Key Points

2021 growth outlook looks quite strong but may not be sustainable:

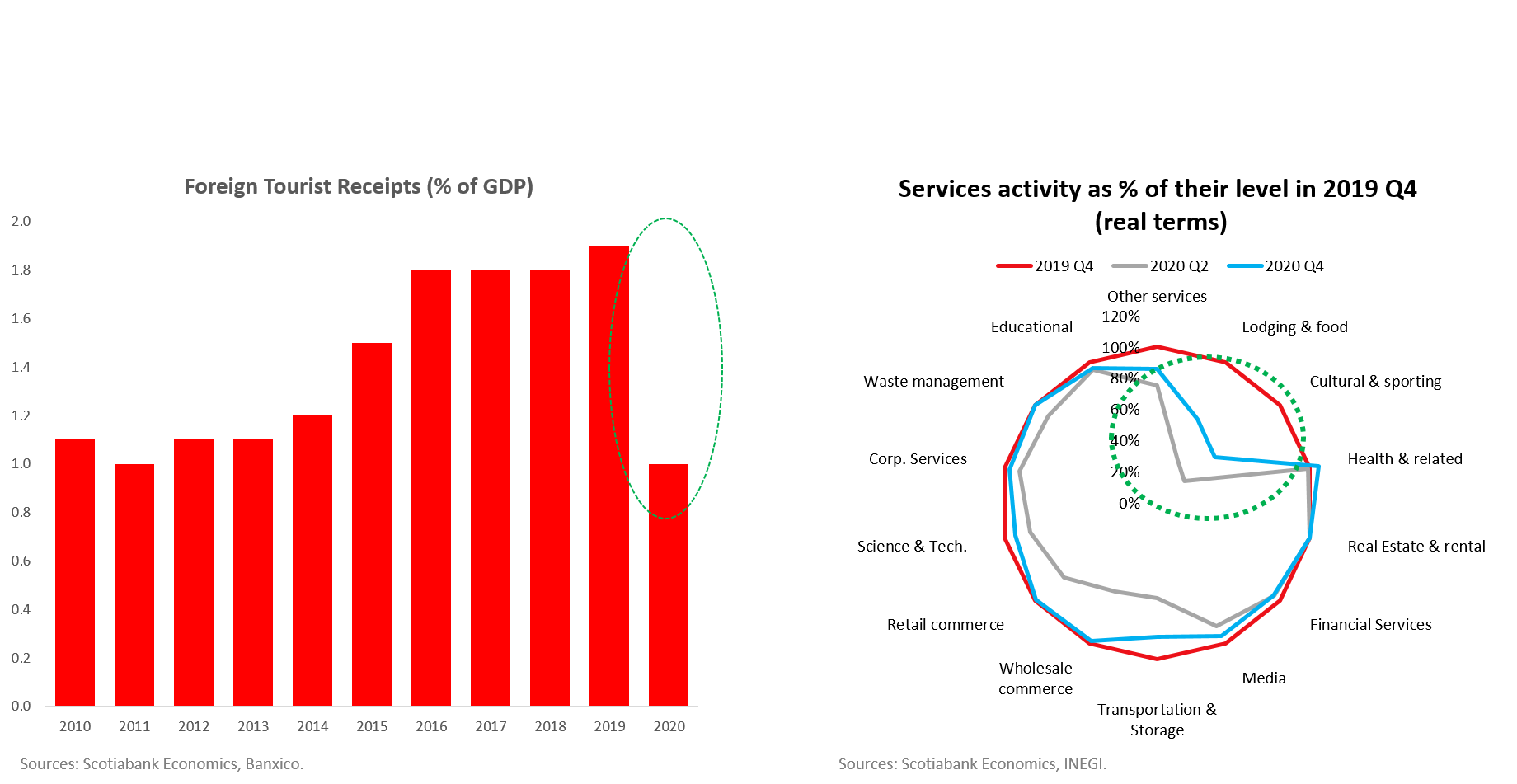

Re-opening of services sector to boost tourism & entertainment

Record remittances from the US helping prop up consumption

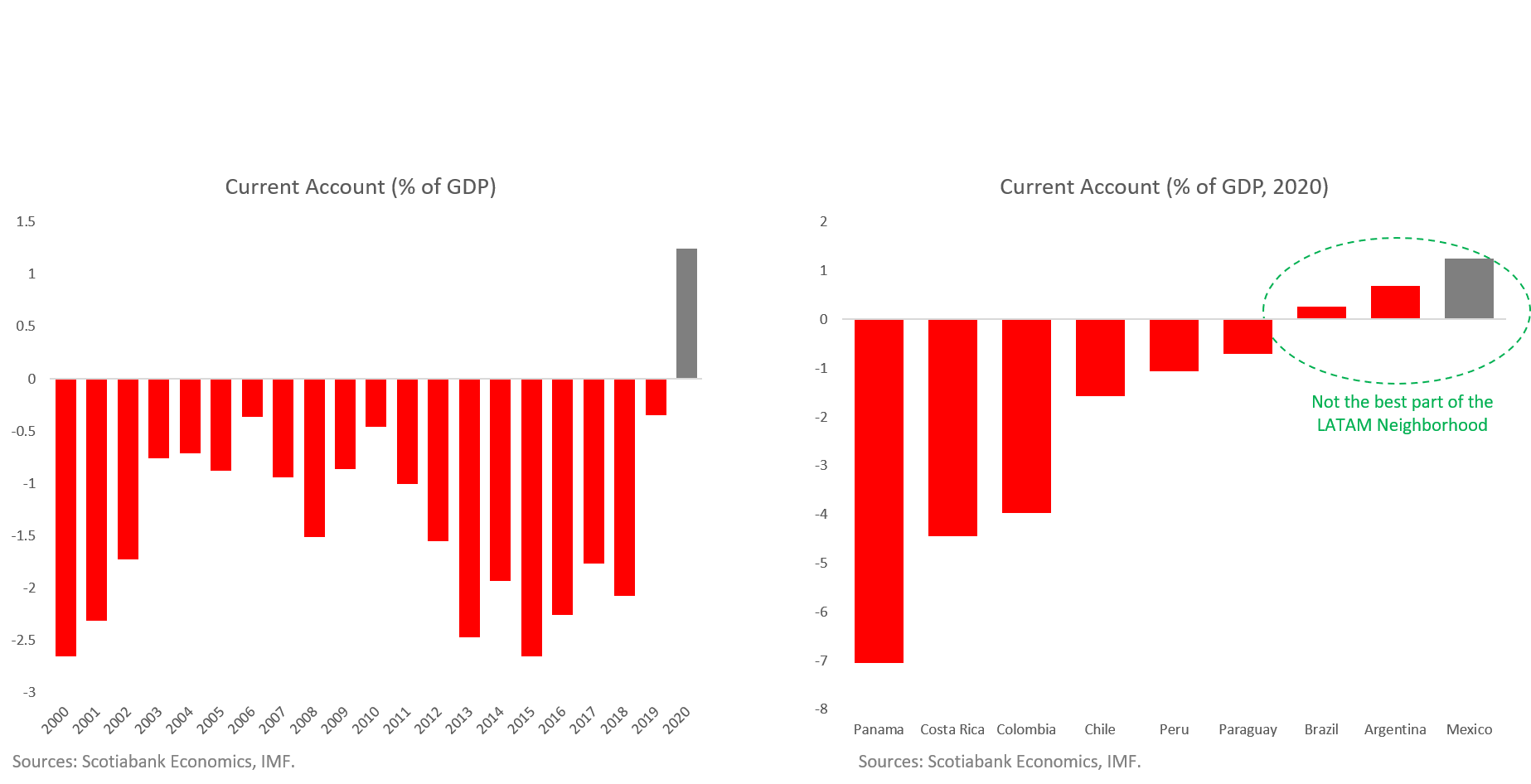

- Record trade surplus—with a jump in net exports—due in large part to weak domestic demand

Main problem for the “4th Transformation” is self-inflicted decline in confidence:

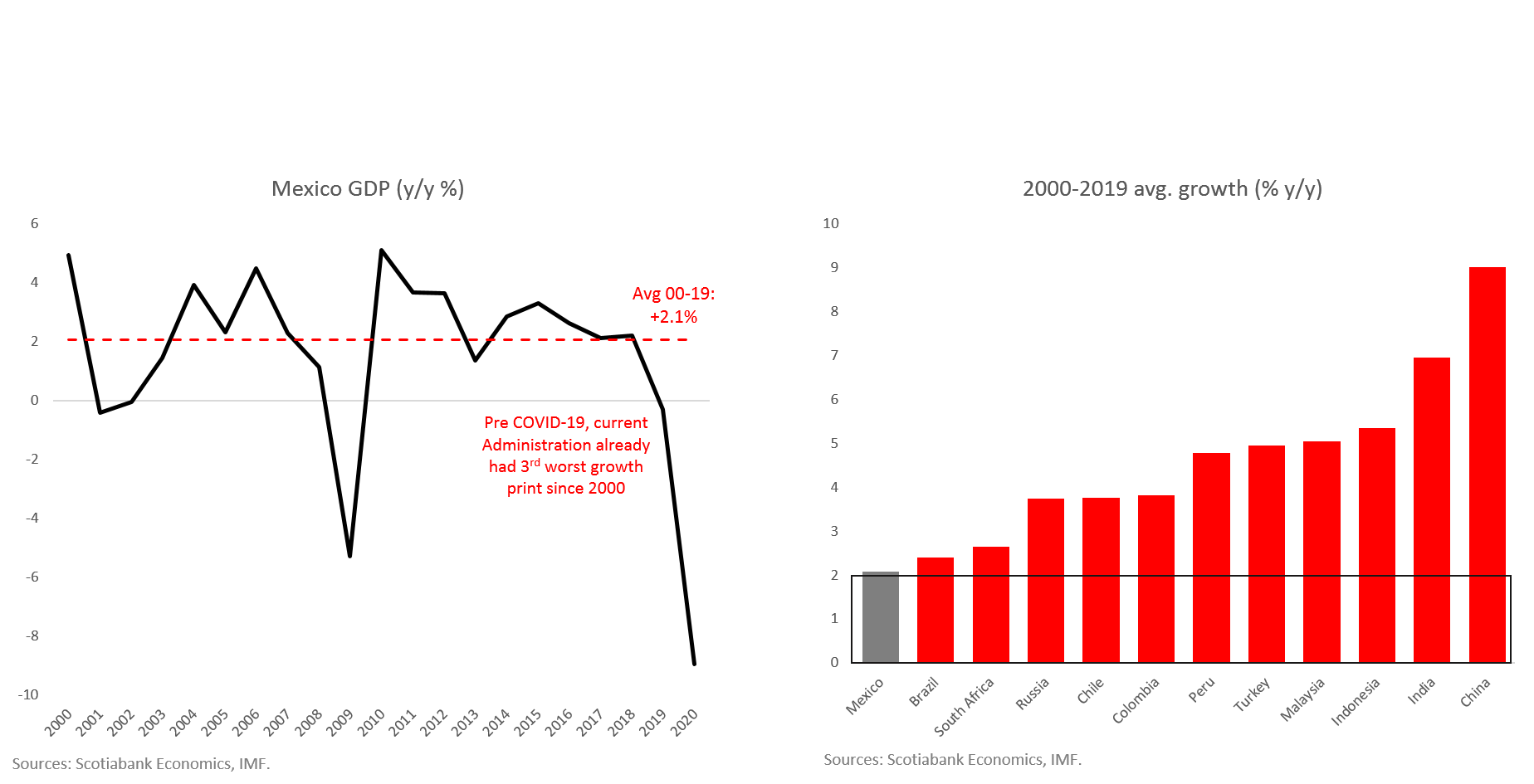

Growth was already weak historically (2.1% 20 yr. avg.)

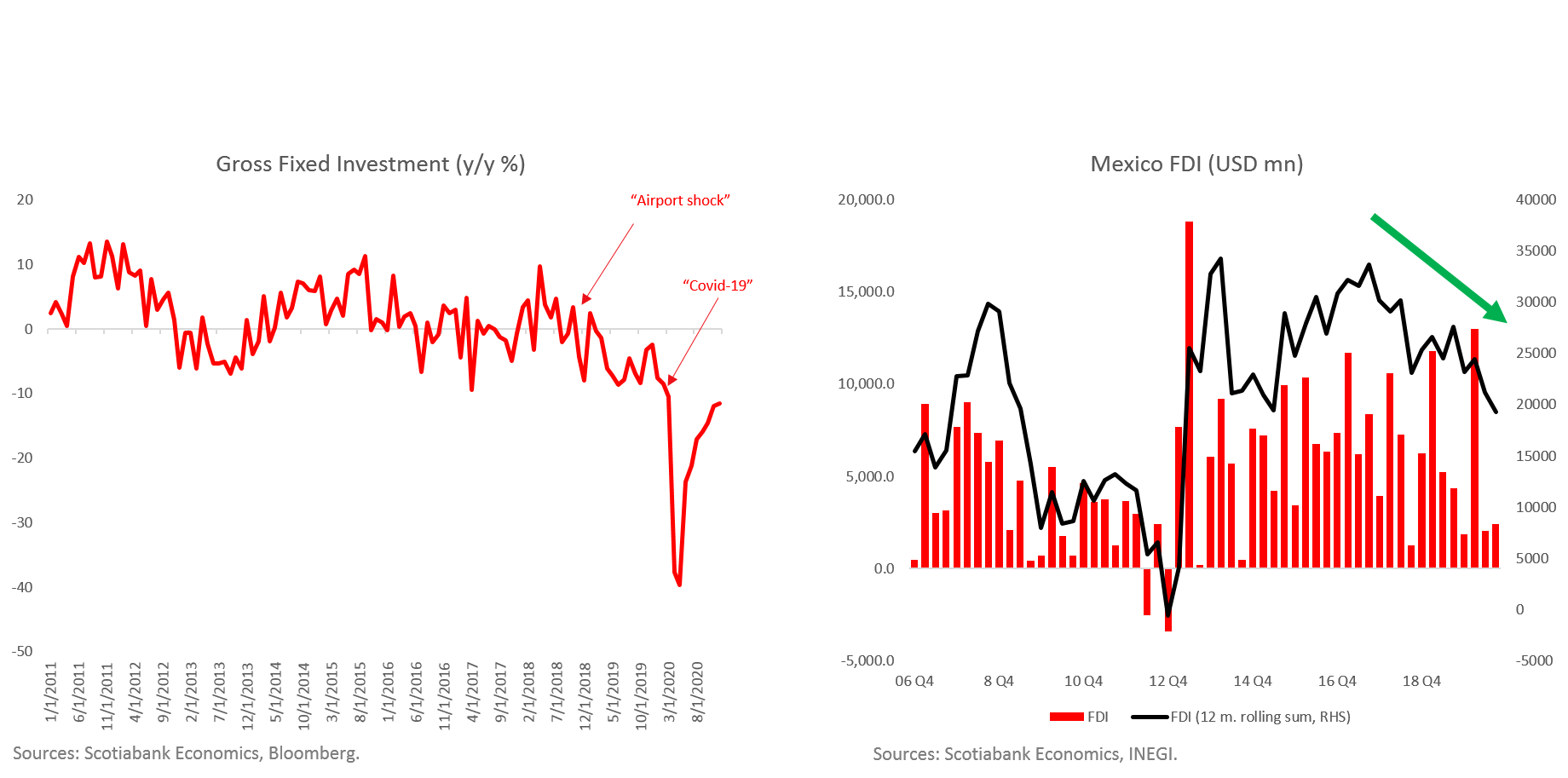

Texcoco Airport cancellation & uncertain business environment reduced investment

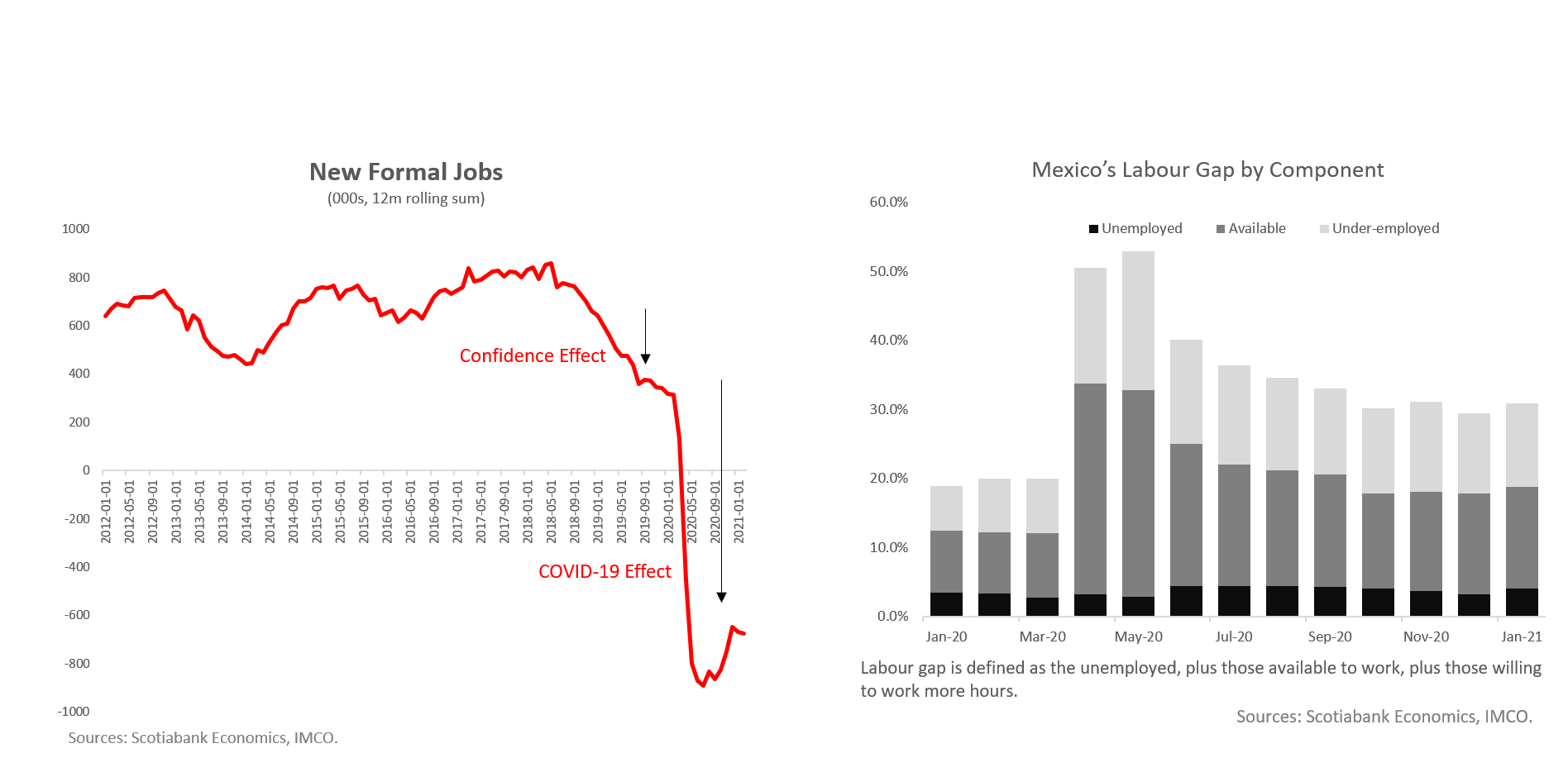

With weakening investment came lower employment creation

- “Mexico costs” are rising

Weaker growth outlook in turn spells trouble for public finances:

Permanent Primary Surplus analysis suggests tax reform or growth boost are necessary

Add Pemex trouble to the mix

- How will the 2022 tax reform impact investment?

Despite all this, Morena still popular with voters:

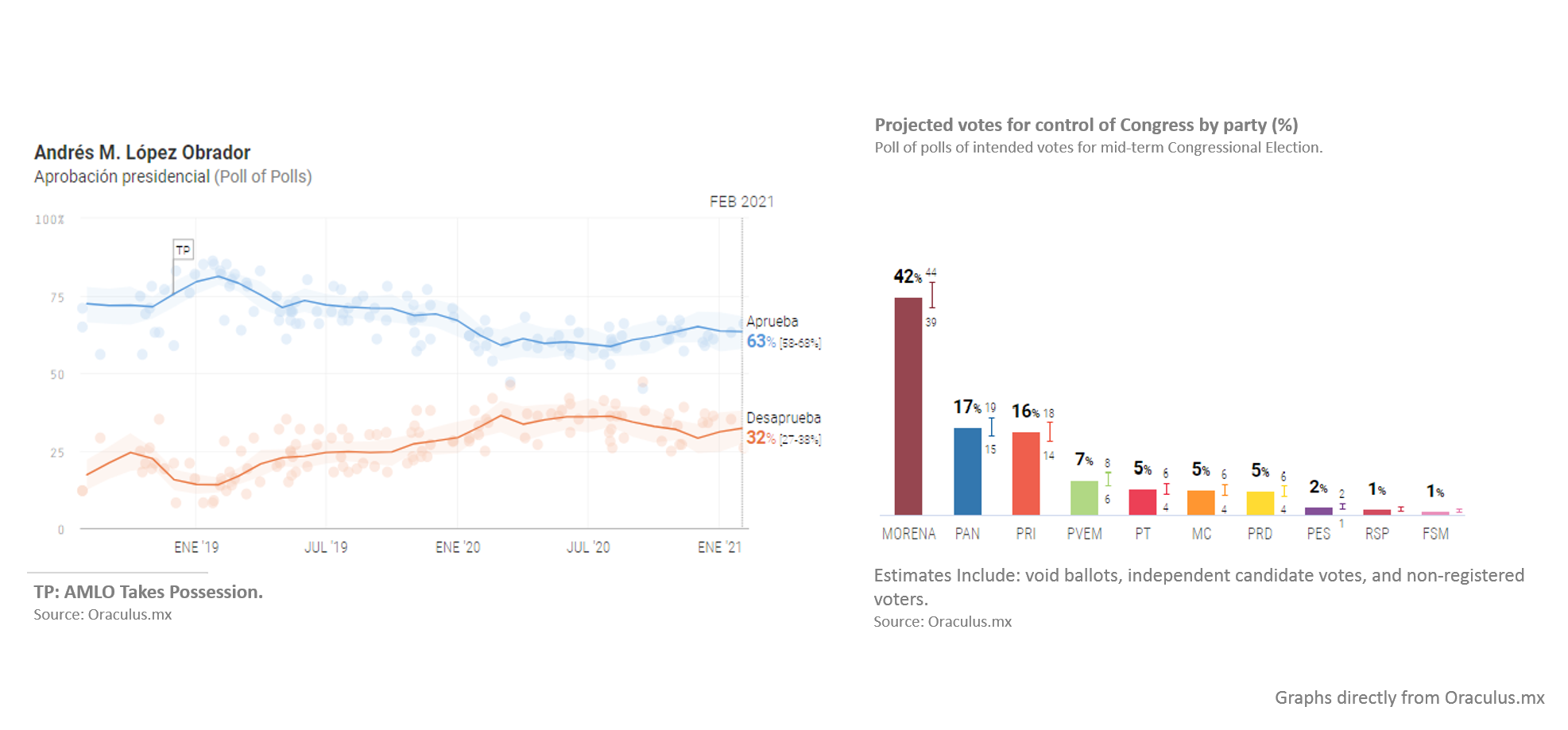

AMLO approval rebounding, approaching 2/3

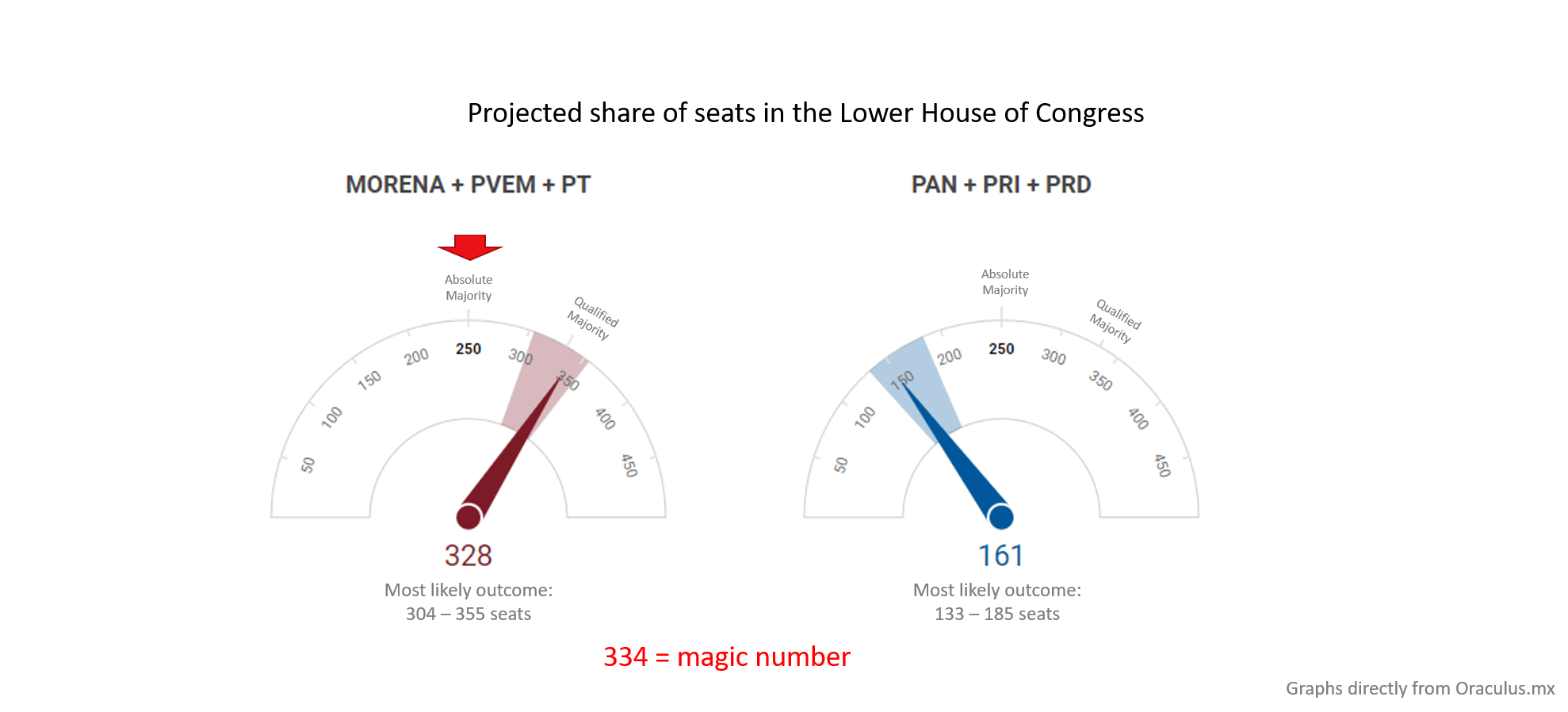

Clever election tactics + weak opposition suggest at least absolute majority in Congress for Morena

2/3 (Constitutional) majority may be in the cards for AMLO H2

First some good news: 2021 growth looks solid

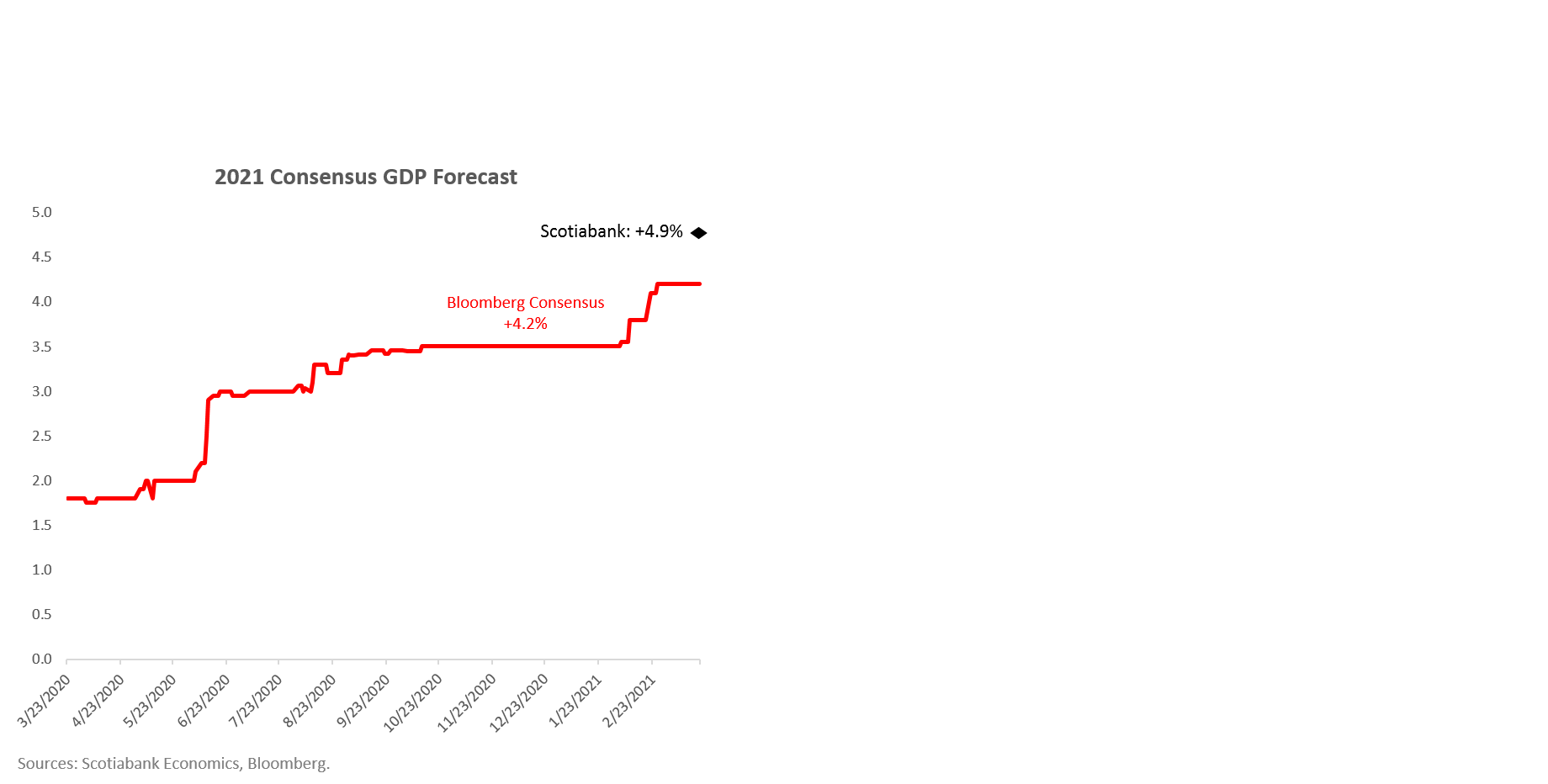

2021 growth forecasts have been rising:

Consensus +4.2%

Banxico +4.8%

Scotiabank +4.9%

FinMin +5.0-5.5%

Base effects / vaccination should drive a big jump in 2021 GDP; particularly in tourism

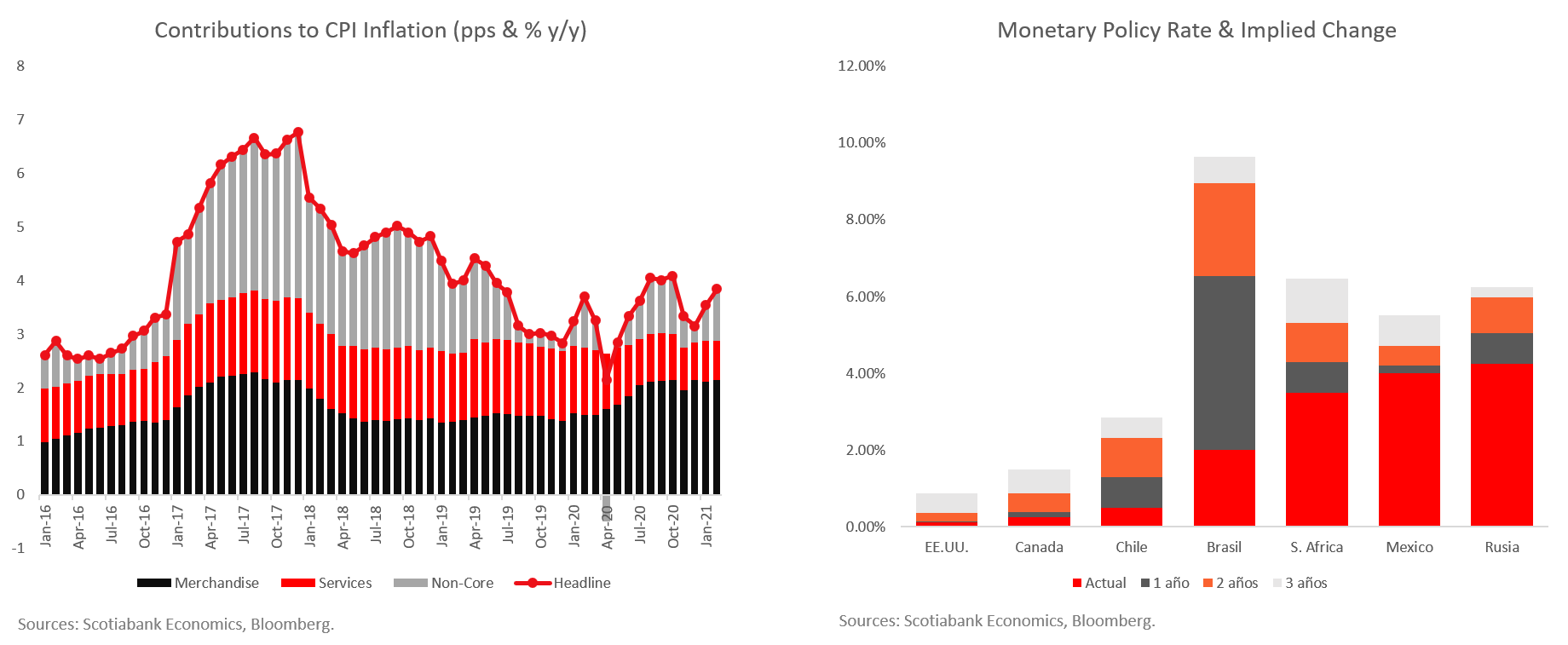

Re-opening to cause services price shock?

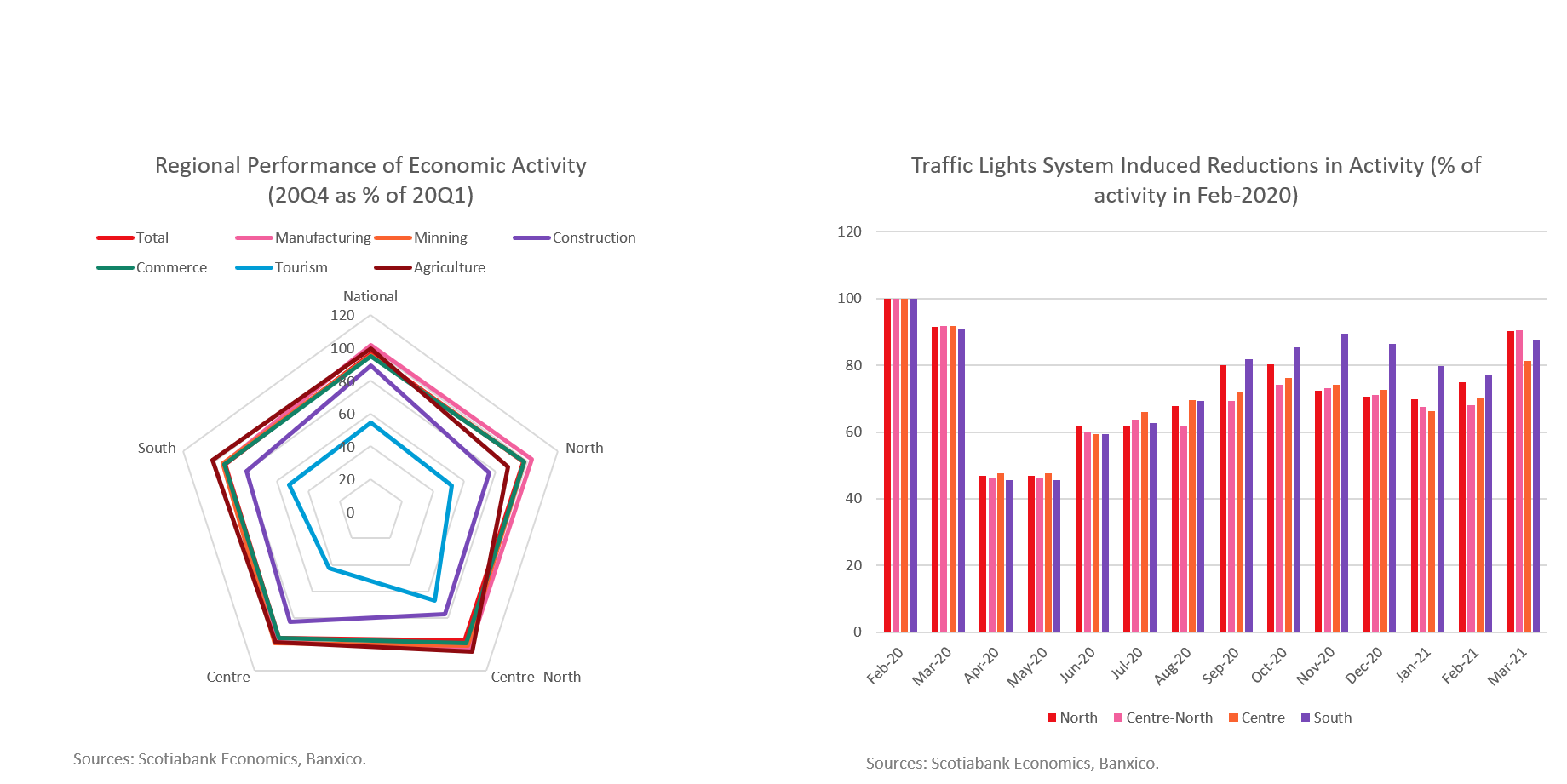

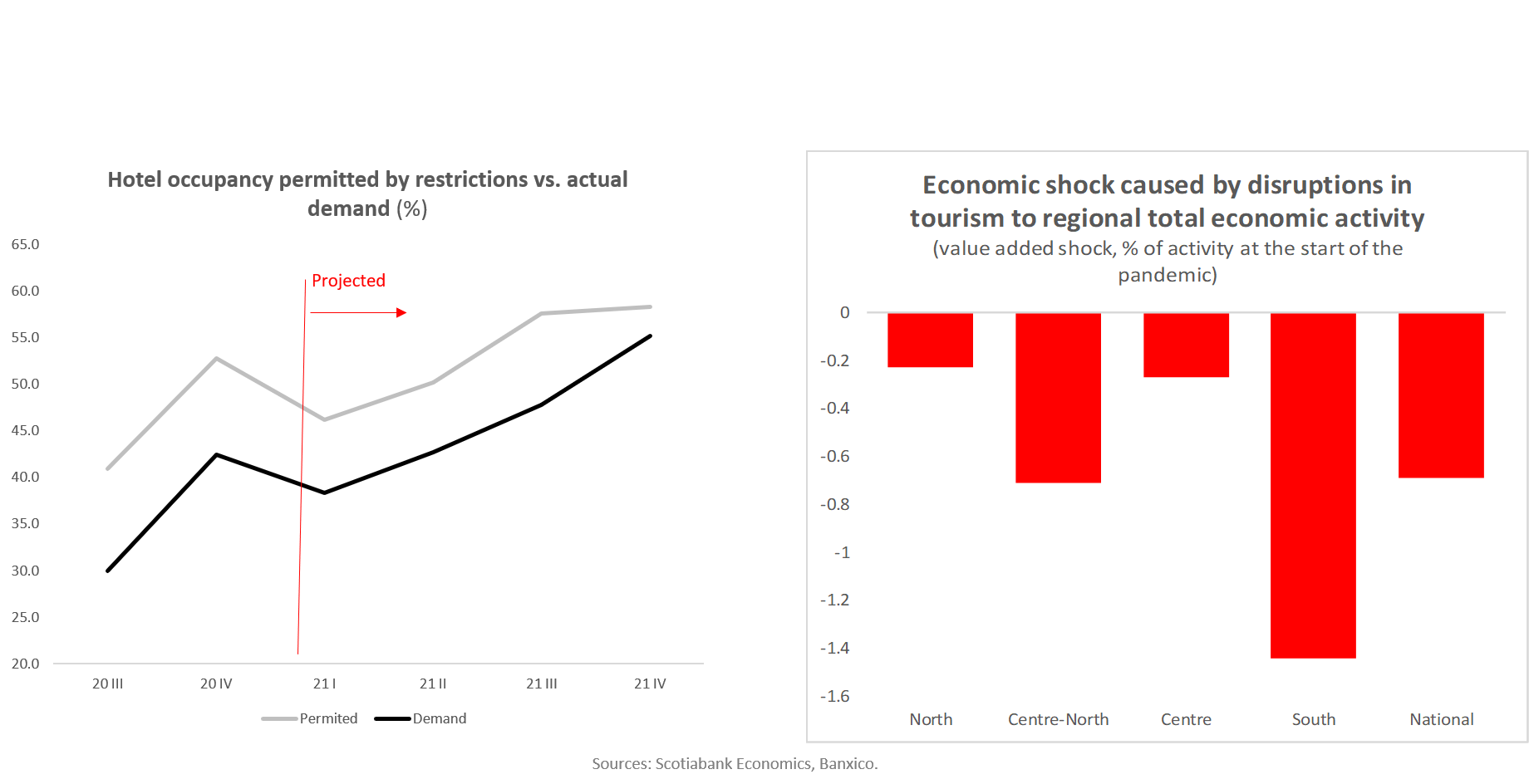

The “K-shaped” recovery story has legs, weakness in tourism & construction

Shock caused by tourism decline hit regions unevenly

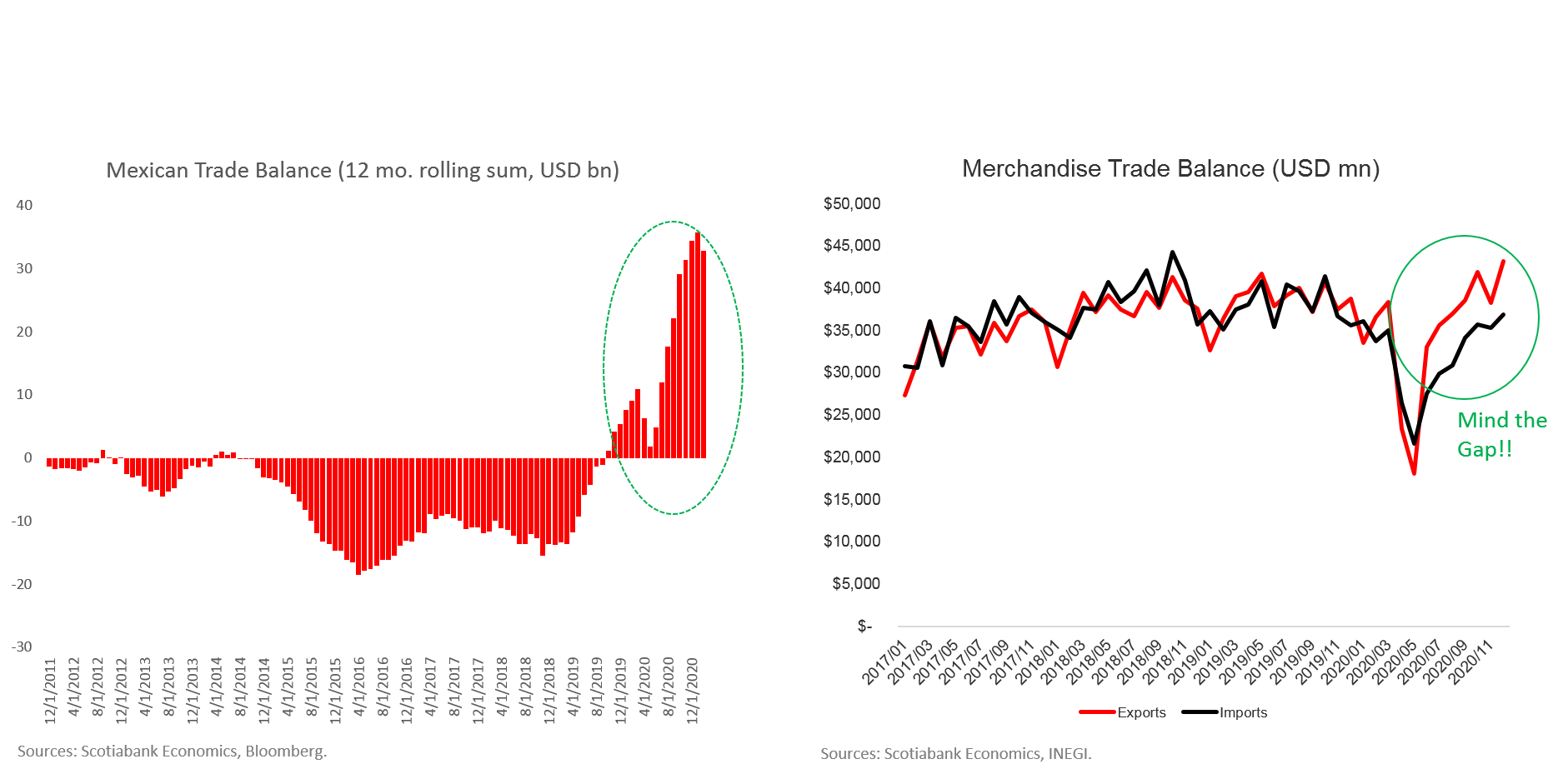

Net exports boosting growth, partly due to demand recovery lag

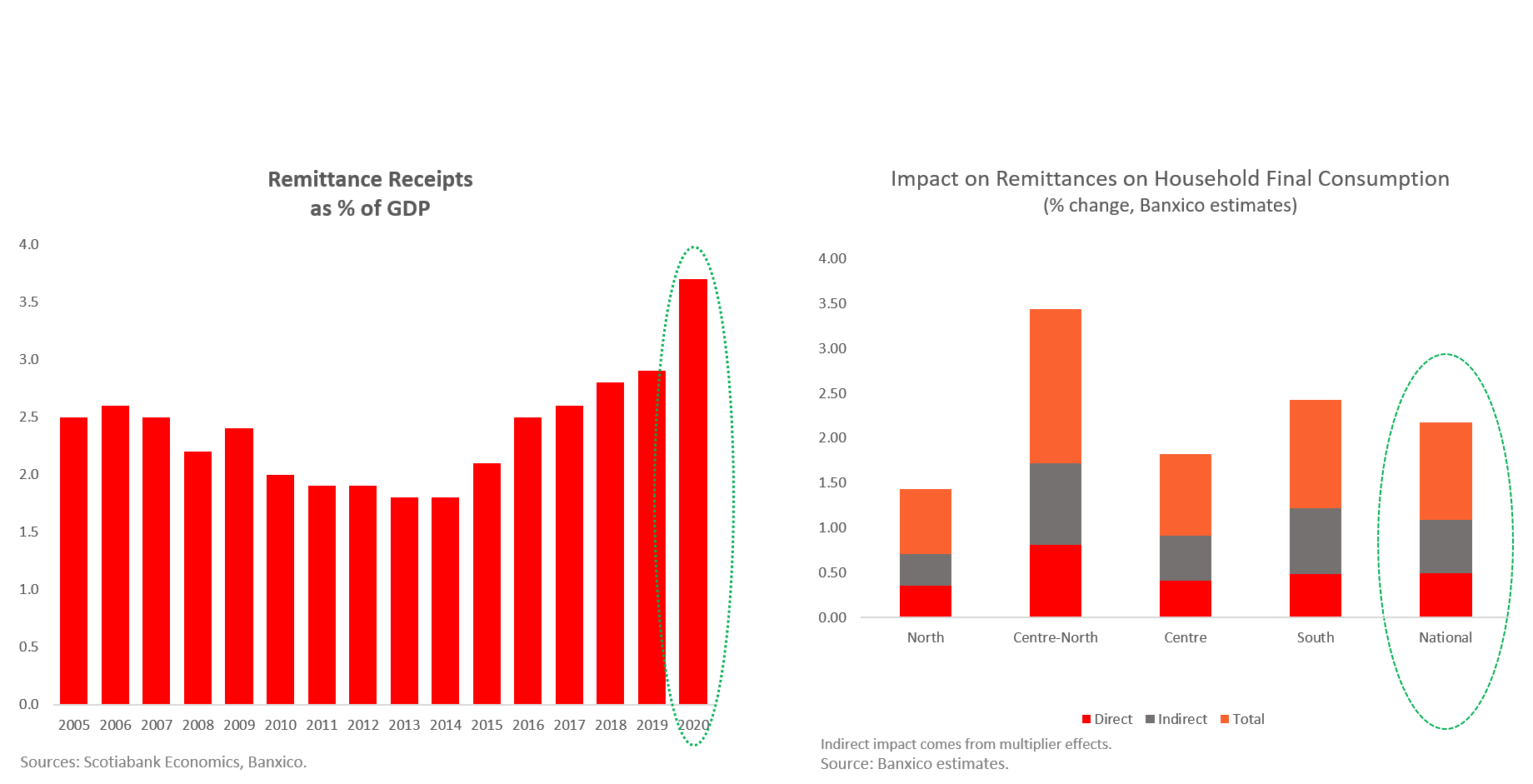

Remittances providing important boost to consumption

Pre AMLO, Mexico already had weak growth

Current Account = Savings – Investment ….

Investment has been falling under AMLO

With low investment comes weakening employment, though reopening will help

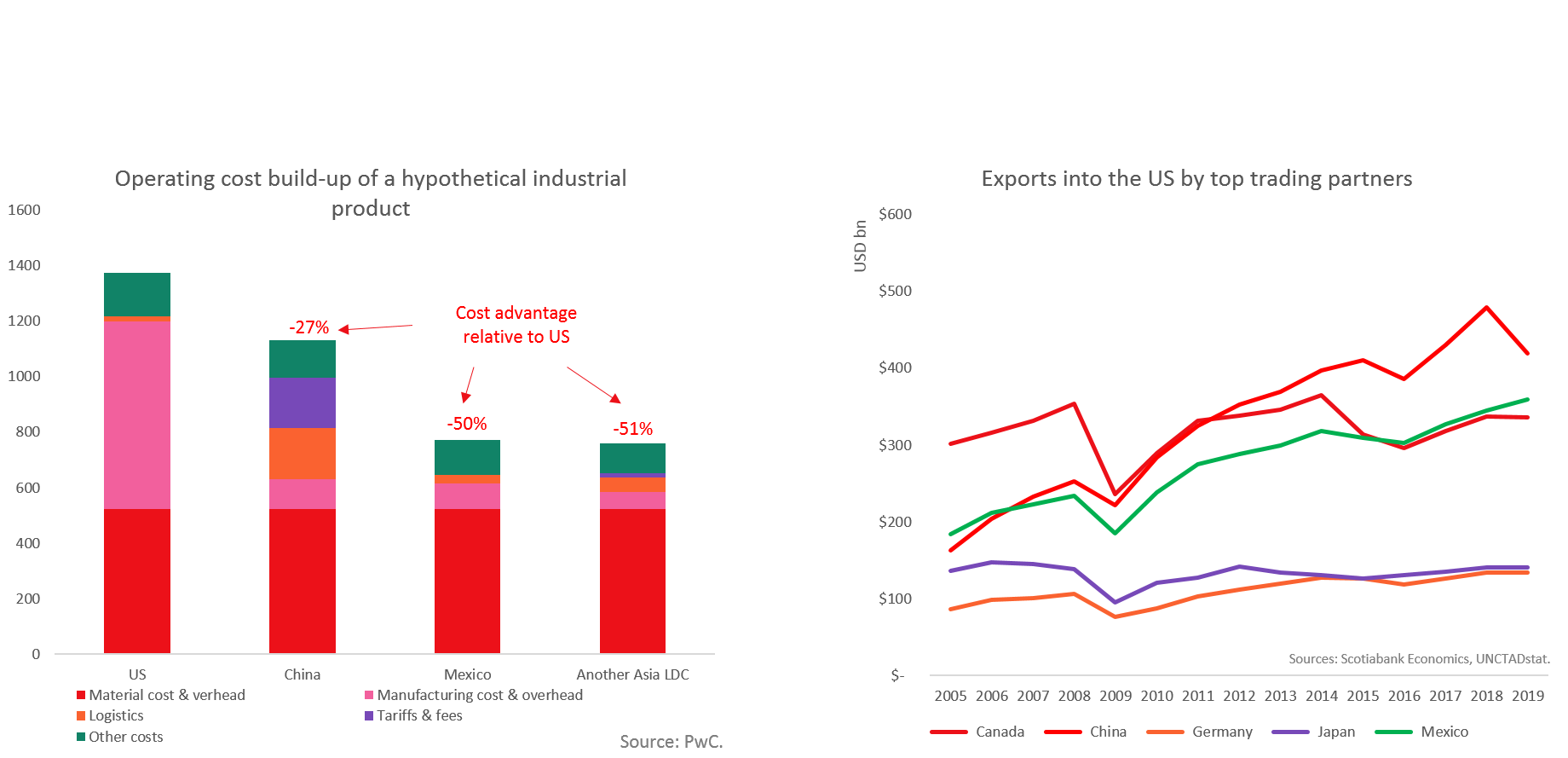

Lower costs of production still substantial advantage

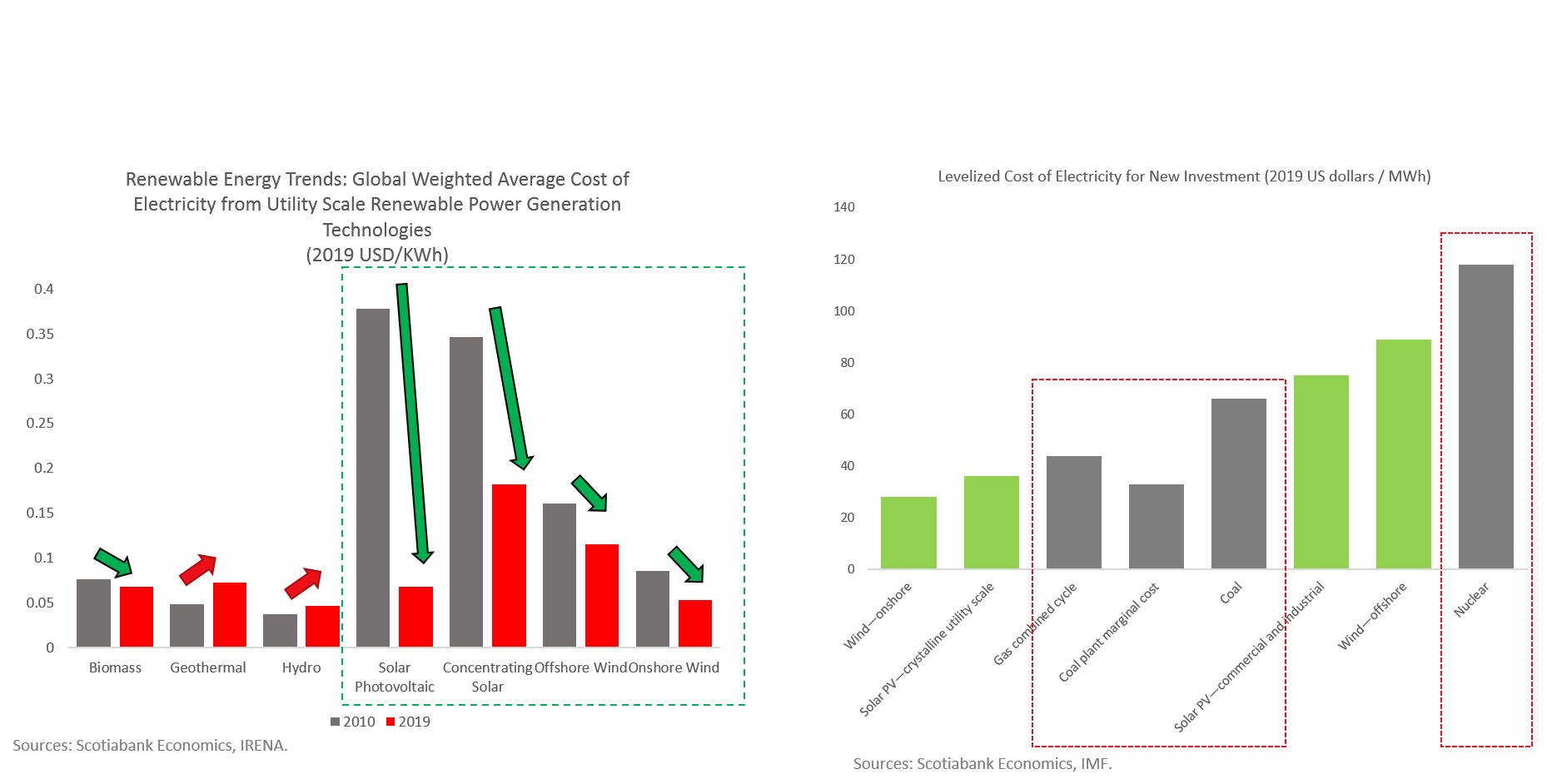

Energy reform: pushing on the wrong types of power?

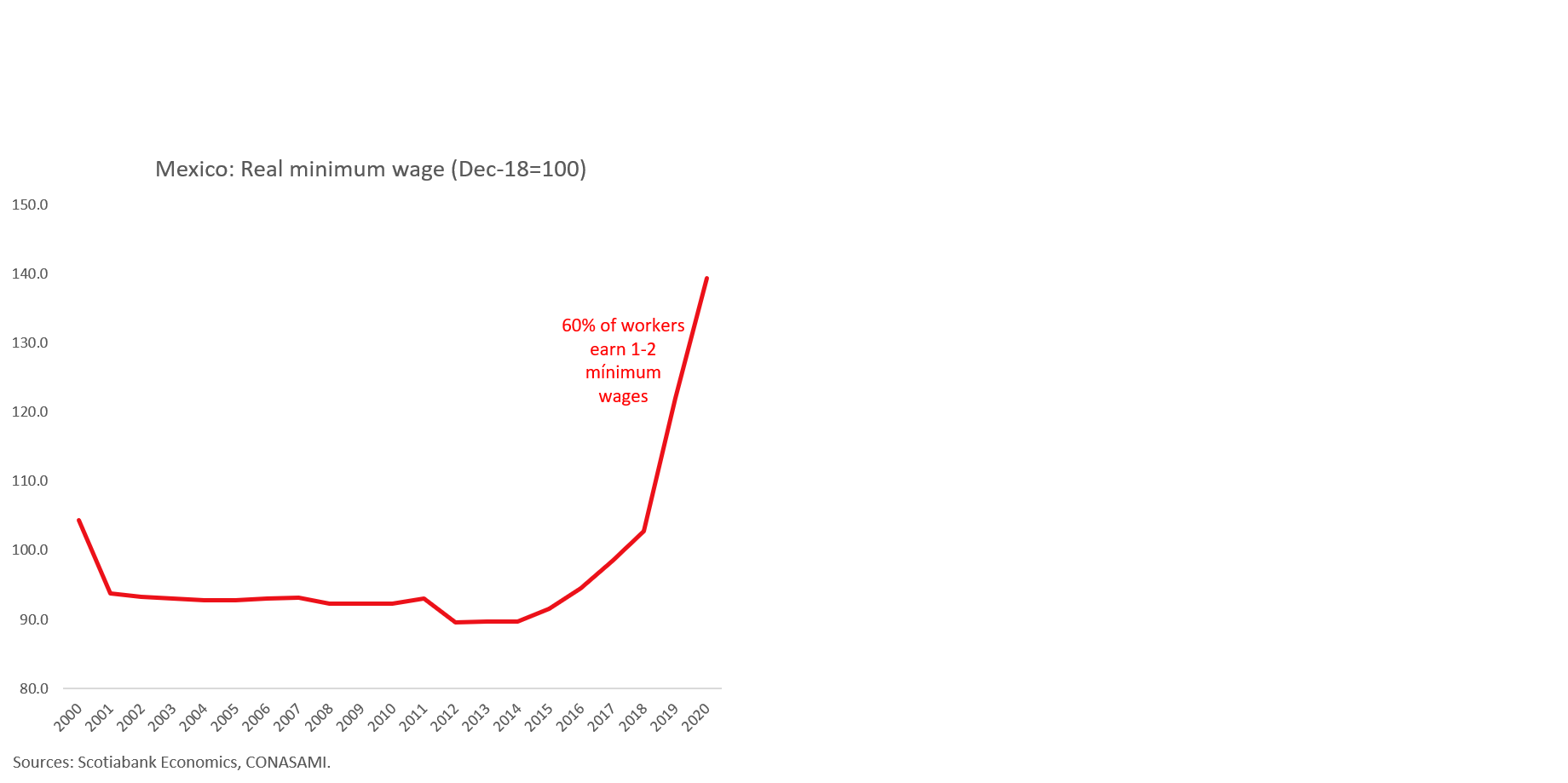

2 years of very strong minimum wage gains eroding competitive advantage

“Mexico Costs” rising:

Minimum wage hikes

Likely power shortages & cost increase

Will relying on dirty power cause “capital cost increase”?

Outsourcing Bill (up to 20% of total formal workers affected; 10-30% increase in costs)

Pension reform (gradual increase from 5.15% to 13.875% in employer contributions over 8-year span)

Tax reform the “last shock”?

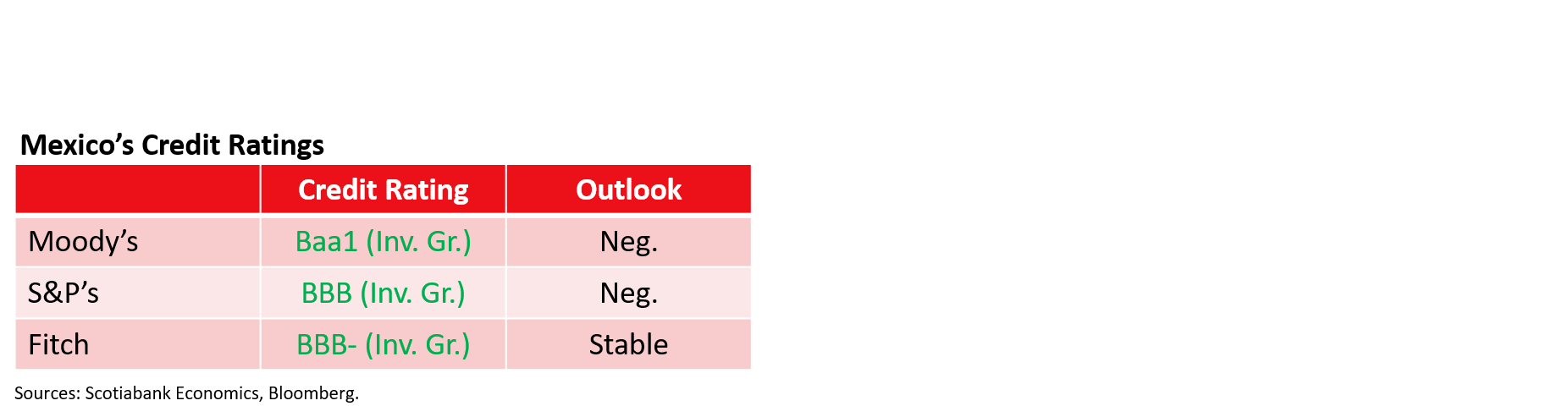

Mexico’s credit ratings & Pemex

Government has hinted a tax reform is coming for the second half of the Administration (2022 onwards), and simultaneously that tax relief for Pemex is part of it.

Topics to include in the tax reform are a subject of contention.

Mexico’s 2 main credit rating risks appear to come from:

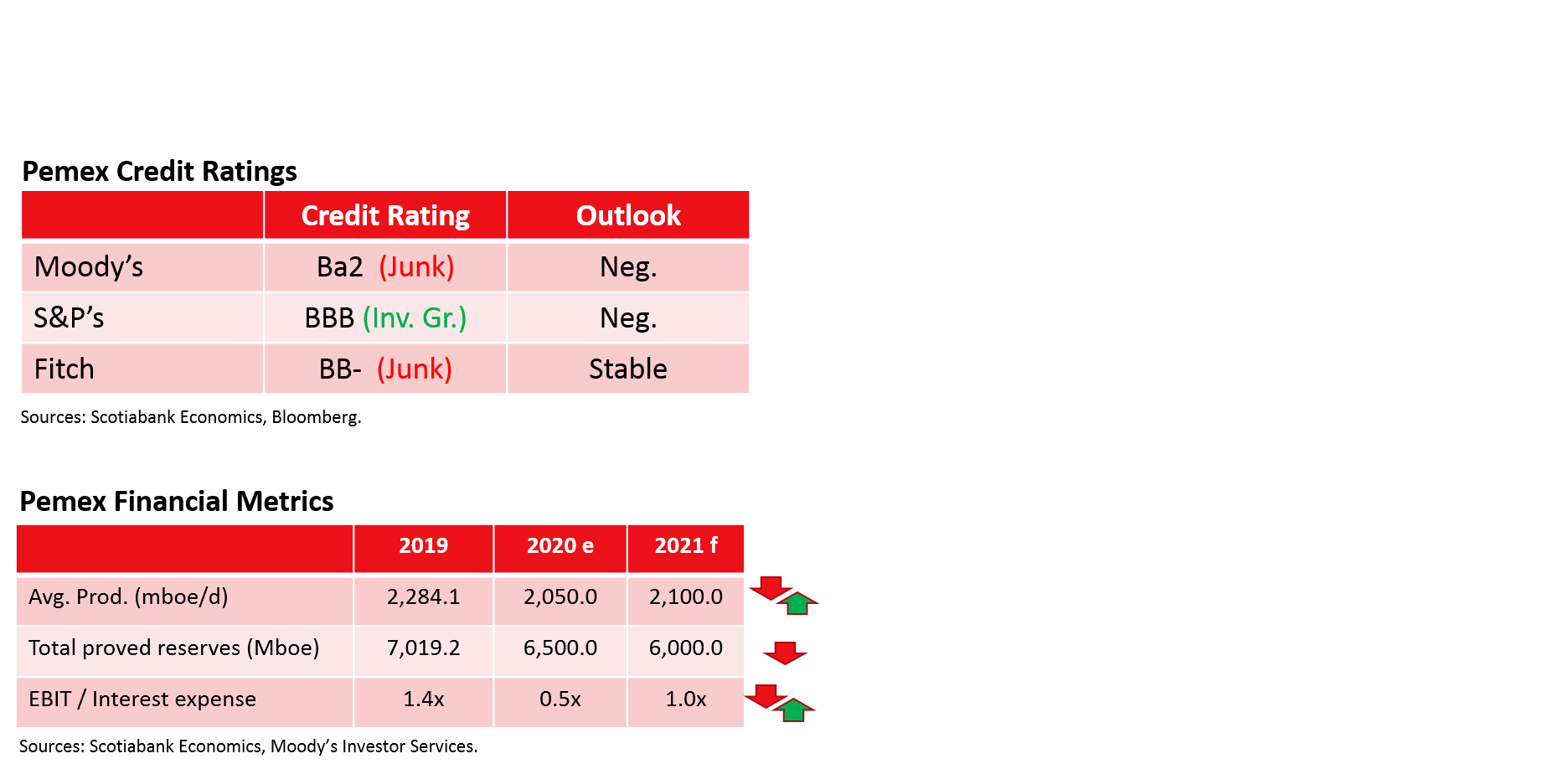

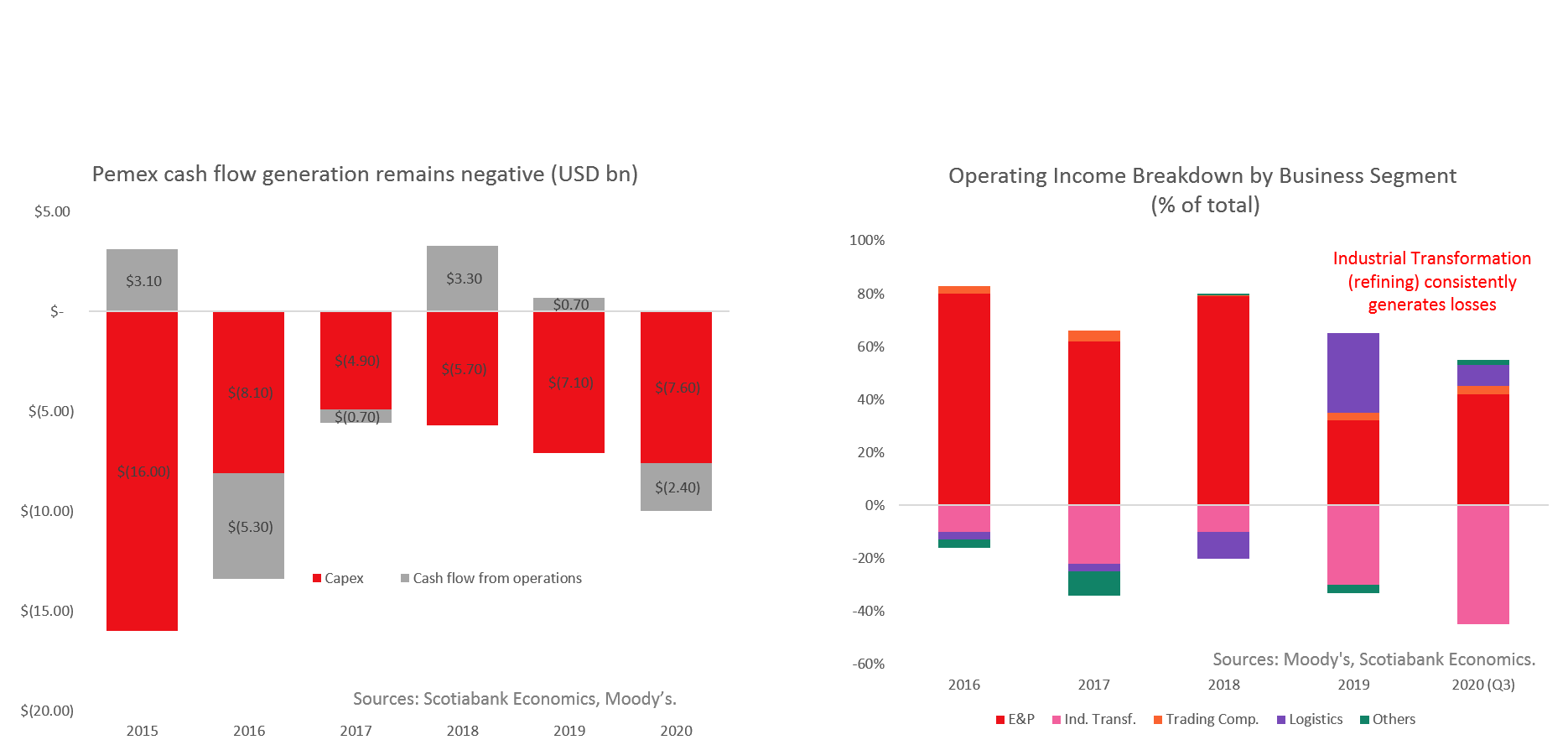

Support for Pemex, which is not only the world’s most indebted oil company, but also fails to generate positive cash flows (in part due to a very onerous tax burden).

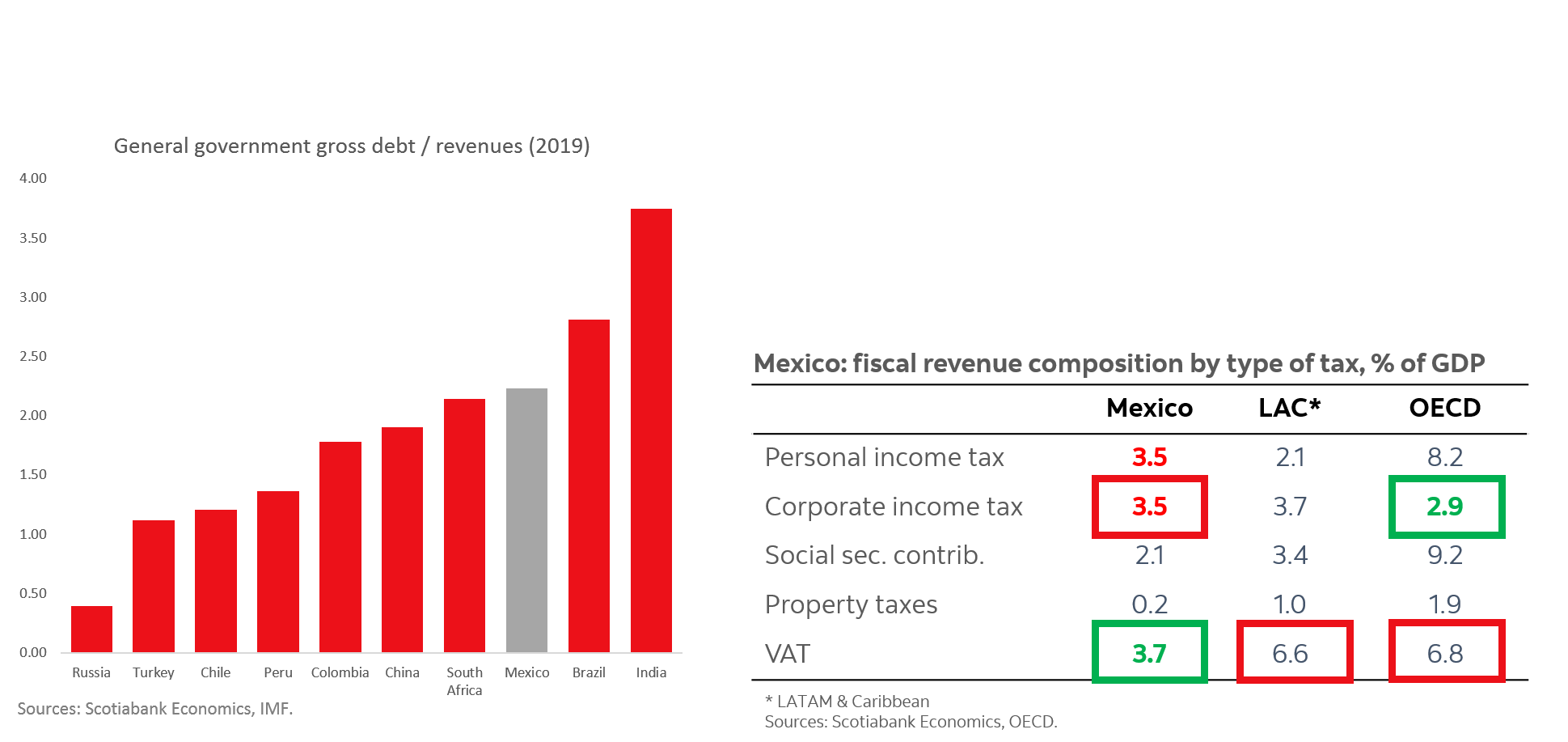

Growth. Over the past 20 years, Mexico has averaged a modest 2.1% growth, but the recent decline in investment, and with it in job creation, may have pushed potential growth even lower.

An analysis of Mexico’s long term debt sustainability suggests that to anchor debt levels, 1 of the following is needed:

Boosting growth by about 2-3 points.

Increasing the primary surplus by 2-3 points.

A fiscal reform that levies an additional 2-3 points.

A combination of the 3 points above.

Rating agencies have flagged a fiscal reform as important to securing the country’s investment grade—expected for 2022

- Fiscal reform will likely be necessary entering 2022. It is key that it’s balanced to protect private sector confidence.

Our estimates, based on the “Permanent Primary Surplus” method suggest a tax reform in the order of 2.0–3.0% of GDP will be needed—including about 1 ppt of GDP for Pemex.

Pemex overview & challenges

Challenges:

Very high debt burden.

Needed support (and/or tax relief) estimates seem to range from USD 10 bn to USD 20 bn (Scotiabank USD 14 bn).

Weak credit metrics & liquidity.

Downstream business lines consistently fail to generate positive cash flows.

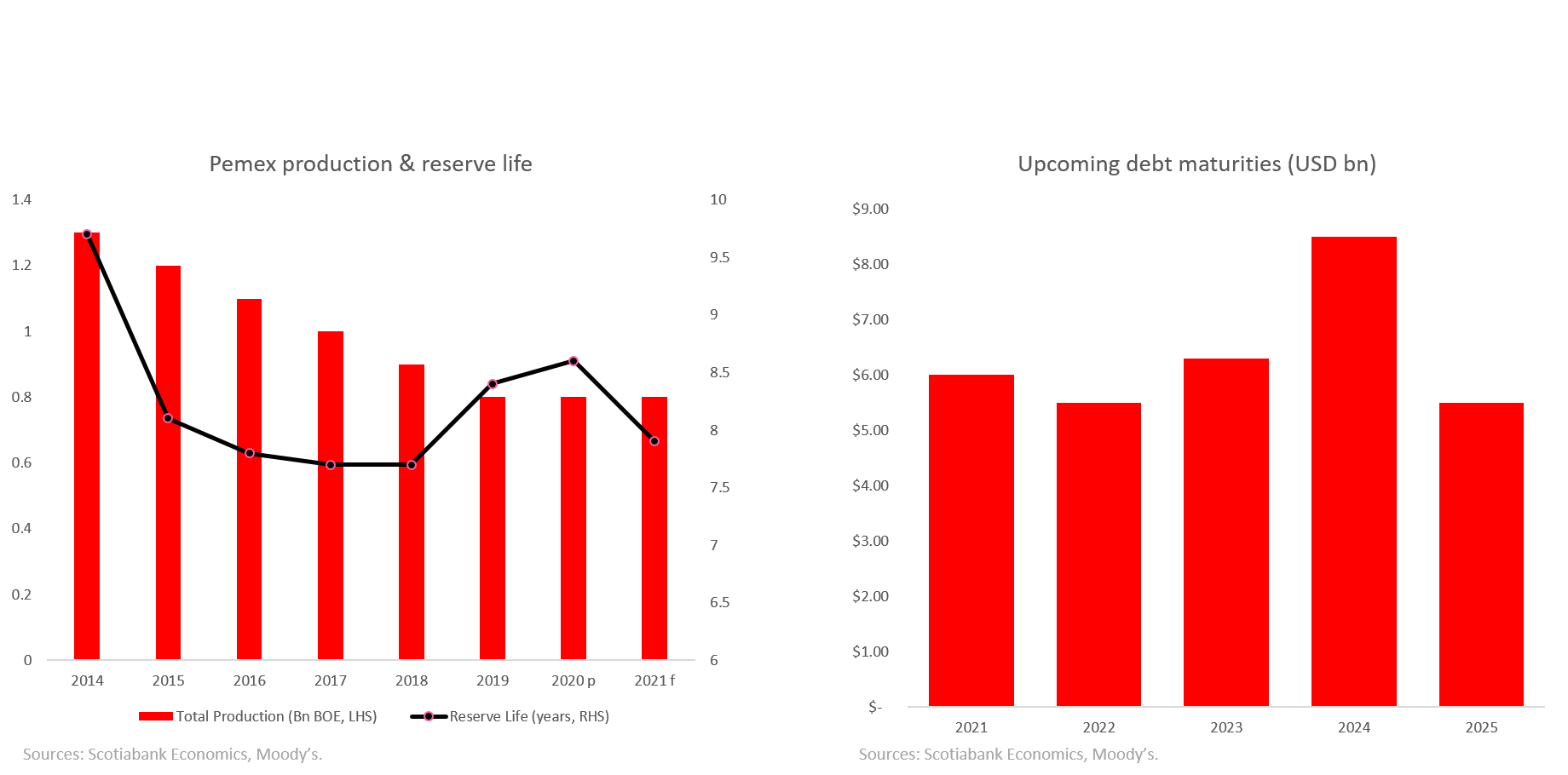

Oil output could be touching bottom, but proven reserves continue to drop, raising some concerns over long term viability.

Pemex’s challenged cash flow generation capacity

Pemex production metrics & debt maturity profile

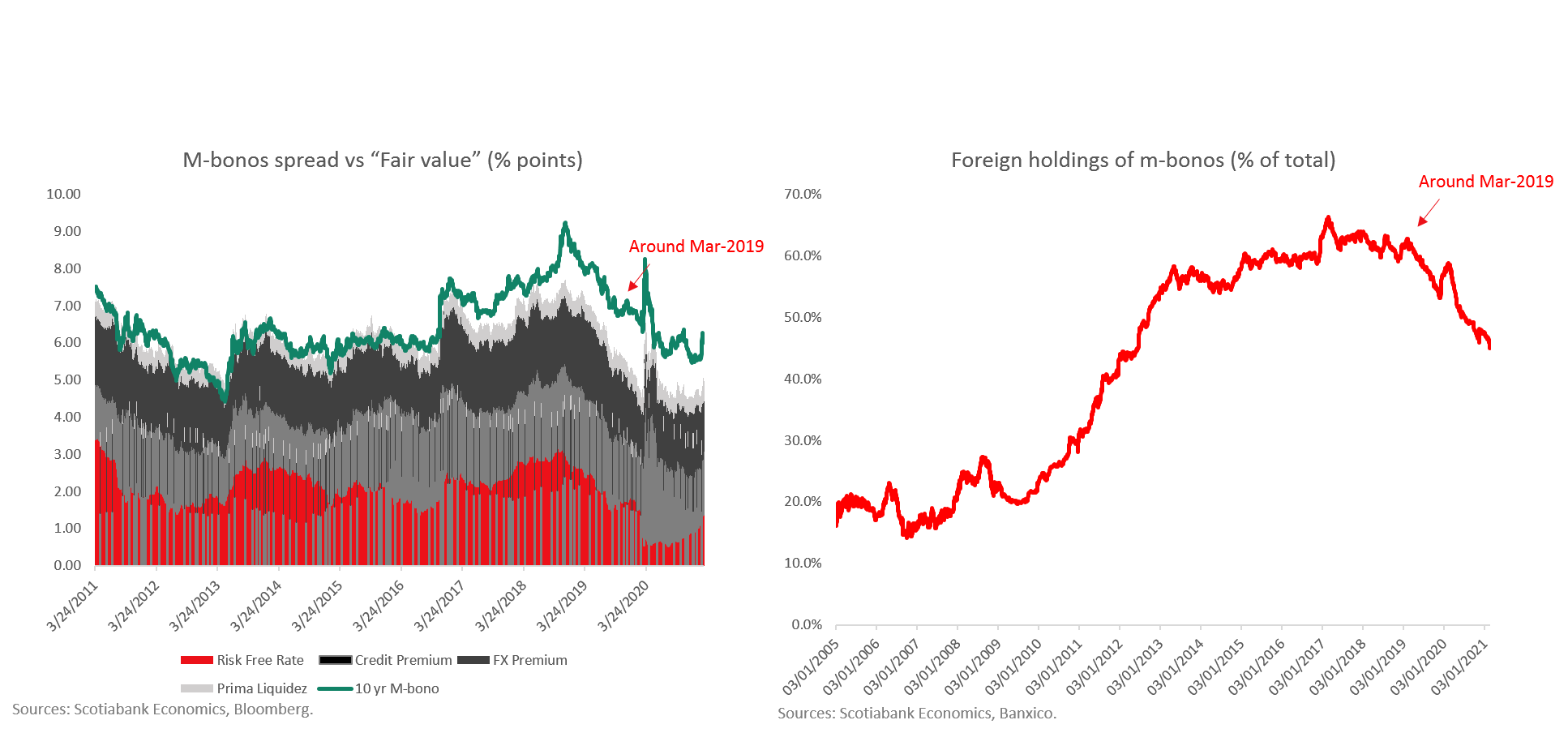

10yr M-bonos look “cheap to fair value”, but constant decline in foreign participation suggests downgrades being priced-in

AMLO approval rate rising, supporting mid-term prospects for Morena

Morena looks likely to retain at least an absolute majority, could get to a “Constitutional”/ Qualified one

DISCLAIMERS

This report is prepared by The Bank of Nova Scotia (Scotiabank) as a resource for clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness and neither the information nor the forecast shall be taken as a representation for which The Bank or its affiliates or any of their employees incur any responsibility. Neither Scotiabank or its affiliates accept any liability whatsoever for any loss arising from any use of this report or its contents. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any of the currencies referred to in this report. Scotiabank, its affiliates and/or their respective officers, directors or employees may from time to time take positions in the currencies mentioned herein as principal or agent. Directors, officers or employees of Scotiabank and its affiliates may serve as directors of corporations referred to herein. Scotiabank and/or its affiliates may have acted as financial advisor and/or underwriter for certain of the corporations mentioned herein and may have received and may receive remuneration for same. This report may include forward-looking statements about the objectives and strategies of members of Scotiabank. Such forward-looking statements are inherently subject to uncertainties beyond the control of the members of Scotiabank including but not limited to economic and financial conditions globally, regulatory development in Canada and elsewhere, technological developments and competition. The reader is cautioned that the member's actual performance could differ materially from such forward-looking statements. You should note that the manner in which you implement any of strategies set out in this report may expose you to significant risk and you should carefully consider your ability to bear such risks through consultation with your legal, accounting and other advisors. Information in this report regarding services and products of Scotiabank is applicable only in jurisdictions where such services and products may lawfully be offered for sale and is void where prohibited by law. If you access this report from outside of Canada, you are responsible for compliance with local, national and international laws. Not all products and services are available across Canada or in all countries. All Scotiabank products and services are subject to the terms of applicable agreements. This research and all information, opinions and conclusions contained in it are protected by copyright. This report may not be reproduced in whole or in part, or referred to in any manner whatsoever nor may the information, opinions and conclusions contained in it be referred to without in each case the prior express consent of Scotiabank. Scotiabank is a Canadian chartered bank. TM Trademark of The Bank of Nova Scotia. Used under license, where applicable. Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including, Scotia Capital Inc. and Scotia Capital (USA) Inc. - all members of Scotiabank.

Dodd-Frank Act Disclaimer: This material has been prepared and distributed by The Bank of Nova Scotia for informational and marketing purposes only and should not be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap. The general transaction, financial, educational and market information contained herein is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap. You need to exercise independent judgment in evaluating this material, and you should consult with your own independent financial, legal, accounting, tax and other professional advisors as to whether any swap or trading strategy involving a swap is suitable or advisable for you.

Go to www.ScotiaFX.com for FX Strategy documents covering G10, Latam, and Asia, as well as commentary from our economics department.

Copyright © 2016, Scotiabank

For enquiries, or to be removed from our FX Strategy distribution list, please contact us by e-mail at scforeignexchange@scotiabank.com.

Click here if you would like to be added to our subscription list.

Click here to view the privacy statement.

To unsubscribe from receiving further Commercial Electronic Messages click this link: https://www.unsubscribe.gbm.scotiabank.com.

™Trademark of The Bank of Nova Scotia. The Scotia Capital trademark is used in association with the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and its various subsidiaries in the countries where they operate. Scotia Capital Inc. is a member of the CIPF.

TM Marca de The Bank of Nova Scotia, utilizada bajo licencia (donde corresponda). Scotiabank, junto con “Banca y Mercados Globales” es el nombre comercial utilizado para designar las actividades de banca corporativa y de inversión global y de mercados de capitales de The Bank of Nova Scotia y algunas de sus empresas afiliadas en los países donde operan, incluyendo Scotia Capital Inc., Scotia Capital (USA) Inc., Scotiabanc Inc., Citadel Hill Advisors L.L.C., The Bank of Nova Scotia Trust Company of New York, Scotiabank Europe plc, Scotiabank (Ireland) Limited, Scotiabank Inverlat S.A., Institución de Banca Múltiple, Scotia Inverlat Casa de Bolsa S.A. de C.V., Scotia Inverlat Derivados S.A. de C.V., que son todas miembros del grupo Scotiabank y usuarios autorizados de la marca. The Bank of Nova Scotia es una institución constituida en Canadá con responsabilidad limitada. Scotia Capital Inc. es miembro del Canadian Investor Protection Fund (Fondo Canadiense de Protección a Inversionistas). Scotia Capital (USA) Inc. es corredor y agente registrado ante la SEC (Comisión de Bolsa y Valores) y miembro de la FINRA, de la Bolsa de Valores de Nueva York (NYSE) y de la NFA. The Bank of Nova Scotia está autorizado y reglamentado por la Oficina del Superintendente de Instituciones Financieras de Canadá. The Bank of Nova Scotia cuenta con la autorización de la Autoridad de Regulación Prudencial del Reino Unido y está sujeto a la reglamentación de la Autoridad de Conducta Financiera y a las limitaciones de la Autoridad de Regulación Prudencial del Reino Unido. Los detalles sobre el alcance de la reglamentación de The Bank of Nova Scotia por parte de la Autoridad de Regulación Prudencial del Reino Unido están disponibles previa solicitud. Scotia Capital Inc. está reglamentado por la Investment Industry Regulatory Organization of Canada (Organización para la Reglamentación del Sector de Inversiones de Canadá) y autorizado y reglamentado por la Autoridad de Conducta Financiera. Scotiabank Europe plc cuenta con la autorización de la Autoridad de Regulación Prudencial del Reino Unido y está reglamentado por la Autoridad de Conducta Financiera y la Autoridad de Regulación Prudencial del Reino Unido. Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V., y Scotia Inverlat Derivados, S.A. de C.V. están autorizados y reglamentados por las autoridades financieras mexicanas. Es posible que los productos y servicios aquí mencionados no estén disponibles en todas las jurisdicciones y sean ofrecidos por entidades jurídicas diferentes, que tienen autorización de usar la marca Scotiabank.

La marca ScotiaMocatta se usa en asociación con las actividades de The Bank of Nova Scotia relacionadas con metales base y preciosos.

La marca Scotia Waterous se usa en asociación con las actividades de asesoría sobre fusiones y adquisiciones de empresas del sector de petróleo y gas que lleva a cabo The Bank of Nova Scotia y algunas de sus subsidiarias, como Scotia Waterous Inc., Scotia Waterous (USA) Inc., Scotia Waterous (UK) Limited y Scotia Capital Inc., todos miembros del grupo Scotiabank y usuarios autorizados de la marca.

Scotia Capital Inc. posee y controla una participación accionaria en TMX Group Limited (TMX) y tiene un director fiduciario dentro de la junta directiva. Como tal, Scotia Capital Inc. podría tener un interés económico en la cotización de acciones en un mercado bursátil que sea propiedad u operado por TMX, incluyendo la Bolsa de Valores de Toronto, el Segmento de Capital de Riesgo de la Bolsa de Valores de Toronto y la Bolsa de Valores Alpha, cada una como Bolsa de Valores independiente. Ninguna persona o empresa tendrá la obligación de adquirir productos o servicios de TMX o de sus afiliados como condición para que Scotia Capital Inc. proporcione o continúe proporcionando un producto o servicio. Scotia Capital Inc. no exige que los emisores de acciones o que los accionistas que pretendan vender acciones coticen en alguna de las Bolsas como condición para que suscriba o continúe suscribiendo o que proporcione o continúe proporcionando un servicio.