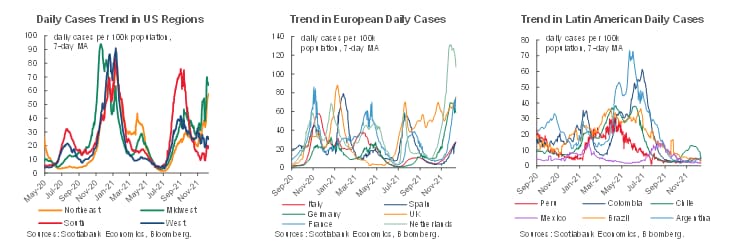

COVID-19: Latam Below G-10 New Case #s

THE LATAM HOTSPOT HAS COOLED

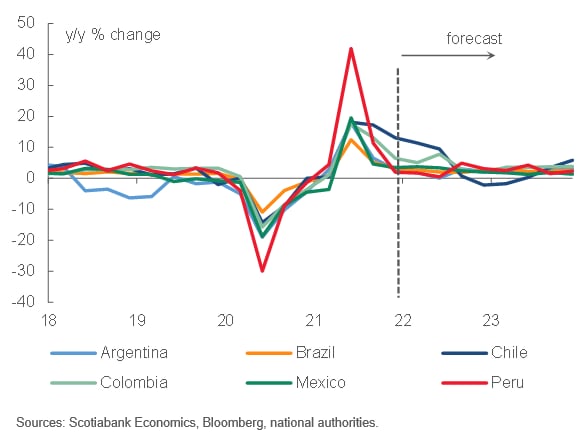

Latam Real GDP Growth Solid into 2022

AR, BR, CL, CO, & PE ALREADY BACK TO PRE-PANDEMIC LEVELS

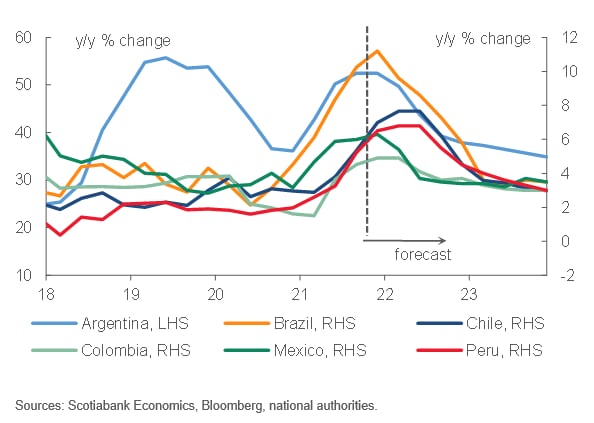

Inflation: Has Risen More than Expected

BIGGEST UPSIDE SURPRISES IN BR, CL, & PE

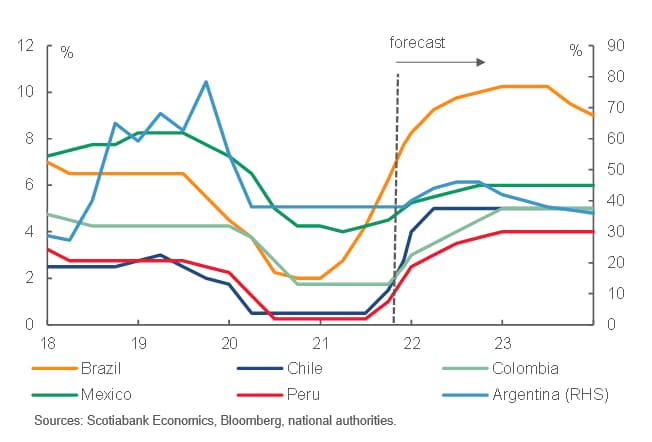

Policy Rates: Topping Out by End-2022

STILL SET TO BE BROADLY ACCOMMODATIVE

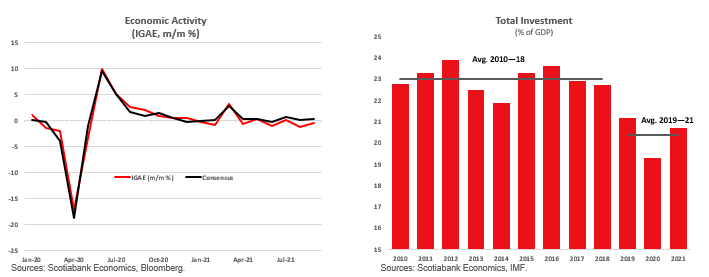

Economists have consistently been too optimistic on Mexican growth in 2021: without greater investment, won’t sustainably see it above 2%.

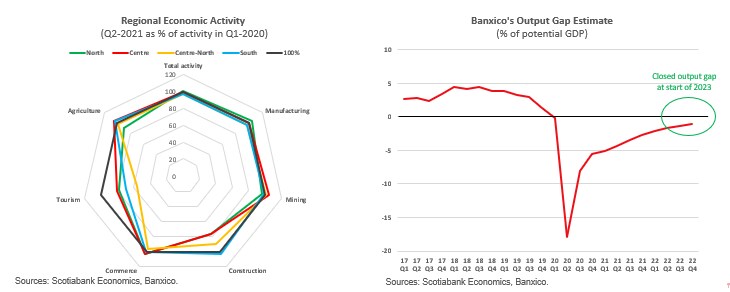

Banxico expects output gap to be nearly shut by end-2022; uneven performance by regions & sectors and spending changes explain some price pressures.

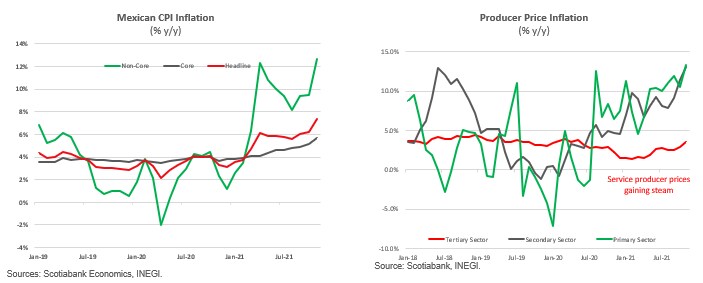

Broad-based inflation shock putting pressure on Banxico; goods driving the shock. Services inflation kicking in as 2021 winds down.

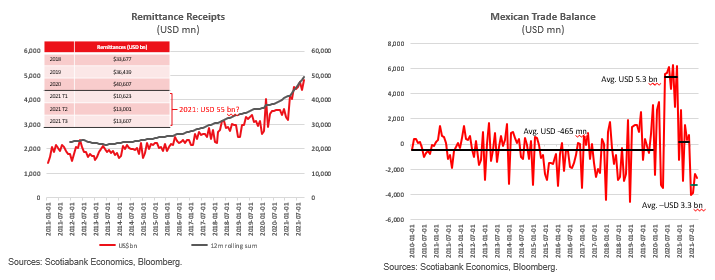

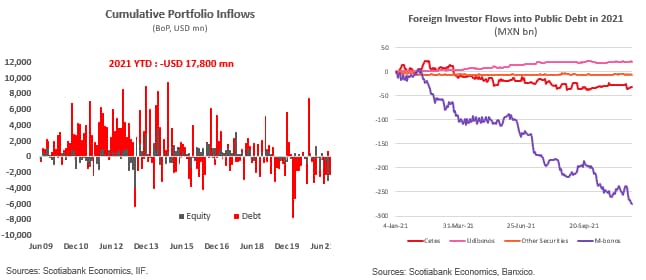

MXN has been propped up by trade & remittances… tourism recovery is key for support going forward.

Capital flows have been a one-way street. Positioning much cleaner, but risks remain.

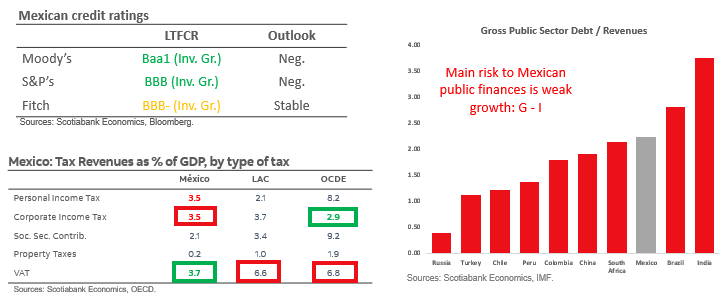

Loss of IG looks difficult in next 12 months; long-term fiscal sustainability affected by growth outlook.

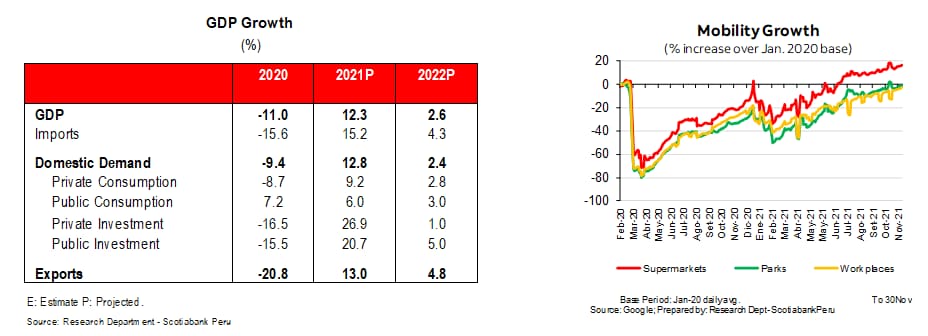

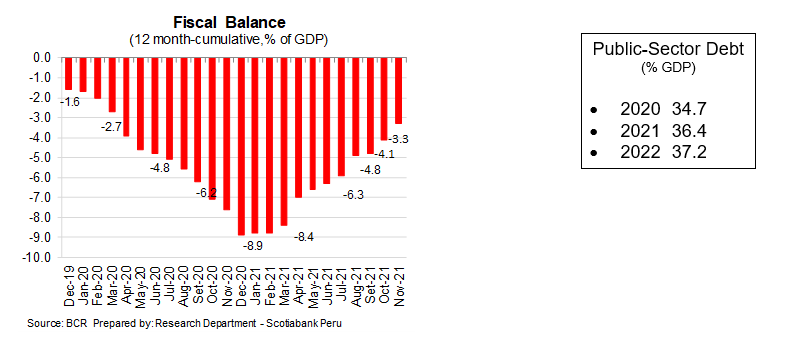

Peru’s state of affairs going into 2022

- Macro balances are strong

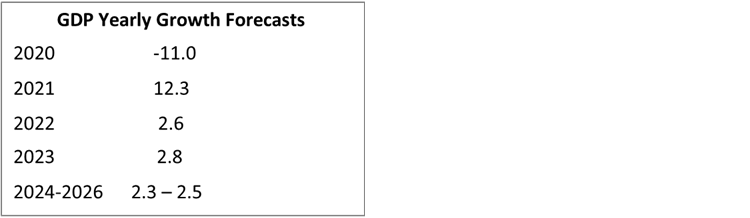

- Surprisingly robust growth

- Resilience in the face of uncertainty

- COVID-19 cases are near their lows

- FX and capital outflows reflect uncertainty

- Government instability

- Policy confusion

- Social conflicts

- Inflation

- 2022 will continue to be politically noisy and challenging

- Terms of risk have shifted from radicalism to underperformance, poor State management and an erratic decision-making process

Investment will be key in 2022

- Peru GDP is at pre-COVID-19 levels

- Recent indicators do not show evidence of politics affecting growth

- Economic management is more institutionalized and mainstream

Macro balances are robust

- Peru’s credit agencies: political concerns versus improving macro balances

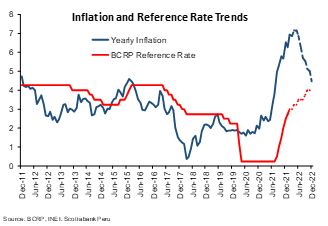

Inflation is a growing concern

- Our inflation forecasts:

- 2021: 6.5%

- 2022: 4.5%

- We expect the BCRP to raise to 2.50% by year end, and to 4.0% in 2022

- Inflation is affecting purchasing power and risks weakening the government further

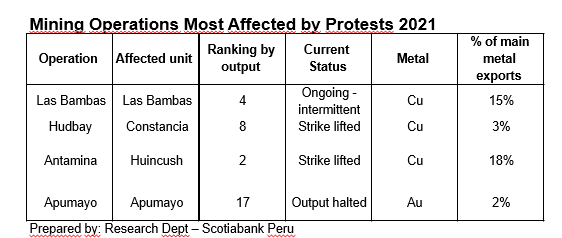

Social conflicts are having a real impact on mining

- Property and predictability of contract and legal matters are a risk

- Government stance favours social conflicts

- Cabinet conflicted over mine closures (Francke vs Vásquez)

- Protests in recent months at mines that represent 38% of Peru’s copper exports

- Also:

- Zinc (Cerro Lindo; 12% of zn output)

- Gold/silver mines (Apumayo, et. al; +7% of au/ag output)

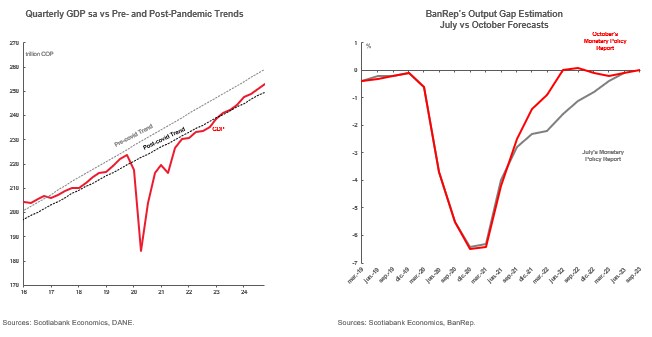

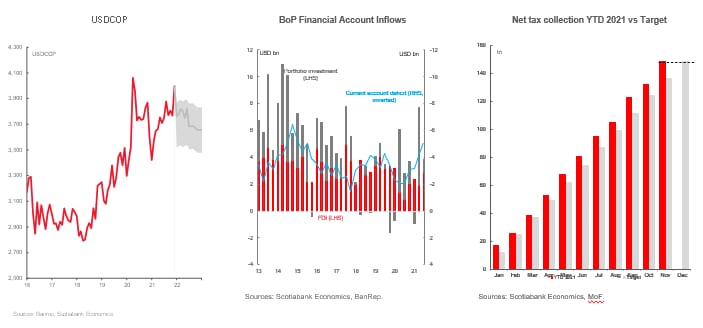

In Q3-2021, Colombia surpassed its pre-pandemic production levels; growth should approach 10% y/y for all of 2021. BanRep expects output gap to close by mid-2022.

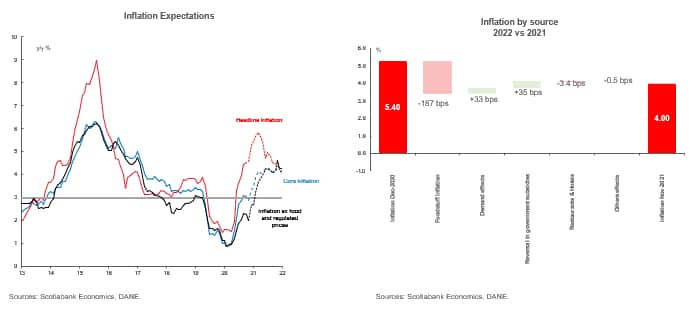

Despite supply shocks being temporary, indexation should extend CPI inflation. Reversion should start in H2-2022, but risks remain that headline closes 2022 above 3% y/y.

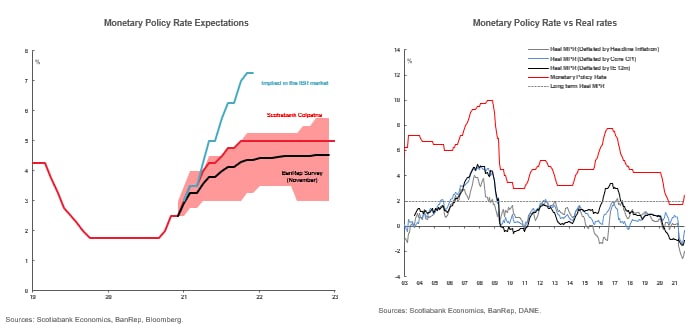

BanRep set to continue more aggressive-than-normal hiking cycle; neutral rate should be reached by mid-2022. IBR market pricing an even higher terminal rate.

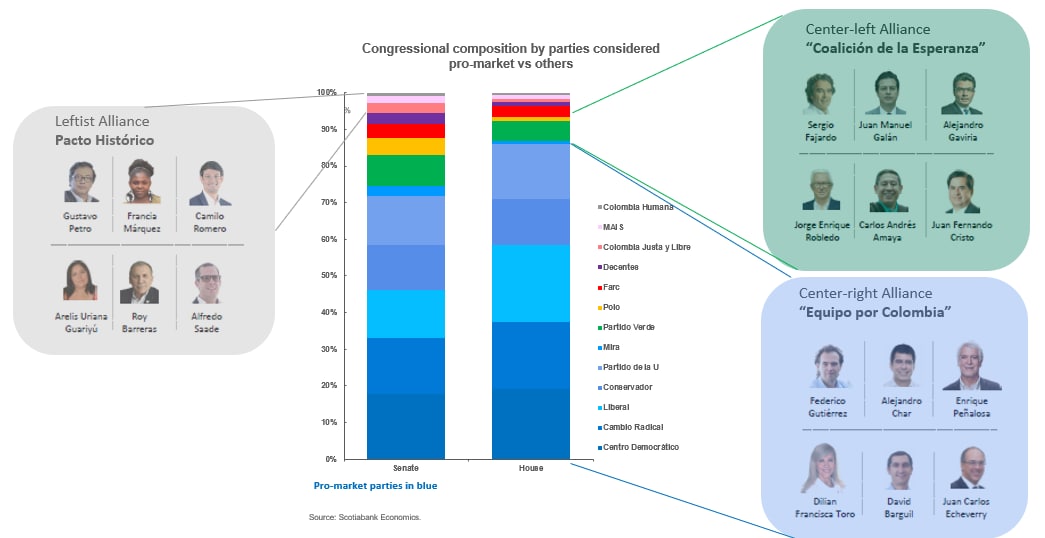

Elections in 2022 are a source of uncertainty. Congressional elections are the first milestone. Strong institutions will prevail.

FX market could remain under pressure owing to higher external deficit and political uncertainty; positive macroeconomic news may be discounted.

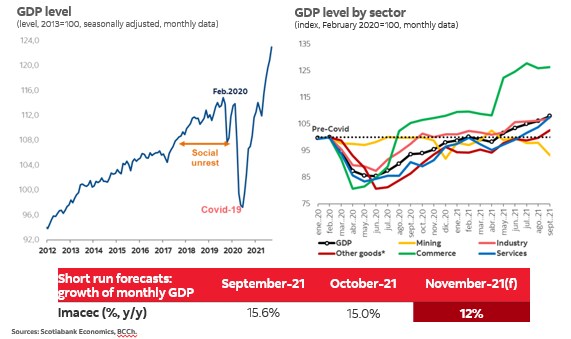

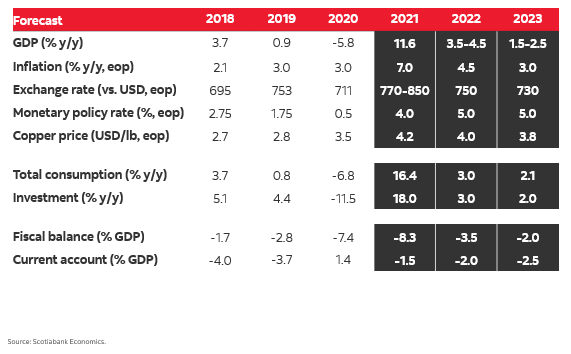

Imacec expanded 15% y/y in October (0.8% m/m) driven by service sectors. GDP growth should reach 11.6% y/y in 2021 and 4.5% y/y in 2022. We estimate that Imacec expanded 12% y/y in November.

Private consumption remains high after three pension fund withdrawals (USD 50 bn) and a strong fiscal impulse. Liquidity is normalizing, but there is still an extra USD 20 bn in chequing and debit accounts that (we project) will last until mid-2022 (at least).

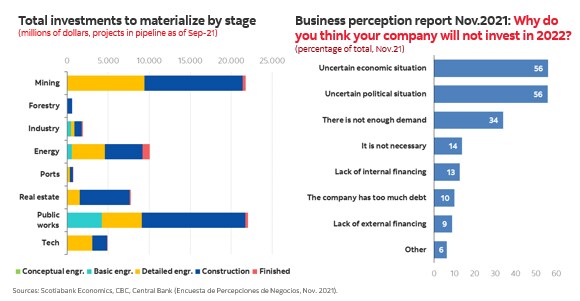

As of September 2021, investment projects in the pipeline for the period 2021–25 reached USD 69.8 bn (54% in construction stage). Investment dynamics depend on the materialization of large projects in mining (public and private) and public works.

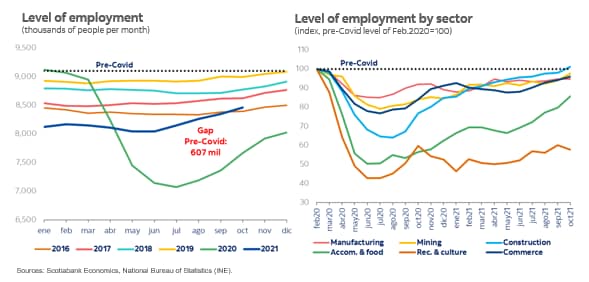

The employment gap vs pre-pandemic levels has shrunk to -607k. By economic sector, job creation has been led by commerce, which has added +28k jobs. The construction sector has also recovered its pre-COVID-19 levels of employment.

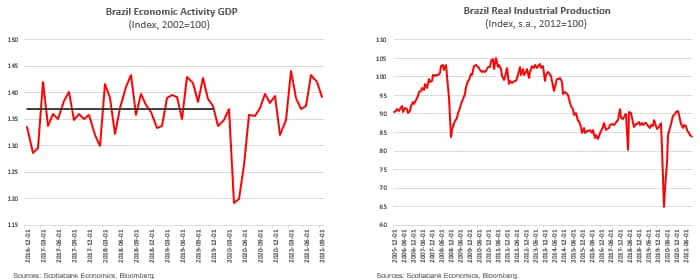

Economic Outlook

Recovery is getting back to pre-pandemic levels, but some sectors have not recovered pre-Dilma benchmarks

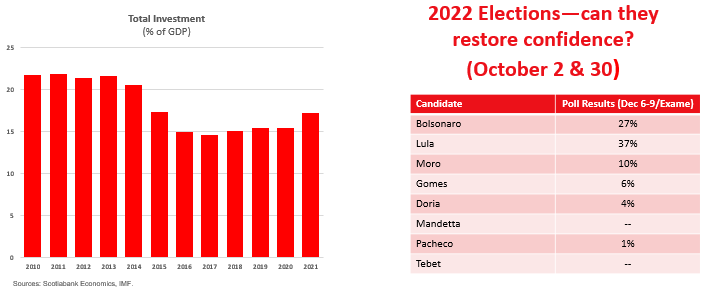

Key to economic weakness = investment.

Can elections restore it?

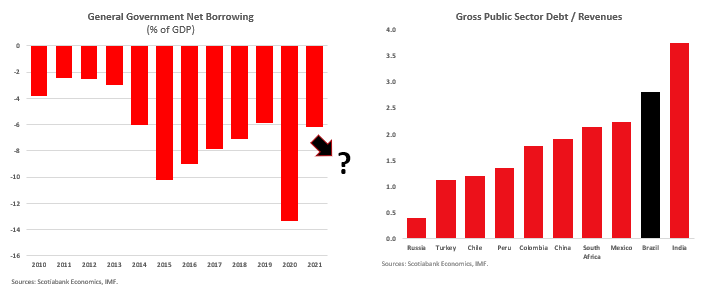

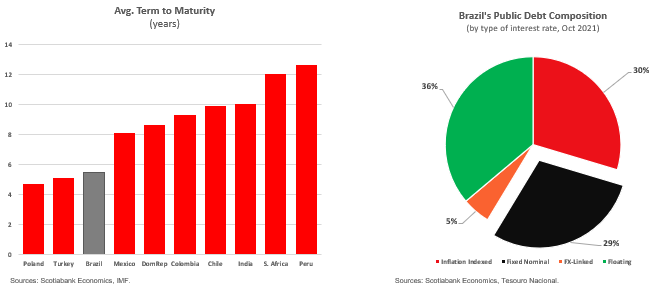

Fiscal deterioration returned with COVID-19 pandemic. Brazil’s high revenue base both a strength and weakness.

Debt composition key element of Brazil’s fiscal vulnerability, makes country sensitive to rising rates

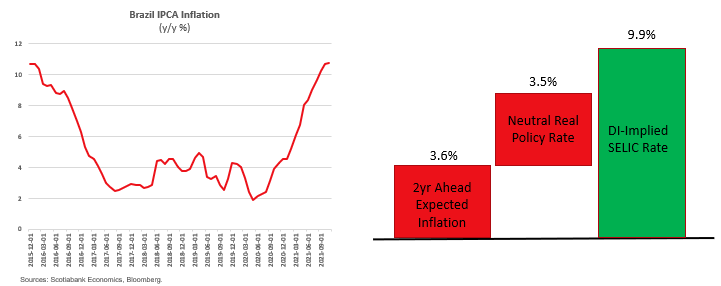

Is aggressive BCB tightening driving an inflection point?

Goods inflation dominates the BCB’s headaches…

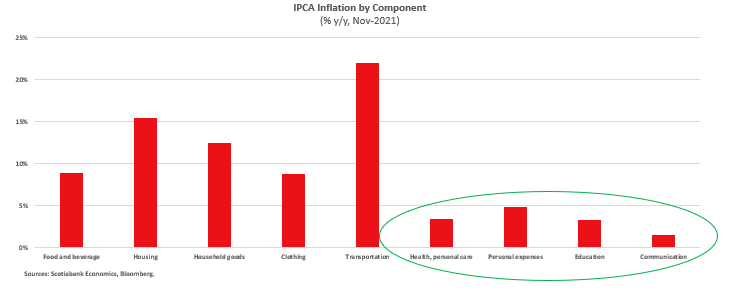

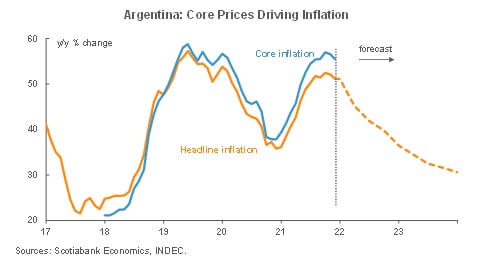

Inflation: Deep in the Core

PRICE GAINS CONTINUE TO HAVE HIGH BREADTH

Inflation: Little Change, as Expected

MONTHLY INFLATION STILL AT 2.5% M/M

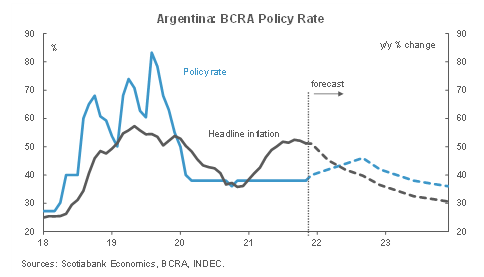

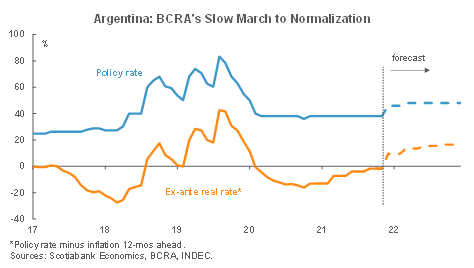

Monetary Policy: A Long Way to Hawkish

REAL RATES SET TO CRAWL OUT OF NEGATIVE TERRITORY

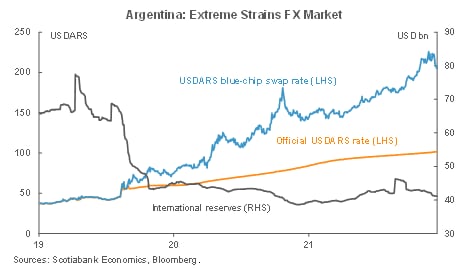

FX: ARS Awaits the IMF

UNIFICATION OF CURRENCIES WILL BE PAINFUL

Keep in Touch

www.scotiabank.com/economics

scotia.economics@scotiabank.com

@ScotiaEconomics

DISCLAIMERS

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including, Scotiabanc Inc.; Citadel Hill Advisors L.L.C.; The Bank of Nova Scotia Trust Company of New York; Scotiabank Europe plc; Scotiabank (Ireland) Limited; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Scotia Inverlat Casa de Bolsa S.A. de C.V., Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorised by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorised by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V., and Scotia Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.