- The ECB followed through on its long-communicated guidance with a 50bps hike today, but accompanied this with very limited signaling regarding the future policy path, against a backdrop of financial stability concerns.

- For now, if markets and the economy get past current turbulence somewhat successfully, the ECB looks set to hike 25bps at its next meeting (and likely the one after that) with a chance it shifts to a faster QT in the second half of 2023.

- Lagarde said that if their baseline persists, then the ECB will still have “a lot more ground to cover”—with the caveat of higher uncertainty in this baseline. The baseline persisting should provide solid support to the EUR and EGB yields , but it may be too early to call.

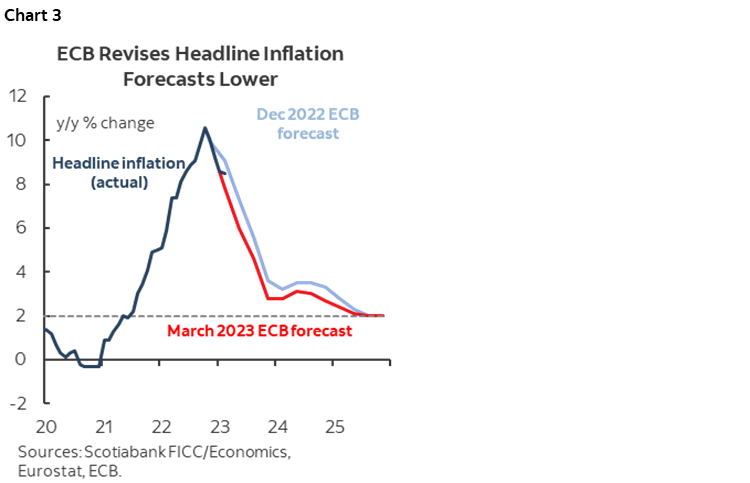

The ECB followed through on its long-communicated guidance with a 50bps hike today, but accompanied this with very limited signaling regarding the future policy path, against a backdrop of financial stability concerns. Had this meeting taken place just one week ago, the bank may have sounded a more hawkish note given today’s revision higher to its core inflation and GDP growth forecasts (table 1).

With the statement and Lagarde’s presser giving us little to go on in terms of what to expect at the May decision, we leave our forecast unchanged, seeing a 25bps hike at the May meeting.

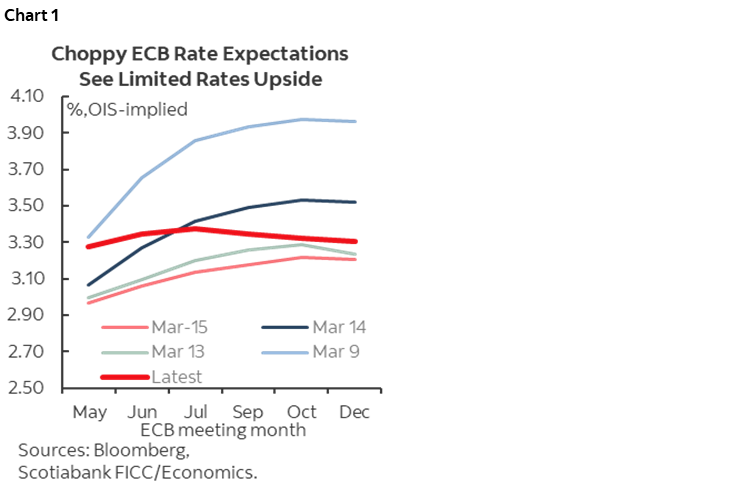

The EUR initially rallied slightly alongside a jump in European yields given the 34bps priced in ahead of the announcement (i.e. a higher chance of a 25bps increase, chart 1 for recent moves). But, the half-point hike seemingly soured the global mood in markets that had even braced for a 25bps move after a ‘dovish’ leak to Bloomberg: de Guindos noting on Tuesday, behind closed doors, that some EU banks may be vulnerable to higher rates. Markets have recovered over the past hour or so (SPX is 1% higher on the day), thanks to reports that large US banks are in talks to support First Republic.

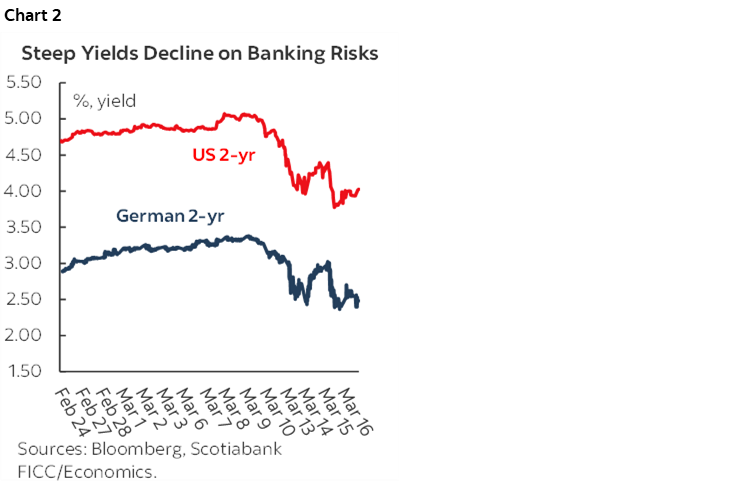

Still, the 15bps or so range in German 2-yr yields since the leak and around and following the statement is relatively narrow when compared to recent market action (chart 2). From the shortly-lived peak on the announcement, the 2yr fell as much as 15bps before a drive higher from US yields on bank news helped them higher to sit at their highest point since before the de Guindos story—at about 2.55% at writing. The spread between German and US 2yr yields has widened by about 20bps since Lagarde finished her presser, however, as European banking risks seem to outweigh those in the US. At writing, the EUR is roughly unchanged on the day just around 1.06 after falling as low as 1.0551 about two hours ago.

It may simply be that case that the EUR and EGBs will remain bound by the evolving situation around Europe’s financial sector (and the US) and it will become clear what the next ECB step will be in due time. For now, if markets and the economy get past current turbulence somewhat successfully, the ECB looks set to hike 25bps at its next meeting (and likely the one after that) with a chance it shifts to a faster QT in the second half of 2023. The fact that hikes look relatively underpriced in markets (chart 1) should be supportive for the EUR as (if) things normalize.

According to Lagarde, the 50bps hike was the only option presented and a “very large majority” backed this choice, with “three or four” preferring to wait to see how the situation unfolds (though not opposing in “in principle”). That looks like strong enough support for today’s hike all things considered.

The complete set of communications seems like a fair compromise given elevated uncertainty; the ECB didn’t give too much away, understandably. The bank has given itself optionality and time to respond to data and see how the situation shakes out, while not feeding the panic in markets with a dovish message or evidence of alarm among the Governing Council. Sticking to the hike that they had teed up is also less of a surprise and allows them to press on with the inflation fight on the hope that the situation resolves itself without too much impact on lending (and thus the economy). Do note that the lower headline inflation forecast (table 1 and chart 3), which sees it steeply falling over the next few months, could act to check the bank’s hawkishness.

The statement, as well as Lagarde and de Guindos at the presser, highlighted the resilience of the banking sector. The ECB has is now clearly in a wait-and-see stance regarding financial risks, but the statement now includes an important mention that the ECB “is fully equipped to provide liquidity support to the euro area financial system if needed and to preserve the smooth transmission of monetary policy.” This may implicitly suggest that the bank will put out fires in banking with its facilities while it continues to hike in line with its inflation goal—particularly its expectation of higher core inflation this year. Lagarde also said that if their baseline persists, then the ECB will still have “a lot more ground to cover”—with the caveat of higher uncertainty in this baseline.

Though the Eurozone economy looks fairly detached from the failure of banks in the US—caused mainly by idiosyncratic rather than systemic challenges—the ECB does not yet have enough information on the possible repercussions of the events in the past few days relating to Credit Suisse to confidently tee up it s next move. Even prior to the recent troubles in the financial sector, the ECB had reason to stick a data dependent approach with inflation on a decelerating path and a falling inflation expectations.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.