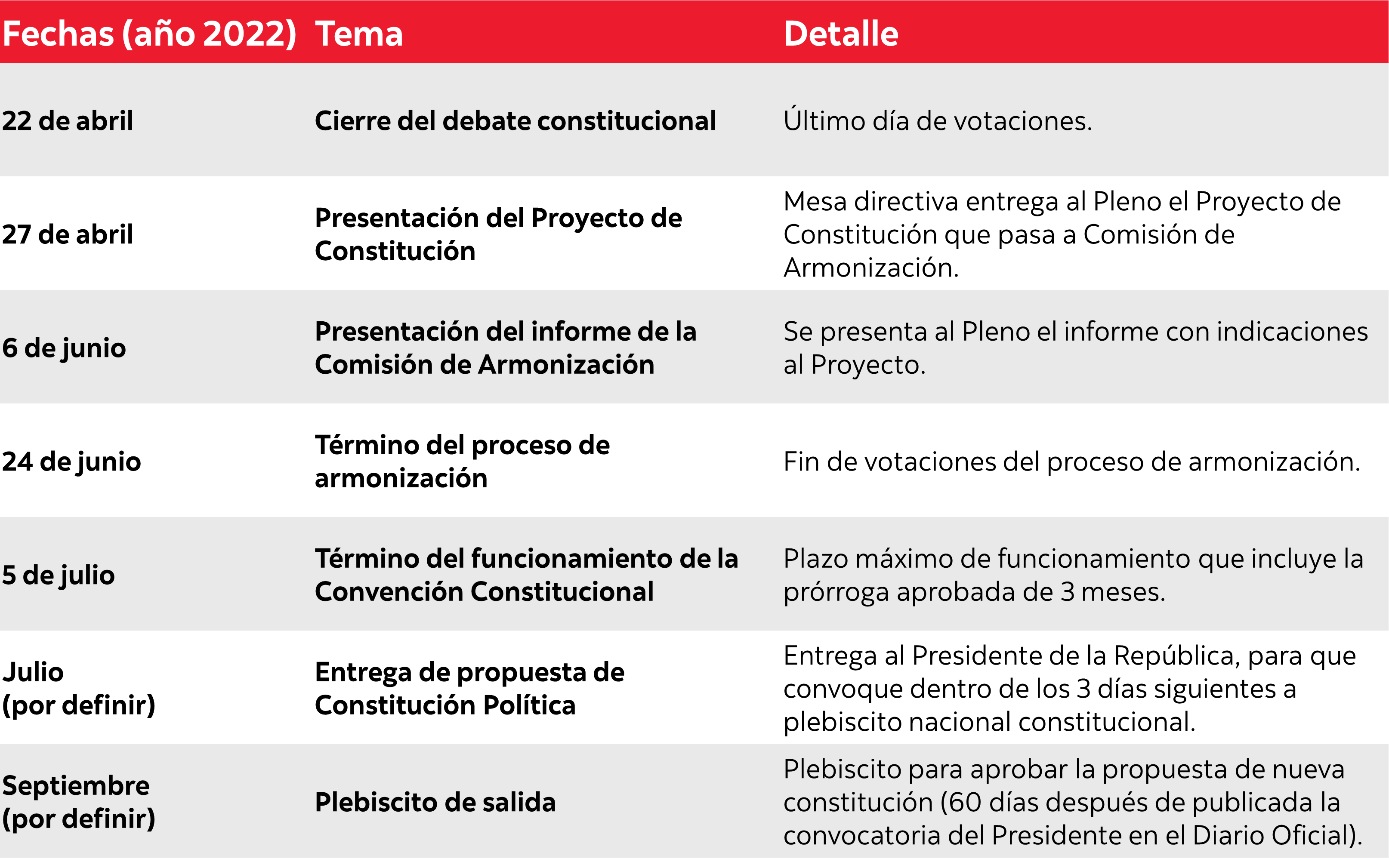

Fechas relevantes

Comisión de Forma de Estado.

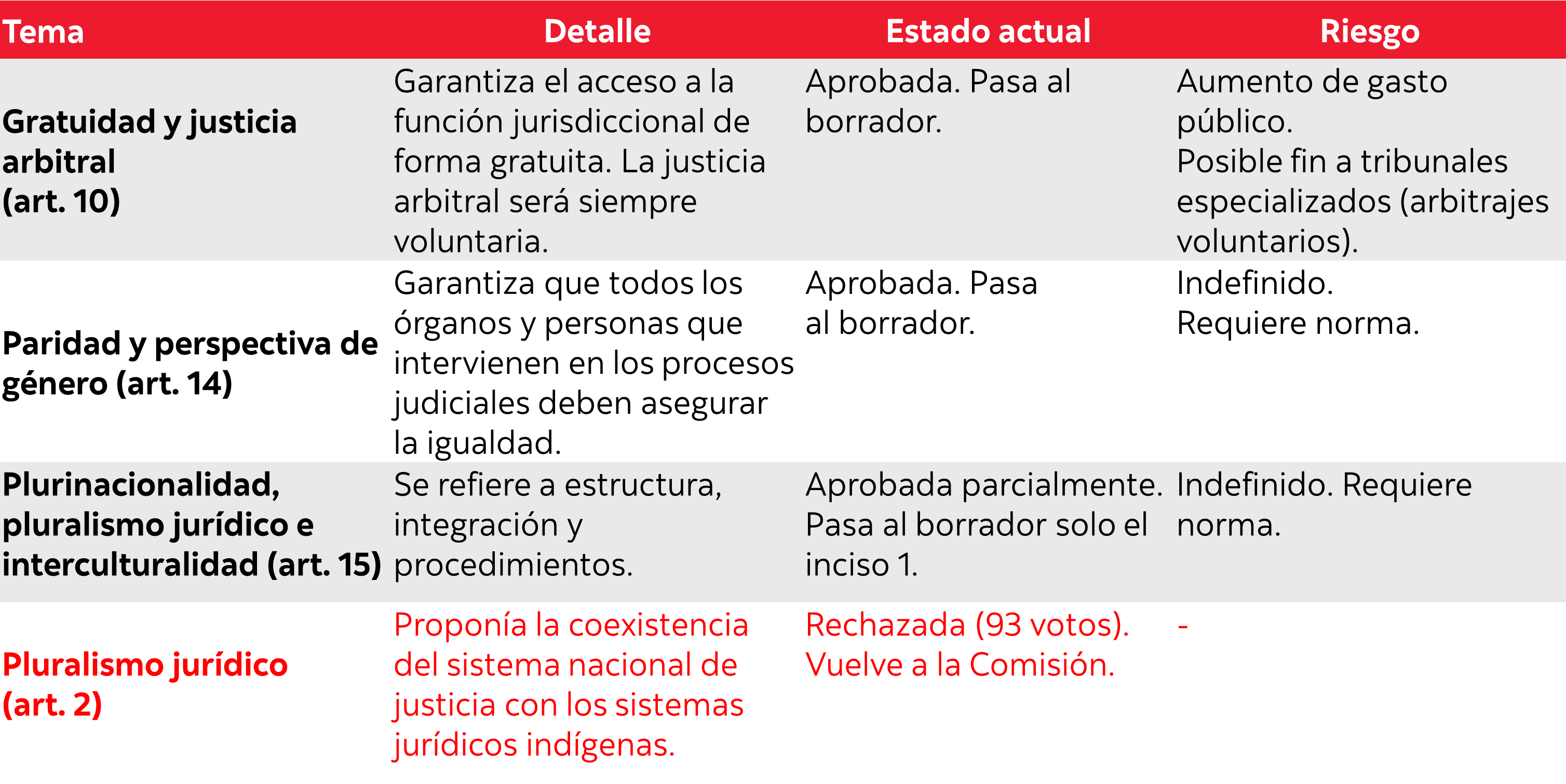

Comisión de Sistemas de Justicia.

Comisión de Sistemas de Conocimientos y Culturas.

Vínculo a Comisión (A la espera de votación en particular en el Pleno)

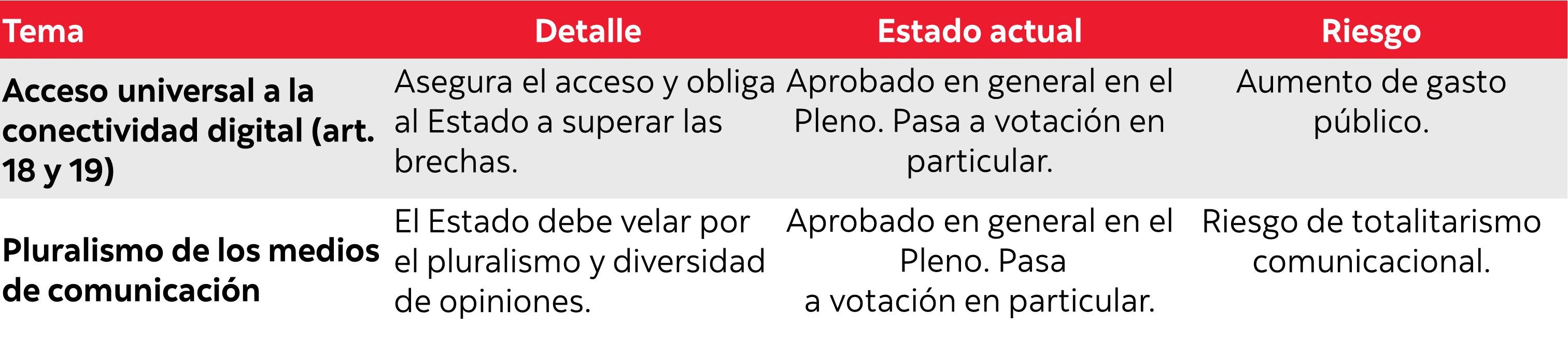

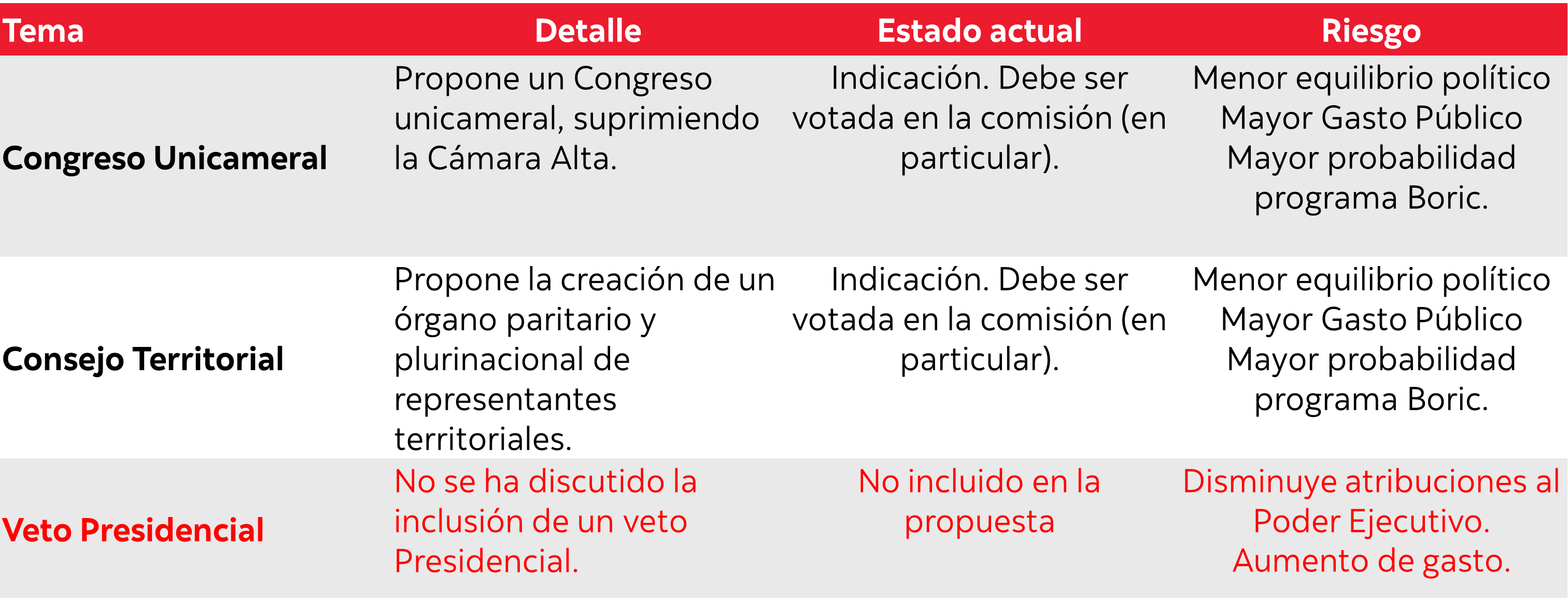

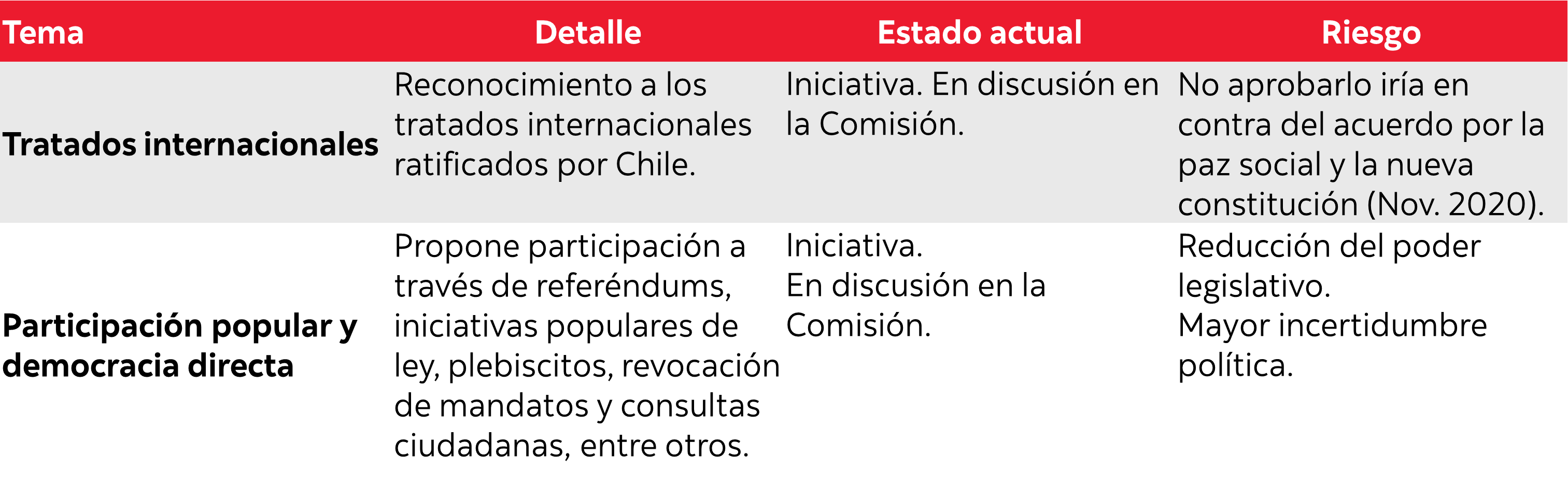

Comisión de Sistema Político.

Vínculo a Comisión (Sigue votación en general en Comisión)

Comisión de Principios Constitucionales.

Vínculo a Comisión (Sigue votación en particular en Comisión).

Comisión de Derechos Fundamentales.

Vínculo a Comisión (Sigue votación en particular en Comisión)

Comisión de Medio Ambiente y Modelo Económico.

Cronograma:

21 feb.-11 mar.: votación en particular sobre Bienes Naturales Comunes

14-25 mar.: votación en particular sobre Modelo Económico.

Vínculo a Comisión (Sigue votación en particular en Comisión)

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.