Key Takeaways

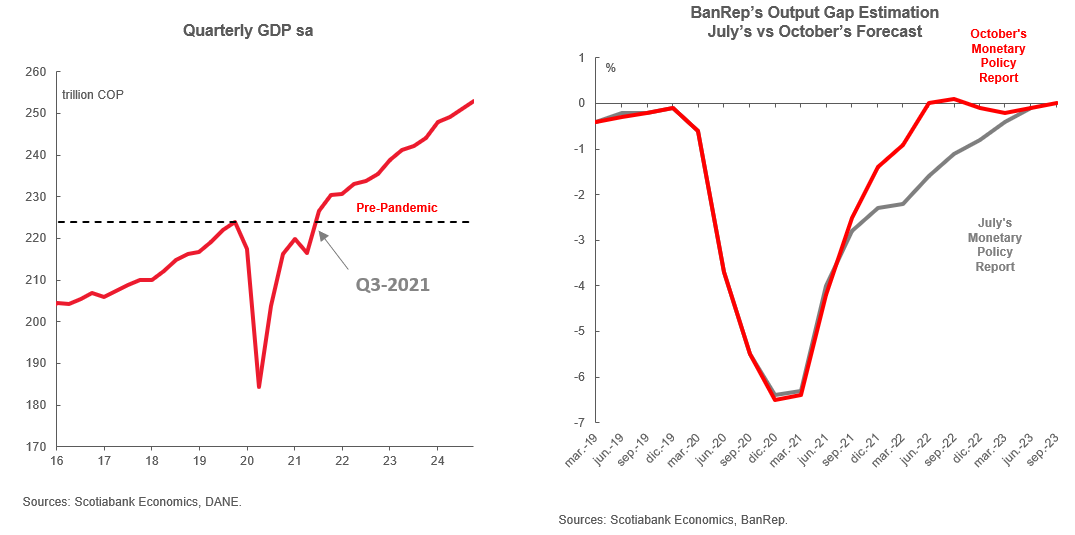

- The economy is reaching pre-pandemic levels of activity sooner than expected as the government lifts restrictions and its vaccination plan advances. The central bank expects the output gap to close by mid-2022.

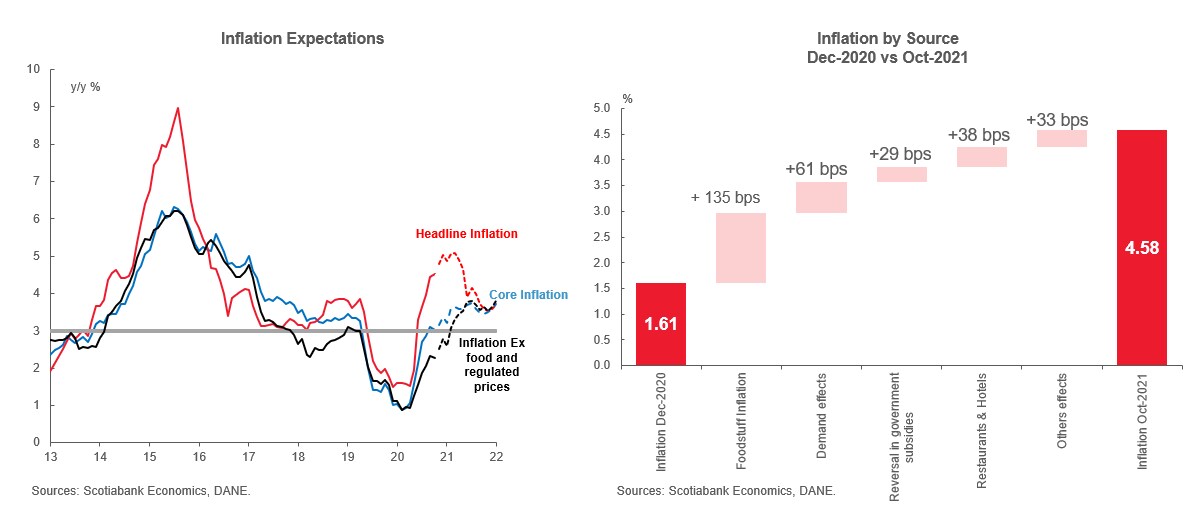

- Inflation should close 2021 around 5% y/y and indexation effects would extend the current temporary shock. In 2022, inflation is expected to end the year at ~3.7% y/y.

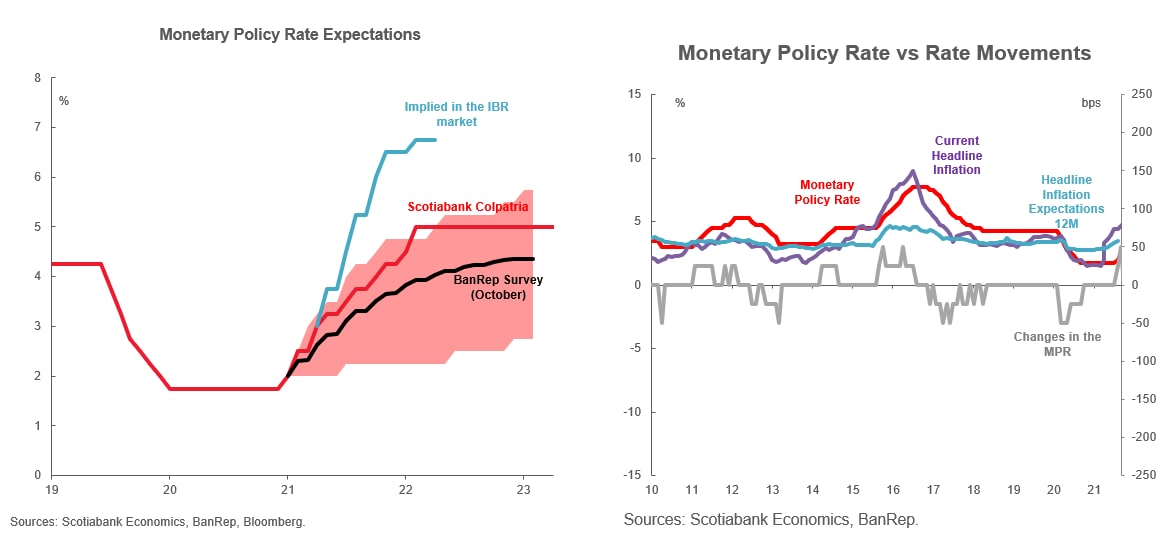

- The central bank has started its hiking cycle. The hawkish side of the BanRep Board has said that the hiking cycle should be faster at the beginning to avoid a more contractionary stance in the future. We expect BanRep to reach the nominal neutral rate of 5% by December 2022.

- Despite positive macroeconomic news and a better fiscal outlook, local asset prices remain volatile. Election campaigns could put further pressure on local markets in 2022.

In Q3-2021, Colombia probably reached pre-pandemic production levels. BanRep expects the output gap to be closed by mid-2022.

Despite supply shocks being temporary, indexation should extend CPI inflation. Reversion in headline inflation should start in the H2-2022, while core inflation should remain within the target range.

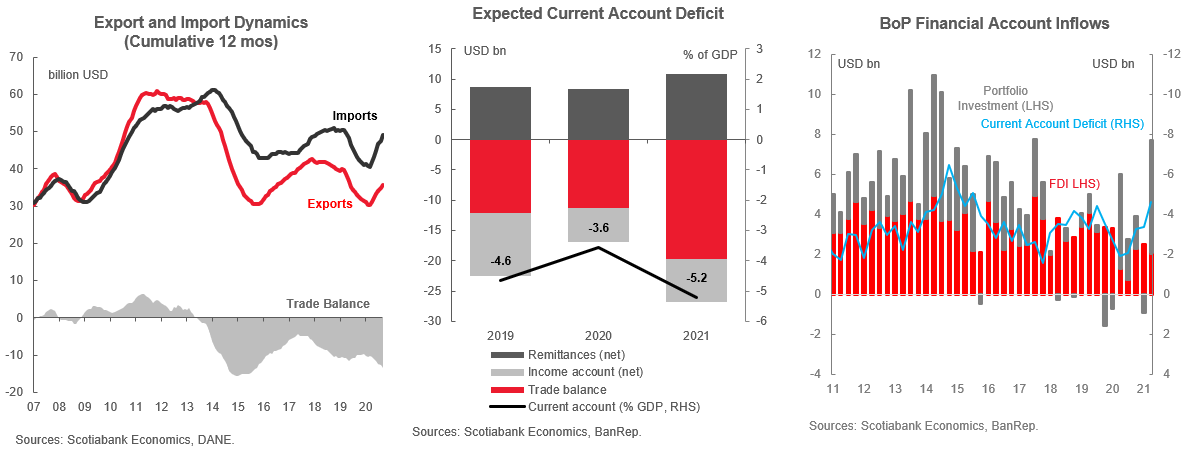

Economic recovery and the asymmetric impact of international prices for exports and imports are together widening the current account deficit. Financing is still sufficient, but FDI recovery is crucial.

The central bank has started a more aggressive-than-normal hiking cycle and the neutral rate should be reached in 2022. The IBR market is pricing an even higher terminal rate that would be achieved sooner.

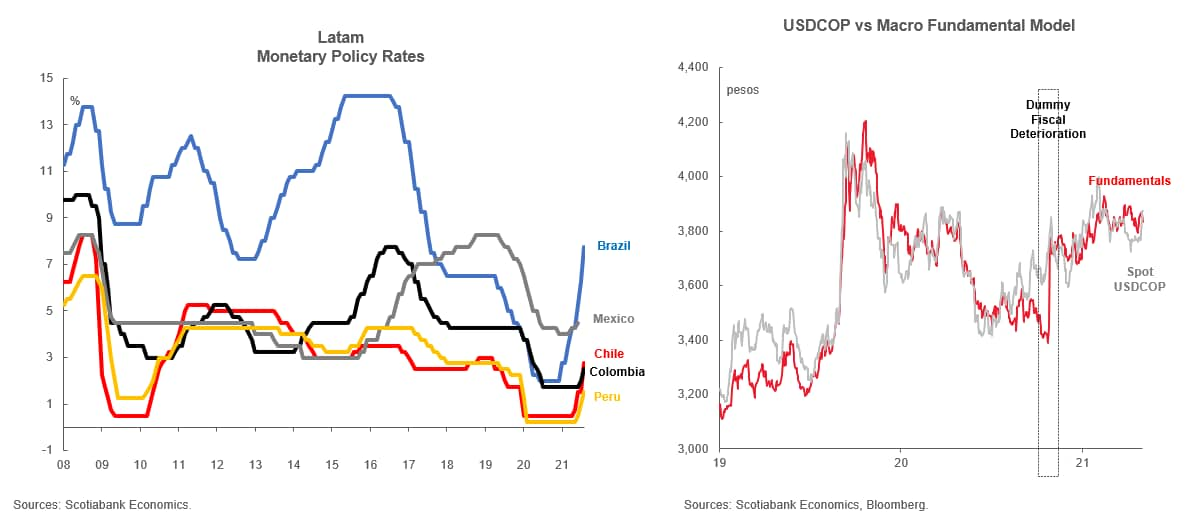

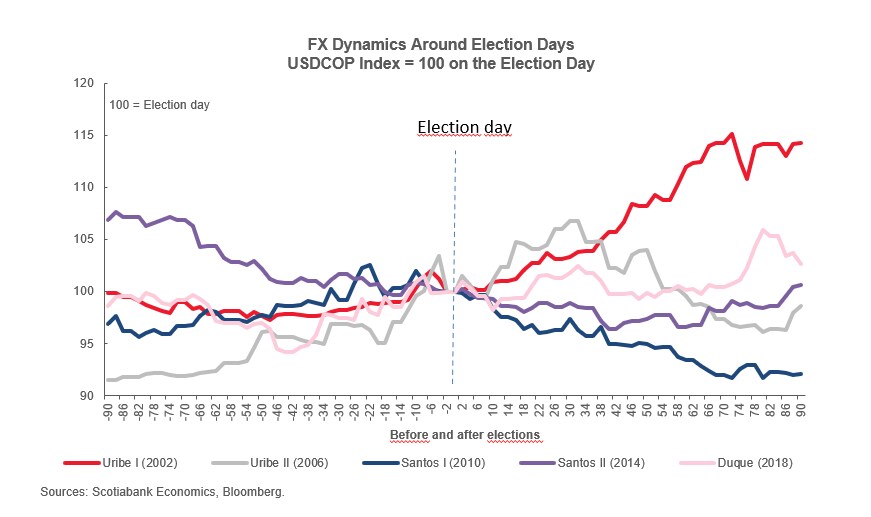

Divergences in monetary policy cycles and the electoral calendar could keep the COP under pressure.

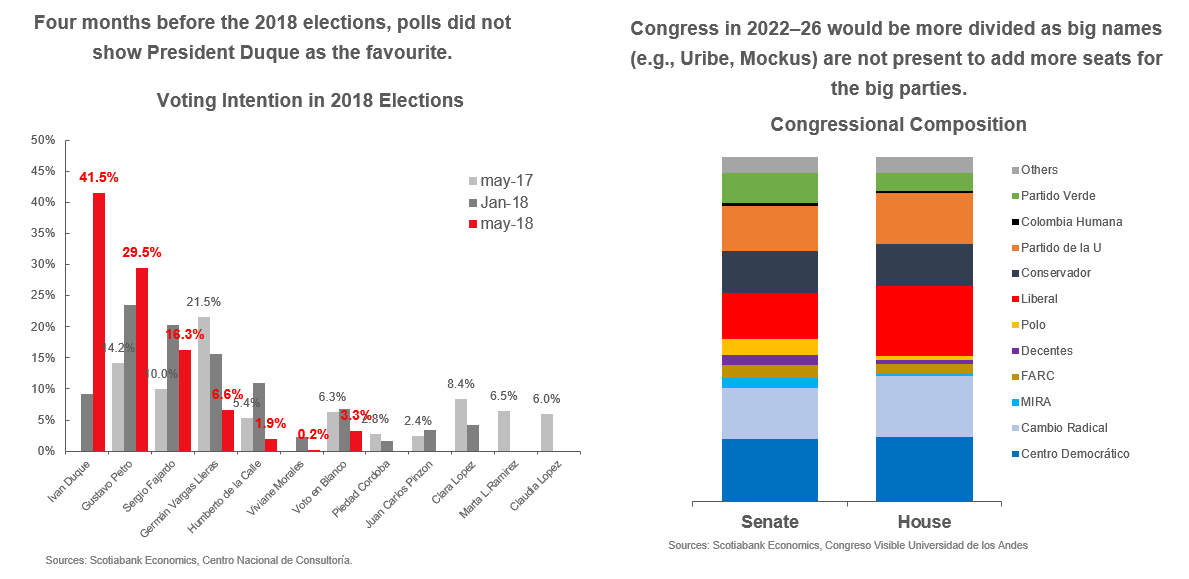

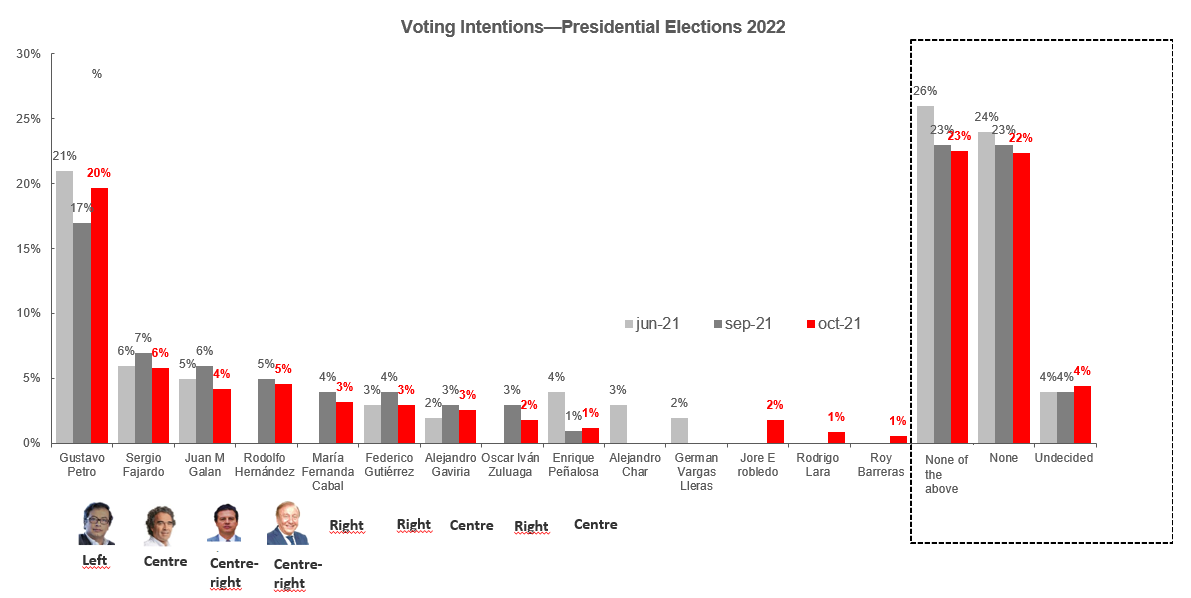

The main phase of the presidential election starts early in 2022. The Congressional elections are the first milestone.

Currently, there are 42 potential presidential candidates. The undecided population leads the polls.

Elections don’t have a certain effect on the exchange rate.

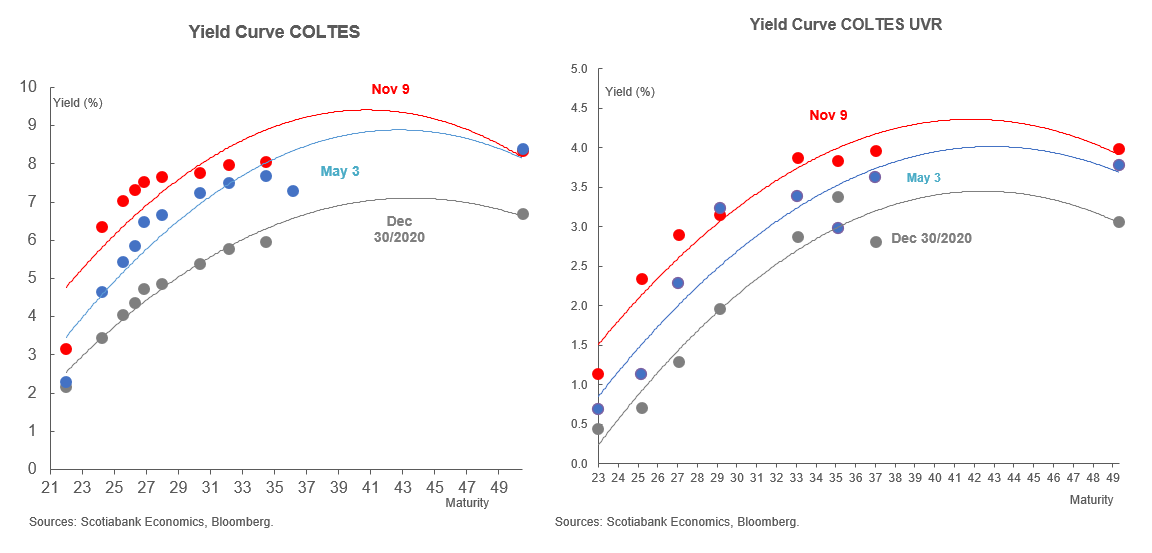

After the shock due to fiscal uncertainty, the long end of the curve has been relatively affected by the local and external environment. Monetary policy is driving movements in the short end and the belly of the curve.

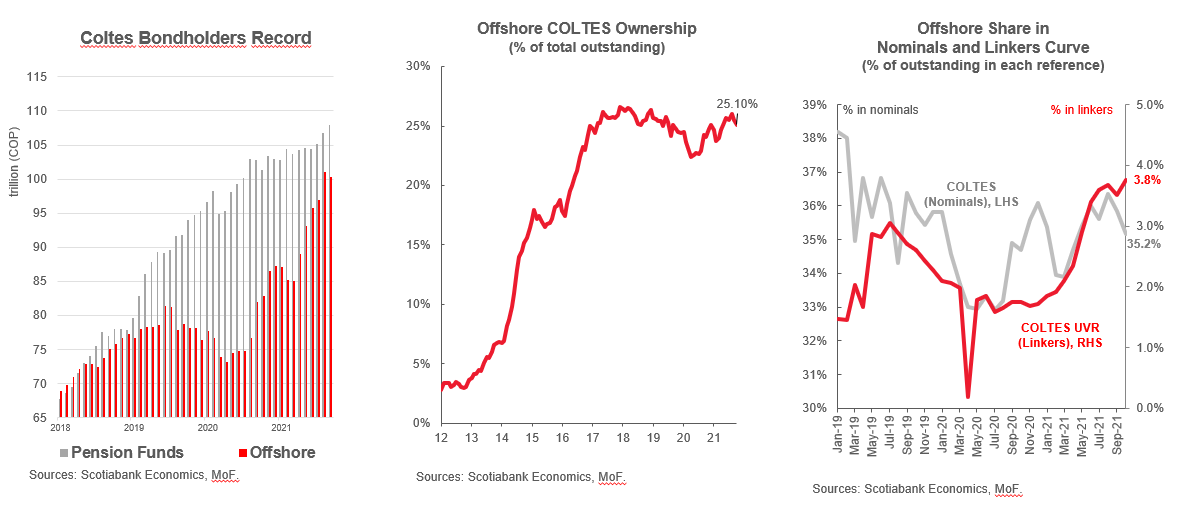

In YTD terms, offshore investors remain the main buyers of COLTES. Positioning on the long end of the linkers curve is gaining momentum.

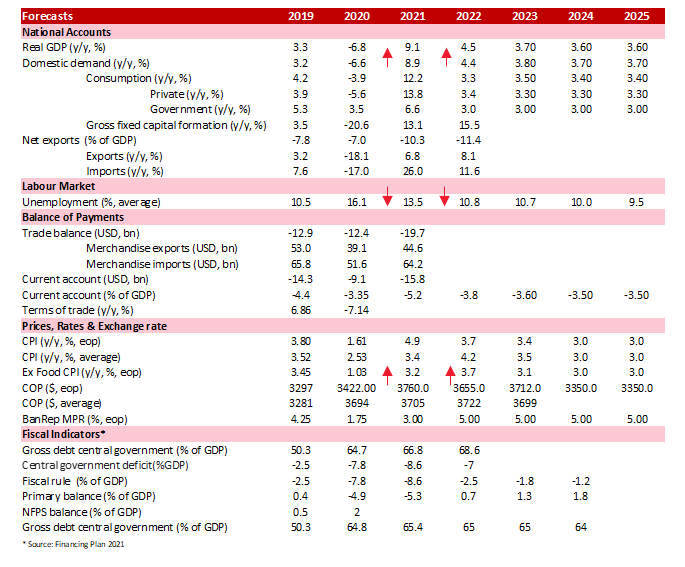

Macroeconomic Forecasts

Este informe ha sido preparado por Scotiabank Colpatria S.A. establecimiento bancario. Las opiniones, estimados y proyecciones contenidas, corresponden a la fecha de divulgación y se encuentran sujetos a cambios sin previo aviso, pues atienden al comportamiento de la economía y el entorno. Los datos expuestos en el documento provienen de fuentes públicas consideradas fidedignas, sin embargo Scotiabank Colpatria S.A. no se hace responsable de su veracidad ni de la interpretación que de los mismos se haga. Este documento no es ni pretende brindar asesoría de inversión; la información, herramientas y material contenido en el texto, son proporcionados meramente con fines informativos y no deben ser utilizados ni entendidos como una oferta, consejo, asesoría o recomendación de inversión ni para comprar, vender o emitir valores y/o cualquier otro instrumento financiero, ni para realizar cualquier otro tipo de transacción financiera. El contenido de la presente comunicación o mensaje no constituye una recomendación profesional para realizar inversiones en los términos del artículo 2.40.1.1.2 del Decreto 2555 de 2010 o las normas que lo modifiquen, sustituyan o complementen.

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.